Article contents

A stakeholder pension is a pension that anyone can get – whether they’re employed, working part-time or self-employed. However, there could be better options out there now.

Pensions are wonderful things that help you save for later on in life. But there are a few different types to get your head around. One of those is a stakeholder pension.

Stakeholder pensions are great as they have relatively low fees and they help you save flexibly for retirement. However, they’re a liiiiittle bit old-school and there are lots of other personal pensions like PensionBee¹ out there nowadays that are even better – we’re talking low fees, lots of flexibility, the chance for your money to grow more and handy websites and apps to help you save. Don’t worry, we’ll explain it all here!

A stakeholder pension is a type of personal pension – that’s a pension that’s set up especially to help you save for retirement.

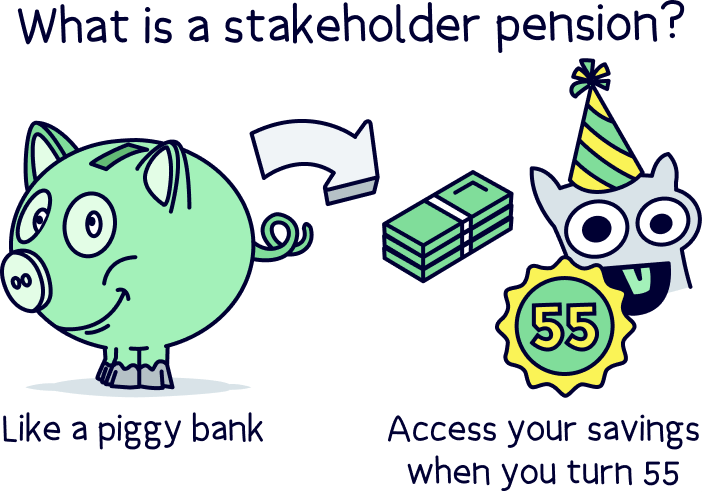

Like most pensions, stakeholder pensions work a bit like piggybanks (pensions that work like this are also known as defined contribution pensions).

You pay money into it throughout your working life. Then, once you turn 55 (or 57 from 2028), you can finally access all those lovely savings you’ve built up. Oh, except they’re actually much better than a piggybank. Here’s why…

Stakeholder pension schemes are designed to be really accessible for everyone – they’re flexible, they have low fees and anyone can set one up. Woohoo! This makes them really popular with people who might otherwise struggle to access a pension – for example, people who work part-time, self-employed people whose income fluctuates, and even people who are unemployed (although anyone can set one up to boost their retirement income, including people with full-time jobs!).

Note: if you're looking to start your own pension check out PensionBee¹, they're 5* rated, easy to use, have low fees and a great track record of growing pensions over time. Here’s our PensionBee review to learn more.

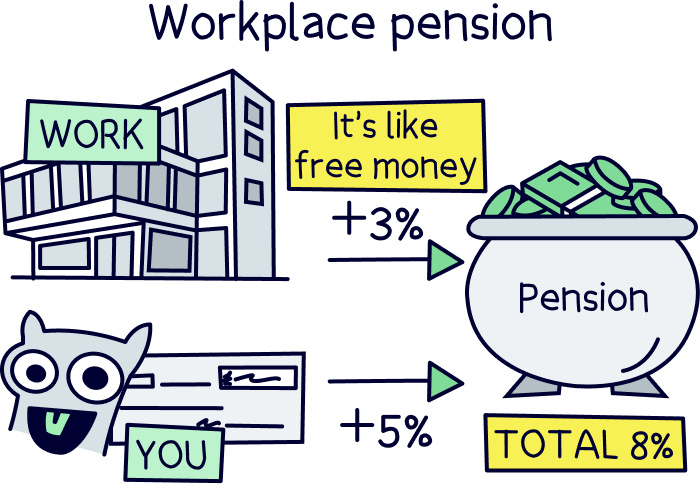

That said, stakeholder pensions can also be set up for you by your employer. If you have an employer, the chances are they’re legally obliged to start a pension for you, known as a workplace pension – you have to contribute a percentage of your earnings each month (at least 5%), and your employer tops that up themselves (they have to add at least 3% from their own pocket). Nice! This doesn’t have to be a stakeholder pension, but it can be.

If you’ve got a workplace pension, and a nice employer who will contribute more than 3% if you contribute more (so if they match your contributions), you should take advantage of this first. Contribute more into your workplace pension scheme before opening a stakeholder pension or any other personal pension – it’s basically free money!

Find the best personal pension for you – you could be £1,000s better off.

Okay, remember how we said that stakeholder pensions are a type of personal pension? Well, there are actually 3 types of personal pension altogether. These are…

We’ll explain what each type is in just a minute. But as a general rule, they’re all designed to help you grow your money over time, and they’ll all give you that lovely thing called tax relief too (kerching!).

However, stakeholder pensions also have to follow some special rules set by the government – these rules are designed to make it easier for you to save flexibly for retirement, so they’re pretty nice! That means when you start a stakeholder pension, you know you’ll get…

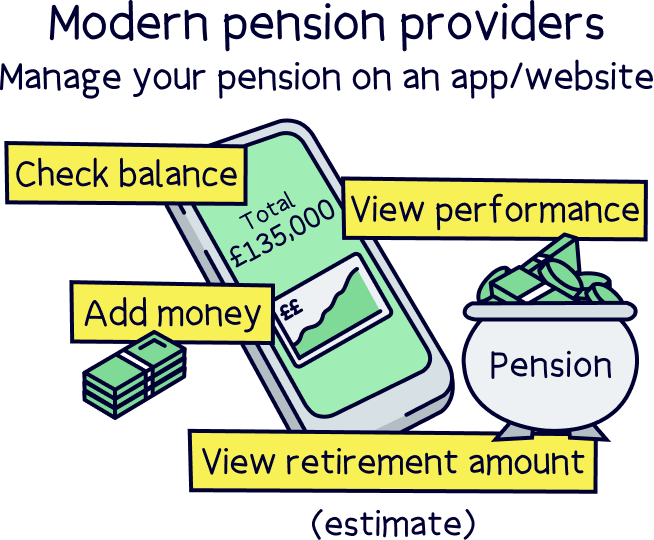

Sounds nice right? Well, yes. However, bear in mind that even though other types of pensions don’t have to follow these rules, some of them are even better. In fact, there are lots of modern pension providers that operate fully online that are generally cheaper and better (plus, they have handy mobile apps that make it easy for you to track your savings on the go!).

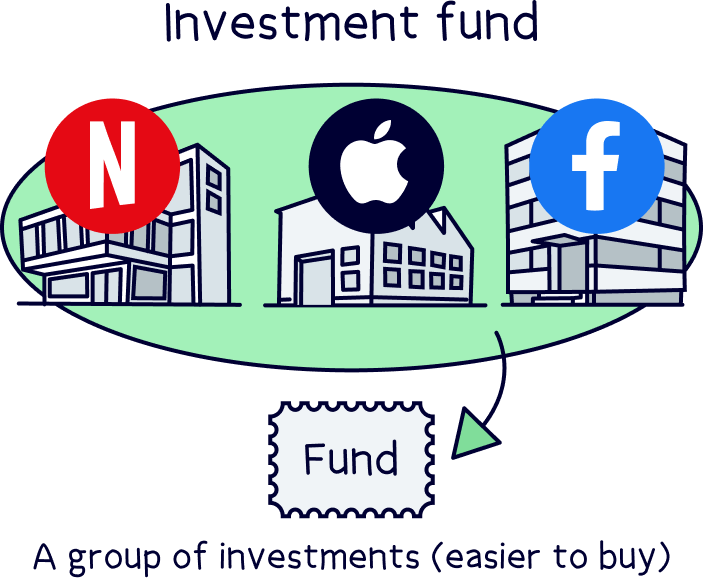

Plus, even though stakeholder pensions are designed to grow like other types of pensions, they may not grow quite as much. This is because they can’t invest in as many funds (funds are when lots of people’s money is pooled together in a collection of investments, designed to help your money grow).

Stakeholder pensions and standard personal pensions are really, really similar. At a glance, you’d probably struggle to tell the difference!

However, the main difference is that with a stakeholder pension, your pension provider will have to follow those extra rules set by the government. That means a stakeholder pension may have…

As you can see, stakeholder pensions can be pretty great, as you’ll know that whichever pension provider you go with, they’ll have to play by these rules – which means cheaper fees and more flexible saving for you! However, don’t forget, you can get all the benefits of a stakeholder pension (like low fees and flexible saving options) with a standard personal pension too – you’ll just need to find the right pension provider.

On that note, PensionBee¹ definitely deserves another shoutout – not only do they offer low fees (just as low as many stakeholder pension providers), but they’ll also let you pay in as much or as little as you want, whenever you want. Oh, and they have a handy mobile app too, which lets you track your money and watch it grow while you’re out and about.

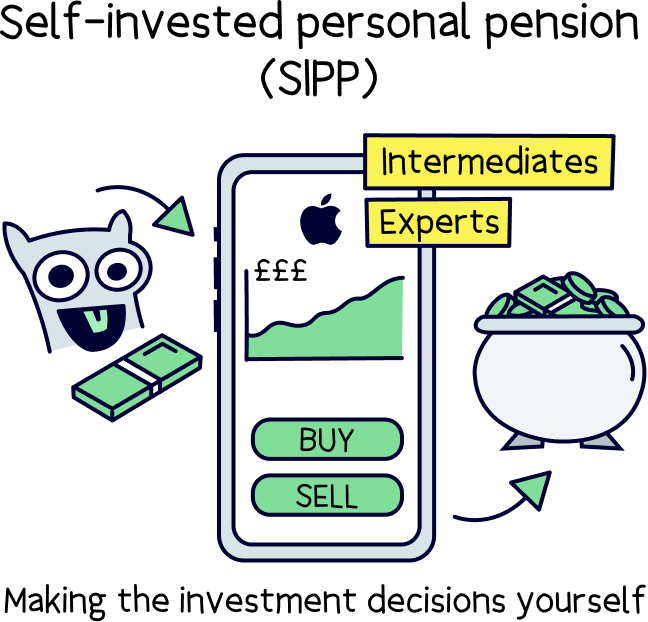

‘SIPP’ stands for ‘self-invested personal pension’. It’s basically a personal pension where you choose exactly what the money in your pension pot is invested in.

This is different from stakeholder pensions (and standard personal pensions!), where your pension provider will normally choose which funds to invest your money in themselves. Yes, they’ll sometimes give you a choice. But in general, the options they give you have been carefully picked out by experts – plus, they’ll look after your investments for you so that you don’t have to worry about that side of things at all.

When you compare the two, SIPPs will normally give you…

Ultimately, we’d only ever recommend SIPPs to people who have a lot of experience investing. But if that sounds like you, here's the best self-invested personal pensions.

However, if you’re not an investment pro, it’s probably going to be safest to let the experts look after your pension for you. After all, you’ve carefully stashed all that cash away ready for retirement, so you want it to be looked after properly! Whether you opt for a stakeholder pension or a standard personal pension, these will allow you to sit back, relax and watch your money grow ready for your sunset years!

Decided that a stakeholder pension is the one for you? Then there’s no time to waste! The earlier you start a pension and start saving, the more chance your money will have to grow ready for when you eventually retire!

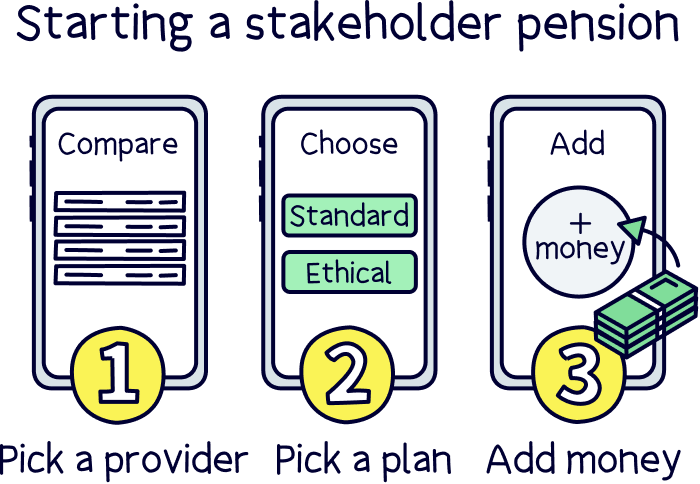

Luckily, starting a stakeholder pension is easy – just follow these simple steps.

First things first, you’ll need to choose a pension provider. Every pension provider is different, so it’s worth spending some time comparing what’s out there – they’ll all have different fees and they may have different rules about things like minimum contributions too. However, if you’ve opted for a stakeholder pension, at least you’ll know that they’ll all have relatively low fees and flexible contribution options, inline with those government rules!

It’s worth noting that there aren’t actually that many providers offering stakeholder pensions. The most popular are insurance providers like Standard Life and Aviva.

Alternatively, if you can’t find a stakeholder pension provider that you love, consider using a personal pension provider that happens to have low fees and flexible contribution options. For instance, PensionBee’s¹ fees are less than 1% and they’ll never charge you a penalty for pausing contributions. Plus, you can pay in as much or as little as you want (and they have a handy mobile app you can use to watch your money grow too!).

Another great pension providers is Beach¹ - an easy to use pension with a great app. Add money or combine old pensions (and find lost pensions). Plus, the customer service is excellent.

Now that you’ve chosen a pension provider, you’ll just need to go ahead and pick a pension plan – this basically just outlines how your money will be looked after, what fees you’ll pay and what funds your money will be invested in. Most pension providers will have a few options!

Don’t worry, your pension provider will make it easy to pick a plan – normally, it’ll be to do with how old you are and how long there is before you retire.

But some pension providers, like PensionBee¹, will have more jazzy options too – like funds that only invest in ethical or socially responsible companies. These are great if you want to feel like you’re saving the world at the same time as saving for retirement. Obviously, we’re a big fan!

Finally, you just need to start saving into your new pension! Congrats!

Some pension providers will ask you to pay a certain amount into your pension to start with, but a stakeholder pension will never make you add more than £20. And anyway, many pension providers will just let you pay in as much or as little as you want, without restricting you at all.

Of course, the more you can save into your pension, the more financially secure you’ll be later on in life. But it’s important not to overstretch yourself either. Stakeholder pensions are designed especially so that you don’t lose out if you have to pause contributions for one reason or another – so they’re perfect if you’re looking for a flexible option that will let you save in the way that’s best for you!

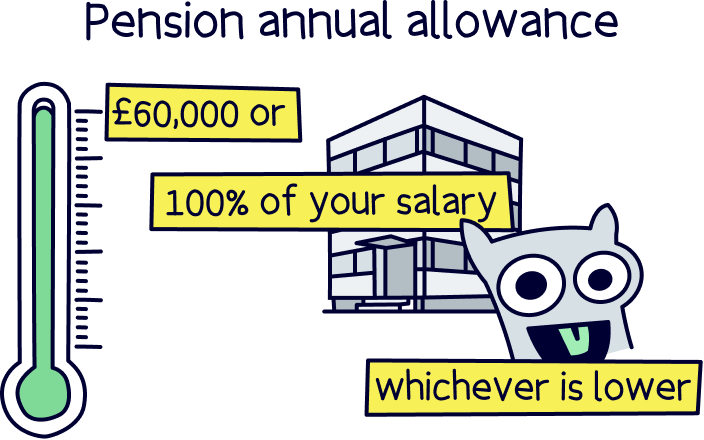

Keen to get saving? It’s a good idea to save as much as you can into a personal pension, however there are limits! And these apply to all private pensions – so stakeholder pensions included.

First, you can’t save more than your total annual income within a tax year (April 6th to April 5th the following year), or more than £60,000, whichever is lower. This is called your annual allowance.

When you want to retire and start spending your savings – you’ll first have to wait until you’re 55 (57 from 2028), although ideally hold out until you fully retire as your money will keep growing while it’s invested within the pension fund.

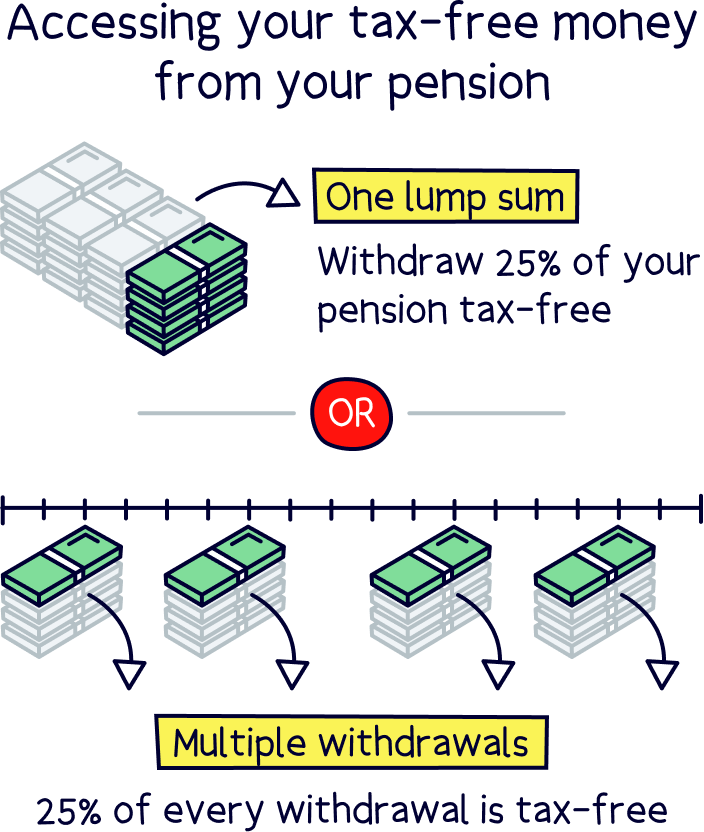

When you do want to take the cash from your stakeholder pension, you can first take 25% of it completely tax free. So that’s no Income Tax to pay at all. You can take this as a tax free lump sum, or, you can take it as a regular income, and the first 25% of each payment will be tax free. You’ll pay Income Tax on the rest if your annual income is above your Personal Allowance of £12,570. Just like a job now. There’s no difference with pensions.

Taking your cash from your pension is called ‘drawdown’, but you can also buy an annuity with your pension funds. This will give you a set income for the rest of your life (or for a set number of years).

Stakeholder pensions have the same retirement benefits as all other private pensions (defined contribution pensions). The only difference is how you save, such as the lower minimum contributions and lower fees.

Retirement may well feel like a long way off right now, but it’ll come round sooner than you think! And the earlier you start saving, the more you’ll thank yourself later.

Starting a stakeholder pension can be a great option as it will guarantee your pension provider will treat you nicely – in other words, you’ll get low fees, low minimum contributions and no penalties for pausing contributions as standard.

But don’t fall into the trap of thinking these are the only pensions that come with these benefits!

Lots of standard personal pension providers, especially more modern companies that are fully online, will also give you these things and more – even though the government doesn’t require them to. So, do your research before discounting them.

Our favourites are PensionBee¹ and Beach¹, which both have pretty low fees. PensionBee is great if you want good customer service and an amazing app that lets you watch your pension grow wherever you are. And Beach¹ is great if you want to save in other kinds of savings accounts alongside a pension (like a tax-free Stocks & Shares ISA managed by a team of experts), meaning you can track all your investment savings in one place. It's also easy to use with a great app.

Whatever you choose, one thing’s certain – by starting a pension (and saving into it regularly), you’re setting yourself up for a lovely life in your golden years. Cruises around the Caribbean, anyone?!

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.