Article contents

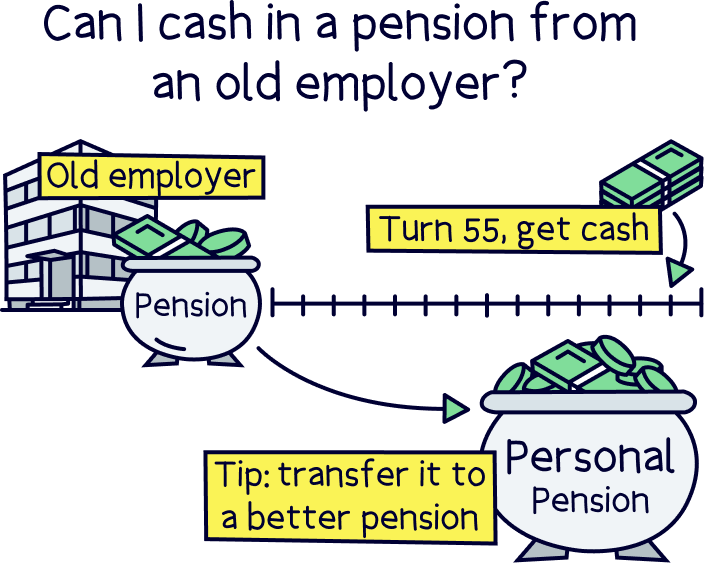

Yes, but you’ll normally have to wait until you’re at least 55! In the meantime you could transfer it to a personal pension where you get to choose who you save with – so you can potentially benefit from lower fees and better investment performance.

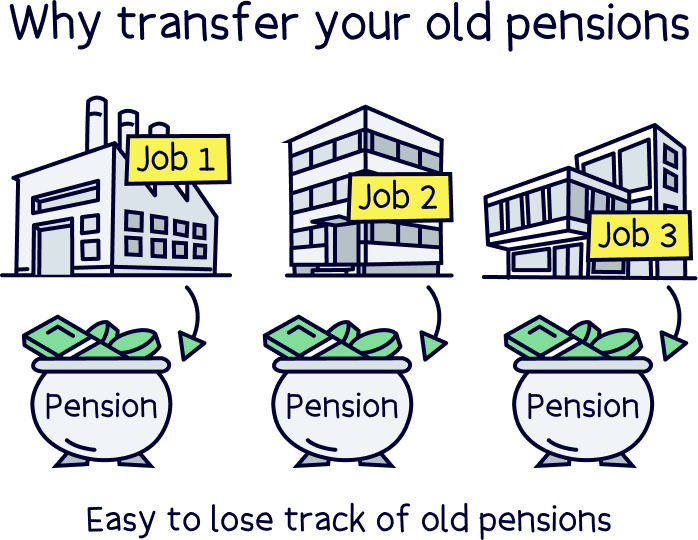

If you’re an employee, chances are you’re going to work for more than one employer in your lifetime. Gone are the days of working in one job from the age of 18 until retirement – instead, UK residents are changing jobs on average 5 times in their working lives (according to AAT).

But if you’re a master at job hopping – or you just fancy a change – you’re probably wondering what will happen to your workplace pension (that’s the pension your employer set up for you) when you change jobs. Don’t worry, your hard-earned savings won’t go to waste. Here’s the lowdown.

Any money you’ve built up in a workplace pension is yours. And it will stay yours – even if you leave your job!

That means you can cash in a pension from an old employer no problem. In other words, you can get all those tasty savings in your pocket as cash. Hooray!

BUT (yep, there’s always a but!), chances are you won’t be able to do so straight away. In the UK, most pensions will make you wait until you’re at least 55 before you take any money out of your pension pot (57 from 2028). So, unless you’ve reached this age, you’ll need to wait a bit before dipping into those lovely savings.

That all sounds easy enough, right? There’s just one problem… by the time you retire, you might well have forgotten all about your old job – and the juicy pension that came with it! Especially if you have lots of different jobs throughout your working life.

For this reason, it’s really important to keep a record of all your old pensions – you don’t want to go losing one, even if there’s only a small amount of money in there (every little helps!). Alternatively, you can choose to lump all your old pensions together in one pot to make them easier to manage. This involves moving your savings from one pension to another, known as a pension transfer.

Nuts About Money tip: Think you might have old pensions you’ve forgotten about? Don’t panic. You can track down any lost pensions using GOV.UK’s find a pension service. Once you know where they are, companies like PensionBee¹ allow you to combine them together and give you access to your money – more on this below!

If you're a bit unsure about pensions and would prefer to speak to an expert, check out Unbiased¹ – it's a free service to find pension experts (financial advisors) in your local area.

Find the best personal pension for you – you could be £1,000s better off.

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Find the best personal pension for you – you could be £1,000s better off.

Changing jobs? Got a while to go until retirement and unsure what to do with your workplace pension? Well, you have a few options. You can…

Here’s the lowdown.

We’re going to start with what we think is the best – you could choose to transfer your old pension to a personal pension (one that you set up yourself). That basically just means moving your savings from your old pension to a new one.

You might think ‘that sounds like a hassle’ but we have some good news. It’s SUPER easy to do and your new pension provider will do all the hard work for you.

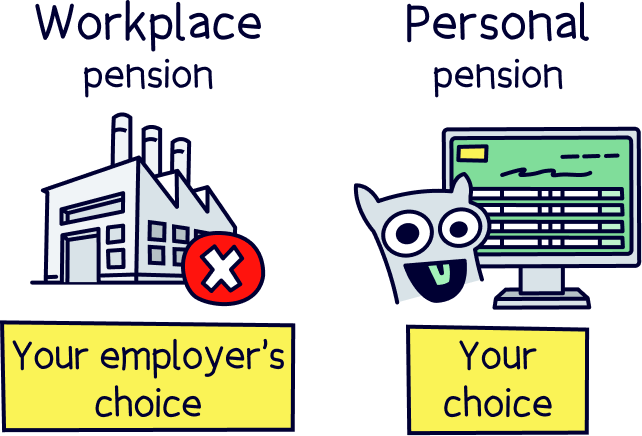

Now, you might think that personal pensions (one you set up yourself) are just for people who don’t have a workplace pension – like people who are self-employed (and so don’t have an employer to set up a workplace pension for them) or people who work part-time (if you earn less than £6,240 per year as an employee, you won’t generally qualify for a workplace pension).

But actually, personal pensions come with loads of benefits that workplace pensions don’t. So, this is a great option for you even if you have a new employer who’s going to be providing you with a workplace pension.

First, unlike with a workplace pension, you get to choose your pension provider! That means you can choose a provider that has cheap fees and that’s got a proven track record for growing money quickly. So, you’ll often end up boosting your savings in retirement even more and ending up with a bigger pot to live off in your golden years!

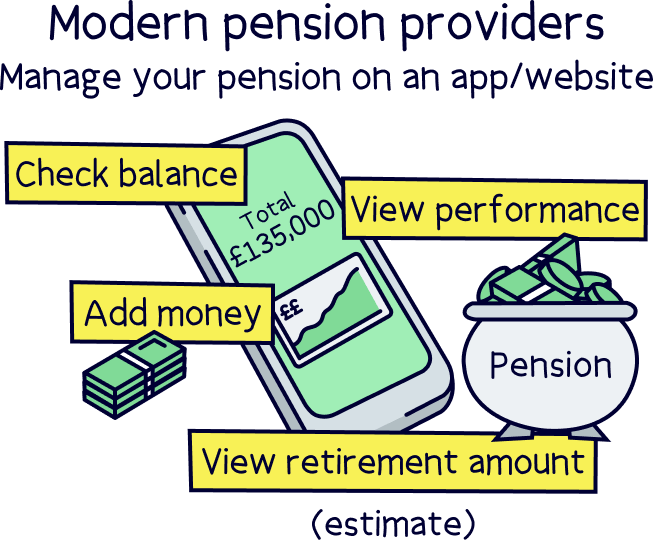

Plus, if you go for a more modern pension provider, you can usually benefit from handy mobile apps that allow you to track your money and watch it grow – making it even easier for you to save for retirement.

There are lots of great providers out there, but one of our favourites has to be PensionBee¹. It has great customer service and its slick mobile app makes saving oh-so-easy. Beach¹ is also great, it's an easy to use pension with a great app. Add money or combine old pensions (and find lost pensions). Plus, the customer service is excellent.

As well as helping you to grow your money quicker, you’ll also find that a pension transfer will make your savings easier to manage. If you’ve had a few employers in the past and a few different pensions, you can move all your old pensions to your new personal pension so that they’re all in one place and you’re less likely to forget about them! Oh, and you’ll have fewer providers to pay fees to.

On top of all that, if you often move jobs, you can just keep your personal pension going instead of having to move your old pensions again when you change employers. Think about it: you’ll have a pension that’s completely in your control no matter what – each time you move jobs, you can just transfer your latest workplace pension over to your personal pension provider so that your savings can keep growing as quickly as possible without you needing to pay hefty fees for the pleasure.

If you don’t fancy setting up a personal pension, a good plan B could be to transfer your old pension across to your new workplace pension. This is pretty easy to do, your new workplace pension provider will sort it all out for you so that you don’t have to lift a finger.

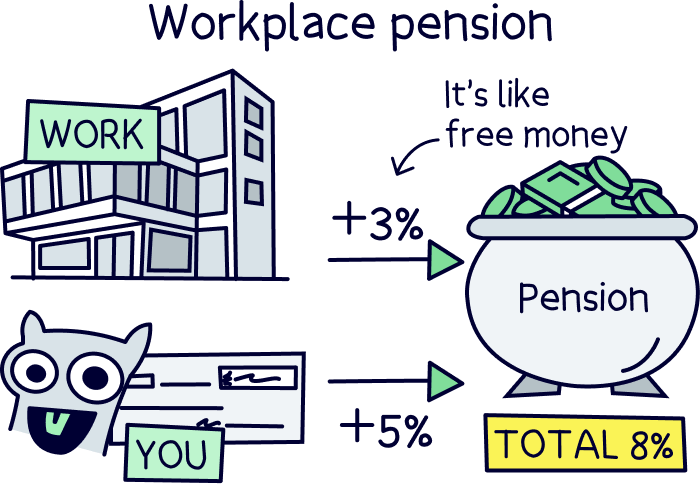

Let’s rewind for a second. Employers are nearly always legally obliged to set up a workplace pension for you, known as ‘auto enrollment.’ Every month, a least 5% of your income will be automatically deducted from your paycheque and will go into your pension. Plus, your employer will contribute at least 3% of what you earn from their own pocket.

So, chances are your new employer will be setting you up a new workplace pension which you can transfer your old pension into.

This will have quite a few of the same benefits as transferring your old pension to a personal pension. If you have a few old pensions, transferring them all to one workplace pension can help you to manage them more easily. And you’ll only have one pension provider to pay fees to.

In fact, some people prefer it because it means all their retirement savings will be in one place, rather than spread out across a personal pension and the new workplace pension.

However, it’s not quite so great as transferring your old pensions over to a personal pension.

Why? Well, personal pensions give you more control over your savings – you get to choose your pension provider so you’ll normally be able to access lower fees and find a provider that has a proven track record for growing money quickly.

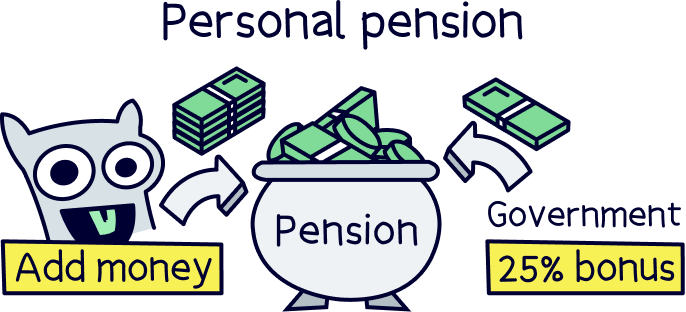

Plus, with companies like PensionBee¹, you can top-up your pension with any cash you might have in a few clicks. You'll also benefit from a free 25% government bonus, this is automatically added to your pension. How great is that?

And, at the end of the day, who doesn’t want to boost their retirement income and save on fees?!

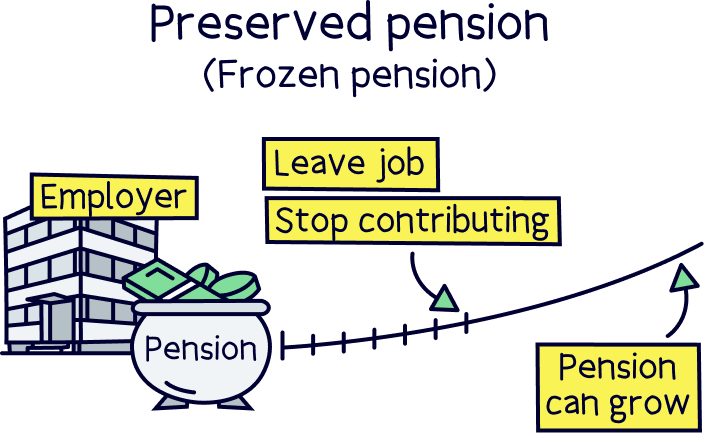

Finally, when you leave your old employer, you can just leave your pension where it is and stop contributing to it. This is known as a ‘preserved pension’ or you may also see it referred to as a ‘frozen pension.’

Yes, you won’t be contributing to it anymore and neither will your new employer. But your pension can still make you money!

Let us explain.

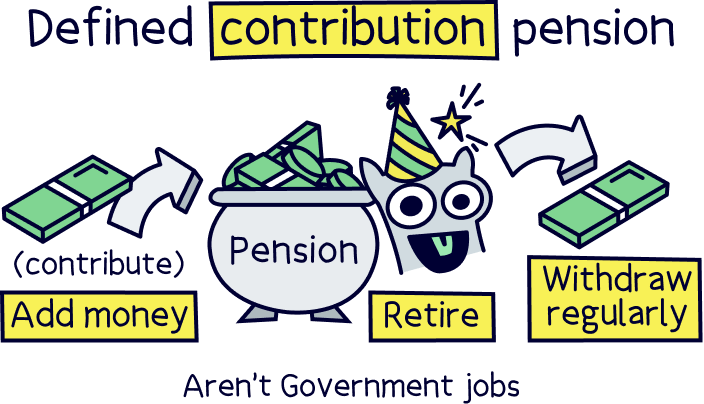

Most workplace pensions are what’s called a ‘defined contribution pension.’ That means they work a bit like a piggybank. You pay into it every month (at least 5% of your income) and your employer also contributes (they’ll normally have to add at least 3% of your income from their own pocket!). However, they’re even better than a piggybank because they’re designed to grow your earnings without you having to do anything at all.

Basically, the money you put into your pension gets invested by experts, which means it’s used to buy things like stocks and shares. As these go up in value, your money should go up in value too, meaning by the time you retire, you’ll have more money to enjoy than what you and your employer actually put in.

If you leave your employer and stop paying into your pension, this means your pension is ‘frozen.’ It won’t grow as fast as it would if you were consistently adding in money. But it will hopefully still grow as your investments continue to grow, just make sure you know what the fees are. High fees will reduce your pension total over the years, it can add up to eye-watering amounts without even knowing it. Our top recommendation PensionBee¹, has low fees, and again, they make it super easy to transfer old pensions over.

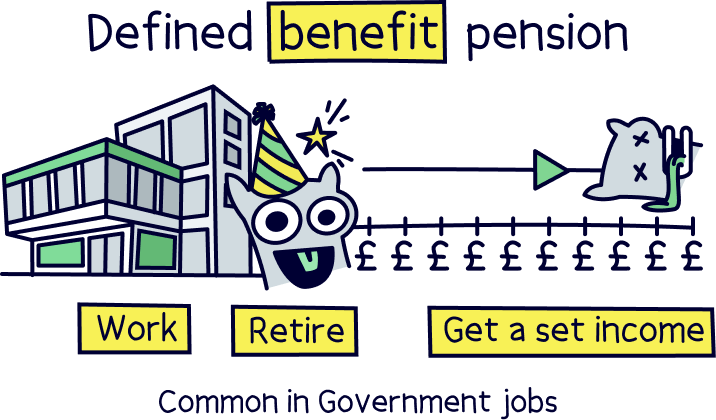

On the other hand, a few people have something called a ‘defined benefit pension.’ Instead of working like a piggybank like a defined contribution pension, your employer (or ex-employer!) will pay you an income in retirement based on your salary and the number of years you worked for them.

If you have one of these, it’s almost always best to leave it where it is, as if you move it elsewhere, you could risk losing some of the special benefits it comes with – like a guaranteed income throughout retirement. For this reason, you’ll legally have to get advice from an independent financial advisor if you’re considering transferring a defined benefit pension. You can find the right one for you using Unbiased¹, which specialises in matching you with expert advisors.

Not sure what kind of pension you have? Then the chances are you have a defined contribution pension (you know, the piggybanks ones!) and you won’t have to worry. After all, nearly all pensions work this way and it’s generally only a few older ones that don’t.

Ultimately, if you choose to leave your pension where it is, you don’t have to do a thing (but please look at the fees you're paying) – simply sit back, relax and let your pension provider (the company looking after your pension) know when you’re ready to start taking an income from it. Just remember, you have to be at least 55 to start taking money from your pension, unless you want to risk paying VERY hefty fees and taxes – you can learn more about that in our article on whether you can withdraw your pension before 55.

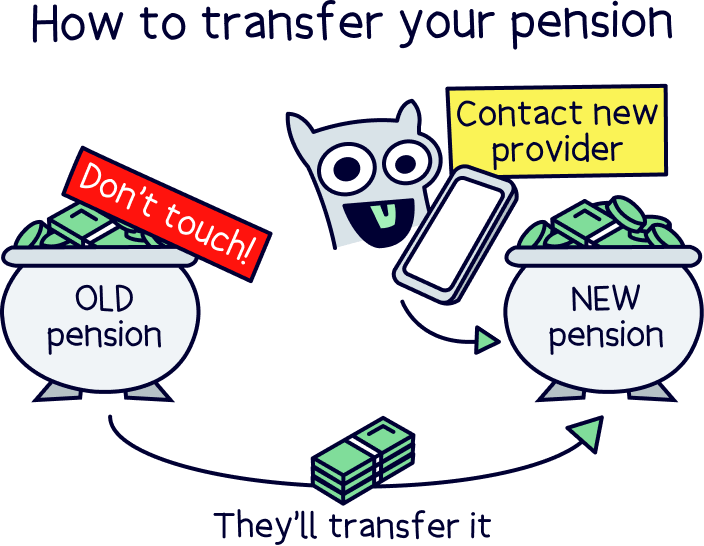

Decided that transferring your old pension is the way forward? Whether you decide to transfer it to your new employer’s workplace pension scheme or to a personal pension, it’s super easy! Here’s how to do it.

First things first, you’ll need to dig out the details of your old pension. Normally, all you’ll need is the name of your pension provider. However, it can be handy if you have more details too, like the value of your pension. And it’s also good to check whether you’ll be charged any fees for leaving.

If you’re not sure where your old pension is, don’t worry. You can use the find a pension tool on GOV.UK to track down any old pensions that you may have forgotten about.

If you already know which pension provider you want to transfer it to, they should also be able to help you to track your old pension down. Some will have their own tool where you can just put in the name of your old employer to find out which pension provider is looking after your pension. Easy!

Next, you’ll need to decide where you want to transfer your old pension to.

We’d recommend transferring it to a personal pension – either one you’ve already set up, or to a new one altogether – as this way, you can choose a provider that has low fees and that can grow your money quicker. Starting a personal pension is really easy. In fact, it can be done in minutes if you choose the right pension provider!

Not sure who to pick? If you like the idea of a handy mobile app that can help you track your money, you’ll love PensionBee¹ and Beach¹. They both have pretty low fees and great customer service too!

Decided which pension provider you want to transfer your old pension to? Then all that’s left is to tell them you want to do a pension transfer.

Normally, you’ll just need to give them the name of your old pension provider. Then, you can sit back and relax – your new pension provider will get in touch with your old one to arrange the whole transfer for you.

Your old pension provider might ask you to confirm the transfer. But other than that, you simply have to wait for those savings to appear in your new pension pot, which normally takes around 2 to 4 weeks. So, enjoy working your way through Netflix’s whole back catalogue while your pension providers do the heavy lifting!

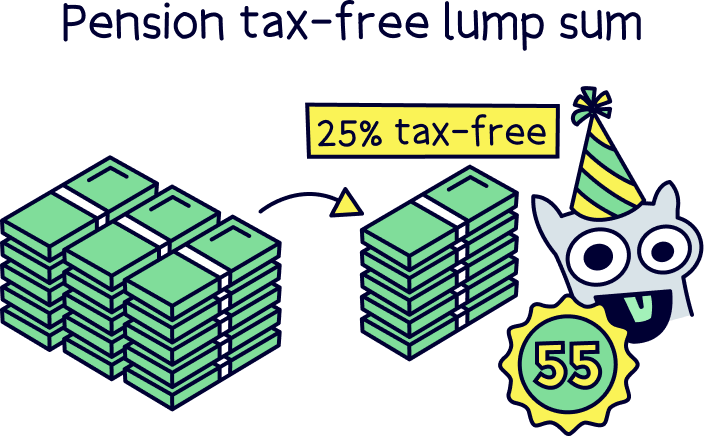

Once you reach the grand (not-so-old) age of 55, you’ll be able to start withdrawing cash from your pension. Kerching!

This applies to pensions from old employers and pensions from current employers. It also applies to personal pensions – they should all work pretty much the same! So, how can you do it?

Well, every pension provider will have its own rules and ways of doing things. But you can normally take the first 25% of your pension pot all at once, as a tax-free lump sum. Nice!

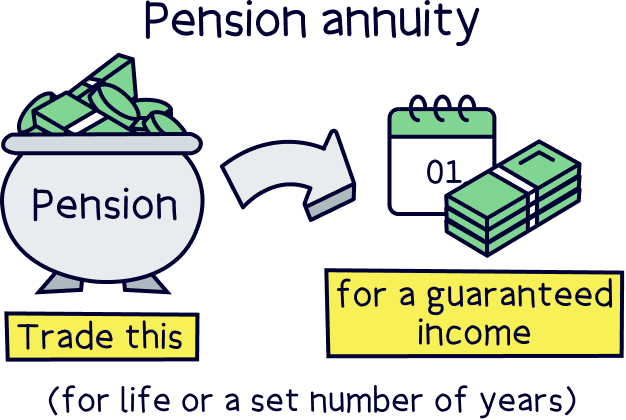

With the remaining 75%, you can…

To learn more about these options, check out our article on how you can take your pension tax-free lump sum.

When you start taking an income from your pension, just remember to check whether you have any old pensions you may have forgotten about. Who knows, if you’ve had many employers, you may just have a few extra pension pots lying around that you didn’t know about (crack out the champagne!). Head to GOV.UK to get started – it’s just 10 minutes of your life but potentially thousands of pounds you could have stashed away!

Even though your old employer set up your workplace pension for you, that money will still be yours when you leave your job! So, it’s up to you what you want to do with it.

If you’re over the age of 55 (or potentially 57 from 2028), you can choose to cash it in to get those juicy savings (and tax-free cash) straight into your pocket. But if you’re younger, you’ll need to wait a bit – so, we’d recommend transferring it over to a personal pension where your savings can grow quicker – check out our guide to personal pensions to get started.

Whatever you choose, just don’t forget where you’ve squirrelled away your savings!! You might laugh but we promise, it’s a thing – according to The Association of British Insurers, there are around 3.3 million lost pension pots in the UK that together are worth around £31.1 billion. Gulp.

So, move on from your old employer and job hop all you want – just keep a track of your old pensions (or where you’ve transferred them to!) and you’ll be perfectly placed to enjoy retirement to the full (cruises around the Caribbean, anyone?!).

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.