Article contents

A Cash ISA is a type of savings account where there’s no tax to pay on the interest at all! It’s much better than keeping your savings under your bed, but there are even better ways to save for your future.

So, you’re looking to put some of your money away for the future? Good stuff. Let’s take a look at Cash ISAs.

A Cash ISA might sound more complicated than a normal savings account. Don’t they have something to do with tax?

But, actually they’re pretty easy to get to grips with, they’re available to almost everyone in the UK, and they can let your savings grow more than they would in a normal savings account or stashing it under your bed.

Spoiler alert: there might be an even better savings option for you, we’ll run through these too so you can save your money wisely. Skip ahead.

An ISA, which stands for Individual Savings Account, is an account where you can save your money without having to pay tax on any of the money you make from, well your money! Such as earning interest on your savings.

But what about the “cash” in Cash ISA? What does that mean?

This just means that your ISA is for your cash savings, and NOT used to buy stocks and shares in the stock market (like you would with a Stocks & Shares ISA, which we also explain later in this guide).

Let’s talk about interest.

You put your money in the bank to keep it safe, but you’re also letting the bank use your money for their other services — things like loans to other customers. So you’re helping them out, too.

To encourage you to save more, the bank gives you interest, so the amount of money you have grows every year.

But, this is where the taxman gets involved. Currently, you have to pay tax on any interest you make over £1,000 per year if you’re a basic-rate taxpayer in the UK (which means you make less than £50,270 per year), or £500 per year if you make more than £50,270 per year (making you a higher rate taxpayer).

For more information on this, check out your Personal Savings Allowance (PSA).

So, let’s say you’re a basic-rate taxpayer and you make £1,150 in interest within a savings account that’s not an ISA. You’d pay no tax on the first £1,000, but the government would want their cut of the extra £150 – so you’d be paying tax on the £150.

Now, this is where ISAs come in.

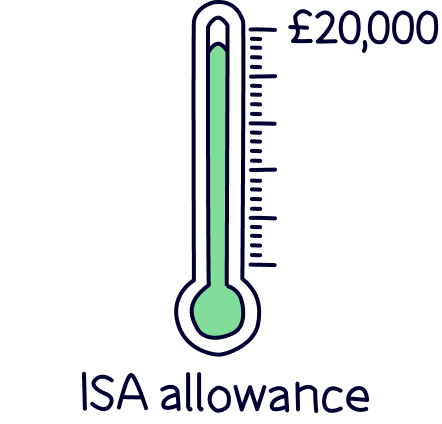

Every UK taxpayer has what’s called an annual ISA allowance, which is the amount of money they’re allowed to save, in total, within ISAs, without having to pay tax on the interest their savings make.

Currently, this allowance is £20,000. So, between 6th April and the following 5th April (which is the UK tax year), you can save £20,000 within ISAs and the taxman will let you keep all the extra money your savings make without paying tax.

Your ISA allowance can be used across all of the different types of ISAs you might have; Stocks & Shares ISA, Lifetime ISA and Innovative Finance ISA – but more on these later!

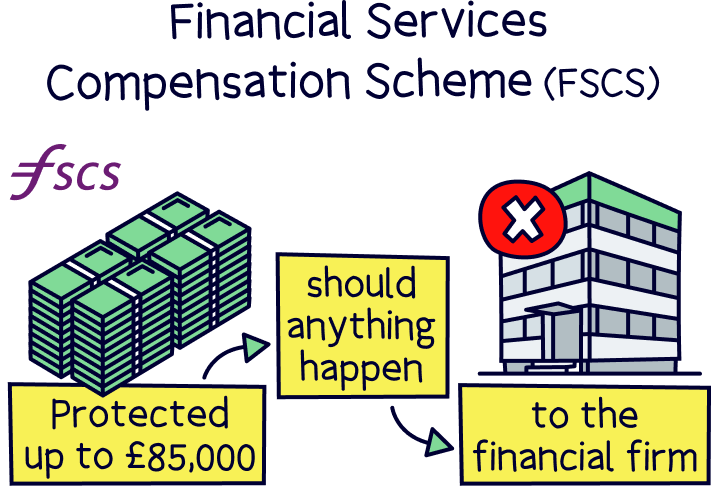

If the bank you’ve put your savings in goes out of business, £85,000 of your money is protected by something called the Financial Services Compensation Scheme (FSCS). And, if you have more than that to invest (lucky you!), you can also spread it across different ISA providers (that’s the people who manage your ISA) if you want to, which means all your savings are protected.

When it comes to Cash ISAs, there’s a few different types:

Opening a Cash ISA is super easy, you’ll normally register an account either online, over the phone, or in a high street branch. Provide some ID (passport or driving licence), transfer some money in and you’re all set.

You’ll need to be over 18 and a UK resident to open a Cash ISA.

The slightly harder bit is finding the best deal out there, but don’t panic, we’re here to help.

It’s best to look around for the best deal, your bank probably won’t give you the best rate.

Nuts About Money tip: before you rush off and get yourself a Cash ISA, we recommend learning a bit more about Stocks & Shares ISAs. They’re not as scary as you might think, safe over the long term, and you’ll make a lot more money from your savings.

Now back to Cash ISAs. To find the best interest rates you can have a look at comparison websites, who, quite handily, search the rates for you. Our favourite comparison sites for Cash ISAs are:

We recommend using a Stocks & Shares ISA. Learn how it compares with a Cash ISA.

These guys tend to have the best rates as they search the most ISA providers. They’ll show instant access ISAs and fixed-rate ISAs. It’s super easy to use too.

They search less ISA providers, but can sometimes have different deals. So it’s worth checking them too.

We recommend using a Stocks & Shares ISA. Learn how it compares with a Cash ISA.

It’s often a good idea to move your Cash ISA around to get the best interest rates, as new Cash ISAs can pop up with better interest rates, or your fixed-rate deal might have come to an end – so a great time to switch to a new deal.

What you want to do is transfer your ISA, rather than close your ISA account and open a new one. It’s super easy to do. In fact, your new provider will handle it all for you.

While we think Cash ISAs are a solid tax-free way to save money, the current (very) low interest rates mean you actually won’t see your money grow much over time.

Let’s say you have a 5-year fixed-rate ISA with a 1% interest rate. If you put £10,000 into that Cash ISA when you open it, you’ll get £100 in interest by the end of the first year.

If you just left that £10,000 in there without adding any more savings for the rest of the 5-year fixed-rate period, you’d end up with roughly £10,500.

Not bad, but not exactly mind-blowing, right? Luckily, there are some alternatives. But first…

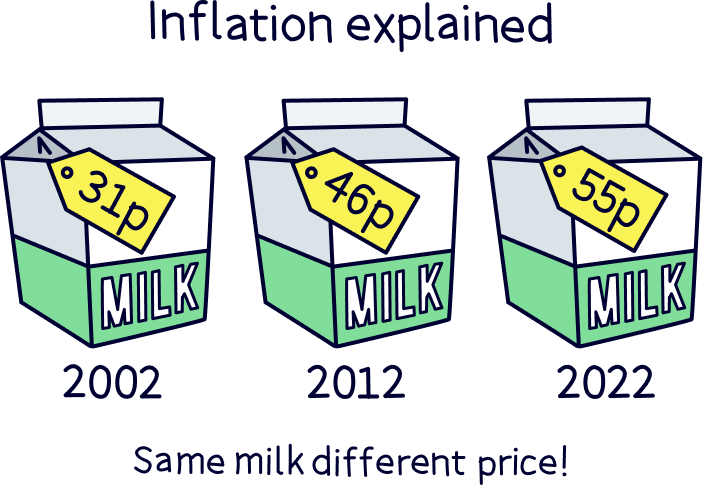

Inflation? Say what now? Inflation is the increasing cost of goods and services over time. With increasing inflation, the cost of living gets higher – which means everyday things get more expensive, things like food and petrol.

For example, a pint of milk cost around 31p in the year 2022, it's 55p – nearly double!

So, why is this important?

Over time, the value of your money (in other words, what your money can buy) will go down, and you’ll actually be becoming poorer as your savings aren’t keeping up with inflation.

How can you beat inflation and grow your money? Our first alternative to a Cash ISA is one of the best options around:

A Stocks & Shares ISA is a type of ISA where the money you save is invested in the stock market. It’s not as scary as it sounds – a Stocks and Shares ISA is actually really safe and reliable, and investing like this will help your money grow much more.

Explainer: The stock market is where stocks and shares (basically, small ownership stakes of businesses) are bought and sold all over the world. So, buying a share is buying the ownership of a company, and if the company does well, the value of your share goes up as the value of the company goes up.

If you can play the long game, you’ll ride out any bumps in the stock market and should make significantly more money from what you put in – don’t worry, you don’t need to actually do anything, the experts will do everything for you.

As a general rule, the annual return on a Stocks and Shares ISA is higher than inflation.

It’s true that your investments can go down as well as up in the short-term, but a Stocks and Shares ISA will almost always outperform a Cash ISA over the long term.

We recommend you try out a Stocks & Shares ISA, even if it’s only using part of the money you have available to save or invest. By the way, you can get ethical Stocks & Shares ISAs too.

Don’t forget: you can have multiple types of ISA at the same time – so you could spread your money between a Cash ISA and Stocks and Shares ISA.

If you want to learn more, we've written about Cash ISAs vs Stocks & Shares ISAs.

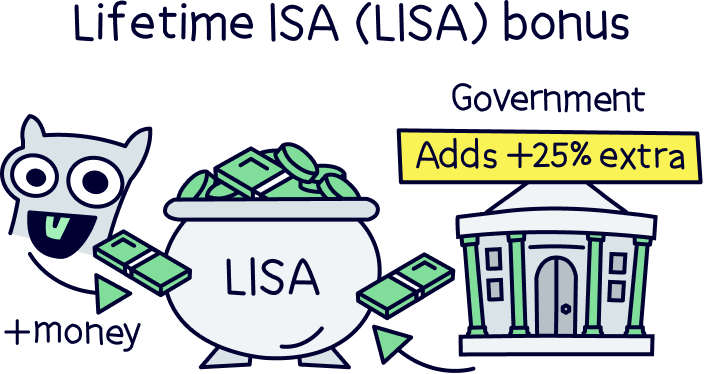

A Lifetime ISA is like supercharging a Cash ISA or Stocks and Shares ISA – you get a massive 25% bonus from the government on the cash you put in!

Too good to be true?

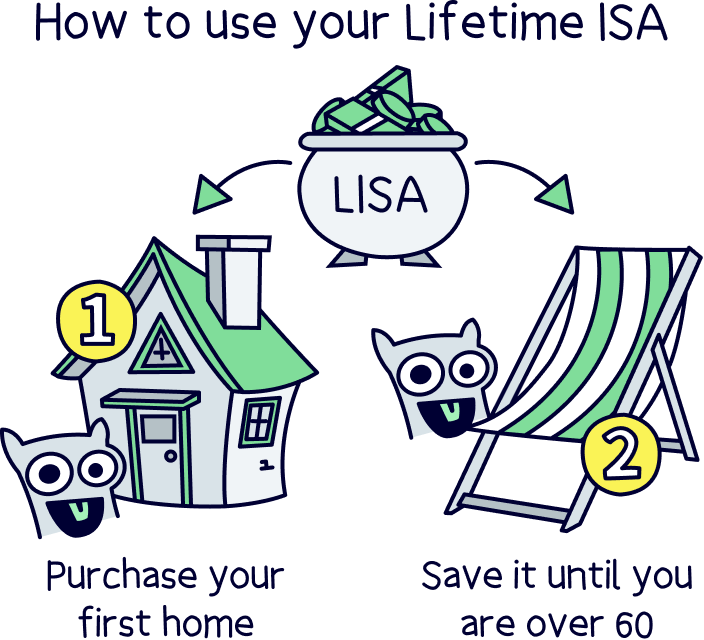

Well, it’s designed for younger people who are saving for their first home (or sometimes later in life, only withdrawing the money when you’re over 60) – and it can only be used for these reasons or you’ll face a 25% withdrawal fee (ouch!).

You can open one between 18 and 39 years old, and keep paying in until you’re 50. There’s also an annual limit of what you can put in, which is £4,000.

So if you managed to put away £4,000 in a single tax year, the government tops that up by an extra £1,000. Blimey!

This is significantly more than you’d get if you were saving using a regular Cash ISA.

And, even better, you could get the long-term saving benefits of a Stocks & Shares ISA with the 25% Lifetime ISA bonus, by opening a Stocks & Shares Lifetime ISA! Win-win.

Want to learn more? We’ve got a guide on Lifetime ISAs and how to find the best one. You can’t go wrong.

Now you know all about Cash ISAs and the great alternatives – we’re looking at you, Stocks and Shares ISA, and Lifetime ISA if you’re still young – well a Stocks & Shares Lifetime ISA.

All that’s left to do is find the right ISA for you, and start saving!

For short term savings, go with a Cash ISA, for long term savings, go with a Stocks & Shares ISA. You’ll be thanking us later!

We recommend using a Stocks & Shares ISA. Learn how it compares with a Cash ISA.

We recommend using a Stocks & Shares ISA. Learn how it compares with a Cash ISA.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things savings, with many years of combined experience writing and talking about savings (and ISAs). Some of our team were top financial advisors. We understand the ins and outs of planning your finances well, how to communicate savings in an easy to understand way (we hope you agree), and of course, how to get the best savings rate for you.

More than 20 years of combined experience researching and writing about savings

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of savings companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

We recommend using a Stocks & Shares ISA. Learn how it compares with a Cash ISA.