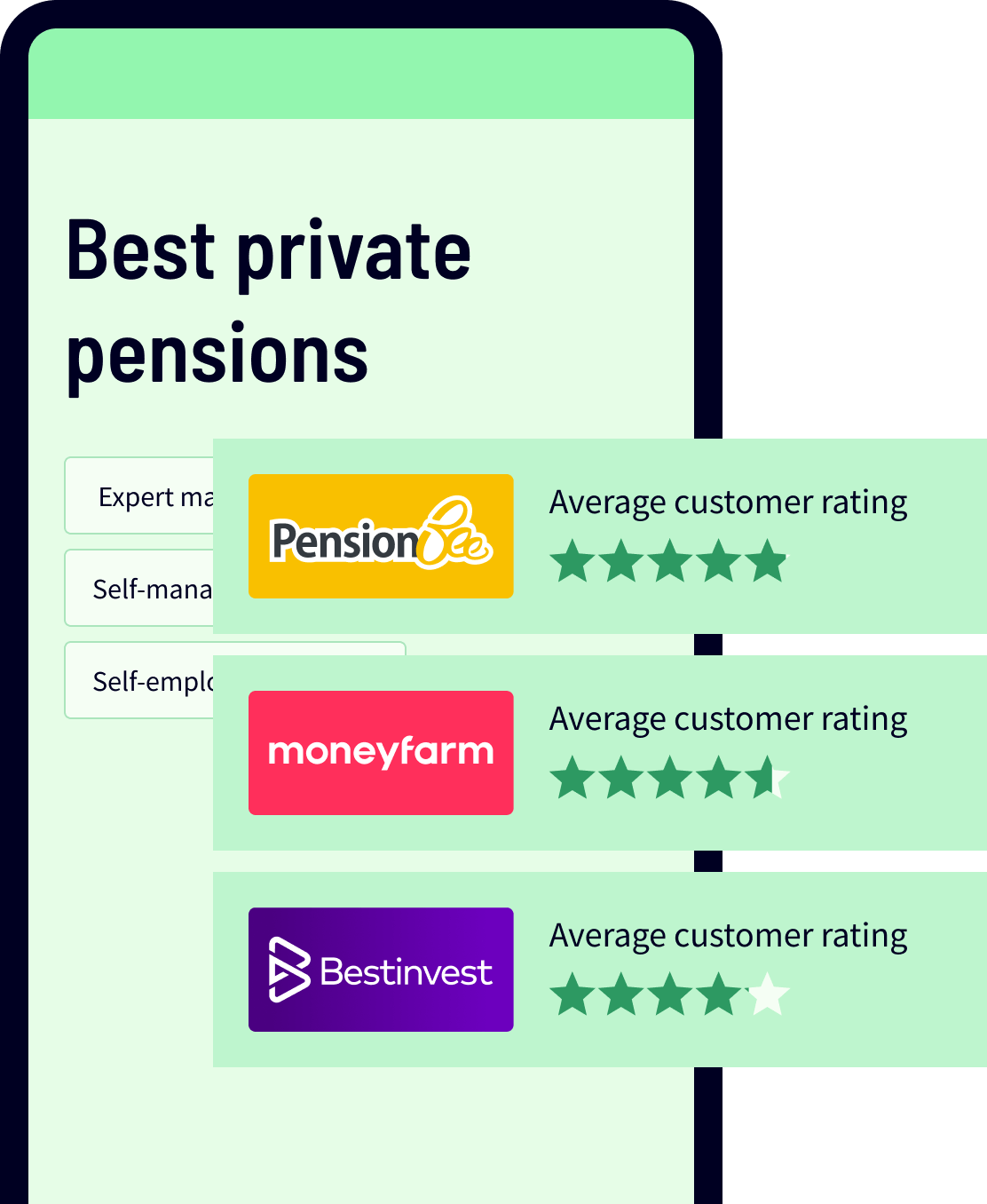

PensionBee makes pensions simple – they'll handle everything for you. They're rated 5 stars, easy to use and have low fees. Highly recommended.

Visit PensionBee¹Capital at risk.

Find and combine lost pensions into one with Beach. It's an easy to use mobile app. Get started in minutes.

Capital at risk.

Compare all the top providers to find the right one for you.