Article contents

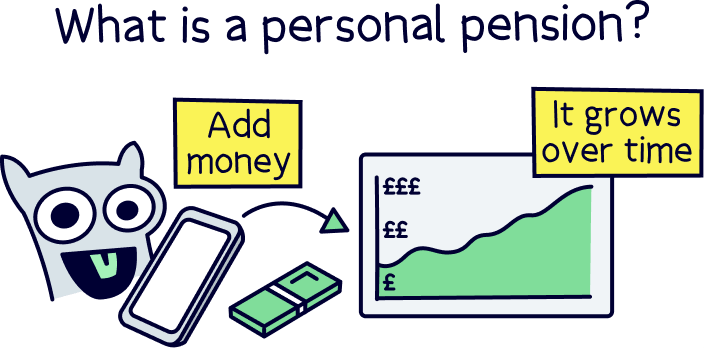

A personal pension is a pension that you set up yourself. It’s a bit like a piggy bank – you choose how much to pay into it, and once you’re retired, you can start taking your savings back out. Except it’s even better, as your money will also grow while it’s sat there!

Retirement might seem like ages away right now, but trust us, it’ll come round sooner than you think! So, you’ll want to start squirrelling away money now to make sure you’re financially stable in your golden years.

One of the ways you can boost your pension savings in retirement is by setting up this wonderful thing called a personal pension. Not sure what exactly that is? Don’t worry, we’ll reveal all here.

A personal pension is a pension you set up yourself – as opposed to a workplace pension, which is a pension your employer sets up for you.

A personal pension and a workplace pension are both types of private pensions. They’re pensions in your name, and you decide how much to save, and what happens to the money.

The other type of pension is a public pension, which is the State Pension. That’s what you’ll get from the government when you retire (at State Pension age, currently 66 but rising to 67 in 2028).

Anyway, a personal pension works a bit like a piggy bank. You choose how much money you want to pay into it – this can either be a regular monthly payment, or just the odd payment here and there when you have some cash to spare. Then, once you turn at least 55 (57 from 2028), you can access those lovely savings you’ve squirrelled away!

Oh, except personal pensions are actually much better than piggy banks. Which brings us onto…

On the surface, you might think that a personal pension looks pretty similar to a normal savings account. And you’re kind of right – a personal pension is pretty much just a fancy type of savings account where you can only access the money you pay in after you hit the age of 55.

However, there are a few things personal pension schemes do that normal savings accounts don’t, to make it even easier for you to save for retirement. Here are a few secret tricks they have up their sleeve!

Let’s go back to our piggy bank analogy for a second – there’s a good reason why we said that personal pensions are much better than piggy banks. With a piggy bank, you’d get the same amount of money out as what you put in. But with a pension on the other hand, you can expect to get a lot more money out than what you pay into it.

Yep, that’s right, your money will do some serious growing while it’s sat there in your pension pot, without you having to do a thing.

That’s because your money will be looked after for you by a pension provider – that’s the company that manages your pension. In other words, experts will spend time trying to grow your money for you, by investing it (that’s when your money is used to buy things like stocks and shares, which are essentially small ownership stakes of companies).

The idea is that as your investments increase in value, your money does too. Yes, it’s true that investments can go up and down in value in the short-term. But pensions are about saving in the long-term, ready for retirement – over a long period of time, your savings will go up overall, which means you’ll have lots more money to enjoy in your golden years than what you paid into your pension in the first place. Woohoo!

Now, all private pensions work this way, not just personal pensions. But the great thing about personal pensions is that you get to choose your own provider (unlike workplace pensions, where your employer will choose your provider for you). So, you can find a personal pension provider that has a pension fund with a proven track record for growing money, and you’ll normally be able to achieve quicker and bigger growth – meaning lots more juicy cash and bigger retirement income to enjoy in your golden years.

Not sure where to look? Why not compare our best personal pensions.

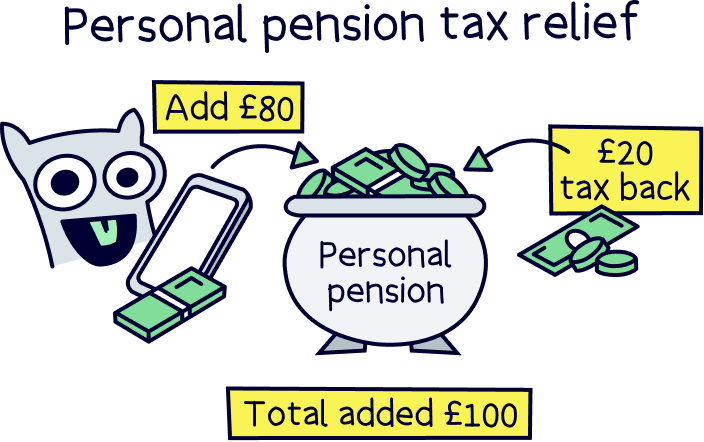

The government wants you to save up for retirement so they’re not left propping you up in old age. To encourage you, they give you this wonderful thing called tax relief. That means you don’t have to pay any tax on the money you pay into your pension. Kerching!

With a workplace pension, you’ll just pay less tax in the first place, as the difference will be worked out before you get your payslip from your employer each month. But with a personal pension, you’ll pay tax like normal. Then, the government will refund the tax you’ve overpaid, straight into your pension pot!

If you’re a basic-rate taxpayer (meaning you earn less than £50,270 per year), you’ll get 20% tax relief. In other words, if you pay £80 into your pension pot, the government will add a £20 bonus to turn it into £100 (£20 is 20% of £100). Nice!

If you’re a higher-rate taxpayer, you’ll be able to get an even bigger bonus to make up for the fact that you pay more tax. On any income you’ve paid 40% tax on, you’ll be able to get 40% tax relief. And if you pay 45% tax on any of your income (as an additional rate taxpayer), you’ll even be able to get some tax relief at 45%. (You can simply claim on a Self Assessment tax return).

Ultimately, this means that personal pensions aren’t just great for saving for retirement – they’re also great at putting more money in your pocket and less in the taxman’s (or taxwoman’s!).

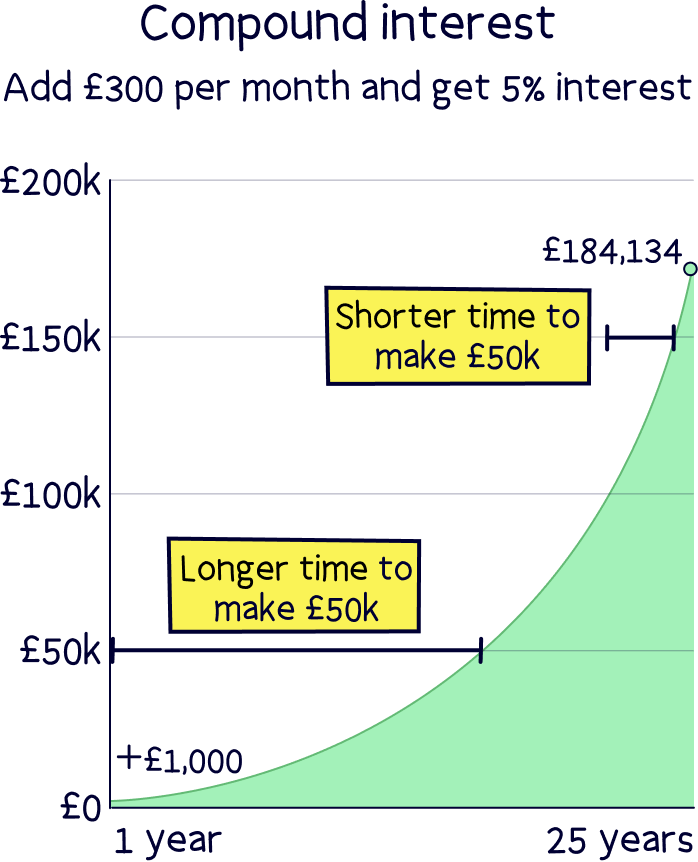

We’ve all heard the phrase ‘every little helps.’ And that’s never been more true than when it comes to pensions. That’s right, small contributions to your personal pension pot can really add up over time, thanks to something called compound interest (also known as compounding interest).

Remember how we said that when you leave your money sitting in a pension, it will grow as your investments increase in value? Well, compound interest refers to the fact that the extra money you’ve made on your savings will also grow.

Okay, okay, we know that sounds confusing. But don’t worry, it’s not as hard to wrap your head around as you might think.

Imagine you invest £1,000 into a personal pension this year. Now let’s say you make a 5% return (that’s a fancy word for the profit you’ve made from your investments). That means in just one year, your savings have increased by £50 without you having to do anything at all – your original £1,000 has now become £1,050!

Now let’s imagine you also make a 5% return in your second year. 5% of £1,050 is £52.50, so you’ve now got £1,102.50. And don’t forget, you haven’t had to do anything at all!

Your money will keep growing like this every year, which means even the smallest amount you add to your personal pension pot can turn into a fairly large amount after a long period of time. And of course, that’s without even counting the money you pay into your pension over the years. If your money kept growing like this for 25 years and you added £300 to your pension every month, you’d end up with £184,134.20! Not bad at all. Another 10 years and it would almost double to £346,561.45!

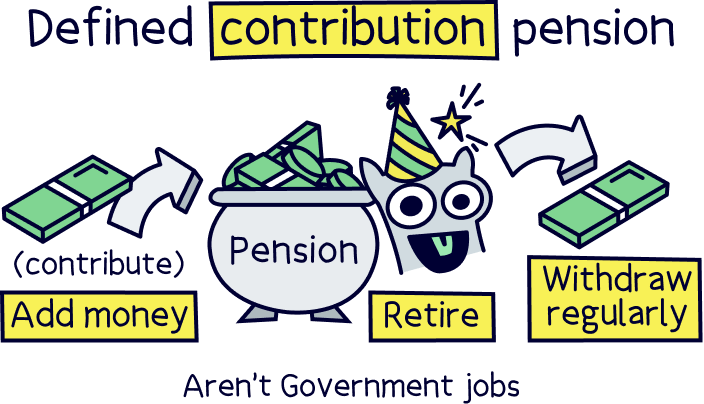

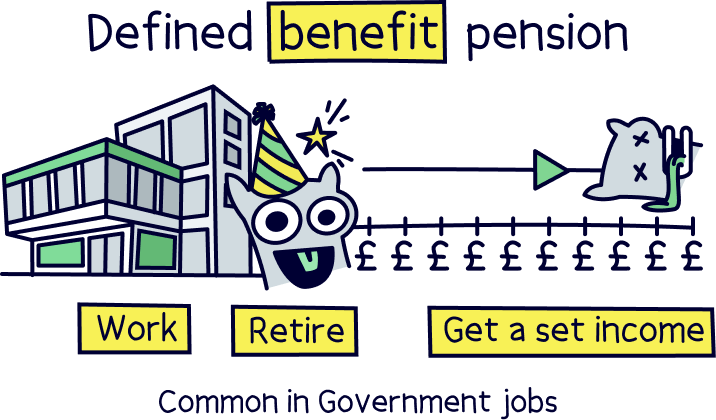

A personal pension is technically called a defined contribution pension (and most workplace pensions) – that means you decide how much to contribute to it, where your pension is saved and how much you want to take out of it when you retire (and when).

However you can also get defined benefit pensions. These are common with workplaces such as the NHS. These are a bit different, and you’ll get a set retirement income when you retire depending on the rules of the pension scheme – such as how long you have worked there and your salary (a final salary pension is a defined benefit pension). You can’t open these unless your workplace offers them, you can only open a personal pension.

Lots of people think that personal pensions are just for people who don’t have a workplace pension – like people who are self-employed or who work part-time and earn very little (if you earn less than £6,240 per year, you won’t qualify for a workplace pension from your employer). In this case, getting a personal pension is going to be a really wise move to help you save up for retirement.

However, what you might not realise is that anyone can get a personal pension. And that includes people who are employed! That’s right, even if you have a workplace pension already, getting a personal pension can be a great way to boost your savings in retirement.

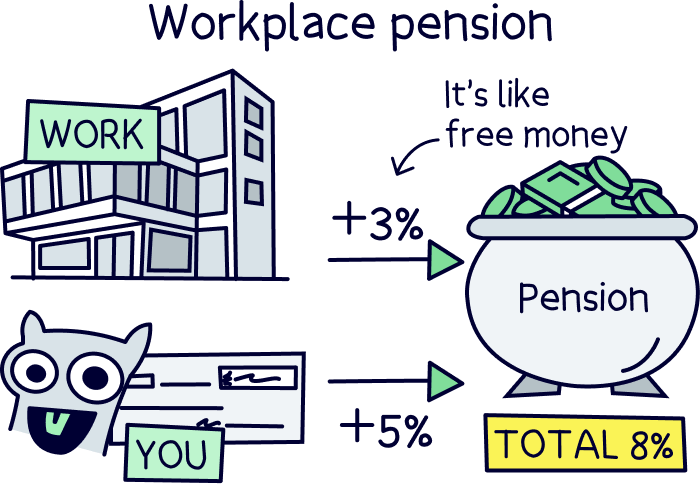

Don’t get us wrong, we’re not saying you should get a personal pension instead of a workplace one. If your employer offers you a workplace pension, you should definitely take it – after all, not only will you pay into it every month (at least 5% of your earnings), but your employer will have to pay into it too (at least 3% of your earnings from their own pocket)! So, a workplace pension means unlocking free money from your employer.

Instead, we’re saying that if you have extra savings and you want to increase your pension contributions, it’s worth considering getting a personal pension as well as your workplace one. Remember, personal pensions will often grow your money quicker than a workplace pension, as you’ll be able to choose a provider with a good track record for growth. They also tend to come with lower fees, which is a bonus!

Not only that, but unlike a workplace pension, you can put as much or as little money as you want into your personal pension (as long as you choose a provider who’ll give you that flexibility – lots do!). That means you can set up regular monthly payments if you choose to, but you can just as easily pay in small amounts here and there whenever you have cash to spare – great if you want to be able to invest more money into your pension some months than others.

Ultimately, personal pensions give you that added bit of flexibility and control over your savings, which is great for boosting your retirement income. In fact, some modern pension companies like PensionBee even have handy mobile apps that let you track your money and watch it grow (over the long term!) on the go. More on them and other great personal pension providers in a bit!

If you have got a workplace pension scheme, you’ll probably be aware your employer makes employer contributions into your pension too. For instance if you add 5% of your salary into your pension pot, your employer will add 3% (by law they have to!).

Some nice employer will add more into your pension if you add more (we know, hard to believe!). So if this is you, you should consider paying more into your workplace pension before opening a personal pension – as you’ll be getting more free cash from your employer!

Now you know what personal pensions are. But there are actually a few different types. You can get…

Let’s break those all down here.

A stakeholder pension is a type of personal pension that has to abide by some extra rules set by the government. Basically, they’re designed to be really accessible for anyone – they have low fees, they’re flexible and anyone can set one up. Yay!

To make sure that they’re as accessible as possible, stakeholder pension providers aren’t allowed to charge you a penalty fee if you pause your pension contributions or decide you want to transfer your pension elsewhere (known as a pension transfer). They can’t force you to add in big sums of money (they have to let you pay in as little as £20 at a time if that’s what you want!). And they can’t charge you high fees (the maximum they’re allowed to charge you is 1.5% a year for the first 10 years, and 1% after that).

All sounds pretty good, right? Well, yes! It is all pretty good. Except that lots of ‘normal’ personal pensions offer all these things too, if not better!

Yes, these personal pension providers don’t have to offer all the same benefits that stakeholder pensions do. But there are lots more standard personal pensions out there than there are stakeholder pensions. So, you’ll have a lot more choice and you’re likely to be able to find an even better deal. Strange world, eh?

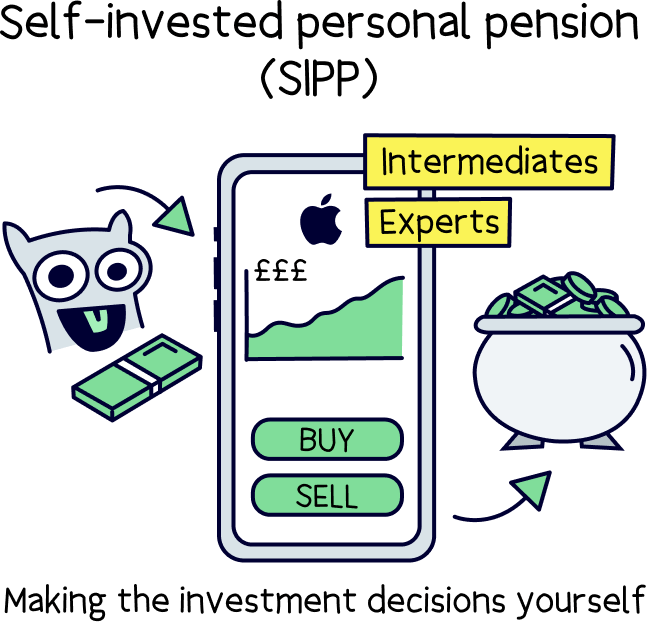

Remember how we said that when you have a personal pension, your money will get invested? Well, with most personal pensions, an expert will handle all that for you – so you can leave your money in the hands of people who really know what they’re doing! However, with self-invested personal pensions, known as SIPPs, you invest your money yourself.

That’s right, you choose exactly where your money goes. Gulp! That means SIPPs are generally better-suited to people who have lots of experience investing as you’ll want to make sure your money is being well looked after!

Not only that, but a SIPP will need a lot more time and attention from you. While most personal pensions will just grow over time without you having to lift a finger, a SIPP will need you to regularly check in to see how your investments are performing – and to change your strategy when needed.

In other words, if you want an easy option where your money gets looked after by experts and you don’t have to do a thing, SIPPs aren’t for you. But if you’re a bit of an investing pro, you might well be up for the challenge!

Last but certainly not least, we have just normal personal pensions. In other words, these are just personal pensions that aren’t stakeholder pensions or SIPPs. And to be honest, they’re what we’ve really been focusing on when we’ve been writing this article.

Why? Well, these ‘normal’ personal pensions are the ones you’re most likely to find. There are loads of providers out there offering these, which means you’ll have the pick of the bunch – in other words, you’ll usually be able to find a provider offering you super low fees and who’s able to grow your money quickly. In fact, you’ll often find that a ‘normal’ personal pension provider can provide you with a better deal than a stakeholder pension provider.

Not only that, but many personal pension providers are super flexible. They’ll let you pay in as much or as little as you want, when you want, without having to worry about penalty charges if you want to pause pension contributions at any point or if you want to move to a different personal pension provider.

If you check out our selection of the best personal pensions, they almost all fall into this category. Just saying!

Private pension providers will normally charge you a fee for managing your pension. But the good news? You’ll normally be able to access cheaper fees with a personal pension than with a workplace pension, as you’ll be able to deliberately choose a provider with low fees! Get in.

Exactly how much you’re charged will vary from provider to provider. Normally, they’ll charge you a percentage of the pension savings you have stored up in your pension pot, every year – and they’ll just take this out of your pension automatically.

If you decide to go for a stakeholder pension, your provider won’t be allowed to charge you more than 1.5% per year for the first 10 years, and then 1% per year after that. However, lots of normal pension providers (aka personal pension providers that don’t offer stakeholder pensions!) will have fees that are just as low as this, if not lower. Our favourite, PensionBee, charges between 0.50% and 0.95% depending on the plan you choose and the amount you put in. Sweet!

Ah, so you’ve understood how great a personal pension is and now want to save as much as possible? Great idea! However there are some rules on what you can pay in.

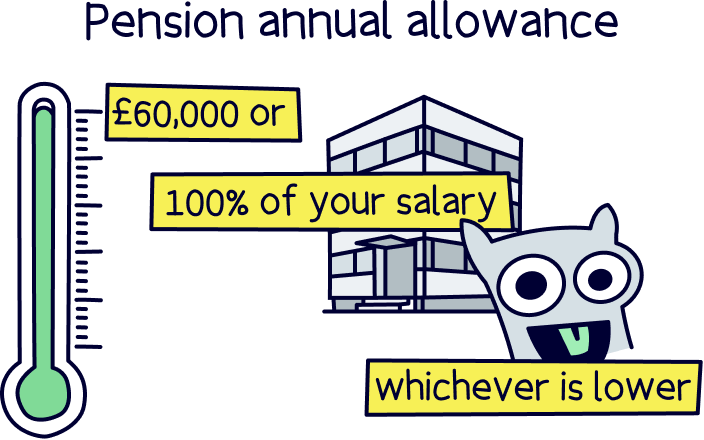

First, you can only pay into your pension as much as your total income per tax year (April 6th to April 5th the following year), or up to £60,000, whichever is lower. This is called your annual allowance, and applies across all of your pensions, so includes your workplace pension if you have one. (Well, you can pay as much as you like in, but you won’t get the tax free benefits).

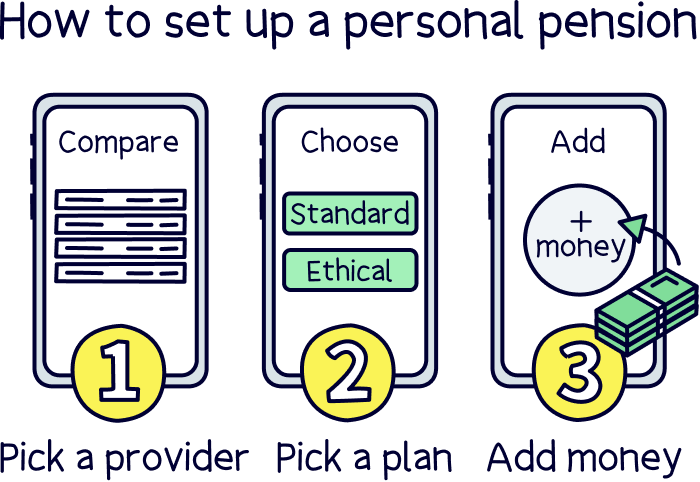

Okay, okay, now we’ve banged on about personal pensions for a bit, you’re probably wondering how to actually get one! Luckily, starting a personal pension is easy – just follow these simple steps.

First things first, you’ll need to choose a personal pension provider who you want to look after your pension savings for you. That means now’s the time to go on the hunt for one of those awesome companies with low fees, a good track record for growing your money and flexible saving options!

Don’t worry – we’ve done the hard work for you and have compared the best personal pensions. Two personal pension providers that deserve a particular mention are PensionBee and Beach¹.

We love PensionBee as it makes it super quick and easy to start saving for retirement. They have great customer service, a good track record for growing your money, low fees and even a handy mobile app. That’s right, you can track your money and watch it grow (over the long term) whenever and wherever you want!

Beach¹ is also really great, they don’t just cater for pensions, they have an easy access account too (a tax-free ISA), plus the app is easy to use and the customer service is excellent.

Find the best personal pension for you – you could be £1,000s better off.

Get £50 added to your pension

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

Great app

A great and easy to use pension. Add money from your bank or combine old pensions into one, (they’ll find lost pensions too).

The customer service is excellent, with support based in the UK.

Beach is an easy to use pension app (and easy to set up), where you just add money and the experts handle everything. It’s all managed on your phone with a great app, and you can see your total pension pot whenever you like.

If you’ve got lost or old pensions, Beach can also find them and move them over too, so you can keep all your retirement savings in one place, and never have to worry about losing them in future.

You’ll get an automatic 25% bonus on the money you add to your pension pot from your bank account (tax relief from the government), which refunds 20% tax on your income, and if you pay 40% or 45% tax, you’ll typically be able to claim the extra back too.

The pension plan (investments) are managed by experts, who are the largest investment company in the world (BlackRock). And they consider things like reducing climate change, meaning your savings could make the world a little better in future too.

You can also save and invest alongside your pension with an easy access pot (access money in around a week), designed for general savings, with the investments managed sensibly by experts too. And money made can be tax-free within an ISA.

Fees: a simple annual fee of up to 0.73% (minimum £3.99 per month).

Minimum deposit: £25

Customer service: excellent

Pros:

Cons:

Find the best personal pension for you – you could be £1,000s better off.

Now you’ve picked a personal pension provider and signed up, you can go ahead and pick a pension plan – a pension plan basically just outlines how your money will be looked after, what fees you’ll pay for the pleasure, and what funds your money will be invested in (a fund is when lots of people’s money is pooled together in a collection of investments to help your money grow).

There’s no need to panic! Your provider will help you to pick the right plan for your needs – normally, they’ll recommend one for you based on a few questions including your age and when you can see yourself retiring.

That said, some more modern personal pension providers like PensionBee have a few more jazzy options to choose from – for example, you can choose to only have your pension invested in companies that are ethical or socially responsible. It goes without saying that we’re all about this at Nuts About Money. After all, why wouldn’t you want to save the planet at the same time as saving for retirement?!

Finally, you just need to start adding money into your brand new pension, so that it can start growing ready for retirement. Simple!

Some personal pension providers will ask you to pay a certain amount into your pension pot to start with, while others will ask you to set up a regular monthly payment. However, most of the modern providers will let you pay in as much or as little as you want, whenever you want.

Of course, the more you pay in, the more financially secure you’ll be later on in life – so we’d recommend paying into your pension pot regularly if you can (and as early as possible to give your money time to grow). But it’s important not to overstretch yourself either! Remember, you won’t be able to withdraw your pension before 55 (unless you want to pay a crazy amount of tax!) so you should only pay in as much as you can afford to.

When it comes to taking money out of your personal pension, you’ll first have to wait until you are at least 55 (57 in 2028), at which point you can start withdrawing money from your pension if you wish.

You can take a massive 25% of your money tax-free, and as a lump sum too. Or, regularly as income and 25% of the total will be tax-free. You’ll pay Income Tax on the rest, just like you do now with a salary on your job (or your income if self-employed). So, you’ll pay Income Tax if your total income is above £12,570 per year in retirement.

However, once you start taking money from it, you often can’t keep saving at the same rate. It’s intended for retirement. We won’t go into this too much now, but your annual allowance could reduce to £4,000 per year. This is called the Money Purchase Annual Allowance.

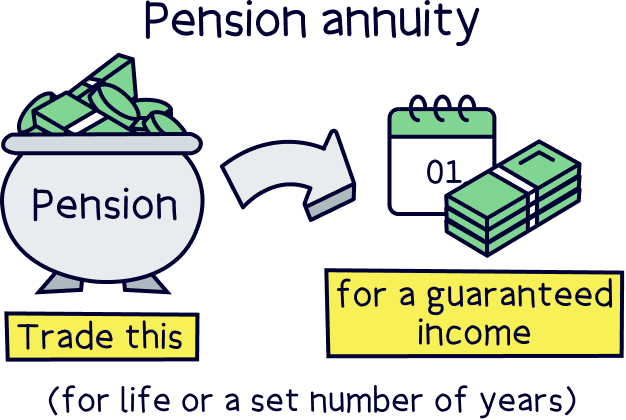

It’s very common to buy an annuity with your pension. This guarantees an income for life (or a set number of years). Or, you can keep it as a pension, and simply take money from it, called ‘drawdown’. (Your investment fund will change to protect the cash in your pension).

Ready to start boosting your pension savings for retirement? Then we’re sure you’ll agree, starting a personal pension is a great shout. Not only is it a sensible way to stash away some savings, but your money will also grow while it sits in your pension pot, and you’ll benefit from that lovely tax relief from the government too!

If that all sounds good to you, then the first step is to choose a personal pension provider – easy peasy because we’ve done all the hard work for you! Just browse our selection of the best personal pensions to get started.

PensionBee¹ is a super simple option that specialises in pensions, with low fees and a handy app that lets you track your money and watch it grow. Meanwhile, Beach¹ is also super simple to use and has an easy access pot alongside a pension, for everyday savings (access the money in around a week).

Either way, there’s no better time to start saving for retirement than now. Chop chop!

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.