Article contents

Yes! You can be taxed on the State Pension just like any other type of income. You have to pay tax if you earn over £12,570 per year, which is known as your Personal Allowance. If you earn more than this, including your State Pension, you’ll need to pay tax.

Get £50 added to your pension.

Visit PensionBee¹Capital at risk.

Are you getting close to being able to claim your State Pension? Or just being super organised and planning in advance for retirement? Get you!

Either way, you’re probably wondering whether or not you have to pay tax on your State Pension. Sadly, your State Pension is taxable (meaning it can be taxed), but whether you actually have to pay tax on it will depend on what other income you have alongside it. Don’t worry, we’ll explain it all here.

First the bad news. The State Pension is taxable. However, there’s also good news. That doesn’t necessarily mean you have to pay tax on it.

Confused? Let us explain.

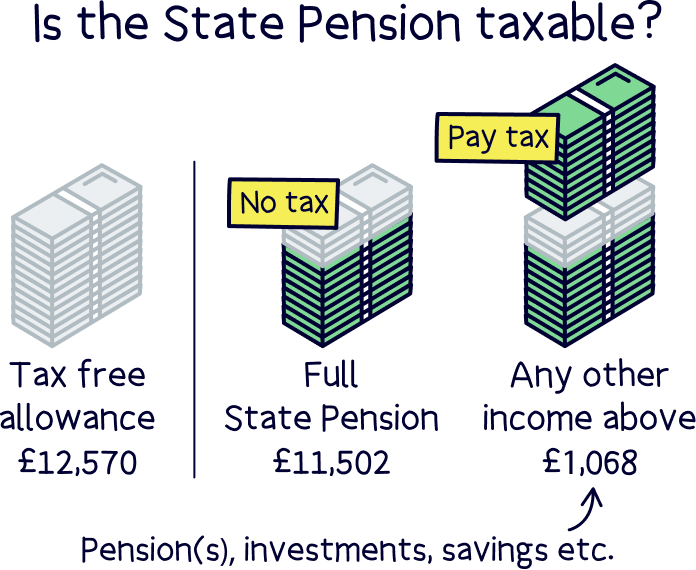

In the UK, you can earn a certain amount of money each year without having to pay tax. This is known as your Personal Allowance. At the moment, the Personal Allowance is £12,570, which means you don’t have to pay any tax on the income you earn up to that amount. Anything you earn over that amount, you have to pay tax on.

When we say that the State Pension is taxable, that means that the State Pension will count towards your Personal Allowance. The maximum State Pension you can receive is currently £11,502 (well beneath the threshold where you have to start paying tax). So, if your State Pension is your only income, you won’t have to pay any tax on it.

However, as great as the State Pension is, it’s not a huge amount of money. So, you’ll probably want to make sure you have another source of income on top, to help tide yourself over in your sunset years – like a workplace pension (a pension your employer sets up for you), a personal pension (a pension you set up yourself) or even a part-time job.

If you have other income as well as your State Pension, you’ll probably find you get tipped over the tax free Personal Allowance and end up having to pay some tax.

Confused? Don’t worry, here’s an example for you.

Imagine you’re entitled to the full State Pension, which means you get that nice £11,502 per year we told you about. Now imagine that you also have a part-time job that earns you £5,000 per year. Add them up and together, that means you’re earning £14,627.80 per year – more than the Personal Allowance.

You still get to earn £12,570 tax-free. But you will have to pay tax on the extra £2,057.80 (£14,627.80 – £12,570 = £2,057.80). Income tax for basic-rate taxpayers (people earning less than £50,270 per year) is 20%, so altogether, you’ll pay £411.56 in tax (20% of £2,057.80 is £411.56).

What this means is that you’re not paying tax on your State Pension specifically. Instead, you’re just paying tax on your income, with your State Pension counting towards what you’ve earned that year. Makes sense, right?!

By the way, the tax you’ll pay is Income Tax – that’s the same tax as your salary now. And if you have other income, it’s on your total annual income.

If you're a bit unsure about pensions and would prefer to speak to an expert, check out Unbiased¹ – it's a free service to find pension experts (financial advisors) in your local area.

Find the best personal pension for you – you could be £1,000s better off.

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Find the best personal pension for you – you could be £1,000s better off.

If your income (including the State Pension) is over the £12,570 tax-free threshold, you might be wondering how that tax actually gets taken.

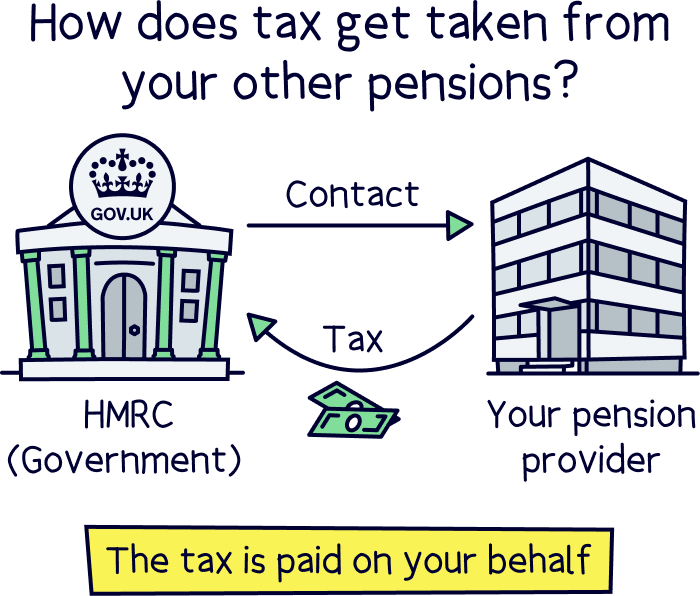

First things first, no tax will be deducted from your State Pension when it’s paid to you. That’s right, you’ll receive the full State Pension payment you’re entitled to, regardless of whether you need to pay tax or not.

Instead, if you need to pay tax, it’ll normally be deducted from your other form of income. Exactly how that works will depend on where else you’re getting an income from.

Often, you’ll get pushed over the tax-free threshold because you have other private pensions that are paying you a retirement income alongside the State Pension.

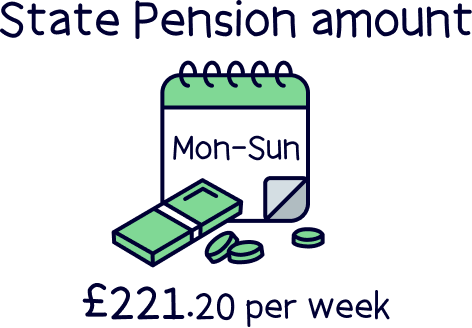

Remember, as lovely as the full State Pension is, the most you’ll get is £11,500 per year. That’s just £221.20 per week – probably not enough to live on without some other form of income alongside it! So, it’s important to pay into a pension throughout your working life, in order to save enough to tide yourself over once you retire. You can set up a personal pension really easily with PensionBee¹, which has a handy app you can use to track your money and watch it grow.

Anyway, let’s say you have another pension that you’re drawing money from at the same time as receiving the State Pension. In this case, HMRC (the part of the government that deals with taxes) will get in contact with your pension provider (the company that controls your pension) and tell them how much tax you owe. Your pension provider will then pay the tax to the government on your behalf, by deducting it from the amount that’s being paid to you, without you having to do a thing.

Oh, there’s just one more thing that you should know. With most workplace and personal pensions, you can take the first 25% of your pension tax-free. So, this pension won’t normally count towards your Personal Allowance until you’ve already taken 25% of it. Kerching!

Did you know you don’t actually have to stop working in order to get the State Pension? That’s right, as long as you qualify for it, you can start claiming it as soon as you hit State Pension age (currently 66, but gradually climbing to 68) – regardless of whether or not you’re still working.

Anyway, if you’re earning over the Personal Allowance and you’re an employee, HMRC will just get in touch with your employer and tell them how much tax you owe. The tax will then get taken off your payslip before it’s handed to you, so that you’re paying the right amount of tax overall.

Again, you don’t have to do anything. However, you should expect to have a bit more tax taken off your payslip than what you did before you started taking the State Pension. This is to make up for the fact that you haven’t had any tax deducted from your State Pension, so don’t worry – it’s normal!

Are you self-employed? Or do you earn money in other ways, like by renting out a property? In this case, you’ll normally have to fill out something called a Self Assessment tax return at the end of the year.

A Self Assessment tax return is basically just a form where you tell HMRC how much you’ve earned that year (don’t forget to include your State Pension!), and how much tax you’ve already paid (if any). It will then calculate how much tax you owe so that you can pay it.

There’s just one downside to paying your tax this way: you’ll normally have to pay it all in one go! So, make sure that you set aside a little bit of money each week or month so that you have enough to pay your taxes with when the time comes.

Self Assessment tax returns can also be a bit complicated to fill in, but don’t worry – you’ll get used to them soon enough. If you want some help, we’d recommend getting in touch with an accountant who can help you fill it in. You can use Unbiased¹ to find the right accountant for you.

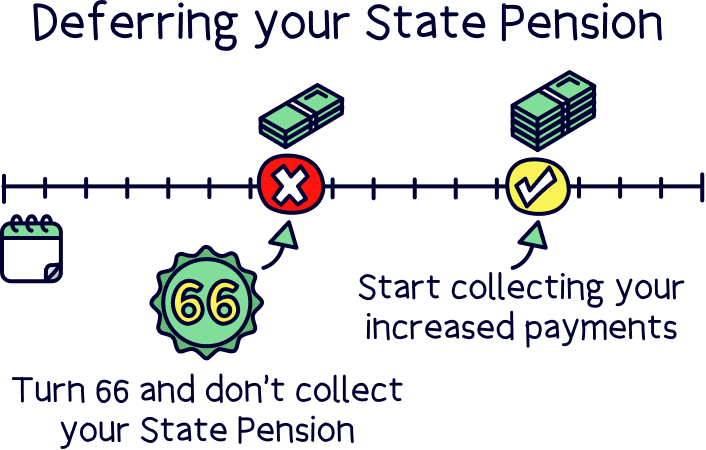

Now, just because you hit State Pension age, that doesn’t mean you have to start taking your State Pension. If you put off taking it until later on, known as ‘deferring your State Pension,’ you could actually increase your State Pension payments!

Exactly how much your State Pension will increase by will depend on when you reach State Pension age and how long you defer it for, but as long as you defer taking it for at least 9 weeks, it’ll increase every week you defer it. Kerching!

So, what does this mean for tax?

Well, you won’t have to pay any Income Tax on your State Pension while you’re not getting it. The same applies whether you defer it or just stop taking it for a while.

However, when you do start taking it, it’ll count towards your Personal Allowance as usual. And because your State Pension payments will be larger, they’ll take up more of your Personal Allowance. So, if you’re over the tax-free threshold, your tax bill may go up just a little bit!

So, in summary, the State Pension is taxable. But you’ll only actually have to pay Income Tax on it if you have another form of income to tip you over the tax-free threshold, known as your Personal Allowance.

Now, it can be tempting to think you need to keep your income as low as possible to avoid paying tax. And we can see why! However, bear in mind that even though the State Pension is a wonderful thing, it’s not a lot of money. Most of us would probably struggle to live on that alone.

That’s why it’s so important to start a pension of your own as well. By starting a pension and paying as much as you can comfortably manage into it throughout your working life, you’ll be able to make sure you’re financially secure when you’re old and grey.

Yes, you might end up tipping yourself over the tax-free threshold. But you’ll also be making sure your sunset years are ones to remember for all the right reasons! If you’re ready to set up a pension of your own, check out PensionBee¹ or Moneyfarm¹ – both easy to use, low cost and a great track record of growing pensions over time.

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

This article was written by the team at Nuts About Money, and fact-checked by 2 independent reviewers. You’re in safe hands.

Find the best personal pension for you – you could be £1,000s better off.