Article contents

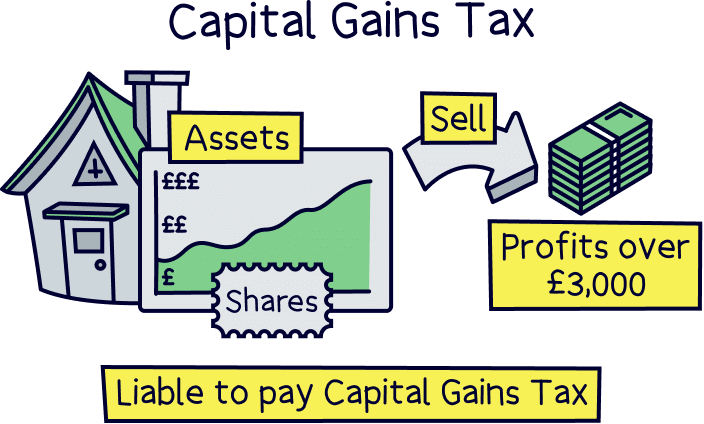

Capital Gains Tax is a tax you’ll pay on any profits you make from selling assets (such as investments or property). You’ll only pay it if you make a profit of over £3,000, which is your tax-free annual allowance. You’ll either pay 18% or 24% depending on how much you earn from your income (basic rate or higher rate taxpayer). With property it’s 18% or 28%.

Tax, you can’t get away from it, so you might as well understand it. Here we'll run through if you should be paying it, to how to pay it, and everything in between.

Capital Gains Tax, or CGT, is what you have to pay when something you own, called an asset, such as investments or property, goes up in value, and then you sell it for a profit. Meaning you have gained capital (a fancy word for money).

Say, for instance, you bought some shares worth £10,000 in a company (shares represent ownership of a company). And then the company does really well, and a few years later the shares are worth £30,000 (not bad!), and you decide it's time to sell them.

You would have made a profit of £20,000. Whoop! However, this £20,000 would be liable for Capital Gains Tax.

Let’s say for now Capital Gains Tax is 20% (more on rates later). You’d have to pay HMRC (the tax people), £4,000 of your £20,000. Not ideal, but you’ve still made £16,000 profit!

However, you might not have to pay it all. We’ll talk about your Capital Gains Tax allowance in just a moment.

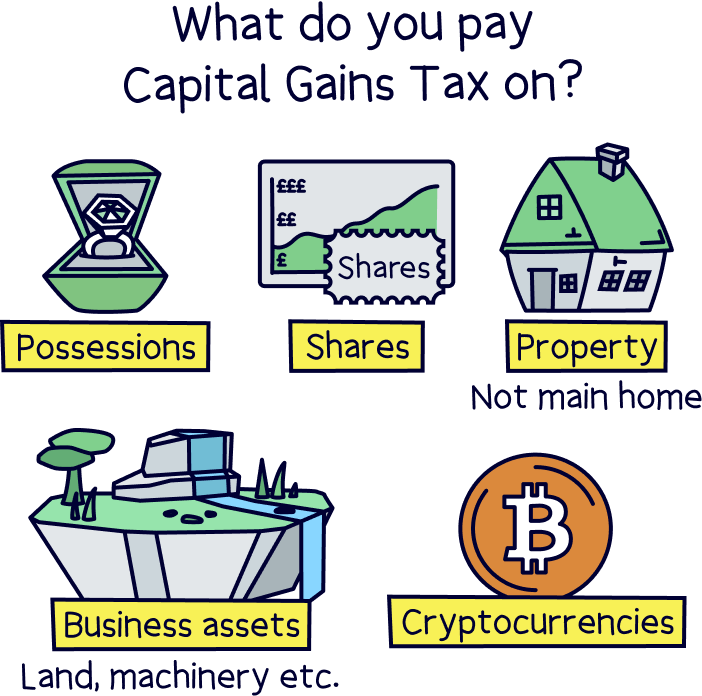

You’ll pay Capital Gains Tax on a lot of things, but there are some exceptions. And some pretty good ones. However first, let’s see what you do pay it on:

By the way, everything you’ll pay tax on is technically known as a ‘chargeable asset’.

You won’t pay any tax if it’s within an ISA (more details below), Premium Bonds, UK government gilts (loans to the government), betting or gambling winnings, and lottery or pools winnings.

If your assets are overseas, you may still have to pay Capital Gains Tax. If you live abroad you may have to pay tax on any money you make from property in the UK, however not on other assets (such as investments), unless you return to the UK within 5 years of leaving.

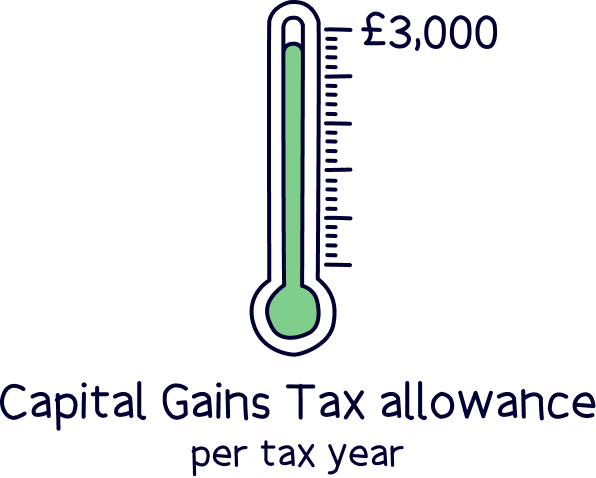

You also won’t pay any tax if the profit is below your Capital Gains Tax allowance. Let’s run through what that is.

Every tax year, which runs from April 6th to April 5th the following year, you get an allowance from the government of £3,000, which you don’t have to pay Capital Gains Tax on. This is called your Capital Gains Tax allowance (well technically the Annual Exemption Allowance). Pretty great right?

That means you can make £3,000 each year in profit from selling your assets (such as investments or property), and you won’t have to pay any tax at all.

Let’s use our same example where we made £20,000 profit and paid £4,000 in tax. Well now, thanks to our allowance, we can take away £3,000 from our £20,000, which leaves us £17,000, and that’s now what we only have to pay Capital Gains Tax on.

So our tax rate of 20% of £17,000 gives us a total of £3,400 – a bit better than the £4,000 we would have paid without the allowance.

But could it be even better? Yes, it could be inside a Stocks & Shares ISA. More on that below.

If the profit was actually inside a trust, which is an account set up to manage assets for people. For instance, someone may be too young to have the responsibility of managing a large sum of money.

Well, if there is a trust, then the Capital Gains Allowance reduces to £1,500 from £3,000.

Use Unbiased to find the right financial advisor for you.

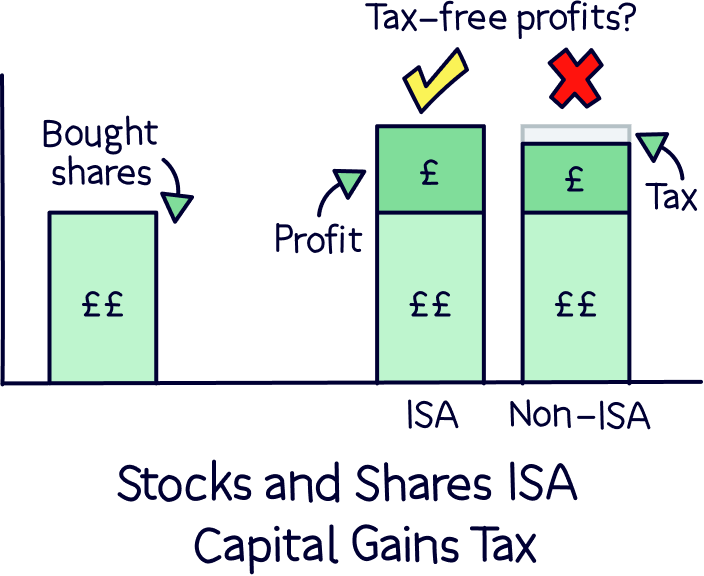

This is where it gets interesting. A Stocks & Shares ISA (Individual Savings Account) is a type of investment account, where you can buy, well, stocks and shares. The difference is it's completely tax-free! You can set one of these up by using an investment platform.

That means there’s no Capital Gains Tax to pay at all, so if we had invested our £10,000 within an ISA, and it turned into £30,000, we’d pay nothing at all on the £20,000 profit!

This is down to the government encouraging saving, and allows you to save up to £20,000 into an ISA each tax year. This allowance can be used for different types of ISAs including a Cash ISA, Lifetime ISA and a Stocks & Shares ISA.

If you want to know more about what an ISA is, here's ISAs explained.

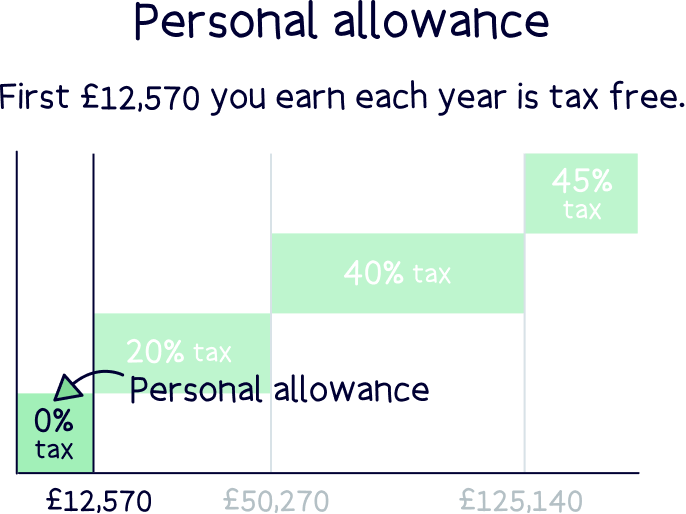

So if you’ve made over £12,570 in one tax year by selling assets. How much Capital Gains Tax would you have to pay?

It depends on how much you earn in a year, either through a salary or other forms of income.

First, you need to work out which Income Tax band you’re in, which is determined by how much total income you make, check the table below to work it out:

Now add the profits you’ve made from selling your asset, so the £20,000 in our example.

Let’s talk about the higher rate and additional rate tax bands first as they are easy to understand.

If the total of your income and the profit from selling the assets puts you in the higher rate or additional rate categories, you’ll pay 20% on your profits. As simple as that.

However, if you are a basic rate tax-payer, you’ll pay 18% tax on your profits, and 24% on any amount that pushes you over into the higher-rate bracket, so over £50,270.

If you don’t have any income, or a low income, you’ll only pay tax if your capital gain is above your Personal Allowance of £12,570.

Another way to work it out is to take your total income and minus the Personal Allowance, currently £12,570, this is called your ‘taxable income’.

For instance, if your taxable income is less than £37,700 (£50,270 - £12,570), then you’ll pay 18% Capital Gains Tax, and if it’s above £37,700, you’ll pay 24% Capital Gains Tax.

Note: if you’re in Scotland, you’ll need to use these same tax bands above, rather than the specific Income Tax bands for Scotland.

This is for every asset except property (the government likes to complicate things). Let’s run through that now.

The amount of Capital Gains Tax on property works in the same way. If you’re a higher rate tax-payer you’ll pay 24% on your profits from property and 18% if you’re a basic rate tax-payer.

If you lose money from selling an asset, you can deduct this amount from what you should be paying in Capital Gains Tax. These are technically called ‘allowable losses’.

You simply need to figure out how much you have lost, and then take that away from the profits you have made.

If you have made losses in the past 3 years, you can also use these losses for this year's figure too. You have up to 4 years to report a loss and still claim it as a reduction in your profits.

By the way, you can’t make a loss from selling or giving an asset to a family member or a ‘connected person’ such as a business partner.

If you are giving a gift to your partner, who must be your husband, wife or civil partner, then you don’t pay any Capital Gains Tax.

That’s unless you:

If they later sell the asset you gave them, they would have to pay Capital Gains Tax on the difference between the value they sold it for and the value at the time you gave it to them.

If you are giving a gift to a charity, you don’t have to pay any Capital Gains Tax.

If you are selling it to a charity however, you will have to pay tax if you are selling it for more than you paid for it, or selling it for less than the current price of the asset.

So you’ve done the maths and got some Capital Gains Tax to pay? Well done on making a profit!

Capital Gains Tax is measured on your profits within a tax year, which runs from April 6th to April 5th the following year – so anything you sell and make a profit within that year, such as investments, will count towards Capital Gains Tax (if it’s eligible).

Once you’ve worked out how much you owe, you’ll have to report it (see below). If you are within your allowance and don’t owe anything, then you don’t need to do anything. Keep enjoying life, and don’t worry about tax for another year!

With property, if you do owe something, just head over to the government website to report it as soon as you can.

If it’s not property, you will need to include it within your Self Assessment tax return, which is also online, and you would do it the year after you’ve made the gain (by 31st January). Here’s where you get started with Self Assessment tax returns. Taxfix¹ can help you with this if you want.

Hopefully we've simplified a pretty complicated topic for you! And you might have just found out you don’t need to pay any tax at all. We love to brighten your day!

And if you do need to pay some tax, at least the bright side is it’s only on your profits, so you’ve still made money. Plus, there’s not too much admin to do, as it’s all online these days.

If you are paying tax on investments, and if you’re not already using one, consider using an ISA to protect your money from the tax people, it saves a lot! Here’s the best Stocks & Shares ISA, and you could even consider a personal pension.

If you're still not sure about Capital Gains Tax, it’s worth speaking to a financial advisor. You can find the best one for you with Unbiased¹.

Use Unbiased to find the right financial advisor for you.

Use Unbiased to find the right financial advisor for you.

Use Unbiased to find the right financial advisor for you.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Use Unbiased to find the right financial advisor for you.