Article contents

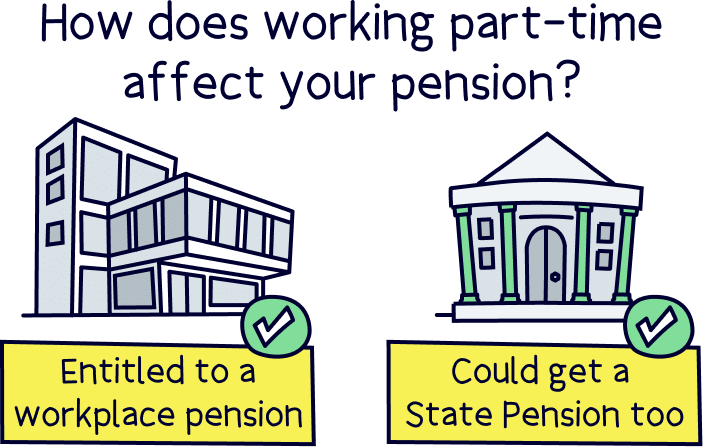

If you work part-time, you still have the same right to a workplace pension as someone who works full-time. As long as you’ve made National Insurance contributions, you should qualify for a State Pension too.

Want to reduce your hours at work? You’re not alone! More and more of us are looking for a better work-life balance and the number of people working part-time has recently jumped to over 8 million in the UK (according to the Office of National Statistics)!

But how does working part-time affect your pension?

Well, you’ll be pleased to know that part-time workers are entitled to a workplace pension, just the same as full-time workers are. Oh, and as long as you meet certain criteria, you should still get a State Pension too. If that all sounds like gobbledygook then don’t worry! We’re here to break it all down for you.

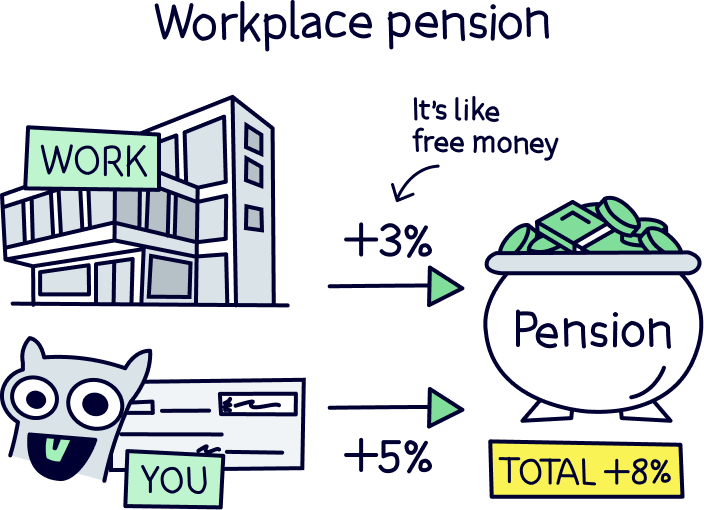

A workplace pension scheme is a pension that your employer sets up for you. You contribute a percentage of your earnings each month (at least 5%), and your employer tops that up themselves (they have to add at least 3% from their own pocket). Kerching!

The money that you and your employer add to your pension is meant to tide you over later on in life – at the moment, you’re allowed to take money from your pension when you turn 55, but it’s rising to 57 in 2028.

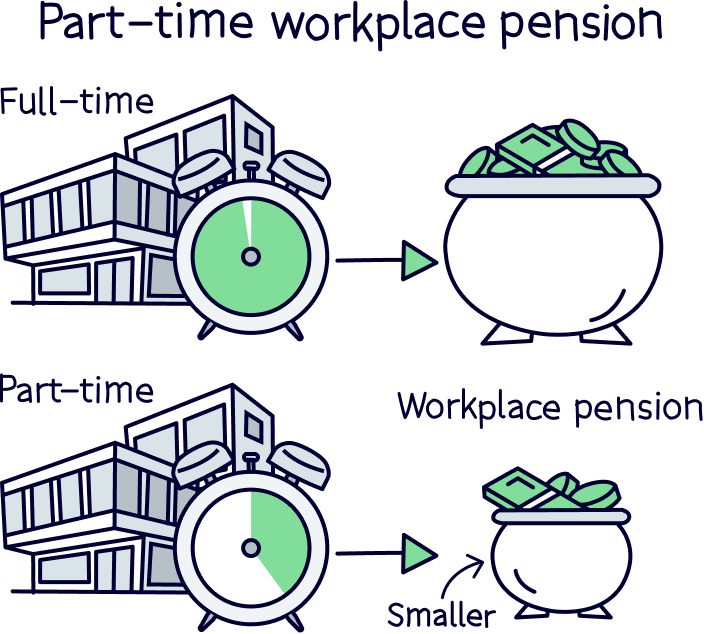

Working part-time doesn’t really affect your workplace pension all that much. If you’re a part-time employee, you’re still entitled to a workplace pension – just like a full-time employee.

The main difference is that you’ll probably be earning less than someone who’s working full-time. That means you won’t have as much money going into your pension each month, so you’ll probably have less to live on when you retire.

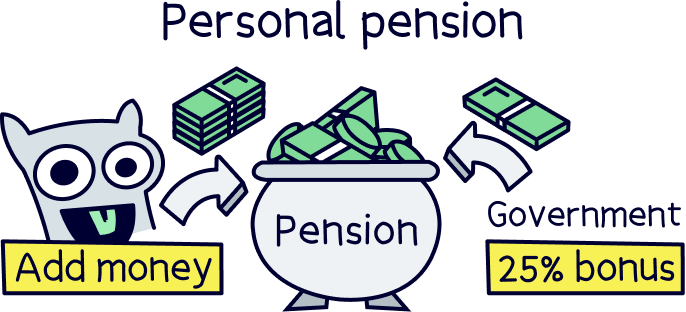

Nuts About Money tip: to help save for your future, open a personal pension. You'll get a 25% bonus every time you save. Our recommend provider is PensionBee¹.

Wondering how to access this wonderful thing called a workplace pension as a part-time worker? Well, if you earn more than a certain amount each year (currently £10,000), the chances are your employer will have to automatically create a pension for you, called ‘auto-enrollment.’ So you won’t have to do anything at all!

You’ll get auto-enrolled if you’re all of these things:

Do you earn less than £10,000 per year? Don’t worry, you may still be able to get a workplace pension.

Although your employer won’t have to automatically enrol you into a pension scheme, you can still ask them to set one up for you if you earn at least £6,240 per year. And the really good news is that they can’t say no! In fact, they’ll still have to make contributions for you out of their own pocket, just the same as if you were auto-enrolled. So, make sure you ask them to arrange one for you if this applies to you!

Just remember, if you're working part-time you probably won't add as much money to your pension as a full time employee, meaning your pension pot probably might not be as high when you retire. You can increase your pension by getting a personal pension through companies like PensionBee¹.

The State Pension is a weekly payment you can get from the government when you reach a certain age, known as State Pension age. Hooray! State Pension age is currently 66, but it’s slowly getting higher and higher (for people born in April 1960 or after, it’ll be 67 and then it’s going to gradually climb to 68).

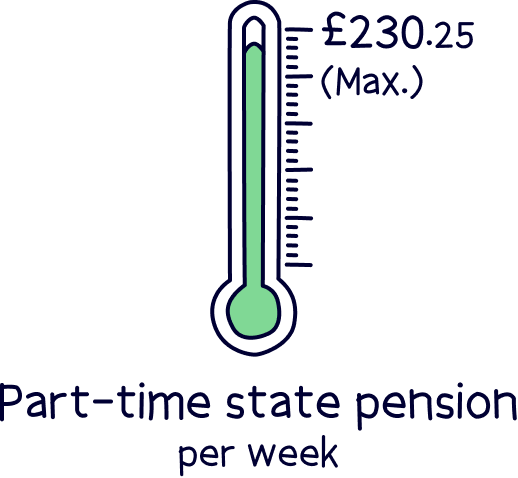

At the moment, the full State Pension is £230.25 a week. It may not sound like much, but the good thing is that you can get it on top of your workplace pension (and on top of your personal pension if you have one, which is a pension you can set up yourself). So it’s a nice extra!

Anyway, what you really want to know is whether your State Pension will be affected by working part-time. The answer? Not directly!

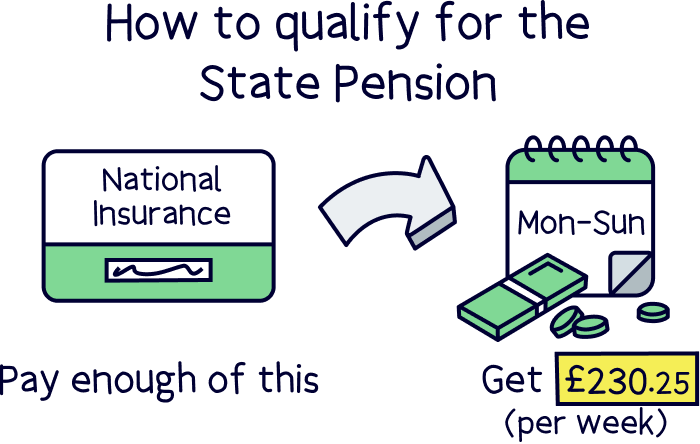

That’s right, you can get the State Pension whether you’re working full-time or part-time. However, in order to qualify for it, you have to make National Insurance contributions over your working life (National Insurance is a payment you make to the government alongside your taxes, to cover things like healthcare).

If you earn very little (which is more likely if you work part-time), you may not need to pay National Insurance. That might sound great, but not paying National Insurance can mean not qualifying for the State Pension. Urgh! Which brings us onto…

If you’re going to qualify for the State Pension, you’ll need to make National Insurance contributions over your working life. You need to pay National Insurance for at least 10 years to get anything at all. But to get the full State Pension (that £230.25 per week we were telling you about), you need to pay it for at least 35 years.

If you earn more than £184 per week (or you make a profit of at least £6,515 a year if you’re self-employed) you have to make National Insurance contributions. So, you should be well-placed to get that nice weekly payment. Awesome!

If you earn more than £120 per week (but less than £184), you don’t have to make National Insurance contributions. But guess what? Your contributions will be marked as paid on your record so that you can still qualify for the State Pension – even more awesome!

However, if you earn less than £120 per week, things can get tricky for you. You don’t have to pay National Insurance. And sadly, if you don’t, nobody’s going to mark it as paid for you. That could very easily mean no State Pension for you later on in life.

But there is some good news! You can avoid this from happening by making voluntary National Insurance contributions (paying National Insurance even though you don’t have to). Although paying something voluntarily might not sound like your idea of fun, at least it will mean you can qualify for that State Pension. Just think of it as buying security for later on in life – your older self will thank you for it!

You’re probably tired of us banging on about how you’ll have less to live off when you retire if you’re working part-time. But it’s true! If you’re working fewer hours, that means you’ll be earning less and likely squirrelling less away into that pension.

Yes, the State Pension can help to top up your income when you reach State Pension age. But in reality, this will only give you a small payment each week, which won’t be enough for most people to live off.

So, why are we going on about this? Contrary to what you might think, we’re not just doing it to rub it in or depress you. Promise! Instead, we want to make sure you know how important it is to start saving for retirement now, so you don’t get caught out in the future.

Luckily, it’s really easy to do that, using something called a personal pension.

A personal pension scheme is one that you set up and pay into yourself. It’s basically a special savings account that you can only access when you reach State Pension age – except better, as you won’t have to pay tax on the earnings you pay into it!

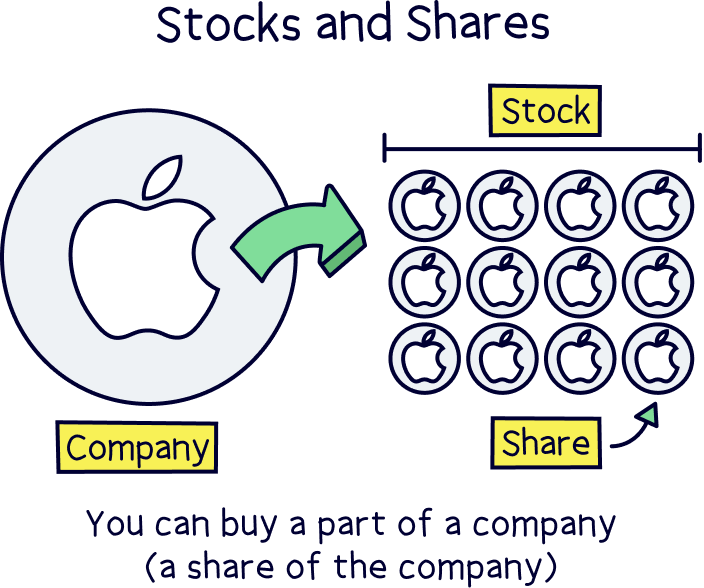

Even better than that, the money you put into your personal pension will get invested (used to buy investments like stocks and shares, which are essentially ownership stakes in companies). The idea is that your investments should increase in value over time so that you have more money to live off when you retire. Pass the champagne!

By setting up a personal pension, you can top up the income you get from your workplace pension and your State Pension. That way, you’ll have enough money to be able to live a nice life when you get older (cruise anyone?!).

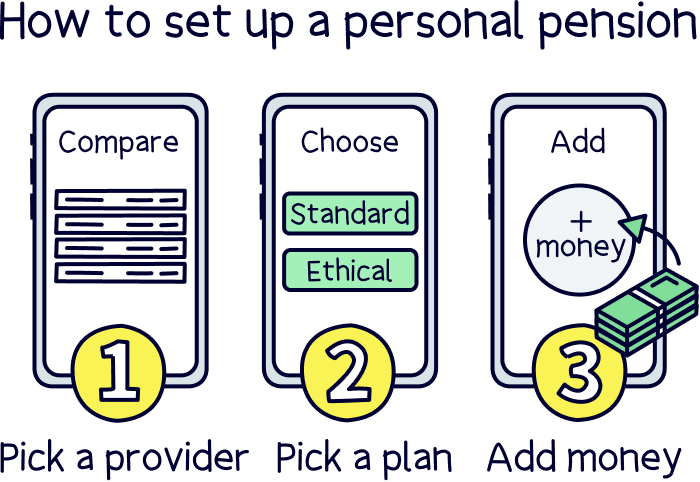

To get a personal pension, you just have to choose a pension provider (those are the companies that give out pensions). Each pension provider will have their own pension plans, which are basically schemes where they lay out how much they’ll charge you and where they’ll put your money (in other words, what kind of investments they’ll make on your behalf). You just need to pick the one that sounds best for you.

Don’t worry, we know that that involves a lot of research, which can be pretty time-consuming. So, to save you time, we’ve done the hard work for you and have picked out our 3 favourite personal pension providers.

These providers all make it super easy to set up a pension and see where your money is going with handy apps and fantastic customer service. We’ve also written reviews about each one to tell you a bit more about why we like them so much – so, have a read if you see a provider below that you like the sound of!

Find the best personal pension for you – you could be £1,000s better off.

Get £50 added to your pension

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

Great app

A great and easy to use pension. Add money from your bank or combine old pensions into one, (they’ll find lost pensions too).

The customer service is excellent, with support based in the UK.

Beach is an easy to use pension app (and easy to set up), where you just add money and the experts handle everything. It’s all managed on your phone with a great app, and you can see your total pension pot whenever you like.

If you’ve got lost or old pensions, Beach can also find them and move them over too, so you can keep all your retirement savings in one place, and never have to worry about losing them in future.

You’ll get an automatic 25% bonus on the money you add to your pension pot from your bank account (tax relief from the government), which refunds 20% tax on your income, and if you pay 40% or 45% tax, you’ll typically be able to claim the extra back too.

The pension plan (investments) are managed by experts, who are the largest investment company in the world (BlackRock). And they consider things like reducing climate change, meaning your savings could make the world a little better in future too.

You can also save and invest alongside your pension with an easy access pot (access money in around a week), designed for general savings, with the investments managed sensibly by experts too. And money made can be tax-free within an ISA.

Fees: a simple annual fee of up to 0.73% (minimum £3.99 per month).

Minimum deposit: £25

Customer service: excellent

Pros:

Cons:

Find the best personal pension for you – you could be £1,000s better off.

As far as we’re concerned, there’s nothing negative about apps and websites that make setting up and managing your pension super easy. In fact, we love them!

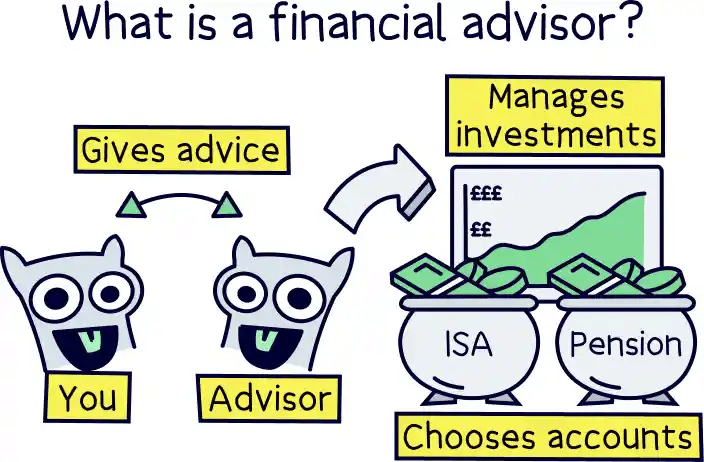

However, we get that not everyone’s comfortable doing things this way. So, if that sounds familiar, you can also just speak to a financial advisor.

Financial advisors are professionals who can help you set up a personal pension, either in-person or over the phone. Just be aware that they can be expensive as they add their own fees on top and don’t always pick the cheapest pension funds!

To find a local pension expert (financial advisor), you can use Unbiased¹, it's a free service to find qualified advisors in your area.

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Find the best personal pension for you – you could be £1,000s better off.

Just want to speak to someone? You can get free guidance from the Pensions and Advisory service (MoneyHelper), a Government organisation set up to help with your pension.

If you work part-time, you’ll be treated exactly the same as someone who works full-time when it comes to pensions. Hooray! The only real difference is that you’ll probably be earning less than someone who works full-time, which means your workplace pension will be smaller. If you earn less than £120 per week, it will also mean you need to make voluntary National Insurance contributions if you want to qualify for the State Pension.

Just bear in mind that even with a workplace pension and a State Pension combined, you might not have enough to live on when you’re older. So, we’d always recommend setting up a personal pension to help top them up. Not only do you not have to pay tax on the earnings you pay into a personal pension, but your money will also get invested so that hopefully, by the time you retire, it will have increased in value.

If that sounds great to you, check out 5* rated PensionBee¹, it's easy to use, low cost and great customer service. You could also check out all the best personal pensions for all the top options.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.