Review contents

Nest is a workplace pension set up by the Government. It’s a simple option for employers to use to make sure their employees have a pension, but overall it’s pretty outdated compared to modern pension providers. If you’re looking to transfer an old pension to Nest, it’s not often a good idea (explained below), and if you’re looking to open a new pension outside of work, or are self-employed, you can’t use Nest, but there’s better options anyway (covered below too).

The National Employment Savings Trust pension, or ‘Nest’ to most people, is a pension provider set up by the Government back in 2010, when the Government made some changes to do with pensions…

They made it so that (almost) everyone is automatically enrolled (entered) into a pension scheme while they’re working, and automatically entered into a pension scheme when they start a new job (called auto-enrolment – you can opt out if you don't want the pension).

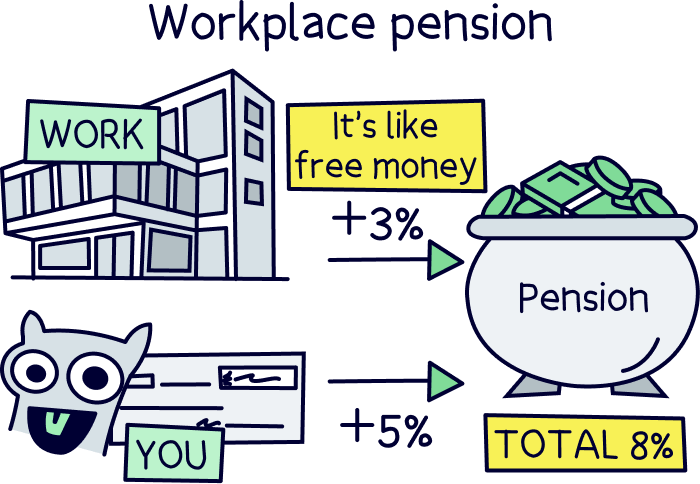

This new scheme also came with some great benefits for pensions, where your employer would have to pay in an additional 3% of your salary themselves, if you paid in 5% of your salary, so it’s like a payrise!

Nest was created at the same time as this scheme, so every employer always had an easy option for a pension provider for their employees (the employer gets to pick which pension provider to use). It’s essentially owned by the Government (technically a public corporation).

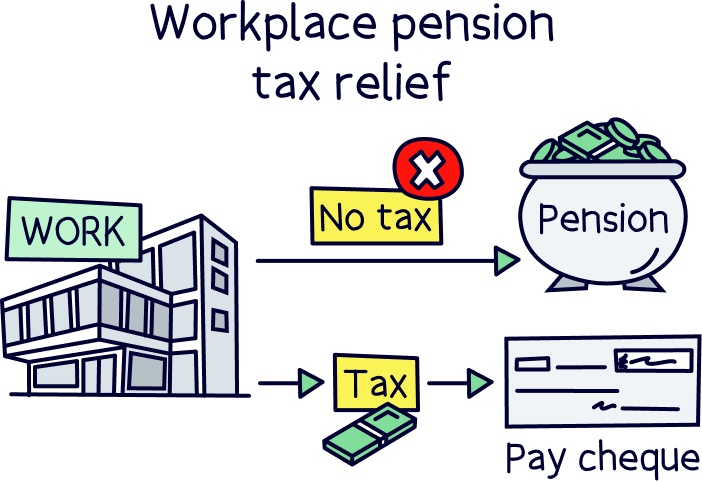

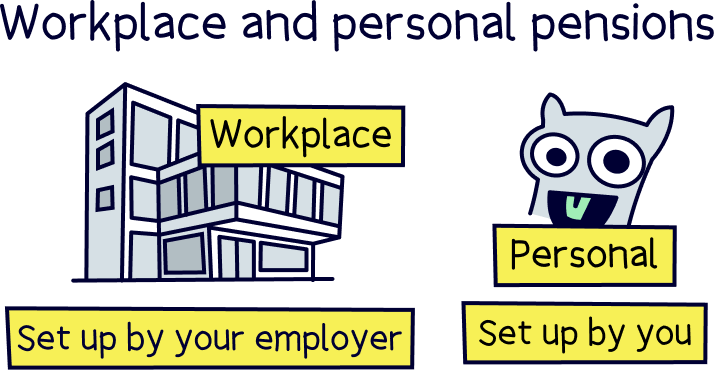

A pension with your employer is called a workplace pension, and the main benefits are that 3% bonus from your employer, money comes out of your salary before tax, and your money will grow tax-free.

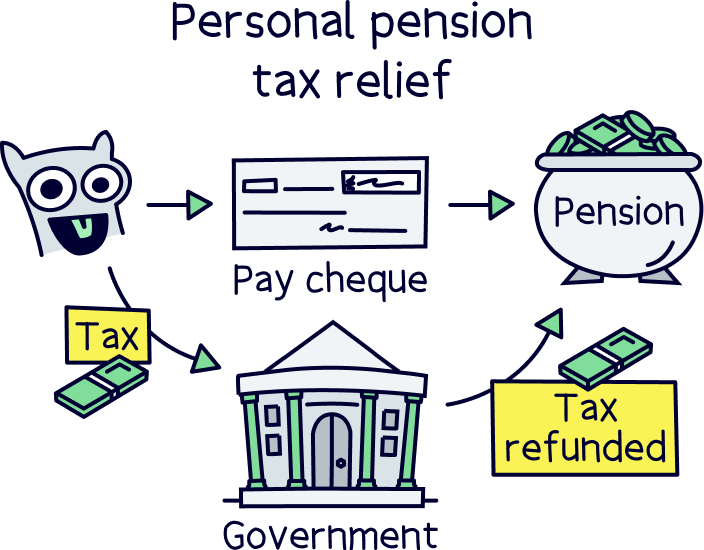

The main alternative is a personal pension, which you set up yourself, and has some great benefits too, such as being able to save tax-free (tax you’ve already paid on your income will be refunded by the Government), and your money growing tax-free too.

With that in mind, Nest is intended for workplace pensions, so pensions arranged by your employer, rather than a pension you can set up yourself (a personal pension).

If you are looking to set a pension up yourself, or are considering moving an old pension to Nest (perhaps because you’ve started a new job)....

You can’t open a brand new pension with Nest, only employers can do it, and it’s not typically the best idea to move old pensions to your current workplace pension – we’ll cover that below.

If you’re looking to transfer any old pensions to Nest, you can do it, but there are some big drawbacks, your pension will then be stuck with Nest until you change jobs in future. We’ll cover this in detail just below too.

Overall, for new pensions, and pension transfers, we recommend checking out PensionBee¹ – it’s a great personal pension, low cost and has a great record of growing pensions over time (you’ll also get £50 for free when you sign up with Nuts About Money). Here’s our PensionBee review to learn more.

Beach¹ is also really great, they don’t just cater for pensions, they have an easy access account too (a tax-free ISA), plus the app is easy to use and the customer service is excellent.

For all the top options check out the best personal pensions.

Anyway, keen to learn more about Nest? Let’s dive in.

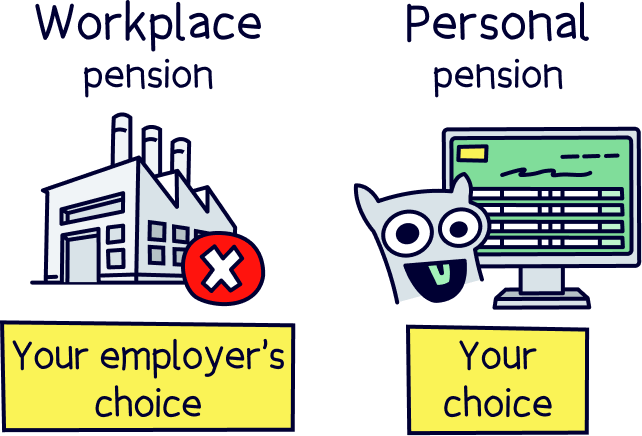

Nest is a workplace pension, which is a pension you’ll get if you’re employed – and by law most companies need to offer most of their employees a workplace pension.

That means you don’t actually get a choice which pension provider you’ll be using – that’s all up to your employer.

Your pension contributions will be taken directly out of your pay each month, and added straight into your Nest pension. You’ll get to decide how much you want to save, and typically if you save 5% of your salary, your employer will add 3% in (by law this is the minimum).

Sometimes, if you have a very nice employer, they might add more in, if you add more in too – this is basically free cash! Often a great idea to do if you have this option.

Other than that, it’s all fairly straightforward, your pension should grow over time, building up your pension pot ready for retirement.

Nuts About Money tip: these days, you’ll need quite a bit for a comfortable retirement – you likely aren’t saving enough! Sorry to put a downer on things. Here’s our guide to how much you should be paying into your pension.

PensionBee is easy to use, low cost, and a great track record of growing pensions.

Let’s just be honest, no, Nest isn’t great if you’re self-employed, it’s intended for people who are employed, and want a workplace pension.

However, if you run a limited company as self-employed, and are the only director, with no employees (so essentially a freelancer with a limited company), you can technically open a Nest pension.

That’s confusing isn’t it? Anyway, if you are self-employed, the world’s your oyster when it comes to pensions…

All you need to do is open a personal pension, rather than a workplace pension – and there’s lots out there – check out the best private pensions for self-employed people to see all the top options.

Now, if you’ve got a Nest pension already, you do have the option to transfer over any other old pensions you might have (e.g. from your old jobs). If you want the reassurance that all your pensions are together in one Nest pension, great, it could be for you.

However, as soon as you move your pensions over to Nest, you can’t move them anywhere else until you get a new job, and get a new pension. Not ideal.

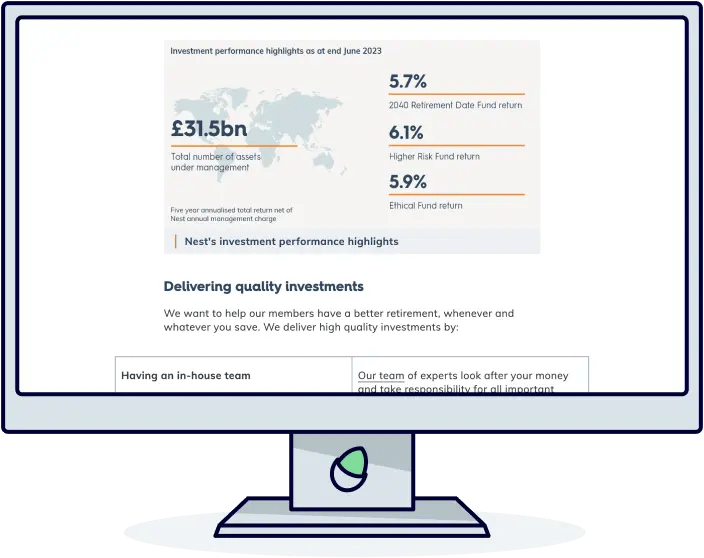

And it's worth mentioning, you probably aren't getting the best deal with Nest, the fees are higher than some others, and the investment performance isn’t the best – there are better options out there, where you have full control over your pension, can move it whenever you like, have low fees, and a great record of growing pensions over time…

As a reminder our top recommendation is the 5* rated PensionBee¹, they’re all of the above, and you can transfer old pensions over super easily. In fact, they’ll handle it all for you, and you also get a dedicated account manager to keep you updated on the progress, and they'll answer any questions you might have.

For all the best options, check out the best personal pensions.

The key bit here is that with pensions, you have the choice of all the personal pension providers out there, so you can pick the best one for you – just like a mobile phone contract, or broadband deal.

You can pick the cheapest option, or the one with the best customer service, or the pension plans that suit you, or the best mobile phone app (you get the idea) – you don’t have to only use your workplace pension that your employer decides for you!

You might be wanting to increase your pension contributions (adding more money) – this is often a very good idea as it will benefit your future self! But, it’s not necessarily the best idea to do this with your current workplace pension – unless you’re happy with the provider, their performance, their fees, and of course their service.

Nuts About Money tip: you can have more than one pension, and often when people want to increase their pension contributions, they open a personal pension – that’s one they open and pay into themselves, rather than their work pension.

Doing this has great benefits, as you get to pick which provider you like, so you can pick one that’s easy to use, low cost and a great customer service – or any criteria that suits you. Again, it’s like choosing a mobile phone contract. It’s your choice!

And, with a personal pension, if you don’t like the provider anymore, you can move to any other provider you like in the future too.

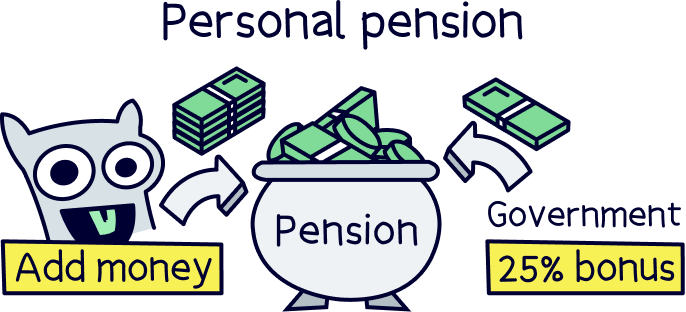

You’ll still get all the same tax benefits as a workplace pension. It just works a bit differently…

You’ll get any tax you’ve paid (at 20%) on your income as a 25% bonus paid directly into your pension, which refunds it all.

And if you’ve paid tax at 40% or 45%, you can claim this back on a Self-Assessment tax return.

If that sounds interesting to you, here’s the best personal pensions.

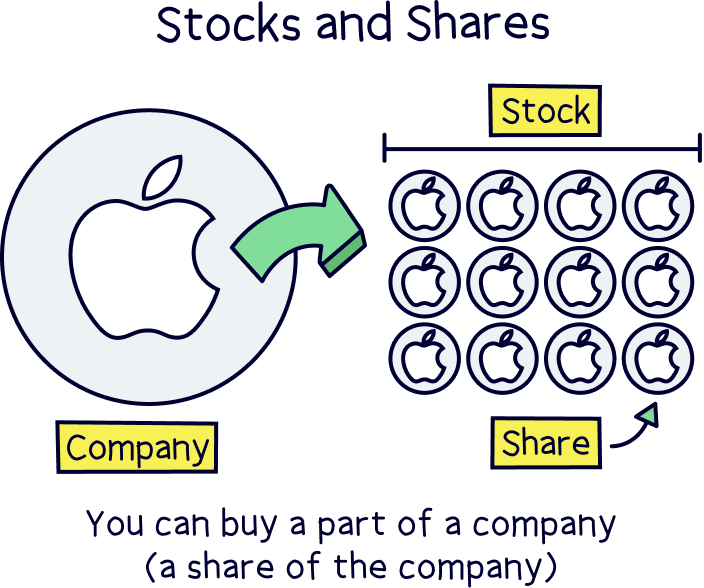

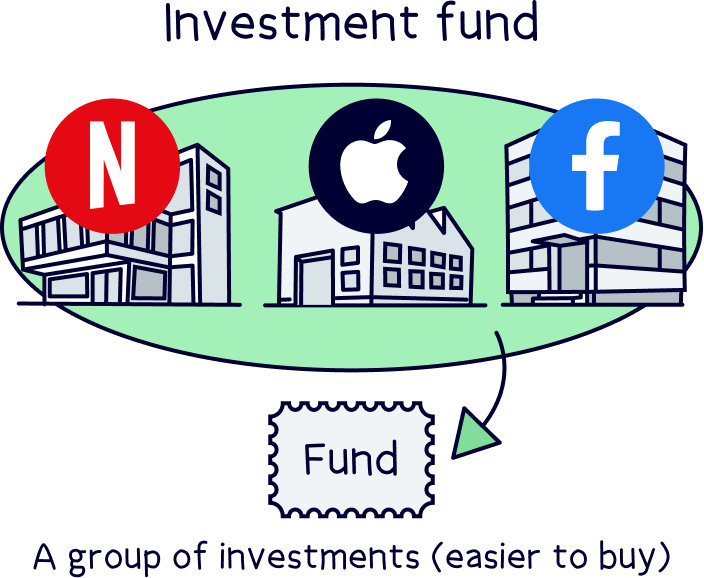

With Nest, your money is invested in a range of different investments, such as stocks and shares (which represents owning part (a share) of the ownership of a company), and things like bonds (loans to governments and large businesses), and possibly even things like commercial property.

These investments are all packaged together into something called an investment fund, and managed by experts to achieve a certain goal (for instance long-term growth). The experts will determine which investments to make within the fund, and the investments can change over time.

So, that means that you need to decide which investment fund you’d like your pension savings to go into. Your options are:

As Nest was set up by the Government, way back in 2010, it’s technically a public corporation, similar to the NHS and the BBC. That means there’s no owners, or shareholders, like you would have with a private company (or public company on the stock market).

It’s technically called the Nest Corporation, and is the ‘trustee’ of the Nest pension scheme. The Trustee is actually 15 people, called board members, alongside the employees of the Nest Corporation.

The board members are helped by specialists in pensions and investing, and running businesses. The corporation reports to the Secretary of State for Work and Pensions who ultimately makes decisions for the country relating to, well, work and pensions.

Note: although there’s no shareholders, that doesn’t mean Nest doesn’t aim to make money – there are still fees involved for Nest pension holders, and they’re not the cheapest (we’ll cover fees below).

Unfortunately, even though it’s effectively a government run organisation, there are still fees to pay with a Nest pension.

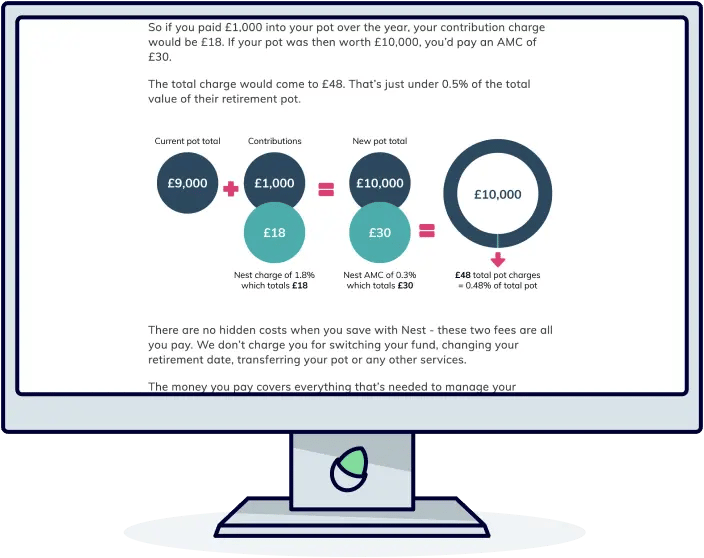

And, they’re a bit complicated. Initially, you’ll pay 1.8% for every contribution you make into your pension. So, if you add £10,000 per year, you’ll be paying £180 per year with this fee.

You’ll then also pay 0.3% per year on your total pension pot.

It’s a bit confusing right? Interestingly, the Government insists that having multiple fees within a pension is bad practice, and should be banned, but their own pension provider has multiple confusing fees... We’ll let you be the judge of that one.

Anyway, here’s how it compares with other providers, let’s use PensionBee as we’ve mentioned them already, and if you were saving £50, £100, £250 or £500 per month.

Overall, PensionBee comes in cheaper. However, it does all depend on which investment plan you choose, and that applies to any provider, they can all have different fees.

We’ve used the common investment plan that’s 0.50% per year with PensionBee, but some plans can be 0.95% per year (and more with other providers).

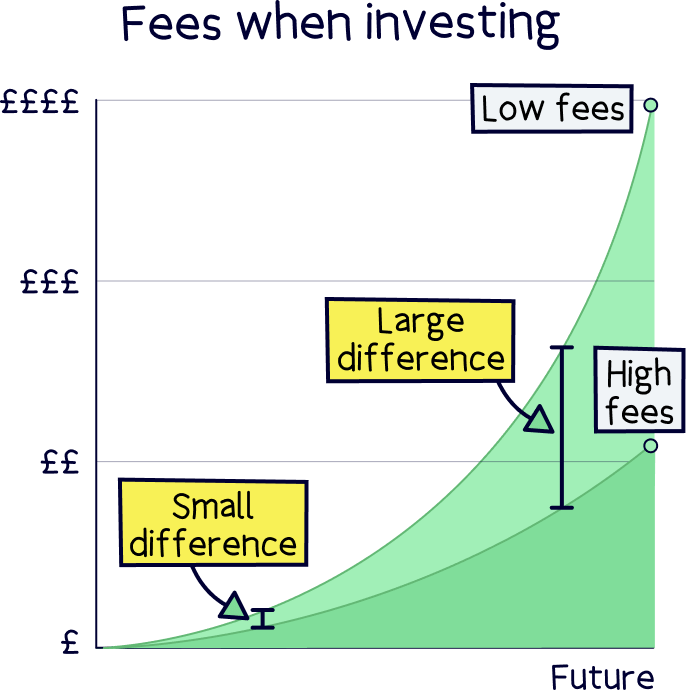

There’s not much in it though – so don’t make a decision based off fees alone (although small differences in fees can make a big difference over time) – consider things that are important to you, such as how easy it is to use, the pension plans themselves, and things like customer service.

If you’re got a large and growing pension pot, PensionBee, and some other pension providers also reduce their fees above £100,000 – so it can work out a lot cheaper over time, than with Nest. (PensionBee cut their fee in half for anything over £100,000.)

Note: if you don’t have a pension at all currently, PensionBee would be cheaper as you avoid the 1.8% fee on all your contributions (that you pay with Nest).

The customer support options are great, although the feedback from the actual service they provide is pretty poor.

There’s a section on the Nest website that answers common questions, such as how to access your account if you’ve forgotten your login details.

If you have more personalised questions, you can also speak to someone on the phone via their support line, or you can use the live chat feature on the website, or send them a text message.

The phone lines are open from 8am to 8pm every day, this is longer than a lot of the other pension providers (including our top choice PensionBee).

Yes, Nest is safe to use. It’s effectively run by the Government.

The investment service is also authorised and regulated in the UK by the Financial Conduct Authority (FCA). This means they have been approved and are trusted to look after and protect your money.

On the popular reviews website, Trustpilot, Nest has a rating of 4.1 out of 5, which is good overall. The service does as intended – a workplace pension scheme for employees to save for their retirement.

However, 20% of the reviews are 1 star, and lot’s of them mention how easy it is to transfer old pensions into Nest, but very hard to get your money out after. They also mention how hard the website is to use, and the customer service being poor.

Here’s a quick recap and the pros and cons of Nest:

Saving for retirement is super important – if you’re not yet saving, it's a great idea to start right away. To have a comfortable retirement you’ll need a very big pension pot by the time you retire.

With that in mind, Nest is great, as it helps employers set up their employees with a pension, and, as with all workplace pensions, you’ll get 3% of your salary, free from your employer if you pay in 5%.

So, if you have a Nest pension with your employer, great, take advantage of the free 3% by paying 5% into it. You will have to use Nest as it's your employers decision – however, you will get to choose which investment plan you’d like to use (with Nest).

If you’re looking to open a pension yourself, in addition to a workplace pension, great! However, you can’t open one with Nest.

There’s a few great personal pension providers out there. Some are easy to use, have a great mobile app, are low cost, have a great record of growing pensions over time, and have great customer service…

Our top recommendation is the top rated PensionBee¹ (and you’ll get £50 added to your pension for free). There’s also Beach¹, where you can save into a pension alongside other great savings accounts, such as with a tax-free ISA. Here’s our Beach review. For all the top options, check out the best personal pensions.

If you’re looking to transfer old pensions over to Nest, we also recommend checking out our recommendations above. Just like shopping for a mobile phone contract, you can pick the best provider for you.

You don’t have to only use your Nest workplace pension – it may not grow as well as other providers, or give you the same service as some of the best pension providers (remember 20% of their reviews were 1 star).

Overall, we’re giving Nest 2 stars. It’s a good option for employers to use and not have to worry much about their employees' pensions again, but the service isn’t great, there’s limited investment options and it’s not necessarily the cheapest out there.

To learn more, head over to the Nest website.

PensionBee is easy to use, low cost, and a great track record of growing pensions.

PensionBee is easy to use, low cost, and a great track record of growing pensions.

PensionBee is easy to use, low cost, and a great track record of growing pensions.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things money, with years of combined experience working in the finance industry and writing about money. We understand the ins and outs, how to get the best deals, save money, and how to communicate money in an easy to understand way (we hope you agree).

More than 20 years of combined experience researching and writing about money

Researched and reviewed a wide range of financial services companies, and have a transparent review process

We follow a strict editorial code to ensure you get the best information possible

PensionBee is easy to use, low cost, and a great track record of growing pensions.