Article contents

It’s a great idea to pay more into your pension so you can have a more comfortable retirement. The best way to do this is max out your pension from work (if they’ll add more money too), otherwise open a personal pension (it’s super easy to do), which is a pension you set up yourself (usually online) – we’ve reviewed all the top options too.

Got a bit of spare cash and are planning to increase your pension contributions? Great! It’s going to be very worthwhile long-term – these days, you’re going to need a pretty huge pension to have a comfortable retirement (we’ll cover that below).

Before we dive into the details, let’s quickly run through the best ways to increase your pension contributions.

1. If you’re employed and have a pension from work, and your employer will match your contributions if you make more (e.g. you pay an extra 1%, they’ll pay an extra 1%), then add more into your work pension to get that extra free cash from your employer, do this until they stop matching your contributions.

2. If your employer won’t match your increased contributions (not many do), or you’re self-employed, the best option is often to open a personal pension and add money directly into it (it’s very easy to do). You'll get some amazing benefits, including a 25% bonus on your contributions.

With that in mind, here’s the best personal pensions – you can set one up in just a few minutes, and be up and adding money in no time.

We’ll cover everything about personal pensions below too.

Experts will handle everything, and you can add money whenever you like.

Find the best personal pension for you – you could be £1,000s better off.

Get £50 added to your pension

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

Great app

A great and easy to use pension. Add money from your bank or combine old pensions into one, (they’ll find lost pensions too).

The customer service is excellent, with support based in the UK.

Beach is an easy to use pension app (and easy to set up), where you just add money and the experts handle everything. It’s all managed on your phone with a great app, and you can see your total pension pot whenever you like.

If you’ve got lost or old pensions, Beach can also find them and move them over too, so you can keep all your retirement savings in one place, and never have to worry about losing them in future.

You’ll get an automatic 25% bonus on the money you add to your pension pot from your bank account (tax relief from the government), which refunds 20% tax on your income, and if you pay 40% or 45% tax, you’ll typically be able to claim the extra back too.

The pension plan (investments) are managed by experts, who are the largest investment company in the world (BlackRock). And they consider things like reducing climate change, meaning your savings could make the world a little better in future too.

You can also save and invest alongside your pension with an easy access pot (access money in around a week), designed for general savings, with the investments managed sensibly by experts too. And money made can be tax-free within an ISA.

Fees: a simple annual fee of up to 0.73% (minimum £3.99 per month).

Minimum deposit: £25

Customer service: excellent

Pros:

Cons:

Find the best personal pension for you – you could be £1,000s better off.

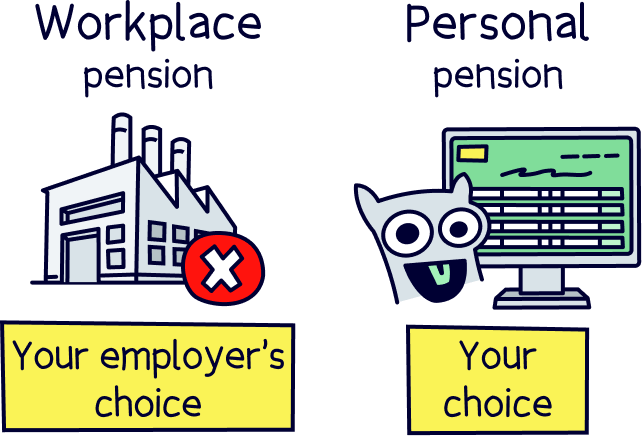

If you have a pension through work, known as a workplace pension, it’s not just you who has to contribute. Your employer legally has to boost your savings for retirement by paying into your pension themselves too. Kerching!

But what happens if you want to save more for retirement? Is upping your pension contributions a good idea?

Well, it’s always a good idea to put aside as much as you can afford for retirement, but depending on where you work, and if your employer will add more into your pension if you do, then you might be better off starting your own personal pension instead of paying more into your workplace pension.

It’s super easy to set up a personal pension, and they’ve typically got much better benefits than a workplace pension. Let’s run through them, and then we’ll explain how to set up a personal pension.

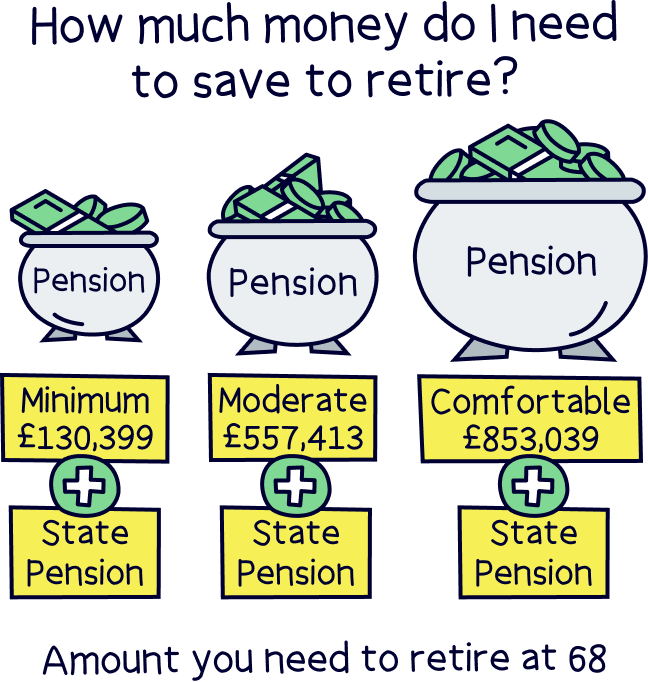

Nuts About Money tip: these days, you’ll likely need a very big pension pot in order to have a comfortable retirement – as much as £853,039 (plus the State Pension), to provide a comfortable income of £43,100 per year. Here’s our guide to how much you’ll need in your pension to learn more.

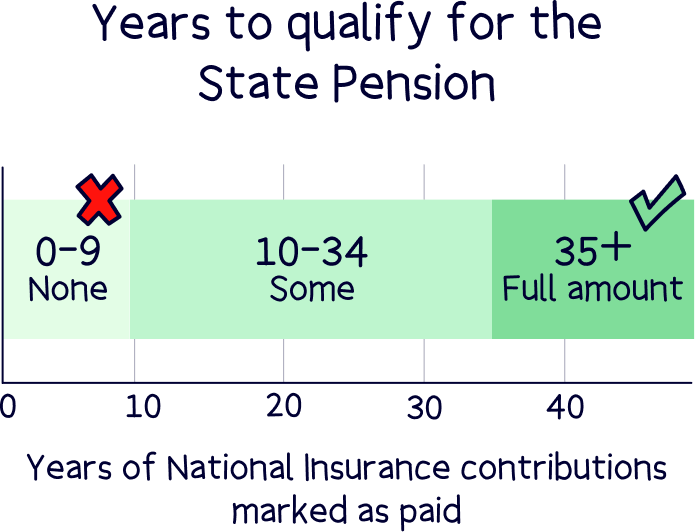

The State Pension is the pension you’ll get from the Government when you reach State Pension age (currently 66 years old). And, you’ll get it if you make at least 10 years worth of National Insurance contributions, but the full amount with 35 years worth.

It’s unlikely to cover many of your bills in retirement, it’s currently just £230.25 per week – and that’s where private pensions come in (workplace and personal pensions), that allow to you save enough (hopefully) to build up a nice big retirement income.

Nuts About Money tip: if you’ve missed a few years paying National Insurance, you might be able to make ‘voluntary National Insurance contributions’. Learn more on the Gov.uk website.

With a personal pension, you’ll be able to decide which pension provider you want your money with, so you can pick a great one, and if you want, you can transfer to another provider whenever you like.

You decide how much you’d like to pay in, and when.

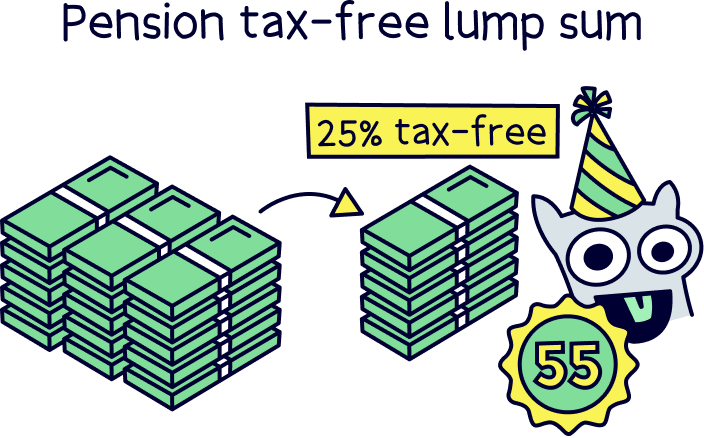

You’ll also get to decide when you want to start withdrawing from age 55 (57 from 2028), if you want to (although it’s a good idea to leave it to go much more over time!).

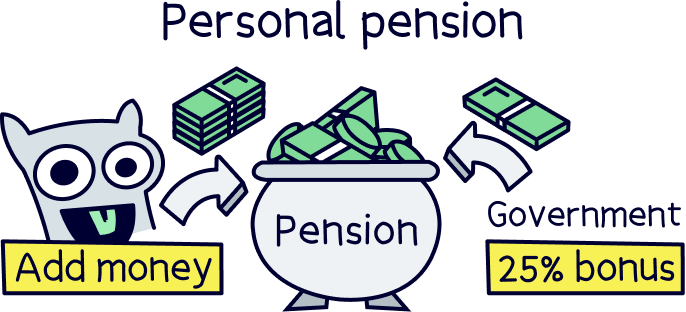

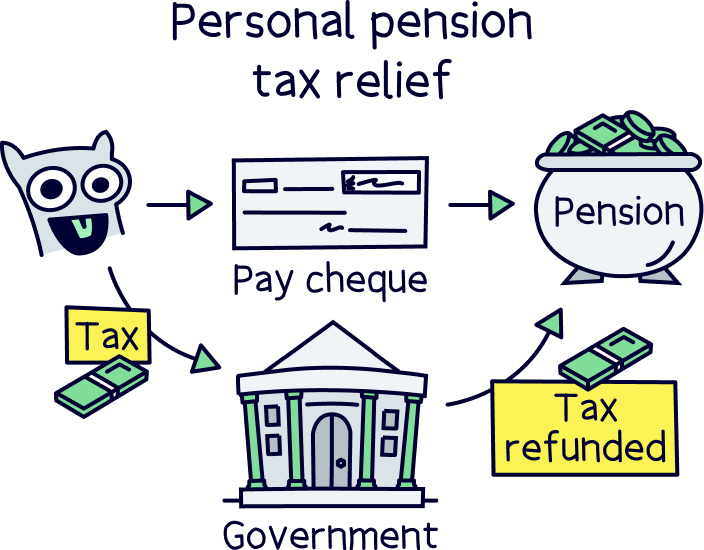

Every time you add money to your personal pension, you’ll automatically get a 25% bonus from the Government (we’re not joking!). This is to refund the money you’ve already paid on your income (e.g. salary).

And if you’re a higher rate taxpayer (40%) or additional rate taxpayer (45%), you can claim back some of the tax paid at those rates too (done a Self Assessment tax return, it’s easy to do but if you want help visit Taxfix¹, their service is low cost, quick and 5* rated).

Your money within your pension will grow tax-free, which means it can grow a lot more over time, and you don’t have to worry about actually paying tax as it grows.

When you do start to withdraw from it, 25% will be completely tax-free. And, you can take this as a tax-free lump sum if you want to (all in one go). You might pay Income Tax on the remaining 75% depending on your income at the time.

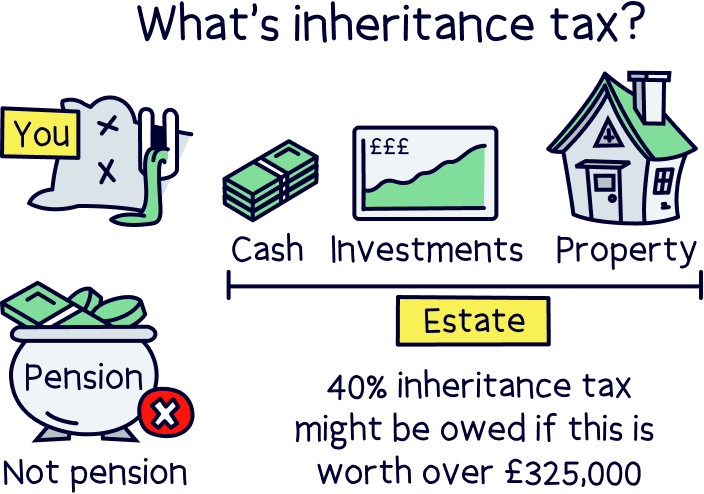

There’s also no Inheritance Tax to pay on pensions when you sadly pass away. They don’t count as part of your ‘estate’, which is all your money and possessions added together.

Pensions are their own separate thing, and you can decide who gets your pension. And, if you pass away before 75, whoever gets your pension won’t have to pay tax at all. If you pass away over 75, they might pay tax (Income Tax) on what they withdraw, it depends on their income at the time.

Personal pensions sound great right? Well before you go and add all your money into one, there is a limit to be aware of – you can only save as much as your total income each year (e.g. salary), or £60,000, whichever is lower. And this applies as a total across all of your pensions (so your workplace pension too if you have one).

And as mentioned you won’t be able to access your money before the age of 55 (57 from 2028).

If your employer won’t match your pension contributions, or you’ve already maxed out your employer’s contributions, you’re often best off starting your own personal pension.

Remember, by starting a personal pension rather than increasing your workplace pension contributions, you get your pick of pension providers. That means you’ll be able to choose a provider with low fees and a great track record of making money grow.

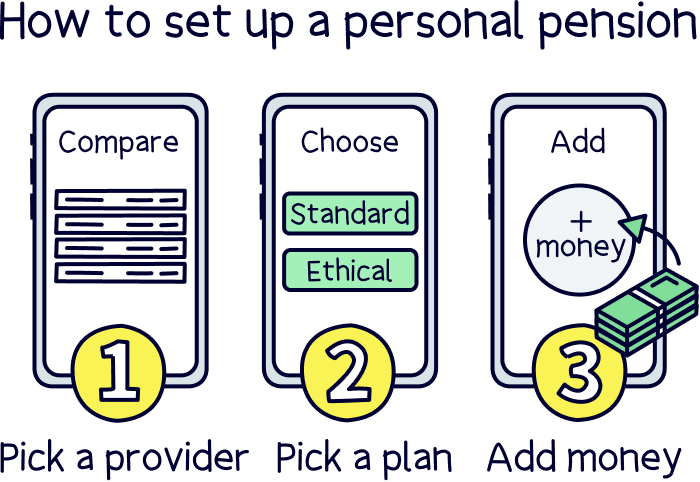

The first step is to choose a pension provider (the company who looks after your pension). Pension providers all offer similar things, but some will do a better job of growing your money than others. And some will charge you higher fees than others will too! So, you should spend some time deciding which one looks right for you.

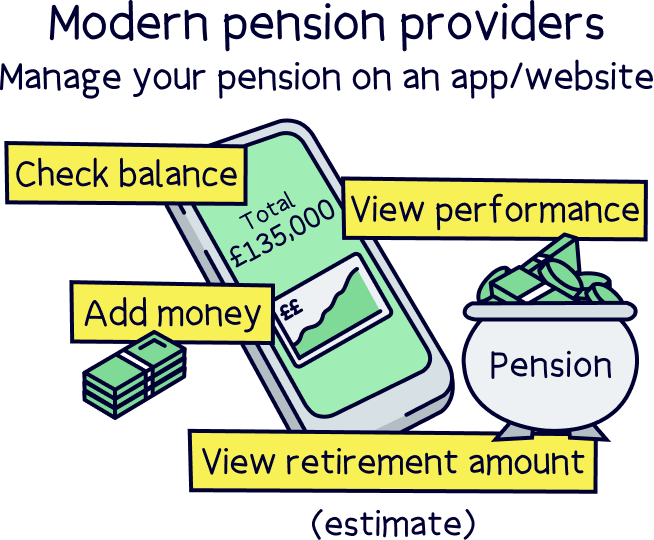

If you’re not sure where to start, we love the modern pension providers that are making it easier to save for retirement. They tend to have handy apps for your phone, so you can keep track of your money and watch it grow. And they often have cheaper fees to boot!

Our favourite is PensionBee¹, it’s easy to use, low cost and a great record of growing pensions over time. Plus, the customer support is great. We’ve also been able to bag you £50 added to your pension when you sign up with Nuts About Money too.

And you’ll love Beach¹ if you’re keen to save within a pension pot and an easy access pot for general savings at the same time.

For all the top options, check out the best pension providers.

Now your pension provider will help you pick a plan. Normally, they’ll just ask you a couple of questions to help you choose how your money will be looked after and how much you’ll pay for the pleasure.

Often, your pension plan will be dictated by how old you are and when you plan to retire. But our favourite providers have other options too, like only investing your money in ethical or socially responsible companies (we’re big fans of those options here at Nuts About Money).

Now you’re all signed up, there’s only one thing left to do: start paying into your pension!

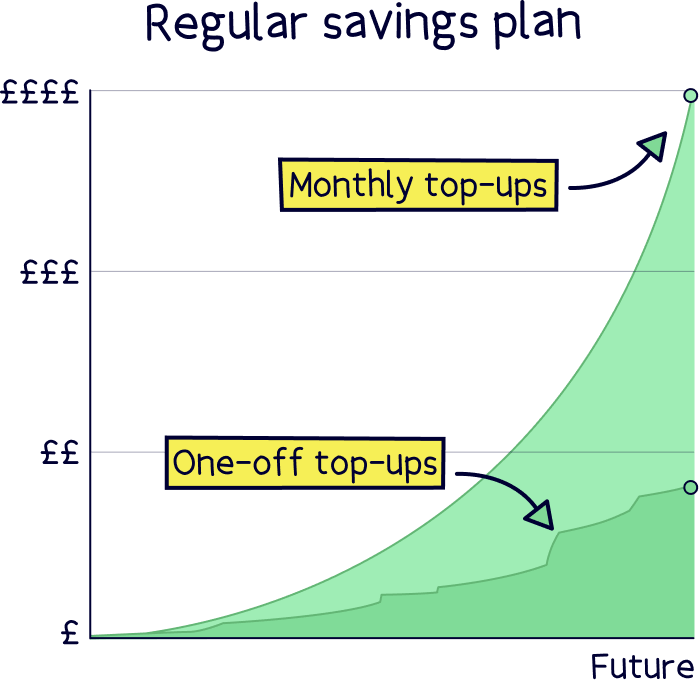

Some personal pension providers will ask you to pay a minimum contribution each month. But most are really flexible and will let you pay as much or as little as you choose.

You can set up a regular/monthly contribution (a great idea to help your pension grow over time), or you can just add in a little bit every now and then when you have some cash to spare. It’s totally up to you!

Remember, it’s sensible to put aside as much as you can afford to, as this will make life easier for you when you’re old and grey.

But at the same time, you won’t be able to access any money you pay into your pension until you’re at least 55. So, it’s important that you don’t overstretch yourself either – you need to be able to live well now as well as later on in life! It’s all about finding the right balance for you.

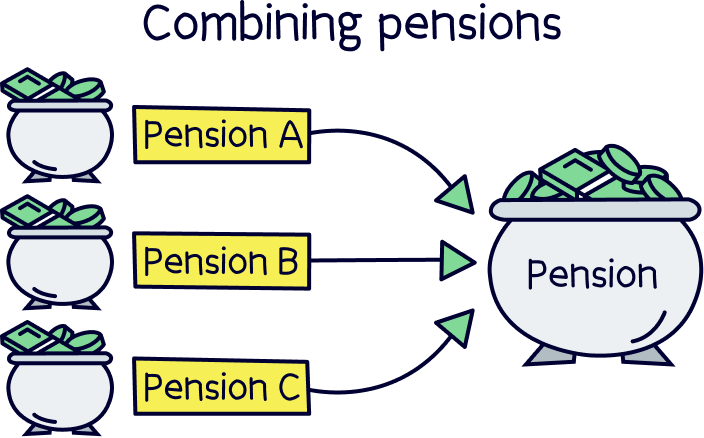

If you’ve had lots of jobs in the past, you can combine your pensions all into your new personal pension (also called consolidating your pension). This can be a pretty good idea to do, as you’ll never forget where they are (which happens a lot), and you can be sure they’re with a provider that you’re happy with.

Note: you can’t transfer your pension with your current job, but whenever you move jobs, you can then transfer it to your personal pension if you want to (usually a good idea).

Great providers such as our recommended option, PensionBee¹, will handle the whole transfer process for you, you don’t need to do a thing – just let them know who your old provider is. And, if you’re not sure, try using the Government’s pension tracing service, or Gretel, a free online service.

We know, we know, nobody likes paying more than they have to. But adding more money into your pension is one area where it really pays off. For one, the more you pay into your pension, the more money you’ll have to live off when you retire. And there are tax benefits that come with putting money into a pension too.

But one BIG reason for making additional voluntary contributions is to do with your employer’s contributions.

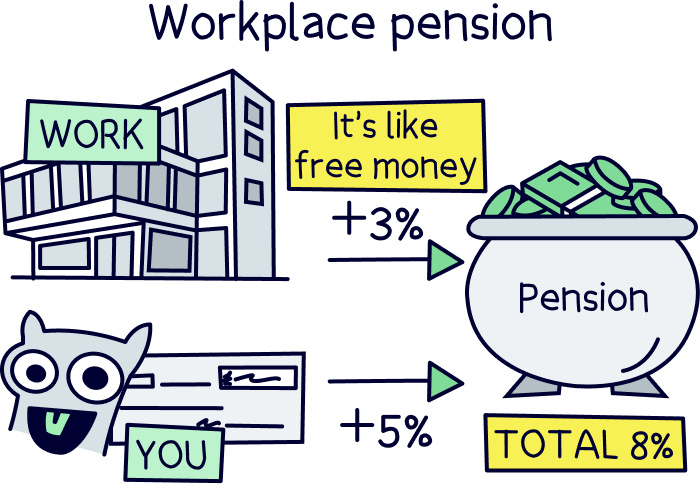

Let us rewind for a moment. Remember how we said that you have to pay at least 5% of your earnings into your pension each month? Well, you’re not the only one contributing to your pension. Your employer also has to contribute at least 3% of your income from their own pocket. Get in!

The key here is ‘at least’. While all employers have to contribute 3%, some very nice employers will choose to contribute more. Often, they’ll do this to attract top talent to their companies.

It normally comes in the form of matching your contributions. In other words, if you pay 5% into your pension each month, your employer will pay 5% too. But if you pay 7% into your pension each month, your employer will also contribute 7%.

If you’re one of the lucky employees who have an employer like this, increasing your pension contributions is pretty much a no-brainer. The more money you pay into your pension, the more free money you get from your employer’s pocket!

Firstly, not all employers are lovely enough to match your contributions. Most employers will only contribute the minimum 3% to your pension, which means you won’t get all that lovely free money by making additional voluntary contributions. Doh!

Similarly, most workplaces that do match their employees’ contributions will put a cap on it. For example, they might say that the maximum they’re willing to contribute to your pension is 12%. If that’s the case, then upping your contributions beyond this won’t unlock more free money either.

Don’t get us wrong, it’s still a good idea to pay more into a pension if you can. But instead of increasing contributions to your workplace pension scheme, in this case, we’d recommend starting a personal pension instead – that’s a pension that you set up yourself.

We love personal pensions because they give you more control over saving for your retirement. Workplace pensions are great and it’s super convenient letting your employer set one up for you. But your employer is unlikely to spend time hunting for the best performing pension providers with the cheapest fees for you, they just want to get the box ticked to say they offer a pension.

With a personal pension, you can find the best pension provider for you, which normally means you’ll end up with someone who can grow your money much faster. Plus, you’ll have the flexibility to save how you want.

Unlike a workplace pension, you won’t have to invest a set amount of money each month – you can contribute as much or as little as you like, even making small one-off payments if that’s what’s best for your bank balance.

So, increasing your workplace pension contributions is a great shout while you’re unlocking more free money from your employer. But if you have additional income you want to add to a pension and you’ve maxed out your employer’s contributions, you’re much better off starting a personal pension alongside your workplace one. That way, you get the best of both worlds!

It’s always a good idea to put as much money into your pension as you can comfortably manage – no matter whether that’s through increased pension contributions or by setting up a new personal pension. Here are the main benefits of upping the amount you put into those pension pots.

You know that rule that says you have to contribute at least 5% of your income to your workplace pension each month? Well, that doesn’t take into account your personal circumstances at all.

Let’s say you start a pension at 40 and you want to retire at 60. That gives you 20 years to save for retirement. On the other hand, if you start a pension at 20 and you want to retire at 60, you’ll have 40 years to save for retirement! So, if you start a pension later, you’ll probably need to put aside a bit more each month in order to save the same amount before you retire.

Similarly, the 5% rule doesn’t take into account your plans for retirement. Some people might not mind cutting back on luxuries in their sunset years, but if you want to live your retirement years to the max (cruises around the Caribbean anyone?!) then you might want to squirrel away a bit more.

Ultimately, the more money you manage to put aside for your retirement, the more comfortably you’ll be able to live when you’re old and grey. As a general rule of thumb, you’re normally advised to save enough so that you have 50% to 66% of your current salary to live off each year when you retire. If you earn £30,000 per year now, that would mean saving enough to pay yourself between £15,000 and £20,000 per year in retirement.

That said, we know that saving up that much can be daunting – especially if you have lots of outgoings, like kids to provide for. Ultimately, the best advice we can give you is to put aside as much as you can manage without overstretching yourself now – you can always up your contributions later down the line. It’s all about working out what’s best for you.

If you want to learn a bit more about how much you’ll need in retirement, check out our guide to how much you should pay into your pension.

Perhaps our favourite thing about pensions is this amazing thing called tax relief.

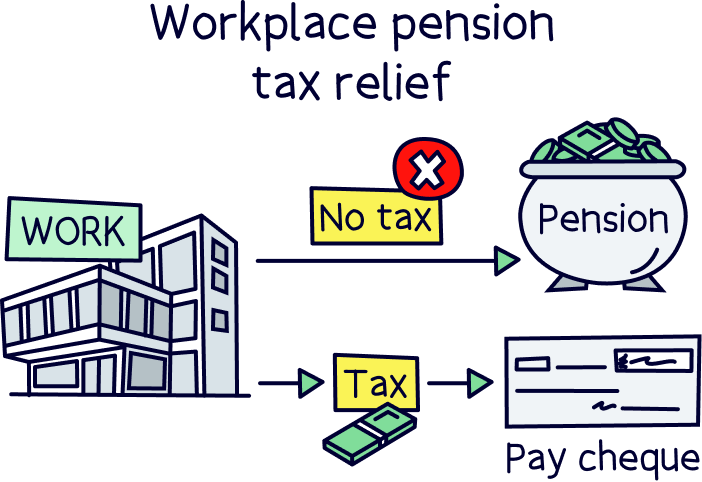

Tax relief refers to the fact that the government doesn’t charge you tax on any income you put into your pension. Happy days! This is all because they want to encourage you to save up for retirement (so they don’t have to support you when you’re older!).

How you get this lovely tax relief is different for workplace pensions and personal pensions (both a type of private pension).

The government won’t take any tax off the money you’re planning on putting in your workplace pension. This is because your employer will tell them how much you’re going to put into your pension in advance.

Your income will be taxed as usual as the government won’t know how much money you’re planning on putting in your pension in advance.

However, once you put money into your pension, you’ll automatically get a 25% bonus from the Government, and if you are a higher rate taxpayer (40%) or additional rate taxpayer (45%) you can claim some of this back on a Self Assessment tax return.

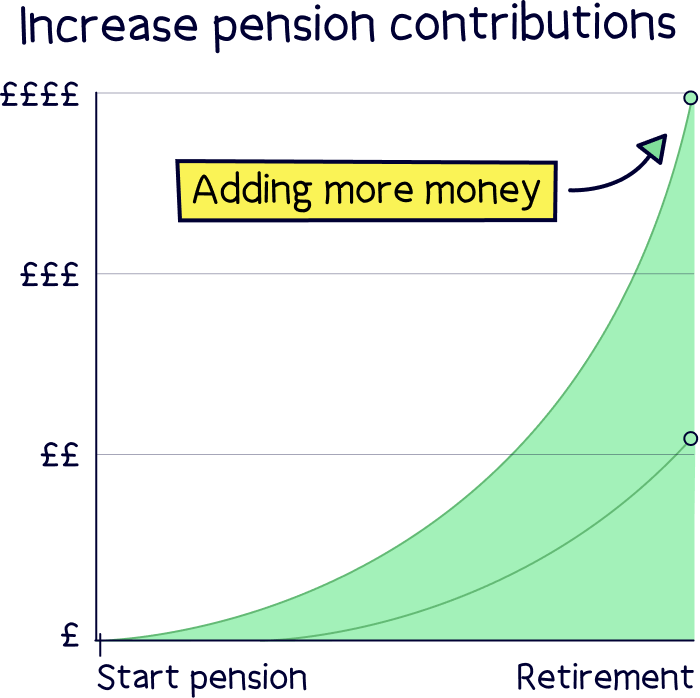

We bet you’ve heard the phrase ‘every little helps.’ And with pensions, it’s absolutely true. Small contributions to your pension pot really can add up over time. This is all thanks to something called ‘compound interest,’ or ‘compounding interest.’

When you leave your money sitting in a savings account like a pension, it will grow as the investments increase in value or you earn interest (more money). Compound interest refers to the fact that this extra money you’ve made on your savings will also grow, so your money is making more money.

Mind boggled? Don’t worry, we’ll break it all down here.

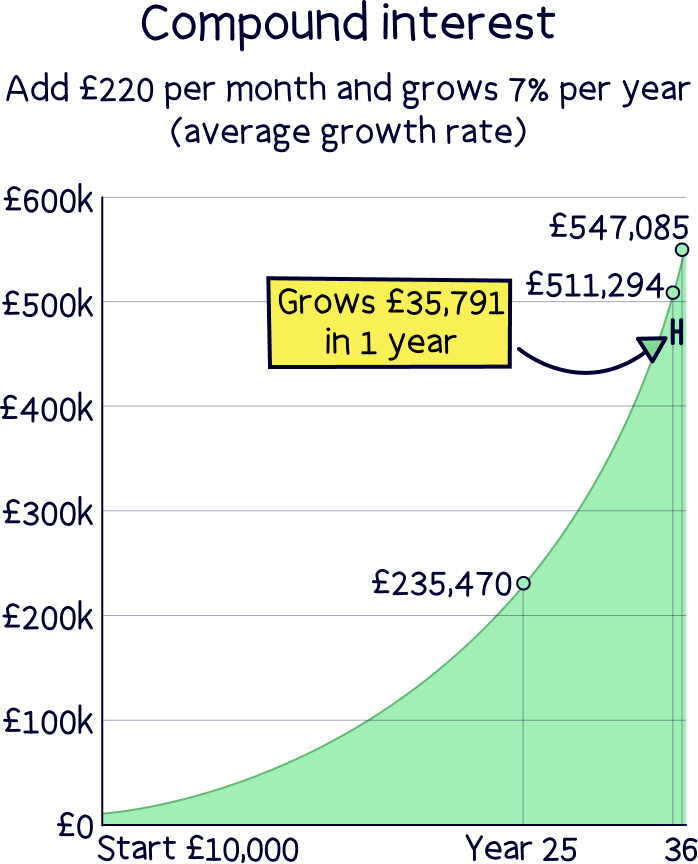

Imagine you have £10,000 in your pension pot currently, are able to save £220 per month, and your pension grows at an average rate of 7% per year.

After 25 years, your pension would have grown to a massive £235,470! And just another 10 years it would have doubled to £511,294. During the next year from there, it could grow by £35,791 in just one year.

Pretty amazing right?!

Adding regular payments as soon as you can, can really impact the total pension pot by the time you retire.

Increasing your pension contributions can unlock more contributions from your employer (if they agree to match your contributions) and help you save more for your sunset years. But how do you do it?

Well, you’ll be pleased to hear that it couldn’t be easier. And we mean it! All you have to do is tell your (the HR department if you have one, or your manager if not), what percentage of your earnings you want to contribute to your pension each month.

Your employer will then sort everything out for you, arranging for your additional voluntary contributions to be collected from your monthly earnings and making sure that the taxman reduces your tax bill accordingly. It’s as easy as that!

So, you can add as much as you want to your pension. But if you want to be able to benefit from that lovely tax relief we told you about, there are limits.

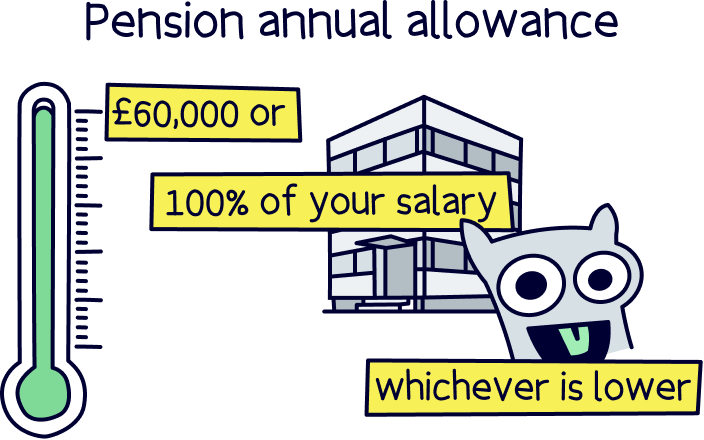

The maximum you can add to your pension while still benefiting fully from tax relief is £60,000. This is known as the ‘annual allowance’ and is set by the government.

However, there’s also this rule: you can only pay in as much as your total income (e.g. salary) each tax year.

In other words, if you earn £30,000 this year, the maximum you can put in your pension (while still receiving tax relief on the whole thing) is £30,000. Or, if you earn £25,000 per year, the maximum is £25,000.

This is unless you didn’t max out on your contributions in the last three tax years, in which case you can use any unused allowance up).

Nuts About Money tip: if you’ve used up your annual limit, you could pay some cash into your partner's pension.

Got some extra income that you can squirrel away into a pension? Go you!

If your employer has agreed to match your contributions, you can make extra pension contributions to unlock more free money from your workplace. Just let your employer know that you want to make additional voluntary contributions and they’ll sort the rest out for you.

If, on the other hand, your employer will only make the minimum 3% contributions to your pension – or you’ve already maxed out your employer contributions – hold fire.

Instead of increasing your workplace pension contributions, you’ll probably be better off starting a personal pension alongside your workplace one.

That way, you get total control over your pension savings. And, you get to choose a top-performing provider with lovely low fees, who are easy to use, and a great track record of growing pensions over time…

As a reminder, our top recommendation is PensionBee¹, for all those reasons, and great customer service. As an added bonus, you’ll get £50 added to your pension for free with Nuts About Money.

There’s also Beach¹ who can handle all of your savings, not just pensions. And for all the top options, check out the best personal pensions.

And that’s all there is to it! Get saving more into your pension – your future self will really thank you.

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.