Article contents

The best sharia-compliant pension overall is PensionBee. You can leave it to the experts with their great sharia pension plan option, it’s easy to use, has low fees and great service. If you want to make your own investment decisions, check out AJ Bell and Interactive Investor, they’ve both got great sharia-compliant investment options, and are low cost.

Looking to save for your future in a sharia-compliant way? You're in the right place.

Note: sharia-compliant pensions (and investing) can also be called halal pensions (and halal investing).

We’ve reviewed a wide range of personal pensions that offer a sharia compliant pension plan. A personal pension is one you can set up yourself (online in minutes) to help boost your overall pension pot, and you can even transfer over any old pensions from old jobs too.

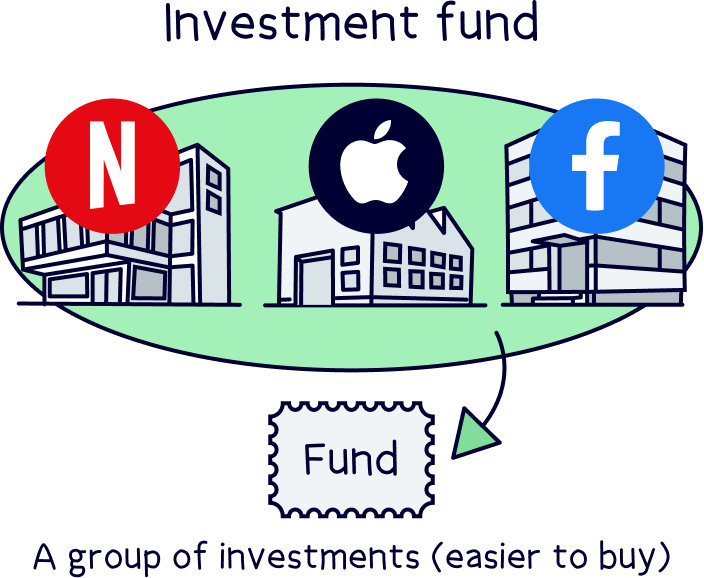

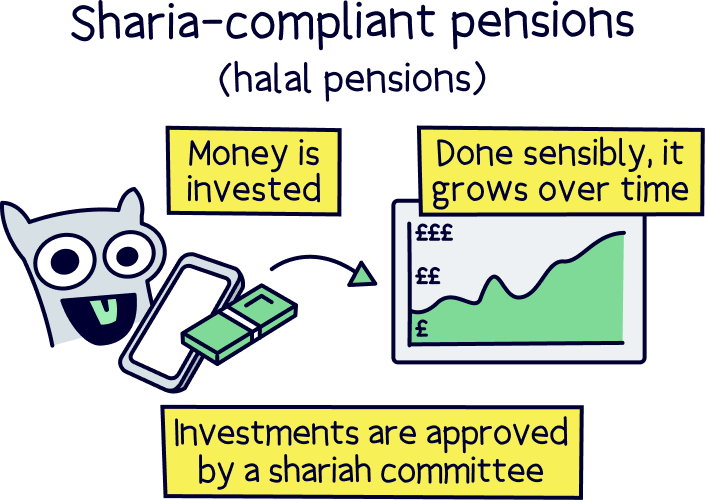

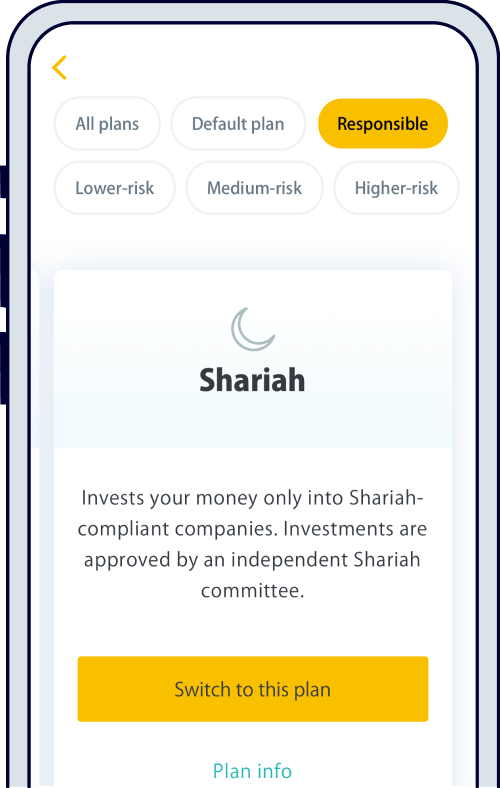

With a sharia pension plan, your money will be invested in a fund (a group of investments) that only invests in sharia compliant investments.

We’ll cover all the details below, but without further ado, here’s they are:

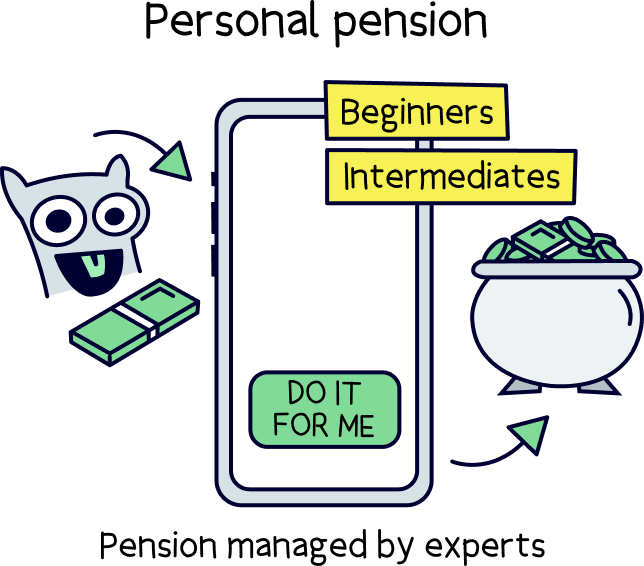

No expertise needed, just select the sharia plan and you’re all set.

PensionBee tops the list – it’s got a great sharia-compliant pension plan, it’s easy to use, and it’s low cost. Plus the service is excellent.

Get £50 added to your pension

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

PensionBee tops the list – it’s got a great sharia-compliant pension plan, it’s easy to use, and it’s low cost. Plus the service is excellent.

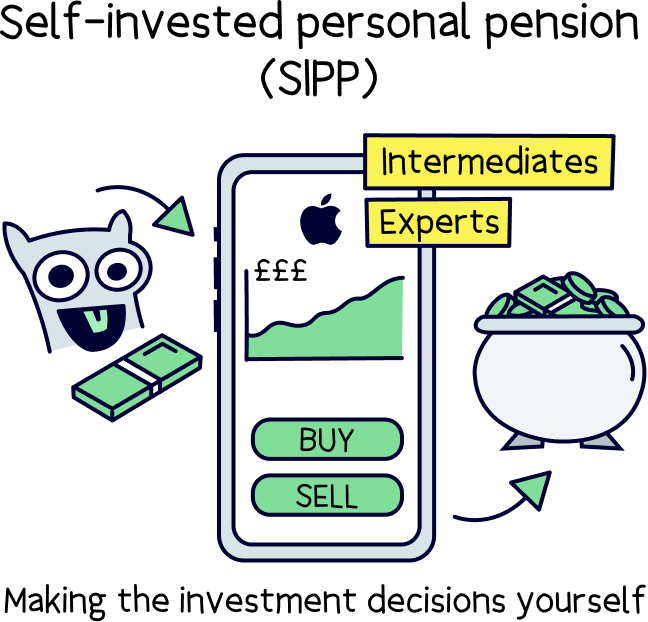

Pick from a range of different Islamic funds within your account (best for those more experienced).

Offers available

Interactive Investor is a well established company, and very popular.

Instead of paying a percentage of the investments in your account (like other investment companies), you’ll instead pay a fixed fee per month – and it’s pretty low, starting at just £5.99 per month for a pension (SIPP).

This makes it one of the cheapest SIPP providers out there, especially if you have a fairly sizeable amount within your pension (e.g. over £30,000).

On top of that, there’s a huge range of investment options (e.g. shares and funds) – one of the largest.

It's easy to use, and the website and app are great. The customer service is excellent too.

A great choice overall.

AJ Bell is well established, with a good reputation.

It's one of the cheapest SIPPs out there (charging a low annual fee).

There's a huge range of investment options – pretty much every investment out there (including both funds and shares).

The customer service is excellent too.

Overall, it's one of the best options for a SIPP.

PensionBee tops the list – it’s got a great sharia-compliant pension plan, it’s easy to use, and it’s low cost. Plus the service is excellent.

Saving for your retirement is incredibly important. If you can save regularly (ideally weekly or monthly), it will really add up to a big pension pot over the years, all ready for a nice comfortable income in retirement.

Picking the right pension provider for you is super important too, luckily we’ve reviewed a wide range of pension providers to find the best.

Here, we’re covering the best shariah-compliant pensions, so you can be confident that whichever one you choose, you’ll be using one of the best options in the UK.

To find the best, we looked at:

We’ve looked at the best expert-managed pension providers (where the experts handle things), and the best self-managed pension providers, where you’ll pick and choose the investments you’d like to make – often called a self-invested personal pension (SIPP).

We’ll also cover everything you need to know about pensions and sharia pensions (halal pensions) below, but first let’s just run through the details of expert-managed sharia pensions and self-managed sharia pensions, so you know which one is right for you.

This is our recommended option for most people, simply let all your pension worries disappear. Let the experts handle things for you – they’ll ensure all investments adhere to Islamic principles, and will aim to grow your money over time.

All you need to do is add money (ideally regularly), and they’ll take care of the rest until you’re ready to retire.

The best provider we recommend is PensionBee¹ – it’s easy to use, low cost, and has a great track record of growing pensions over time, and of course, a great sharia pension plan. You’ll also get £50 added to your pension for free if you sign up with Nuts About Money.

Note: if you are self-employed, you’ll also be able to use this as your pension, and pay in from your business bank account.

The alternative is making your own investment decisions within a self-invested personal pension (SIPP). If you have a bit of experience in investing, you might want to do this, but if you prefer a more hands-off approach, you could simply opt for the expert-managed option too.

Anyway, you’ll need to sign up to an investment platform. Our recommendations are AJ Bell¹, and Interactive Investor¹, as they have a good range of sharia-compliant investments.

Once you’re set up, you’ll need to search on the platform (app or website) to find sharia investments – these typically come in the form of a fund, which is a group of investments put together and managed by an expert, often with a certain goal for the fund, such as long-term growth, or regular income.

Some popular sharia-compliant funds you can find are:

Anyway, we won’t cover them all, you get the idea. For those even more experienced, you can of course buy individual shares in companies or other socially responsible funds, that you know are shariah-compliant – AJ Bell¹ and Interactive Investor¹ both have a huge range of investment options.

Let’s rewind for a second, what actually is a sharia pension, and why is it different?

With pensions, your money is invested with the aim of growing it over time – that can mean buying shares in companies, buying investment funds (often groups of shares), and things like bonds, which are effectively loans to governments, and large corporations.

Well, if you’re part of the Islamic faith (a muslim), there are some rules when it comes to investing (and lending and borrowing money), which is part of Sharia law.

A key one being that you are not allowed to earn interest from lending money (called riba). Shariah-compliant savings accounts earn an expected profit rate, rather than interest, which is profit from business activities (trade) rather than lending.

And, there are certain industries that you aren’t allowed to invest in, which are:

Note: these can also be called haram industries.

The whole category is called Islamic finance, and anything that doesn’t fit the rules is called non-Islamic finance. Islamic finance has a set of 3 key principles, which are ethical investing, no interest and transparency.

Ethical investing effectively means avoiding investments in certain industries (like this above), and some ethical investment options will aim to invest in things that have a positive impact on the world (such as green energy). This can also be called socially responsible investing.

Some shariah-compliant pensions (halal pensions) will allow a small percentage of income to come from large companies that have operations across multiple business areas, where some could be non-compliant (for instance 5%) – and this is typically donated to community charities.

No interest means that no interest can be either paid, or received, from an investment (e.g. a loan). The idea is interest creates inequalities in the community (e.g. rich getting richer). Instead, money is made from profits from business operations and investments, rather than interest itself – and is measured by a ‘profit rate’.

This relates to transparency in financial contracts and agreements. Essentially, they should be clear, simple and easy to understand, jargon-free and shouldn’t contain anything that might cause issues in the future.

Typically, for shariah pensions, and all shariah investment plans and funds, the investments will be reviewed and approved by an independent shariah committee – which is a group of knowledgeable experts, who can assess if an investment is shariah-compliant or not.

There are a few types of pensions in the UK, there’s the State Pension and there’s private pensions, which consist of workplace pensions and personal pensions…

We’ll cover all those below, but just to jump ahead first, we’re looking at personal pensions as part of this page, which is a pension you set up yourself (rather than your employer), so you can pick a shariah-compliant pension, and decide how much, and when to contribute to it – and they’re a great way of boosting your pension pot overall.

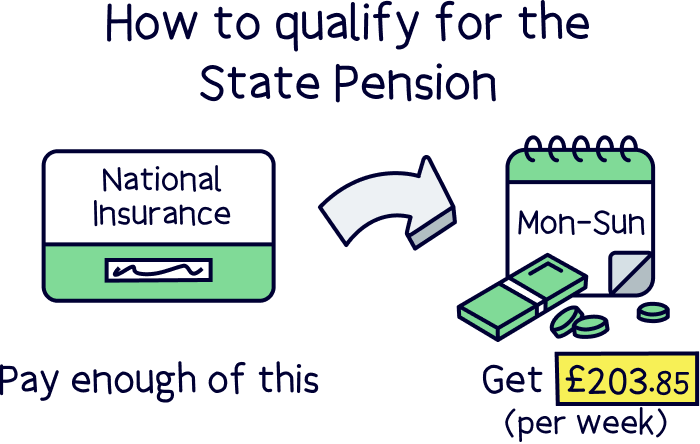

This is the pension you’ll get from the Government when you reach retirement age, which is currently 66 years old – that’s as long as you make at least 10 years worth of National Insurance contributions, and 35 years to get the full amount.

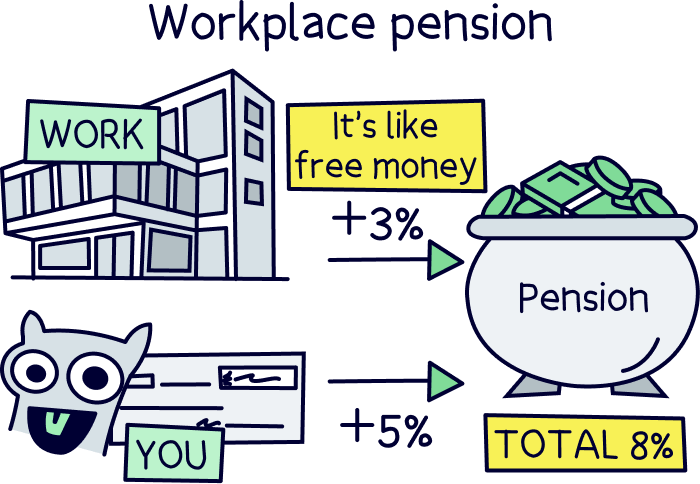

A workplace pension is a pension you’ll get from your job (if you’re employed), your employer will set it up for you, and you’ll have to ‘opt-out’ if you don’t want it. They’ve got an amazing benefit though, if you save 5% of your annual salary into each year, by law, your employer must add 3% – so it’s like a payrise!

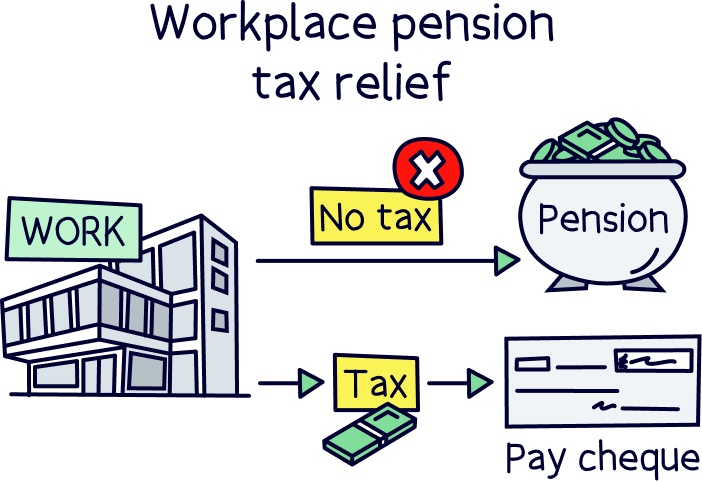

Your money will grow tax-free too – meaning money is transferred to your pension before you pay tax on your salary. You might pay tax when you retire and start withdrawing from it – it depends on your income at the time.

You can start withdrawing from it at age 55 (57 from 2028) if you want to.

The downside to workplace pensions is that your employer will pick the pension provider, which is often just any old one to get the box ticked, rather than assessing if it’s the right one for you – in this instance, a shariah-compliant pension.

However, you may find shariah-compliant pension plans with your workplace pension provider (such as with Nest pensions – the Government owned workplace pension scheme).

A personal pension is a pension you can easily set up yourself, and you get to pick the pension provider, and pension plan you’d like. Personal pensions are a great way to help boost your pension savings, either in addition to a workplace pension, or if you’re self-employed, as your only option (but a great one).

Nuts About Money tip: if you are self-employed, check out our guide to the best self-employed pensions.

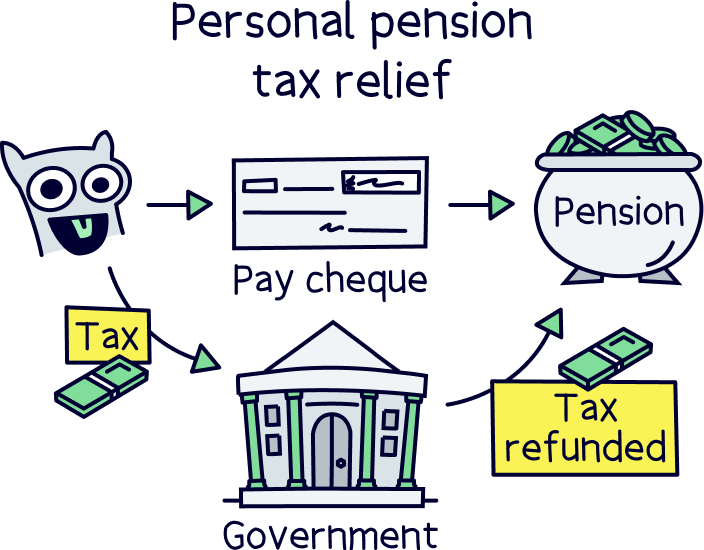

When you save into a personal pension, you’ll get a massive 25% bonus from the Government, on all of your contributions – which is to refund the tax paid on your income (as you’ll pay into a personal pension from your bank account after you’ve paid tax on your salary).

Plus, your money will grow tax-free, just like a workplace pension, so it can grow much bigger over time. However, you might pay tax when it comes to withdrawing it, although the first 25% is completely fax-free – and you can take this as a tax-free lump sum if you like.

You can also start withdrawing your money from age 55 (57 from 2028) if you want to.

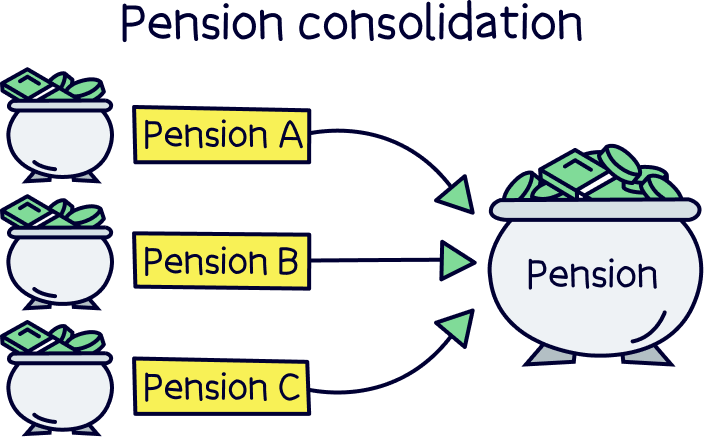

You can also move any of your old pensions (such as from old jobs) over to your personal pension too, called consolidating your pension.

It’s often a good idea to keep them all together so you don’t forget where they are when it's time to retire (which happens more than you think!). And, you can potentially benefit from lower fees, and of course, use the provider you’d like to use, such as one that’s easy to use, and have shariah-compliant plans (such as PensionBee¹ for all of those reasons).

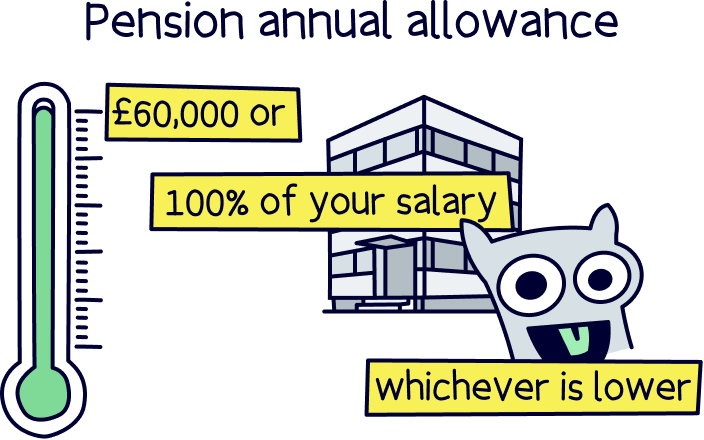

By the way, there are some limits when it comes to saving in a pension – the main one is that you can only save as much as your annual income (e.g. your salary), or up to £60,000, whichever is lower.

This applies as a total on all your private pensions, so your workplace pension, and personal pension (if you have one), and includes that 25% government bonus.

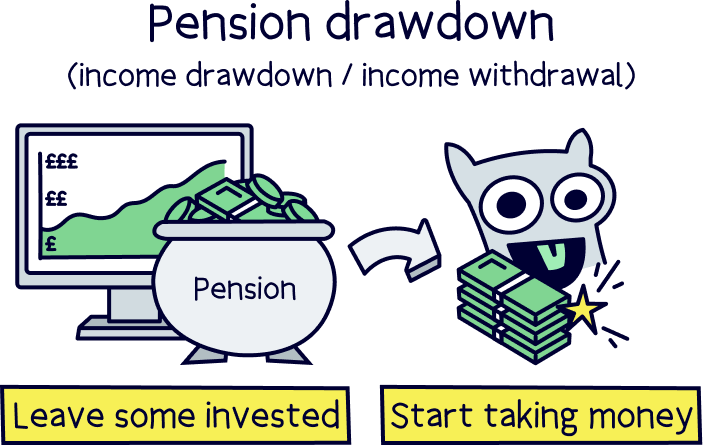

If you’re nearing retirement, getting a few (or a lot) of grey hairs nearing 55 years old, then you might be thinking about withdrawing some of your money from your pension – this is called pension drawdown.

You can still keep your money invested in a pension, so it can keep growing over time, but withdraw from it as and when you’d like.

Note: typically, when withdrawing money from your pension, the amount you can save each year reduces to £10,000. This is called the Money Purchase Annual Allowance (MPAA).

With that in mind, the best pension drawdown provider for a shariah-compliant pension, again is PensionBee¹ – that’s because they offer drawdown (not many do), and also offer a great shariah pension (again, not many do), and it’s easy to use and low cost. Can you tell we're big fans?!

If you’re making your own investments within a self-invested personal pension, our two recommended pension providers, AJ Bell¹, and Interactive Investor¹, also offer drawdown, and shariah pension plans, and they’re low cost too.

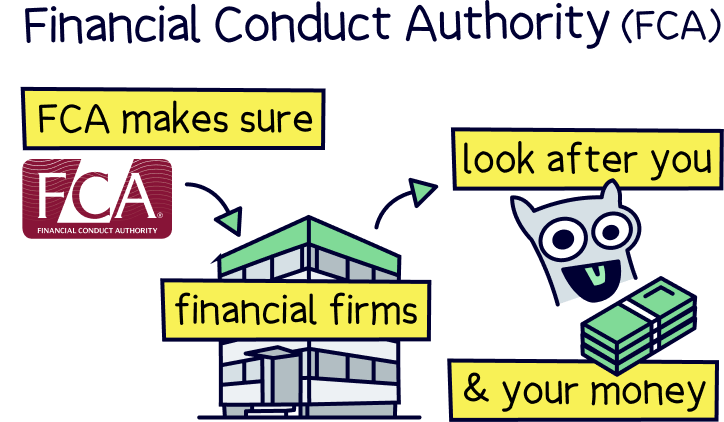

Yep, it’s perfectly safe to invest within a personal pension – all pensions are regulated and authorised by the Financial Conduct Authority (FCA), they’re the people who make sure your money and investments are being looked after.

If you’re unsure about a pension company, check the FCA register to see if they’ve been authorised.

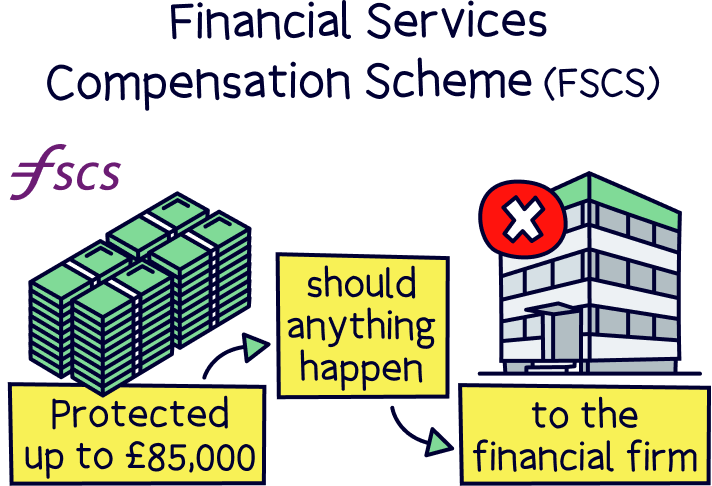

That also means you’re protected by the Financial Services Compensation Scheme (FSCS), which means you’ll be compensated by up to £85,000 should anything happen to your pension provider, and they were holding your cash.

The investments themselves are held separately with large banks and financial institutions, all in your name, separate to your pension provider, so if anything were to happen to your provider, your investments can only be returned to you (or transferred to another provider).

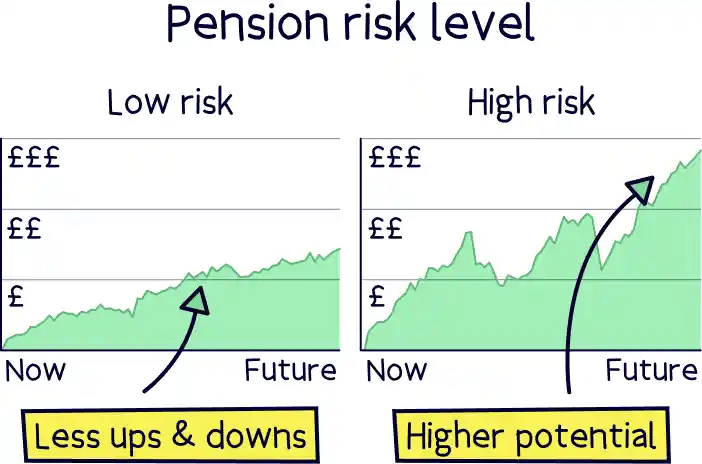

However, that doesn’t mean you can’t lose money, your investments could still go down in value – but over the long term, they should typically rise significantly in value, ready for a comfortable retirement (provided you are investing sensibly – it’s often a good idea to use an expert).

There we have it for the best shariah pensions (halal pensions for muslims). Not as complicated as you first thought?

To recap, you’ve got two main options, you could simply let the experts handle things, or make your own investment decisions.

Letting the experts handle things is highly recommended – they’ll aim to grow your money over time, with investments adhering to the Islamic principles, you just put your feet up and watch your money grow.

The best expert-managed sharia pension is PensionBee¹, it’s easy to use, low cost and has a great sharia plan. You’ll also get £50 added to your pension for free with Nuts About Money.

If you’re keen to make your own investments, check out AJ Bell¹, and Interactive Investor¹, they’ve both got a wide range of sharia investment funds, and a wide range of individual stocks and shares – plus they’re low cost.

There we have it. All the best growing your pension!

PensionBee tops the list – it’s got a great sharia-compliant pension plan, it’s easy to use, and it’s low cost. Plus the service is excellent.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

PensionBee tops the list – it’s got a great sharia-compliant pension plan, it’s easy to use, and it’s low cost. Plus the service is excellent.