Article contents

Stocks and Shares ISAs are a kind of savings account where your money gets invested in successful, or likely to be successful, companies via the stock market, rather than kept as savings in the bank. It's safer than it sounds, easy, and all handled by experts. Best of all, it makes way more cash in the long term.

Let’s talk about Stocks and Shares ISAs. The best (and super easy) way to grow your money over time. Don’t worry if you don’t know anything about stocks and shares, you don’t actually need to know anything to enjoy the huge benefits – it’s all managed by experts for you.

By putting your head-earned dough into a Stocks and Shares ISA, it’ll make you a lot more money in the long-term than any other savings account. Interested? Let’s go through everything you need to know and how to get started.

If you just want to know the best Stocks & Shares ISAs, skip ahead here.

What is an ISA? And why are a Stocks & Shares ISA so unique? Well, ISA stands for ‘Individual Savings Account’, and it’s a savings account with one massive benefit – you don’t pay any tax at all when your money grows.

Usually, if the money in your bank account earns interest, the government counts it as income (i.e. money you earn) and you have to pay tax on it.

With normal savings accounts, that aren’t ISAs, you pay tax every year on interest over £1,000 if you’re a basic-rate taxpayer (earning between £12,571 and £50,270 per year) and on interest over £500 if you’re a higher rate taxpayer (earning £50,271 or more). These limits are your Personal Savings Allowance (PSA).

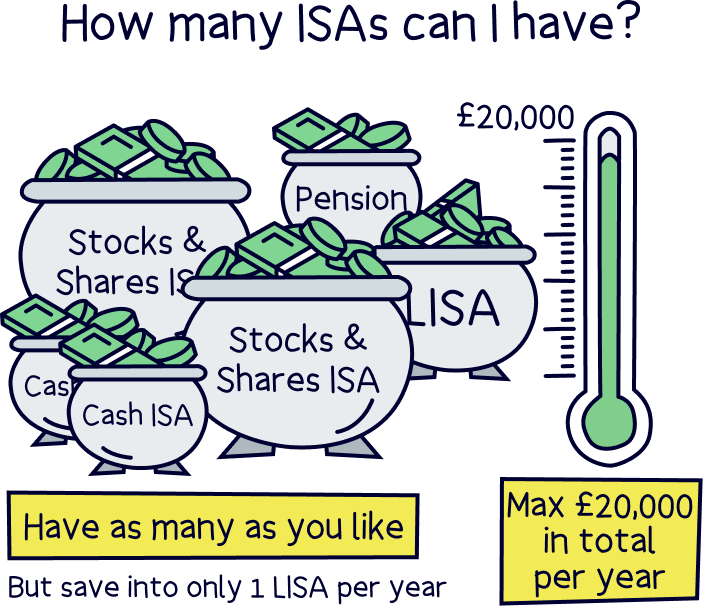

However, to encourage saving, UK residents get an annual ISA allowance, which means that you can put a certain amount into ISAs each year without paying any taxes at all on the extra money these accounts make. How good is that?! This allowance is currently £20,000.

You can put your savings into one ISA, or split it across different kinds of ISAs, such as a Cash ISA or a Lifetime ISA (more on this later). Here’s more about all the different types of ISAs.

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.

Firstly you can make a lot more money with a Stocks and Shares ISA than you can with any other type of ISA. How come?

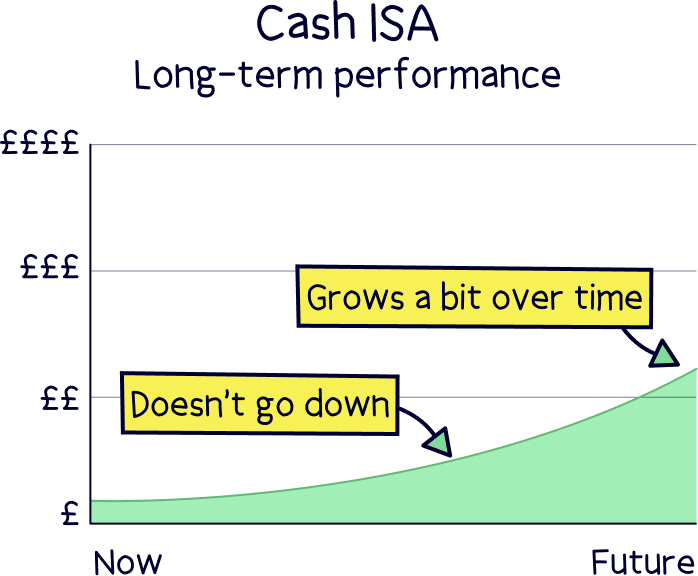

With a Cash ISA (a type of ISA where you just save your money and it makes interest), the ISA provider (that’s the company who manages your ISA, for instance a bank), will decide the interest rate you get.

However, with a Stocks and Shares ISA, where your money is invested by experts, your money grows based on how things are going with the stock market – such as businesses becoming more valuable. Over time this can make you way more money (and we mean waaay more).

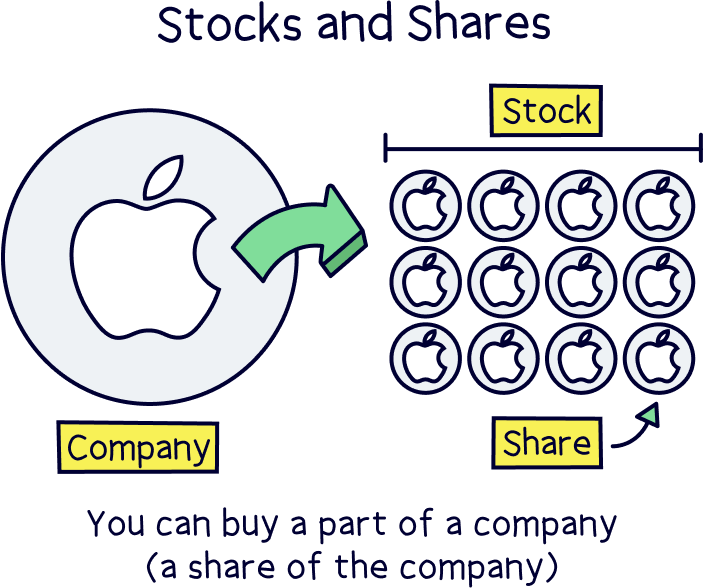

Explainer: Stock markets are where stocks and shares (very small ownership stakes in companies) are bought and sold around the world. Generally, if the companies that you invest in do well, the value of those shares go up. When you come to sell them in the future, you will get more back than you invested in the first place.

Imagine it like this: Your regular Cash ISA or savings account is like a safe kept with an ISA provider. It’s yours, and you can either put more money into your safe or take it out when you need to.

With a Stocks and Shares ISA, you still give your money to your ISA provider, but instead of keeping it locked in a safe, they make sure it gets invested smartly in the stock market. It’s all handled by experts that know how to grow money safely over time, so you don’t have to do anything.

When you put more money into your Stocks and Shares ISA, you’re asking your ISA provider to invest (buy) more. When you take your money out of your account, your stocks and shares are sold and you get the money they make from selling them.

And there’s an extra financial bonus when it comes to Stocks and Shares ISAs:

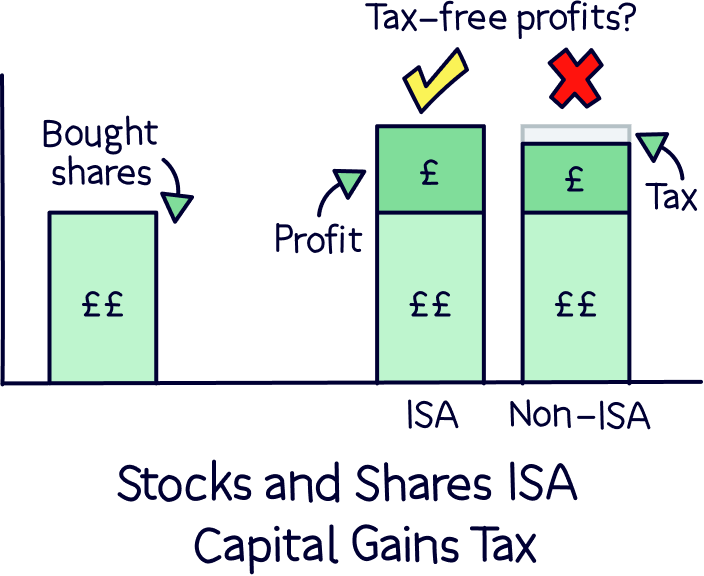

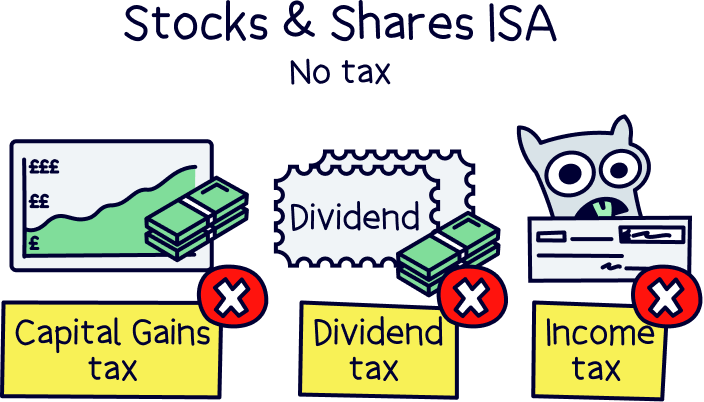

If you owned shares in a company and they grew in value, you’d have to pay something called Capital Gains Tax. That’s because the extra money (or capital) you make is growing (or gaining) – in other words, money you’ve made. But, if you’ve put money into the stock market through a Stocks and Shares ISA and your investment grows (hopefully by a lot!), you don’t have to pay this, or any tax at all.

When you put your money into a Stocks and Shares ISA, you’re not strictly saving — you’re investing. This means your cash is used by your ISA provider for investments in:

The average returns on a Stocks and Shares ISA (managed by experts) can be around 7-8% per year on average over time. If you’d invested your full £20,000 that year, you may have been up £2,600. That’s wildly different from a Cash ISA.

Bear in mind that even if your returns aren’t quite this high, you’ll still come out with a really healthy payback over the course of 5-10 years. Stocks and Shares ISAs are a long-term play, so even if the stock market fluctuates, you’ll ride it out and should come out on top.

Put simply: you can’t guarantee how much you’ll earn from a Stocks and Shares ISA, but it’s fair to say that it’s likely to be a heck of a lot more than you would earn with a Cash ISA over time.

If you’re a UK resident over 18 years old, or a crown employee living/working abroad (for example, if you’re in the armed forces), you can open a Stocks and Shares ISA.

You don’t have to pass an economics exam, or bring a list of stocks and shares yourself (although some ISA providers let you choose exactly where to invest your money). And you don’t need to check how the stock market does each day. It’s all handled for you by experts. You can just sit back, relax and watch your money grow over time.

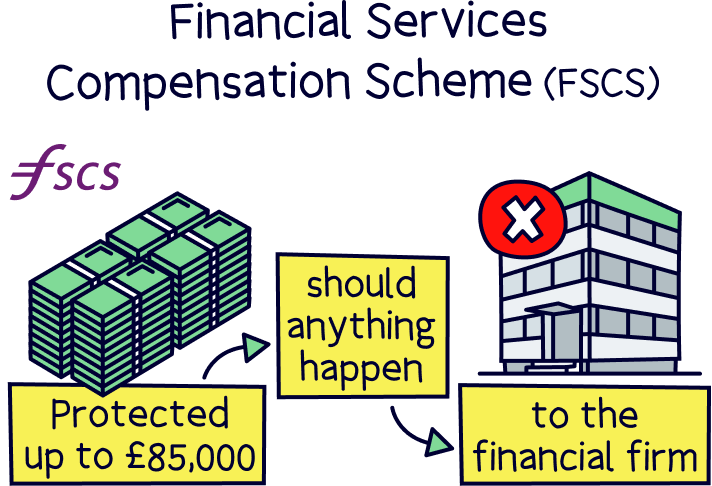

Your money is extremely safe in any type of ISA. If your ISA provider goes out of business (which is extremely rare of course), you’re protected up to £85,000 by something called the Financial Services Compensation Scheme (FSCS). In addition, as your money is in the investments themselves, you have extra protection and they would still exist and be all in your name, and they can only be returned to you.

The money you invest can go up and down with this kind of ISA. This is the reason why a Stocks and Shares ISA makes most sense when you want to set your money aside for 5 years or more, because over time there will be more ups than downs. This means you’ll ride out the bumps and your money should grow over the long-term, providing it is invested wisely (tip: just use an expert-managed Stocks & Shares ISA to make investments for you – more on these below).

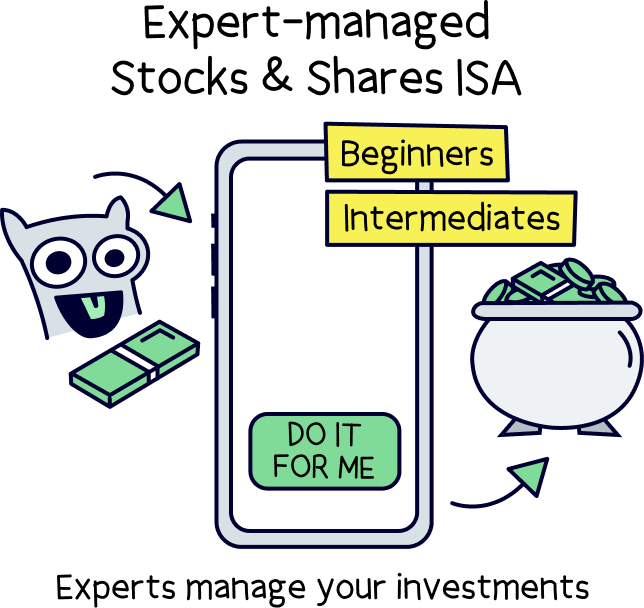

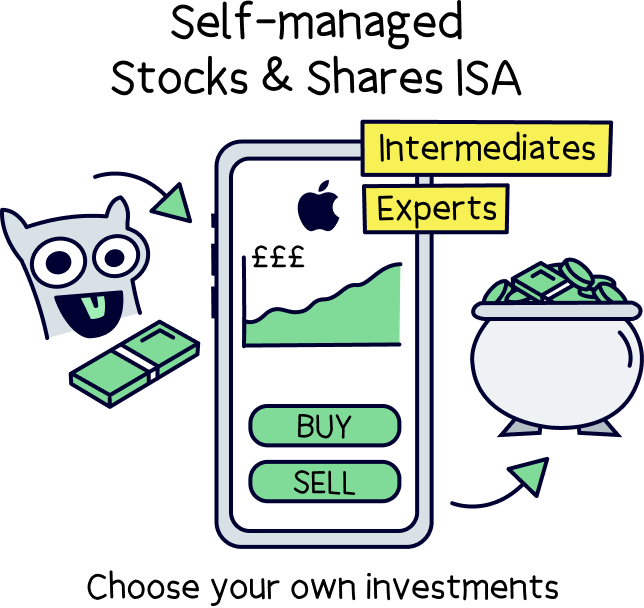

There’s only 2 main types. You can go for an ISA managed completely by the experts, you just sit back and watch your money grow. Or, you can opt for a ‘do-it-yourself’ Stocks and Shares ISA, where you’d pick the investments you want to make.

If you’re a beginner to Stocks & Shares ISAs, go for an expert-managed ISA. And, even if you’re a savings pro, it’s often best to use an expert-managed ISA too – let the experts do all the work, you just sit back and relax.

If you wanted more control over your investments, such as buying shares in a specific company or a specific fund, then a self-managed ISA might suit you better.

Let’s get into each type a bit more…

These are your ‘standard’ Stocks and Shares ISAs, and if you’re new to investing these are the ones for you. All you need to do is add money!

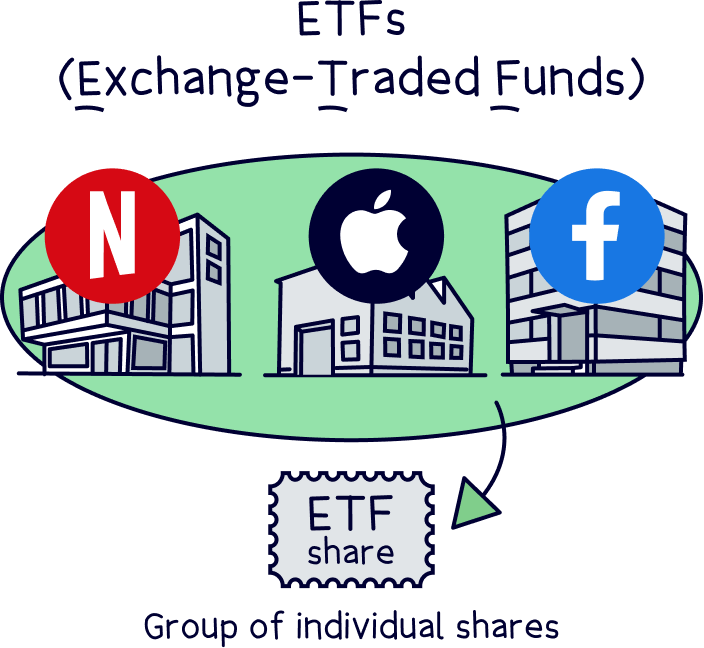

The Stocks & Shares ISA provider you choose will work with an investment fund and those experts will take care of everything related to how and where your money is invested – which will normally be invested in shares across a wide range of large, successful companies normally via investment funds (exchange-traded funds, ETFs).

With some ISA providers, to make things even simpler and cheaper, you can opt for a ‘robo-advisor’. This is where the computers take over, and determine which companies and funds your money is invested in. Don’t fear though, they’re actually really good at making money!

This is actually quite rare though, most robo-advisors are actually run by people – it’s just become a term to cover expert-managed ISAs that use technology such as an app or website.

Here's our recommended expert-managed Stocks & Shares ISAs.

Think of yourself as a pro? Know your Apples from your Blackberrys? Or maybe, you’re ready to learn a bit more about investing.

A self-managed ISA gives you control of your money so that you can manage it all yourself – that means choosing, buying and selling investments.

You won’t be using the same ISA provider as an expert-managed ISA, you’ll need one that acts as a broker, which is a company that buys and sells stocks and shares for you from stock markets around the world.

Here's our recommended self-managed Stocks & Shares ISAs.

There’s also an increasing variety of Ethical Stocks & Shares ISAs out there. Investing in an ethical ISA means you know your cash won’t be invested in companies that damage the environment (so no oil companies etc), treat their workers badly, or take part in any other nasty shenanigans. It’s definitely the way forward to a healthier future, and the investment returns are just as good, in fact often better!

Opening a Stocks and Shares ISA is not so different from opening any typical savings account.

To get started, you’ll typically apply and manage everything directly from an app on your phone or through a website – it’s really as simple as that. You just download the ISA providers app, or head to their website and get started (our recommendations are below).

Plus you can use the app or website to get full transparency of your money, whenever you like, with up-to-date balances, and without ever having to speak to anyone (unless you want to of course!).

Once the account is set up, you simply transfer some money into it and you’re all set. We’d recommend you also set up a regular automatic payment into the account too (also known as a standing order) – you’ll be surprised how quickly your money builds up.

We’ve also done the hard work researching the best ISAs for you too. We carried out our own analysis on the best performing Stocks and Shares ISAs and put together the best Stocks and Shares ISAs overall. And here's the results...

Beginner to saving and investing? No problem! You’ve made a great decision to start. Investing is the best way to grow your money over time – however that doesn’t mean buying anything and everything!

If you’re a beginner it’s best to let the experts handle things for you until you learn more about investing – although it’s still a good idea to let the experts handle things if you do know what you’re doing.

Here’s the best Stocks & Shares ISAs for beginners:

Easy to use

A great and easy to use investing app. Add money from your bank or transfer your existing ISA, with the investments handled by experts. There’s a pension pot too.

The customer service is excellent, and has email and phone support based in the UK.

Beach is an easy to use investing app (and easy to set up), just add money and the experts handle everything. It’s all managed on your phone with a great app, and you can see your total savings whenever you like.

You’ll get an easy access pot (access money in around a week), which can be an ISA where all the money you make is tax-free (save up to £20,000 per tax year), and a standard account for those saving in addition to this (or who don’t want an ISA), where there’s no contribution limits (but also no tax-free benefits).

The investments are managed by experts from the largest investment company in the world (BlackRock). And they consider things like reducing climate change, meaning your savings could make the world a little better in future too.

There’s also an optional pension pot to save for retirement, so you can keep all your savings in one place, and if you’ve got lost or old pensions, Beach can also find them and move them over too.

Fees: a simple annual fee of up to 0.98% (minimum £4.99 per month).

Minimum deposit: £25

Customer service: excellent

Pros:

Cons:

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.

Take control and manage your own investments – from picking individual stocks to finding new growth funds. The power is in your hands.

Here's the best Stocks & Shares ISAs:

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.

Get up to £100 free share

Lightyear is an awesome mobile app with very low cost investing.

There’s a decent range of investment options (over 4,000 stocks and ETFs), you can store multiple currencies, and the app itself is modern and super slick.

There's no account fees and no trading fees. There's also very low currency conversion fees of 0.35%, or you can hold the currency itself, and avoid this fee.

You can invest with a tax-free ISA, a regular account and a business account.

And if you’ve got cash savings, you’ll also get one of the best rates possible with their Cash ISA (it matches the Bank of England base rate).

Offers available

interactive investor (or simply ii) is a very well-established investment platform with 30 years of helping people make their money do more. They’ve successfully kept with the times, and are still a leading platform today.

ii has one of the widest ranges of investment options out there, and the platform itself (whether you’re on the website or the app) is easy to use, suited to both beginners and experienced investors.

It’s low cost overall, and fairly unique in that it charges a flat monthly fee depending on which account you’d like (e.g. an ISA for tax-free investing, or a pension to save for retirement), rather than a percentage of your investments.

ii offers a range of account types to suit your financial goals, including an ISA (which can be self-managed or managed by their experts for the same fee), a Trading Account, and a three-time Which? Recommended Personal Pension (SIPP).

Their plans start from £4.99 a month, with a range of unique benefits as you move to higher-priced plans (such as free accounts for your friends and family). There’s also useful analytical tools, which are embedded in the platform, and are great for in-depth insight into the markets, helping to make smarter investment decisions.

Trades typically cost from £3.99 per investment (buying or selling), although regular investing monthly is free. Other fees apply too, depending on what you’re investing in.

If you’ve got a larger portfolio, ii’s flat fee makes investing very low cost. And if you’re just starting out, it’s still low cost overall, but the monthly fee will be a higher proportion of your investments while you’re building up your portfolio.

The UK-based customer service team is excellent and award-winning, with both online and phone available (which is very rare these days).

Overall, we think ii is great, and definitely worth checking out to see if it’s right for you.

Best for: experienced investors with a growing portfolio (benefit from the flat fee)

Nuts About Money rating: 5 stars

Fees: low

Minimum deposit: £25

AJ Bell is well established, with a good reputation.

It's one of the cheapest traditional stock brokers out there (charging a low annual fee).

There's a huge range of investment options – pretty much every investment out there (including both funds and shares).

The customer service is great too.

Overall, it's one of the best options.

The fees on Stocks and Shares ISAs can sometimes be a bit confusing. This is because there tends to be a mixture of different fees for the different services.

But don’t worry, they’re typically all rolled into one fee that the ISA provider will sort out automatically, which will come from your investment. And it’s not often a lot of money, you’ll still be making a lot more than other savings accounts even with this fee.

The fees involved are often:

Overall, these fees are pretty low and not much for the amount of money you could make. Let’s say you’ve invested £20,000 and it’s grown by 13%. You now have £22,600 in your ISA. If your fee is 0.3%, that’s an annual fee of just £67.80.

Practically, making a Stocks and Shares ISA withdrawal is almost as simple as taking money out of your bank. Just hit withdraw on the app or website. The only difference is it could take a few days to land in your bank account. Why? Your ISA provider will need to sell your investments, which can take a few days.

However, always try and play the long game with a Stocks and Shares ISA, and try not to withdraw your cash unless you really need it – that way you’ll be making more money over time.

You can have as many ISAs as you like, and open as many new ones as you like each tax year too. The only limitation is you can only save into one Lifetime ISA each tax year.

An investment platform is a place to buy and sell investments, such as stocks and shares and investment funds, and normally suited for experienced investors. They’re online, via a website and normally a phone app.

You can open your Stocks & Shares ISA on the investment platform as an account option, and then make your investments within the account and benefit from all the tax benefits (i.e. no Capital Gains Tax on your profits, and add up to £20,000 per year).

Our best Stocks & Shares ISAs above are investment platforms – most modern places where you invest can be called an investment platform (unless it’s somewhere that just handles savings account such as a Cash ISA provider).

Learn more about investing and find more options with our best investment platforms UK.

An investment portfolio is all of your investments grouped together – so everything you own! It effectively represents your net worth (that’s how much you are worth personally).

Most investment platforms or investment apps will call the amount you have on their platform your portfolio, but really it’s everything you have across all the different investment accounts you have with all the different providers (if you have more than one), plus your cash too.

The Financial Services Compensation Scheme (FSCS) is a scheme set up by the government to protect you when you use a financial services provider such as a bank, a pension, a mortgage and of course investments.

So when you save money within a Stocks & Shares ISA, you are protected by the FSCS – and that means that if the ISA provider goes out of business, you’ll get up to £85,000 back.

However, most of your money would actually be within the investments themselves, and they’ve got even more protection – they’re in your name, and would still exist even though your provider has closed, and they can only be returned to you.

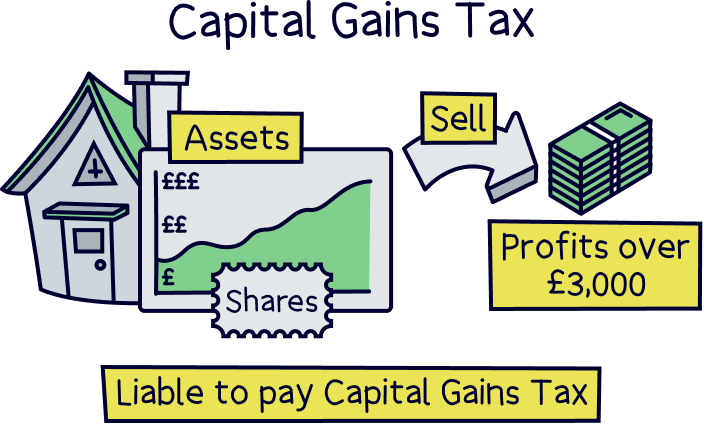

Capital Gains tax is tax you have to pay whenever something you own (called an asset), makes money – so when it’s value increases over time. Expect to pay 18% or 24% tax depending on how much you earn for investments like stocks and shares and investment funds.

And you’ll only pay this when you earn more than £3,000 per year in profit, and you only pay it on the profit you make – that's when you sell an asset.

However, with a Stocks & Shares ISA you can forget about it completely. You’ll never pay tax on anything you make, ever!

That’s why investment ISAs are a great way to grow you money over time.

Stocks and Shares ISAs have the potential to make you a lot of money, and while they’re really accessible and less risky than you might think, you still might not feel like a Stocks and Shares ISA is for you right now.

Or, you might not be fully convinced yet – you could invest a little in a Stocks & Shares ISA and the rest in another savings account.

That’s ok. There are lots of other options out there:

A Cash ISA will give you interest on your savings, just like a regular savings account, but with the benefit of the interest being completely tax-free.

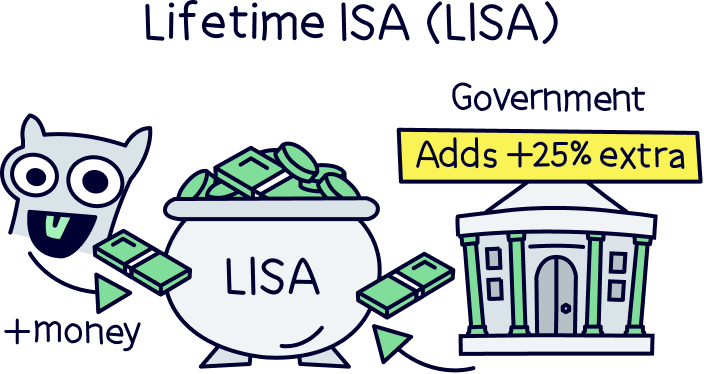

If you’re saving for your first home, you could opt for a Lifetime ISA. With this, the government will top up your savings by a massive 25% each year.

If you add £4,000 per year (the maximum allowed), that’s an additional £1,000. Amazing! The only downside is that you get a 25% penalty if you withdraw your money for any other reason than a first house deposit or after you’re 60 years old.

But it gets even better – you can get a Stocks & Shares Lifetime ISA, which means you get all the long term saving benefits of stocks and shares, with the additional 25% bonus on all the money you put in. Winning!

The alternative Lifetime ISA you could opt for is a Cash Lifetime ISA, which would give you interest on your money (similar to a Cash ISA), with the added bonus of 25% extra free!

You could also invest in a personal pension and build up your savings for retirement (often called a private pension as it's in your name, just like a workplace pension – a pension from your employer).

You’ll be able to save completely tax free, so you’ll get a bonus of 25% of whatever you put in (up to £60,000 or 100% of your earnings, whichever is lower, and across all of your pensions), and if you’re a higher rate taxpayer you can claim some of the tax back that you’ve paid 40% on too.

It’s a great idea to have a personal pension alongside a workplace pension (f you have one), so you can have a comfortable retirement with no money worries.

Here's where to learn more about pensions and find the best private pension providers.

Stocks and Shares ISAs are really easy to set up, and you’ll make a lot of money in the long-term – totally tax-free. There’s no time like the present, check out our recommendations to find the right Stocks & Shares ISA for you, and get saving today!

If you want to learn even more, here's our guide to investing for beginners.

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.