Review contents

PensionBee is one of the most popular pension companies in the UK. They offer an easy to use mobile app (and website) where you can either open a new pension, or transfer existing pensions, and their experts will aim to grow your pension over time. When the time comes to retire, you can withdraw regularly easily too. The customer service is excellent, with a dedicated account manager, and the fees are low. 5 stars from us.

Planning your pension and retirement? PensionBee are a modern option to plan, save and manage your pension – all within an easy to use app, or via their website. (There’s also experts on hand to help whenever you need it too.)

They’re very popular, with over 250,000 customers in the UK, saving over £5 billion in total.

PensionBee’s aim is to make pensions super simple – you don’t really need to know much about pensions or do much yourself. You can either open a brand new pension and start saving, or if you’ve got any old pensions from old jobs lying around, they can hunt these down and move them over to PensionBee for you.

There’s a range of pension plans to choose from (a pension plan is where your money is invested with the aim to grow it over time), all managed by experts, and each plan is suited to different types of people – for instance, ethical investing (like environmentally friendly companies etc.), or those who just want to use their standard plan, or those nearing retirement (amongst others).

They’re all clearly explained and easy to understand, but if you want help, you can get guidance through all the options over the phone.

PensionBee will contribute £50 to your pension when you open a PensionBee account (with Nuts About Money).

The plans are all growing in value very well too (we’ll cover the investment performance below).

And it’s all for one simple annual fee, ranging from 0.50% to 0.95% of your pension pot per year (that’s pretty low cost). And even better – the fee halves on the portion of your savings over £100,000 saved.

If you’re nearing retirement, or already in retirement, you can use PensionBee to manage your pension pot in retirement too – letting your money continue to grow over time, while withdrawing from it as and when you like (e.g. monthly). Or, PensionBee can help you find the right annuity (guaranteed income) for you (more on this below).

PensionBee is also pretty much perfect if you’re self-employed, as you can add money to your pension whenever you like, and even pay in from a limited company to save more tax (more on that later too).

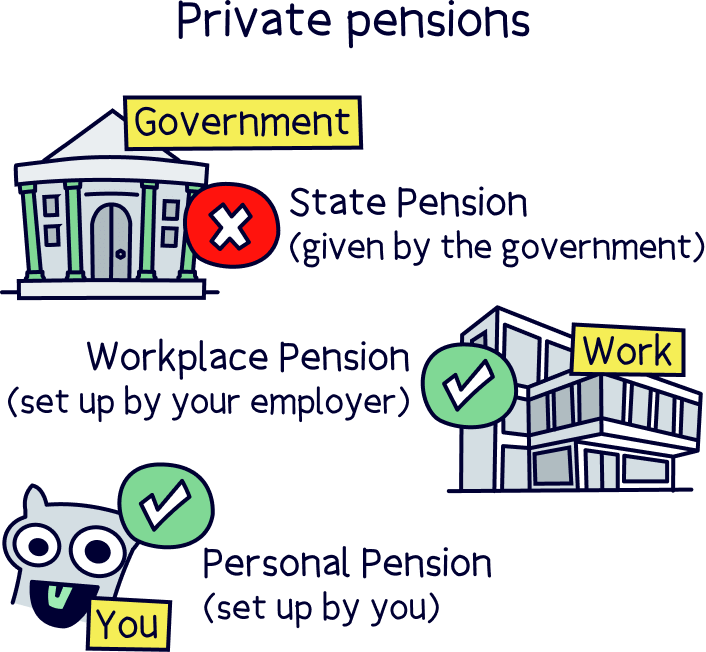

Getting slightly technical, PensionBee is a personal pension, which is a pension you set up yourself, rather than a workplace pension (which is set up by your employer at work). Both are types of private pensions (as they are private to you), so the word private pension is often used for a personal pension.

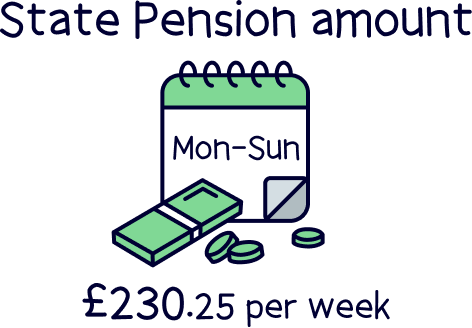

The alternative is the State Pension (the government pension), which you’ll likely get at State Pension age (currently 66), but what you’ll get isn't that much these days (currently £230.25 per week) – which is where private pensions come in, to help build a secure financial future.

We typically recommend most people open and save into a personal pension alongside their workplace pension in order to grow their total pension pot larger – as we’ll all need a very hefty pension pot for a comfortable retirement income these days.

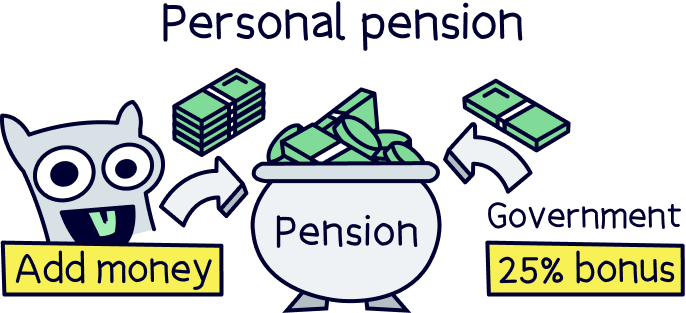

Important: you'll also get a massive 25% bonus from the government on all the money you add to your PensionBee personal pension (and can claim back even more if you pay 40% or 45% tax on your income – more on that later).

The PensionBee app itself is really great, you’ll be able to manage and track your pension whenever you like, all from your phone (actually viewing your total pension balance at any time – pretty cool). Plus there's easy to use tools to plan ahead, and work out how much you might want to be saving for the retirement you want.

The PensionBee app is available on both Apple and Android devices and very highly rated. It’s rated 4.8 out of 5 from 7,000 reviews on the Apple App Store and 4.6 out of 5 from 5,000 reviews on Google Play.

You don’t have to use the app if you don’t want to though – you can use PensionBee on their website too.

Already keen to get started? Head over to the PensionBee website¹ – you’ll also get £50 added to your pension for free (with Nuts About Money).

Want to learn more? Let’s get into the details.

I moved my pension (from my old job) to PensionBee, over 4 years ago, and have been continually saving into it since.

I find the fee very reasonable, and I’m able to manage things myself via their pension plan options, and it was easy to understand them all.

The transfer process was seamless, with a dedicated advisor who sorted everything, and regular updates via the app and over email.

My pension has been growing way faster than I thought, originally within the ‘Fossil Fuel Free’ plan and now the Tracker plan. So far it's grown a lot (although I know there will be ups and downs in future).

I've found the app really easy to use, and it makes managing my pension easier, such as making changes to my regular top ups, and being able to make contributions from my limited company (as I’m self-employed).

Overall, I’ve found it great, and can’t rate it highly enough.

PensionBee’s mission is to make pensions simple for everyone, very similar to our mission here at Nuts About Money, educating people about money in the simplest way possible (we hope some of our articles have already helped you).

They’ve been around for quite a while now, since 2014, and grown in popularity and size since, with 100,000s of customers, looking after billions of pounds. They also sponsor the Premier League football team Brentford.

They’re a big company, with their shares trading on the London Stock Exchange (LSE). That means they have to adhere to strict rules and regulations about how the business is run, and are FCA authorised – more on that later.

PensionBee themselves have a focus on doing business for good, with a strong focus on ESG factors embedded within the business (environment, social and governance). That’s things like becoming net zero (no carbon footprint), hiring a diverse and inclusive workforce, with gender equality, and overall operating in a responsible way.

They’ve won a lot of awards over the years too, for the app itself, but also customer service, and the service overall.

PensionBee is super simple, all you need to do is sign up on their website or app and either start a brand new pension, or transfer over an existing pension. The initial setup only takes a few minutes.

After that, you’ll pick from easy to understand investment options (pension plans), and then it’s all over to their experts – if you've requested a pension transfer they'll handle this, and they will continually manage the investments over time. You just sit back and relax until retirement.

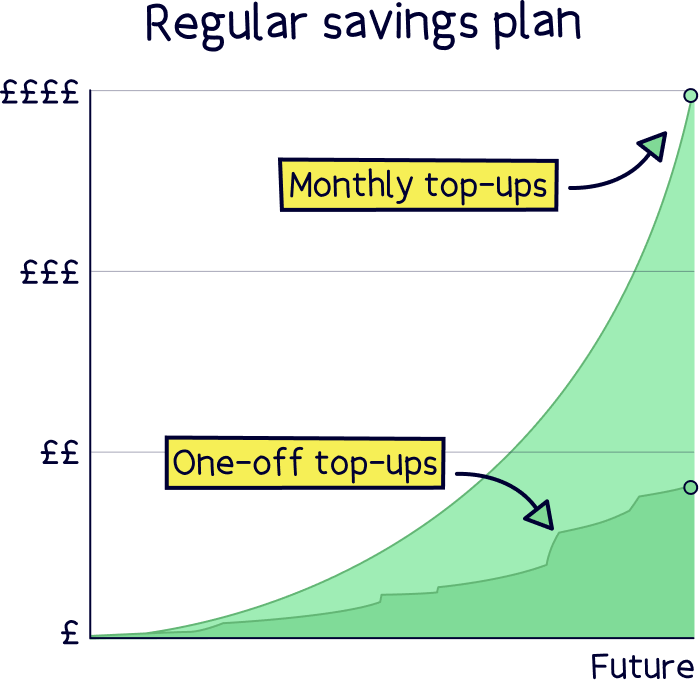

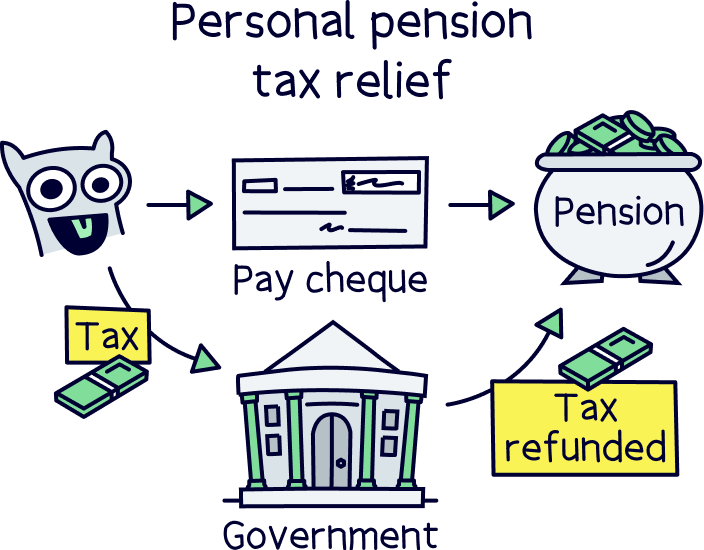

Although saying that, we recommend you keep adding money to it if you can (ideally monthly) – it will really help build your pension pot over time. And everytime you contribute to your pension with PensionBee (and all personal pensions), you’ll get a massive 25% bonus from the government on everything you put in. It's basically free money!

This is technically called tax relief, and is to refund you the tax paid at 20% (basic rate tax) on your income – as saving into a pension is supposed to be tax free. And, if you pay higher rate tax (40%), or additional rate tax (45%), you can claim some tax back at those rates too (on a Self Assessment tax return, TaxScouts¹ can help you with this.).

Conveniently, adding money to PensionBee is super easy, you can either do it as a one-off top up, or a regular top up, all handled within the app itself (or website).

You can start a brand new pension with PensionBee even if you have other pensions and want to keep them where they are. Simply get started on the PensionBee website¹ – you’ll even get £50 added to your pension for free too (with Nuts About Money).

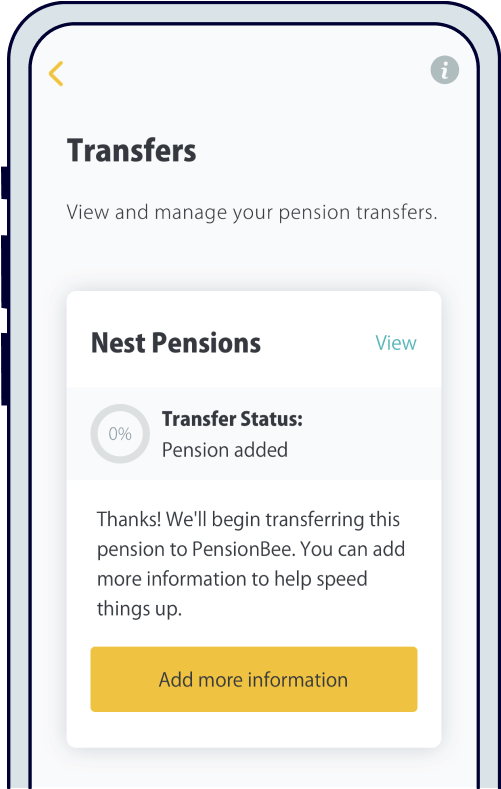

This is where PensionBee is really great, they will take care of pretty much everything when it comes to transferring your pension. All you need to know is your previous pension provider, and sometimes not even that, just where you used to work.

Nuts About Money tip: if you aren’t sure, you can try the government’s pension tracing service.

That really is it. They’ll go out and find your pension and move it over to PensionBee, all for free, and keep you updated on how the transfers are going in the app too (it can take a few weeks, and depending on who the provider is, a bit longer).

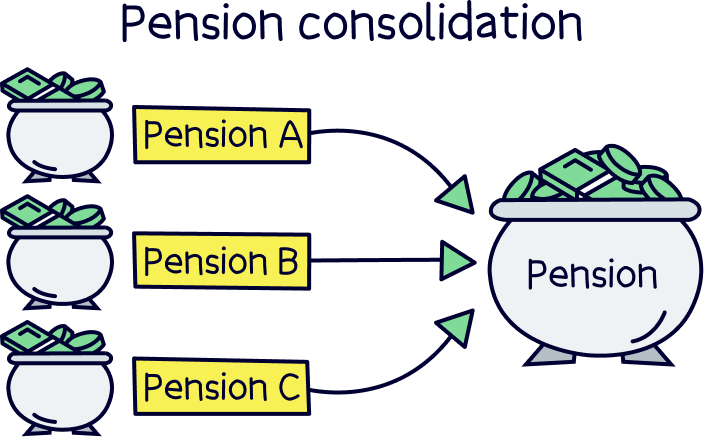

Moving your pensions over is called consolidating your pension, and often a good idea. First, so you don’t lose track of them, and second, you can sometimes benefit from lower fees if they’re all in one place. Plus, you can then decide how you want your money invested (e.g. no fossil fuel companies).

However, you can’t transfer over your current workplace pension (one your current employer set up for you) if you’re still paying into it – you can’t move this anywhere in fact, you have to wait until you get a new, and hopefully better job! But you can always start a new one with PensionBee alongside it.

PensionBee works either as an app on your phone, or you can use their website (or even a bit of both). The app is very easy to use, and very simple – showing you the basics of your pension, without all the jargon and complicated things that typically go along with pensions.

You can see your current pension balance whenever you like, how much you’ve saved, and all of your savings history (such as the government bonuses). And you can also make one-off top ups or change your regular savings plan within the app itself.

You can also change pension plans whenever you like, in just a few clicks (more on those below).

It’s simple, not overcomplicated and works great. You can also contact customer support directly from the app – via phone call or email.

The website is pretty much exactly the same, just on a bigger screen – there’s no extra features, and just as simple.

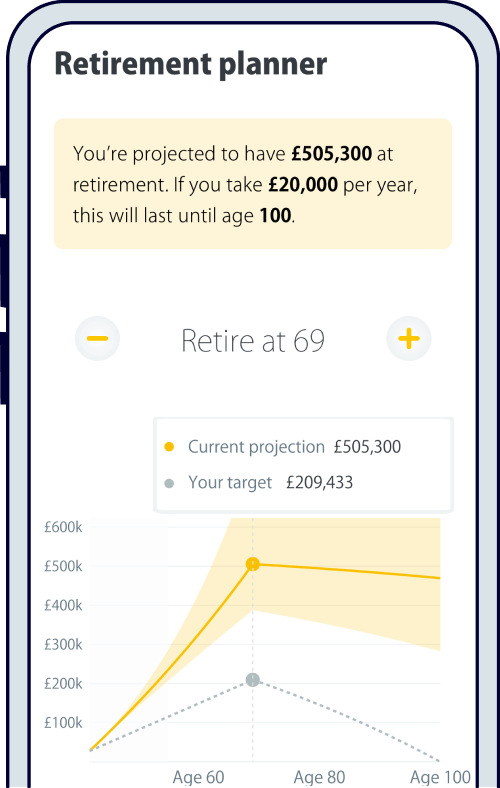

PensionBee also provides a retirement planner tool directly within their app, so you continually check if you’re on track for the retirement you’d like.

It’s pretty useful, and will help you work out how much your pension pot is likely to be, how much you can withdraw per year (your retirement income), and how long it will last (e.g. last until 85 years old) – so you can make changes to get your pension pot growing in the right way for a comfortable retirement.

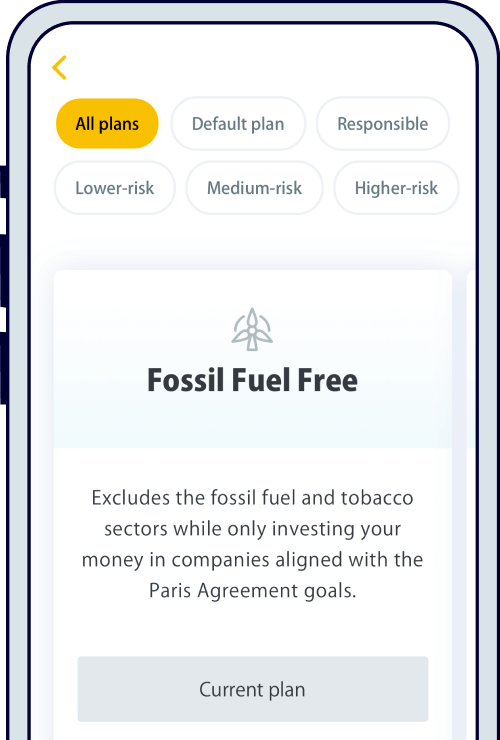

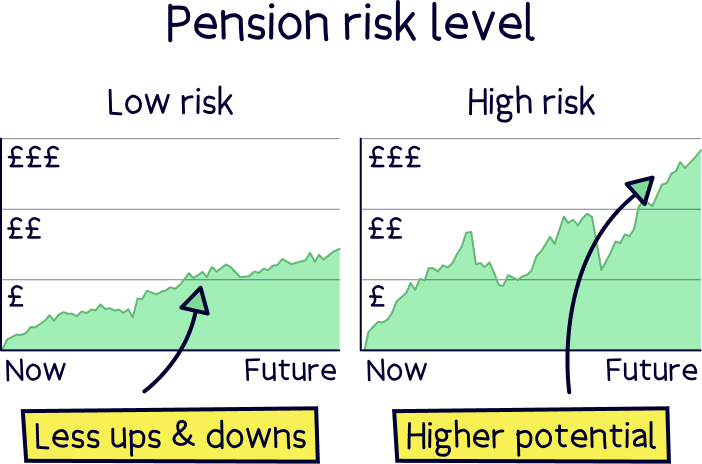

Choosing where to invest your money is super simple and there's a great range of pension plans to choose from. You only need to pick one, and you can change whenever you like too.

The plans are based on how much risk you’d like to take (don’t be put off by the word risk!). The higher the risk, the more ups and downs there will be in the short term, but ultimately should grow more in the long term.

Often the risk level is determined by your age – when you are young(ish), it’s typically completely fine to have a higher risk pension plan, as you’ve got lots of time to ride out the ups and downs of the market, and benefit from higher investment growth in the long term.

If you’re looking to retire in the next few years, a lower risk plan that keeps your money safe (but expected to grow less), would likely be the best option for you.

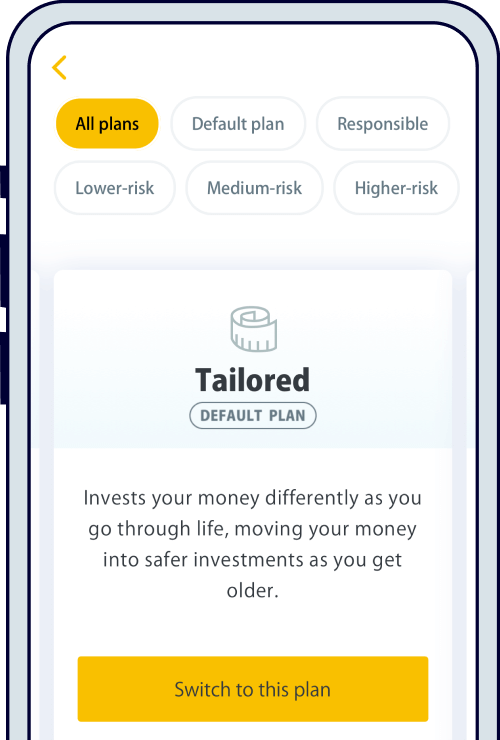

With PensionBee, there’s a default plan for if you’re under 50, and a default plan for if you’re over 50. And, there’s other options too that might suit you, depending on what type of pension plan you prefer.

Overall, it’s a great range of plans. And, with all the plans, your money is in safe hands – the plans are managed by some of the biggest money managers in the world, such as HSBC, Legal & General, State Street Global Advisors and BlackRock.

PensionBee doesn’t provide advice personalised to you (e.g. which plan is best for you), but you can chat to their friendly experts (over the phone or email) who can guide you through all the different options in detail.

But ultimately, it’s your choice which plan to choose. And you can simply pick the default plan and never have to worry about it again.

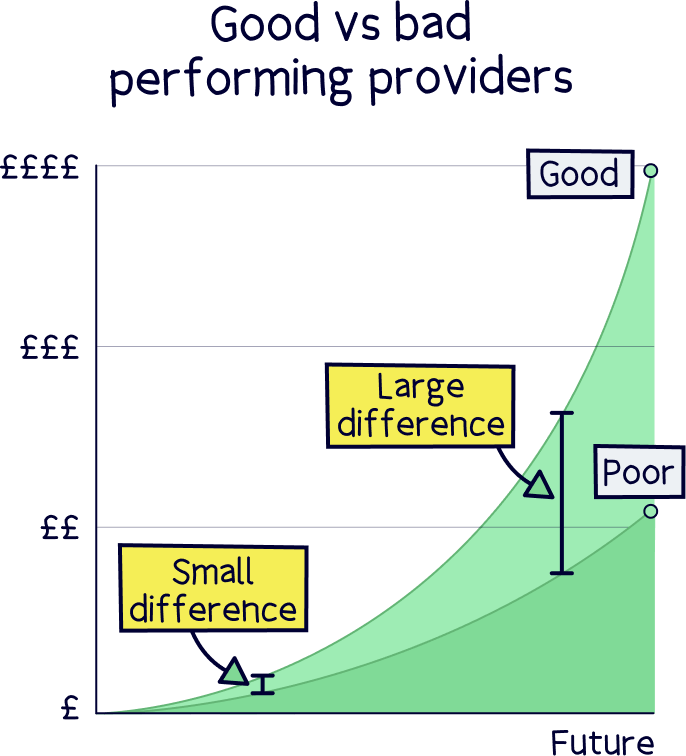

One of the most important factors in saving for retirement is how much it will grow over the years – and there can be a huge difference with how much you’ll retire with depending on where and how your money is invested (e.g. which pension provider and their pension plans).

With PensionBee, they work with some of the largest investment companies in the world, to make sure your money is growing in the best way possible for retirement. Just to recap, they’re HSBC, BlackRock, State Street Global Advisors and L&G.

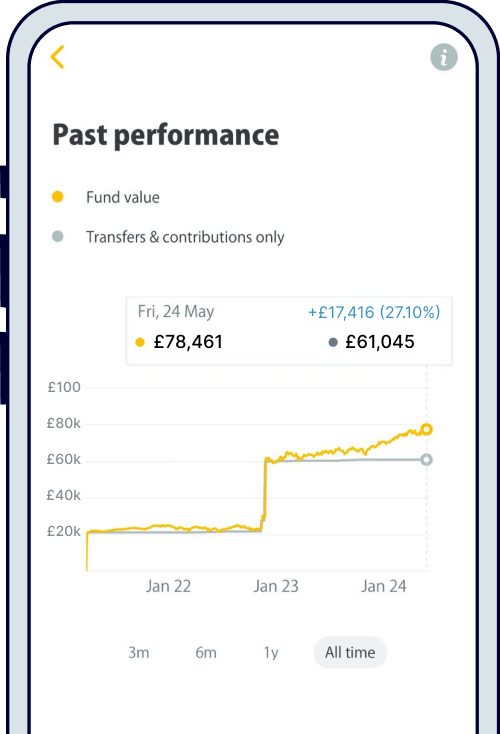

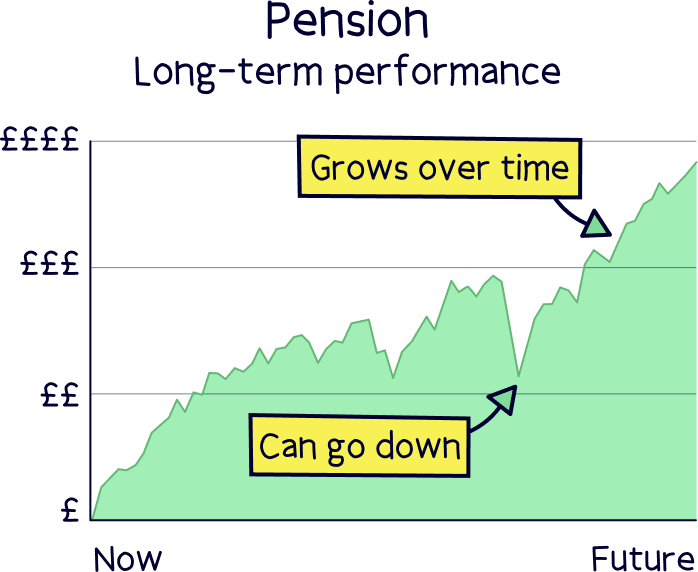

As a personal customer of PensionBee myself, my pension is invested in the Tracker plan, so let’s take a look at the performance over the years.

Overall, that's pretty great, and very typical of pension plans and investing. This plan essentially tracks the world economy, which as an average grows continuously, and is a very popular method of investing.

Note: good (or bad) past performance doesn’t mean it will continue into the future – however pension plans are intended to grow in a sensible way over time, with no drastic ups and downs, it should typically trend upwards.

This is just one pension plan, and you can see there’s ups and downs along the way, but ultimately the aim is to grow significantly over the years – the earlier you get saving into a pension, the bigger your pension will be at retirement.

We won’t run through data comparisons for every pension plan, but here’s the data for 2024 from the other popular plans. We’ll just use one year for now to give an indication.

However, this bit is important – don’t simply pick a pension provider or pension plan based off the biggest increases (wherever your pension or money might be). Pensions aim to build up a big pension pot and often over multiple decades – so you should rarely look at short term performance (e.g. under 5 years). There will always be ups and downs along the way.

Also consider using a provider and plan that is perfect for you, maybe one with a great mobile app, one that’s easy to use, where you can invest ethically, or maybe one where you can get financial advice if you’d like it (among many other options!).

Pensions are often an afterthought if you’re self-employed, probably because you're too busy running a business or helping clients! But PensionBee has thought about you guys too.

You can open a brand new pension for yourself, you just need to add some money, and then you’re away. Add in as much or as little whenever you want to, or set up a regular contribution (e.g. monthly), it’s all entirely up to you.

You’ll get the 25% tax bonus from the government when you transfer money from your bank account too, all super easy (you get this with all personal pensions). And you can claim back any higher rate tax (40%) or additional rate tax (45%) on your Self Assessment tax return.

It gets even better if you run your business through a limited company, you can actually make employer contributions to your PensionBee pension, which means you use your company bank account, and your company actually saves into your pension rather than you personally.

Doing this means your pension contributions count as a business expense, so you can also reduce your Corporation Tax, which can be between 19% - 25%. That’s a big saving, and is on top of money going into your pension tax-free (from the company).

Nuts About Money tip: interested in learning more about pensions for the self-employed? Here’s our guide to self-employed pensions.

If you're ready to get started with PensionBee, sign up here and get £50¹ added to your pension for free (with Nuts About Money).

When it comes to retiring, it’s also super easy to start withdrawing money from your PensionBee pension.

It’s a pretty great feature – being able to manage your retirement income. A lot of pension providers don’t offer the ability to withdraw and manage your retirement income, you typically have to switch providers to one that does, which can come with extra fees, stress and of course admin (but it could be a great idea depending on your circumstances and preferences).

With PensionBee, and all personal pensions, you can start withdrawing cash from your pension at age 55 (57 from 2028) – although we typically recommend you keep it invested for longer until you officially retire, so you have a nice big retirement income when you need it.

There’s 2 options to start taking your pension, the first is ‘drawdown’, which is simply taking money out of your pension whenever you like (e.g. monthly withdrawals as a regular income) – you can even withdraw 25% completely tax-free too, and as a lump sum (all in one go).

With a ‘drawdown' pension, your money left within your pension can keep growing, and you could switch to a lower risk plan with PensionBee that provides a more regular income (so no big ups and downs).

The second retirement option is to exchange your pension for an ‘annuity’, which gives you an income for the rest of your life. PensionBee partner with Legal & General to offer this option, and they’ll handle everything for you. Although you can choose an annuity from wherever you like when you retire, it doesn’t have to be with PensionBee.

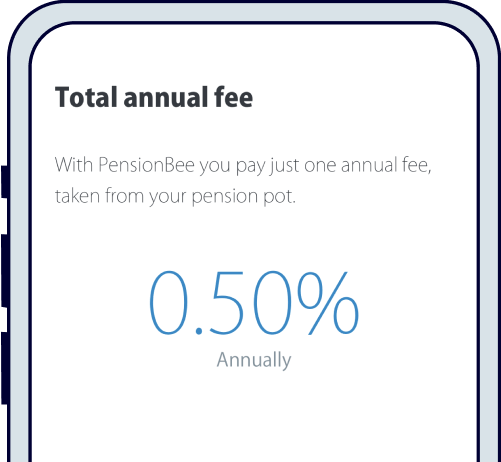

Overall PensionBee is low cost, with one simple annual fee. There’s no fees for opening a pension, moving or consolidating your existing pensions into PensionBee.

The only fee you’ll pay is one, low annual fee depending on which fund you choose. And this ranges from 0.50% to 0.95%, which is deducted from your pension automatically, so you don’t need to worry about actually paying it.

And better yet, if your pension is over £100,000, the fees halve for any money above that. Not too bad at all.

For comparison, with a financial advisor, you’ll be looking at around 2.14% per year on average (FCA research), for them to manage your pension for you (and other investments if you have them). But you can find lots of great advisors for less than that (if you do want personal advice).

You can find some pension options around 0.25% per year, which is pretty great, but these are often managing your pension yourself – for instance deciding the investment strategy, and buying and selling investments. However, there are often fees to buy the investments (trading fees), and fees within the investments themselves, which can range from around 0.20% - 1.5%+, depending on how you want to invest, so there’s not a huge amount of difference in it.

Note: we don’t typically recommend making your own investments with a pension unless you’re an experienced investor. If you are, check out the best SIPPs (self-invested personal pension).

So, overall, it’s one of the cheapest options out there to have experts manage your pension for you, and it’s just one simple annual fee.

And, if you ever wanted to move your money away from PensionBee, it’s easy to do too, whenever you like, for free.

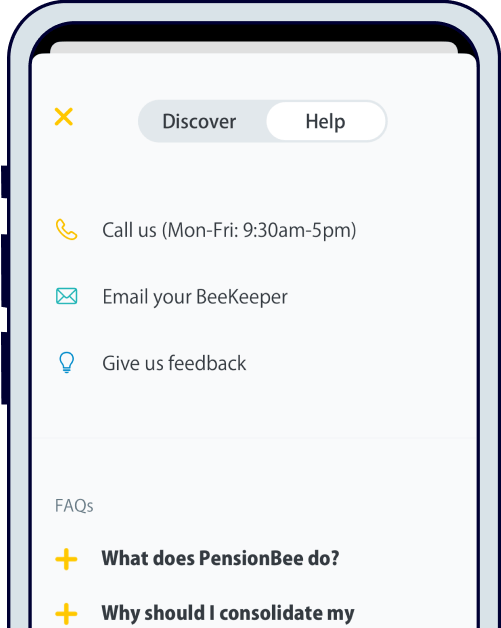

The customer service is excellent.

When you sign up, you'll be given a dedicated account manager (called a BeeKeeper), who will be there to help you with anything you need. They'll also move your pensions over from your other providers if you want to.

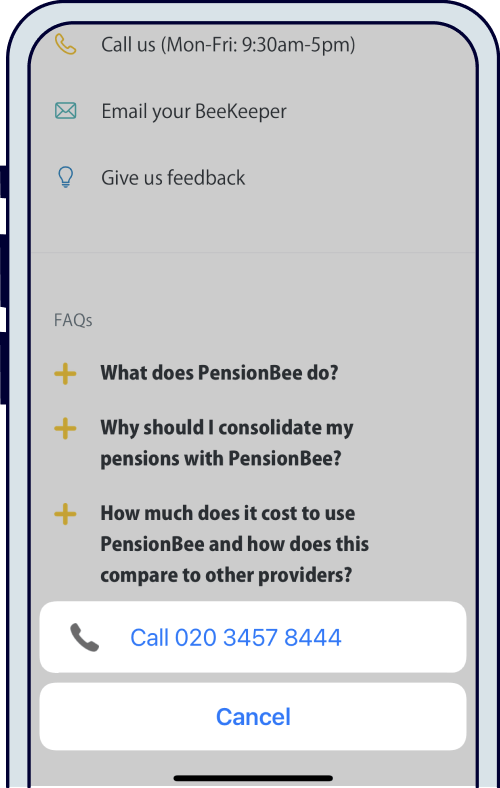

In addition to that, there's an additional customer support team (real people to chat to) on the phone whenever you need them (in the UK too), well Monday - Friday 9:30am to 5pm.

Or if you prefer you can email in, and normally your BeeKeeper will get back to you shortly.

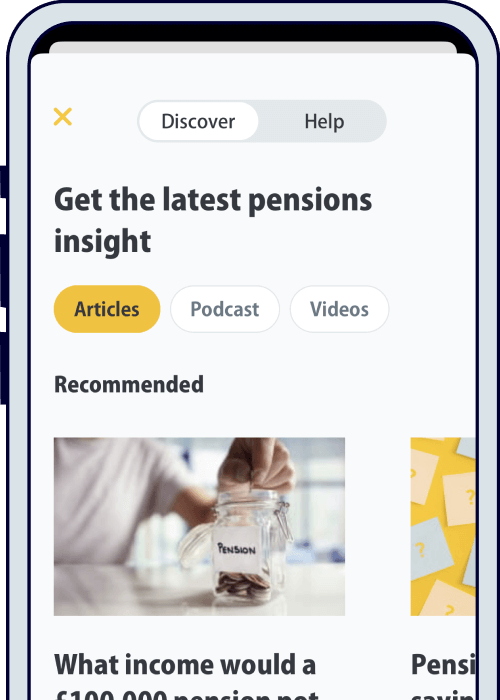

There's also an online help centre with answers to pretty much any question you might have about PensionBee or pensions in general. It's really great. They even do a podcast with talks about lots of pension topics in a helpful and educational way.

Don’t worry, your money is completely safe.

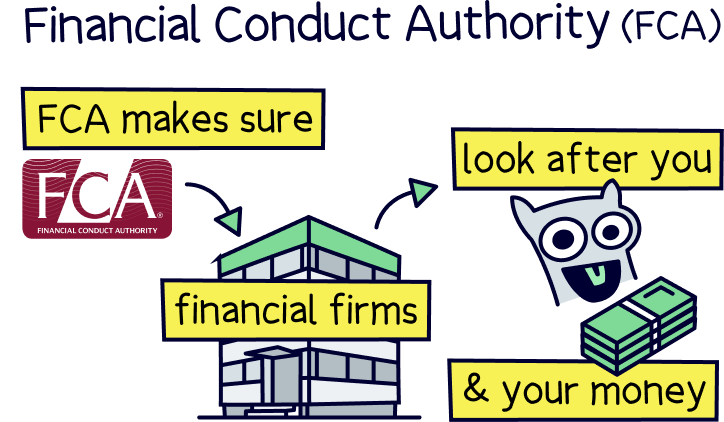

PensionBee has been approved to look after your money by the Financial Conduct Authority (FCA), and is regularly reviewed.

PensionBee is also a large company that trades on the London Stock Exchange, meaning it has very strict standards for how the business is run and how its finances are managed.

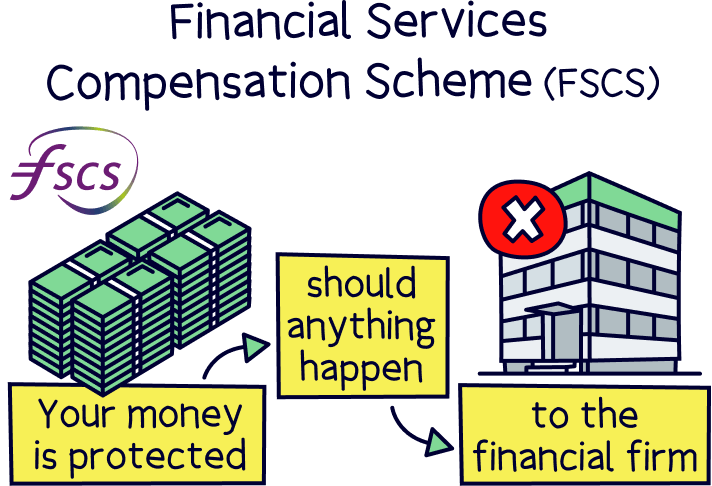

Your money is also protected under the Financial Services Compensation Scheme (FSCS), so if your pension provider, or bank holding your money, were to go out of business, and any of your money wasn’t returned to you, they would step in and provide compensation.

However, that is very unlikely to happen, as when you invest in a pension, your money is invested into funds (the pension plans described above), and these are held with very large financial companies and banks (such as HSBC), all in your name, and they can only be returned to you – your pension provider cannot access any of your money themselves.

As part of this structure with PensionBee, 100% of your money is protected and covered by the FSCS scheme, there is no upper limit (sometimes it can be £85,000 with SIPP providers and different types of investments).

The value of these funds change over time depending on how well the economy and investments are performing. So although they almost always trend higher over time (and that's how your pension grows), they can sometimes drop in value in the short-term, and therefore your balance may show less than what you invested.

This isn't too much of a problem for pensions or any long-term saving plans, as over the long-term, which is many years for a pension, the result is a very large gain!

Don't let doubts put you off. Saving and investing in a pension is typically the best way to save for a comfortable and happy retirement.

Here's a quick recap and the pros and cons of PensionBee:

PensionBee has got an excellent rating on the popular reviews website, Trustpilot, with a score of 4.6 from over 11,800 reviews. And for a company in financial services where customer service isn't normally that great, this rating is awesome.

Most of the reviews mention how easy the app and website is to use, and the low fees, and that their pension is growing nicely over time – and we can vouch for all of that.

A company that’s made pensions super simple, has low fees, and a great choice of pension plans – plus awesome customer service. What’s not to love?!

PensionBee offers a good app (and website) to manage your pension, and give you up-to-date information on your pension whenever you want it, with the experts looking after the investments.

If you’ve got existing pensions, they do all the hard work to move your existing pensions over, and for free.

Or, simply start a new pension if you don’t have any pensions to transfer – it’s a great idea to boost your pension pot alongside a pension from work (or if you’re self-employed). Plus, you’ll automatically get a 25% government bonus every time you add more cash (and claim back more tax if you’re a higher earner).

The pension plans themselves are easy to understand, and offer a great range to suit pretty much everyone, whatever stage of life you’re at (including after retiring), and your personal preferences (such as ethical investing).

The plans are growing well over time too – as good as you could possibly hope for really. All managed by experts, and with large financial companies who know what they’re doing.

The fees are low too – one simple annual fee, ranging from 0.50% to 0.95% per year, depending on your pension plan, and these reduce by half if you have over £100,000 saved.

As a summary, PensionBee puts you back in control of your pension – allowing you to have your pension savings all in one place, making it easy to view and manage, and for one simple annual fee.

We’re not sure what else you could ask for from a pension company to be honest. It’s great. It’s a big 5 stars from us.

If you’re keen to get started, or learn more, head over to the PensionBee website¹ – you'll also get £50 for free too, with Nuts About Money.

PensionBee will contribute £50 to your pension when you open a PensionBee account (with Nuts About Money).

PensionBee will contribute £50 to your pension when you open a PensionBee account (with Nuts About Money).

PensionBee will contribute £50 to your pension when you open a PensionBee account (with Nuts About Money).

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things money, with years of combined experience working in the finance industry and writing about money. We understand the ins and outs, how to get the best deals, save money, and how to communicate money in an easy to understand way (we hope you agree).

More than 20 years of combined experience researching and writing about money

Researched and reviewed a wide range of financial services companies, and have a transparent review process

We follow a strict editorial code to ensure you get the best information possible

PensionBee will contribute £50 to your pension when you open a PensionBee account (with Nuts About Money).