Article contents

A Cash ISA and a Stocks and Shares ISA are both tax-free savings accounts. If you use a sensible investment strategy, managed by experts, over the long term a Stocks & Shares ISA usually performs better, your money has the potential to grow significantly more.

In this article, we’re going to help you choose between two of the most popular and common types of ISA: the Cash ISA and the Stocks and Shares ISA.

ISA stands for ‘individual savings account’ and is a savings or investment account in the UK to help you save tax-free.

Cash ISAs are a great option to stash your money that you might need soon, because they slowly grow in value (you get paid interest), and they don't go down in value. Plus you don’t pay any tax on any of the interest you earn.

Having said that, you can grow your money much more over time through a Stocks and Shares ISA. If you use the right company your cash can be invested sensibly by experts. Don’t worry — it’s not as risky as it sounds. Here's our top investment companies where experts look after your investments.

Simply put, both are great options, much better than keeping money under your bed. But investing in a Stocks and Shares ISA pays off far better in the long term.

Heads up, we’ll mention an ‘ISA provider’ a lot. This is just the company that manages your ISA (sometimes called an ISA manager). They can be either a bank, a building society, an online website or an app on your phone.

First, we’ll explain everything you need to know about Cash ISAs. If we’ve already convinced you about Stocks and Shares ISAs, head straight to Stocks and Shares ISAs article.

In some ways, a Cash ISA is pretty similar to a savings account that you’ll probably be familiar with. The big difference is that you don’t have to pay tax on any of the interest you earn on your savings. Awesome!

Explainer: Interest is the cost of borrowing money. When you put your money in an account, the bank pays you interest because they’re essentially “borrowing it” to use for their services (such as loans to other customers).

With a savings account that’s not a Cash ISA, if you’re a basic-rate taxpayer (meaning you earn less than £50,270 per year) you’ll pay tax on any interest you make over £1,000 per year. So if you make £1,150 in interest, the government would want their cut of the extra £150.

And if you earn more than £50,270 per year (meaning you’re considered a higher-rate taxpayer), you’ll pay tax on any interest you earn that’s over £500 per year. So if you made £1,150 in interest, the government would want their cut of the extra £650.

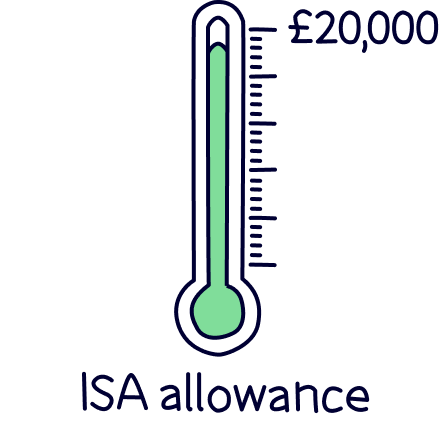

With a Cash ISA, and all ISAs, you can save up to £20,000 every year and not pay a penny in tax. Winning!

Sold on Cash ISAs? Here's the best Cash ISAs. You can also find out how much your Cash ISA could be worth in the future with our Cash ISA calculator, and find out more about Cash ISAs with our Cash ISAs complete guide.

You can get a few different types of Cash ISAs, which are:

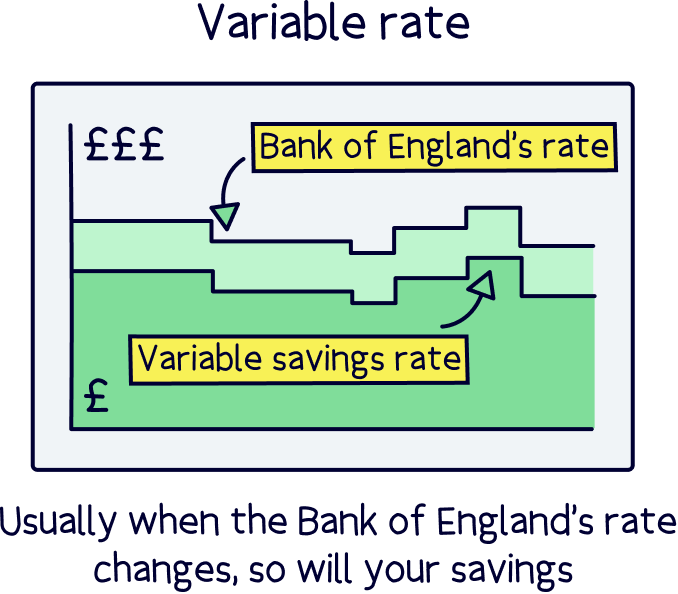

With instant-access ISAs and flexible ISAs you can withdraw your money whenever you like. But you’ll typically be getting a lower interest rate for the ability to do so. Here's the top easy access Cash ISAs.

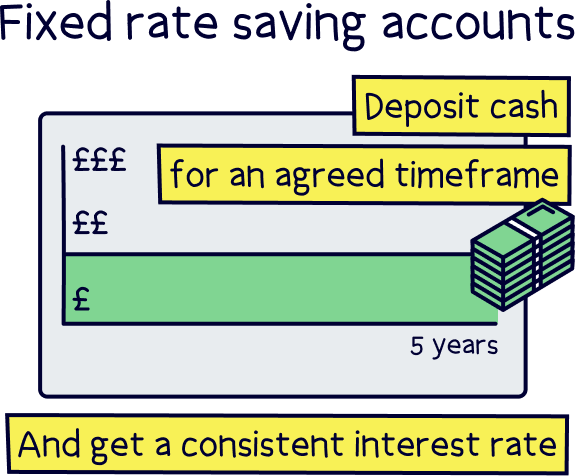

With a fixed-rate Cash ISA, you are lending your money to the bank for a period of time, usually 1 to 5 years, and they want to lend that money back out to other customers, so don’t want you to withdraw your money.

For that reason they’ll give you a higher interest rate, but add withdrawal fees to deter you from taking your money out before your deal ends. And the fees can be quite high! Here's the top fixed-rate Cash ISAs.

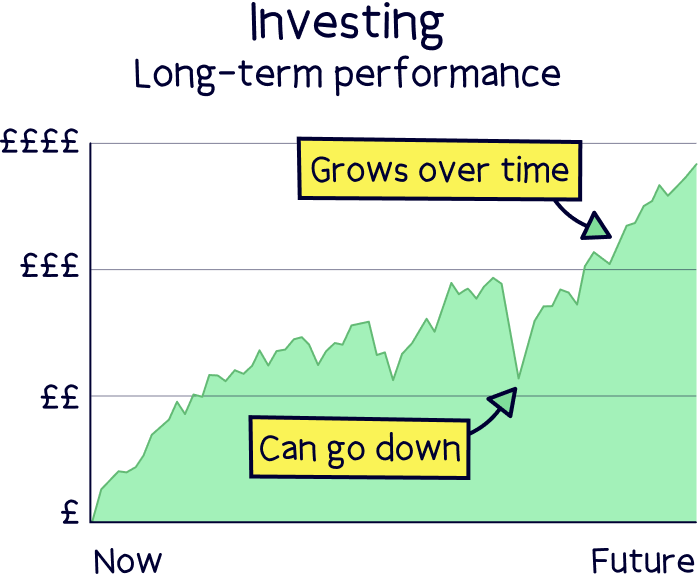

If you haven’t guessed yet, we’re big fans of Stocks and Shares ISAs. They allow you to really get your money working for you, and build up your savings over time to amounts you might not quite believe. The amount you can make is far greater than a Cash ISA.

Nuts About Money tip: see how much you could save with our Stocks and Shares ISA calculator.

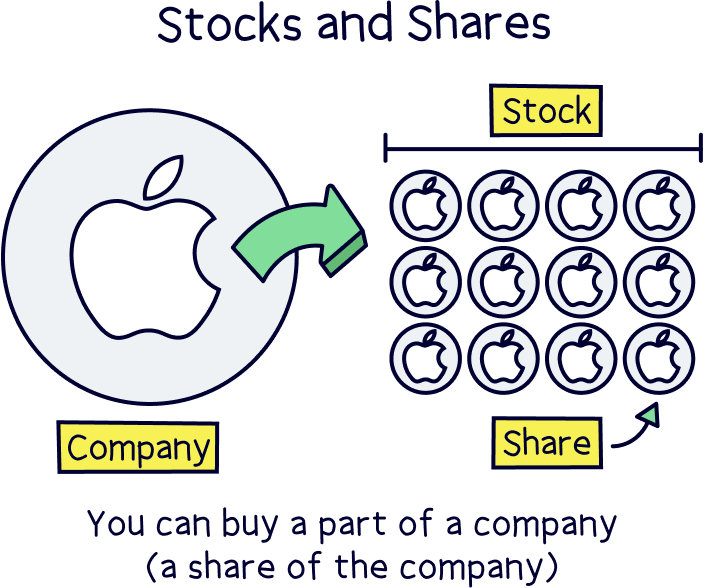

Note: stocks and shares are where you own part of a company, you own a ‘share’ of the company.

You might have heard that stocks and shares are ‘risky’, or you’ll lose money investing. Or you might even find them scary and too confusing for you. But that’s why we’re here – explaining the real facts and benefits, and how easy it is for you to get started and start growing your savings. It's all explained below.

A Stocks and Shares ISA acts like a Cash ISA, or even a normal savings account. You’ll open an account with an ISA provider (that’s a company who manages the ISA for you), put money in it, ideally regularly, and if you choose an expert managed Stocks and Shares ISA, experts will invest your money sensibly over time (explained in more detail below).

Best of all – everything you earn within your ISA is completely tax free! That’s huge.

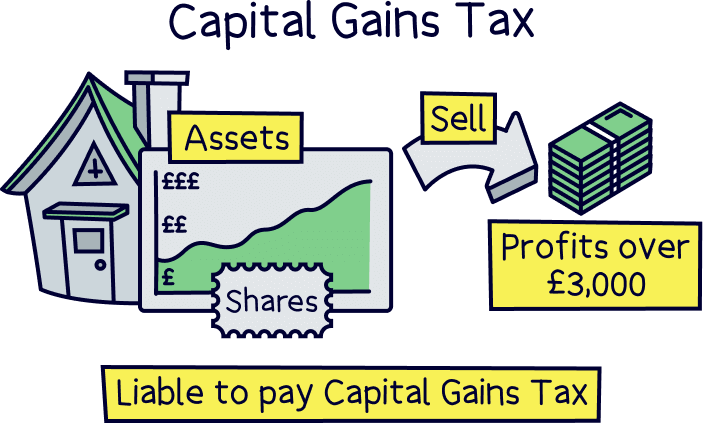

Normally if you buy and sell stocks and shares outside of an ISA, you’ll be paying Capital Gains Tax on the increase in value of your money. Capital is a fancy word for money, and if you ‘gain’ more, the Government wants their cut.

If your ‘gains’ are below £3,000, which is your Capital Gains Tax free allowance, you won’t pay any tax anyway, but if your gains are above that, expect to pay 18% if you are a basic rate tax-payer (earn less than £50,270 per year) and 24% if you are a higher rate tax payer (earn more than £50,270 per year). Plus you have to deal with the admin of actually working it out and paying it.

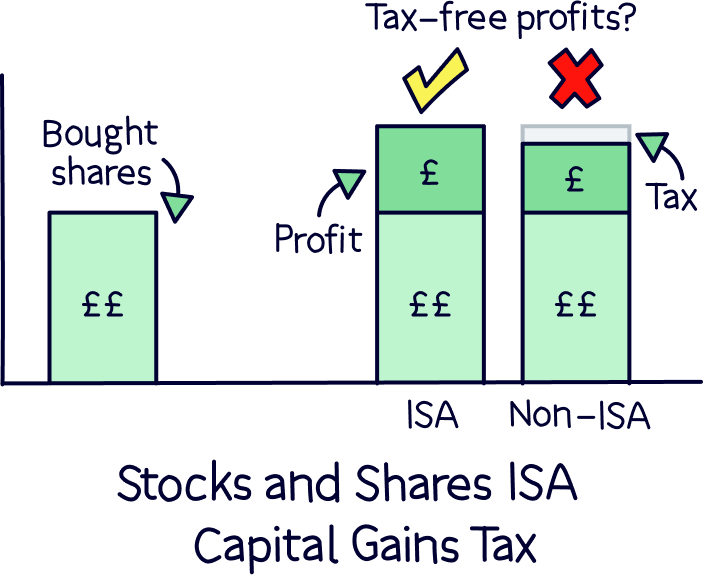

This is where the ISA comes in. All the increase of your money (gains) within a Stocks and Shares ISA, is completely free of Capital Gains Tax, forever. And that applies to any tax, so includes tax on any interest earned and tax on company profits paid out to you (called dividends). So year after year as your money grows and grows, you’ll never have to worry about paying tax at all. Result!

Better still, the money you aren’t paying in tax you get to keep invested to make you even more money, year after year, with your account growing and growing. This is called compound interest and it’s a real game changer – it’s how you can begin to make large sums of money from very small amounts.

Nuts About Money tip: find out how much your Stocks and Shares ISA could be worth in the future with our ISA calculator.

Check out the best Stocks & Shares ISAs managed by experts.

So, no tax sounds great, but how does it all work, what even is a stock and a share?

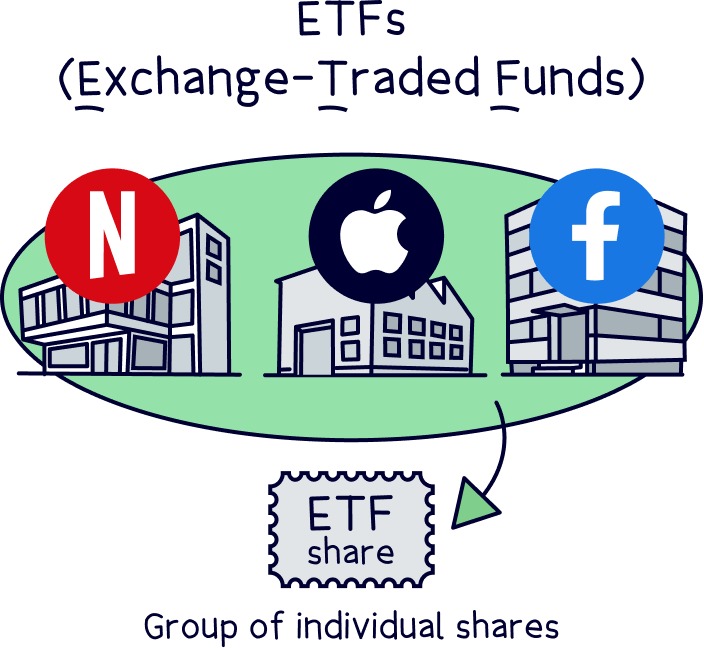

Well, your ISA provider will work with an investment fund(s), and these experts will decide how and where your money is invested. These normally consist of:

Don’t worry if you don’t understand the above, the experts can handle everything for you (if you use an expert-managed Stocks & Shares ISAs).

Your ISA provider will often give you a few options to choose from to make it simple and that’s all you need to do. For example, only investing your money in socially responsible companies (i.e. no tobacco firms, or bad energy companies) – we’re big promoters ourselves of your investments having a good impact on the world, you can make the world a better place and still make money. Go green! The future will thank you! Find out more with our ethical ISAs article.

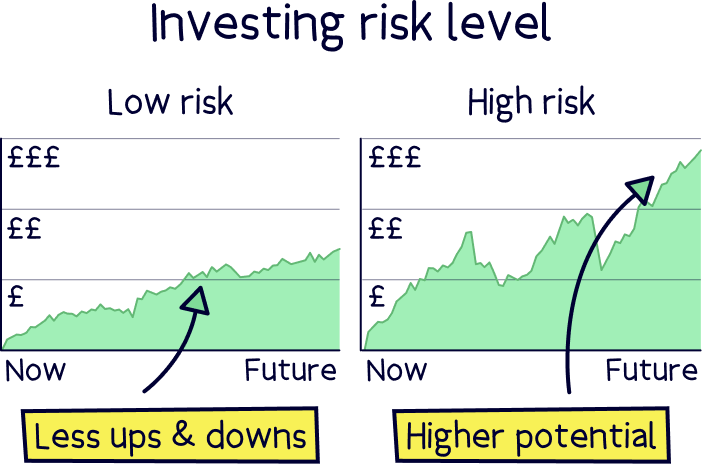

And they’ll also ask which ‘risk’ level you would like, but often suggest the best one for you – which is often dictated by your age or if you’re planning to buy something soon. For instance if you’re nearing retirement, you’d prefer the amount in your account to be more stable, so low risk, all ready for your actual retirement.

Nuts About Money tip: saving for retirement is a great idea, here's our page on pensions to learn more about saving for retirement.

If you’re young and not planning to take the money out for years and years, you’d pick a higher risk option, which means some of the investments made could be allocated to investments that have a high chance of growing a lot, but also a small chance they might not work out as expected. For instance, your money might get invested in the electric vehicle industry – where it’s highly likely to succeed and grow a lot, but not certain.

If you let the experts manage the investments, whichever risk level you choose, you won't lose all of your money within your ISA. Each investment is only a small proportion of the total investments within the investment fund, and the vast majority are safe and stable investments. Long term growth is the goal of most investment funds – and they are very good at managing risk and investments to do just that.

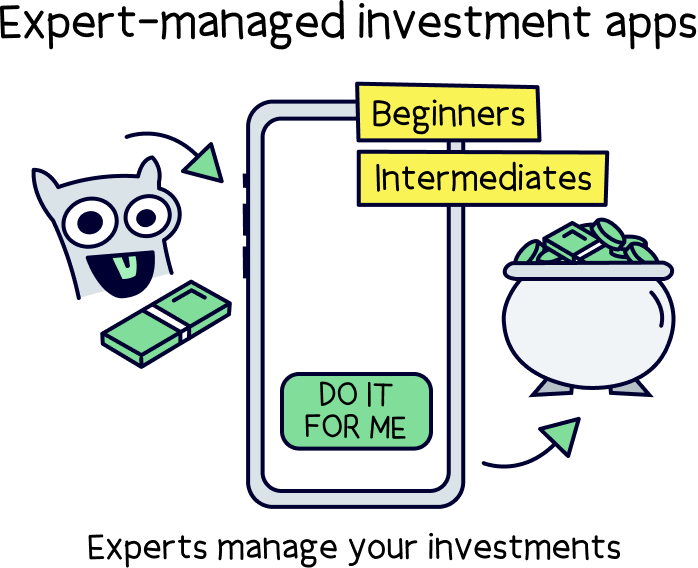

Stocks & Shares ISAs come in 2 different types, you’ve got expert-managed Stocks & Shares ISAs and then you’ve got self-managed Stocks & Shares ISAs.

With expert-managed Stocks & Shares ISAs, there’s not much to do, experts handle everything for you – all you need to do is add money! After that just sit back, relax and watch your money grow over time.

These are perfect for beginners new to investing, all the way to experienced investors who want an easy life. You can’t go wrong.

Self-managed Stocks & Shares ISAs give you much more control over your investments, you’re the one who decides where you money goes – which shares to buy, which funds to buy, and when to sell and buy investments.

It can be a bit daunting, but once you know the basics and are confident with your investments, you’re able to have much greater flexibility and a lot more options to invest your money. But, it’s not recommended for those new to investing, stick with an expert-managed ISA to start with if that’s you.

It’s worth remembering that you’re often getting experts to manage your investments and help your money grow. And more importantly, protect it, with responsible investment strategies.

It’s worth it, because it’s in their best interest to make sure you do well. Usually it means they get paid more, too – so it’s a mutual win-win.

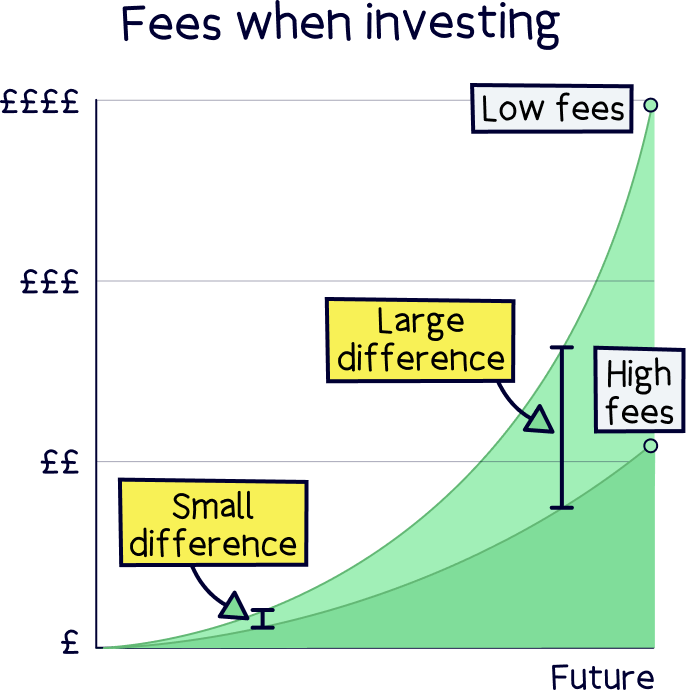

ISA providers normally charge around 0.25% – 2% for most expert-managed providers, and the lower end for self-managed providers (but there can be fees for making investments). Here's the Cheapest Stocks and Shares ISAs.

First – we don’t think you should withdraw your money unless it’s absolutely necessary. It’s better to save and grow your savings over time.

But if you have to withdraw your money from your Stocks and Shares ISA, your ISA provider will sell your investments. This will normally take from a day to a week.

If you haven’t been investing with experts for long, you might get back more or you might get back less than you put in. This is the main thing to watch out for when withdrawing from a Stocks and Shares ISA – different from a Cash ISA, where you know the interest rate you’ve been getting.

It’s worth repeating: Stocks and Shares ISAs are for the medium-to-long-term. Again, here's our Stocks and Shares ISA calculator.

Stocks and Shares ISAs have a reputation for riskiness that they don’t deserve!

Yes, your money can go up and down. But if you keep it invested for the long-term (with the help of experts), you will ride out the bumps in the stock market and come out with an impressive amount at the end. Find out how much with our Stocks and Shares ISA calculator.

Investing in a Stocks and Shares ISA is actually less risky than letting your money sit in a low-interest savings account or even a Cash ISA for long periods of time, because you’re ‘making your money work for you’. As we described shortly, you won’t get hit so badly by rising inflation devaluing your savings either.

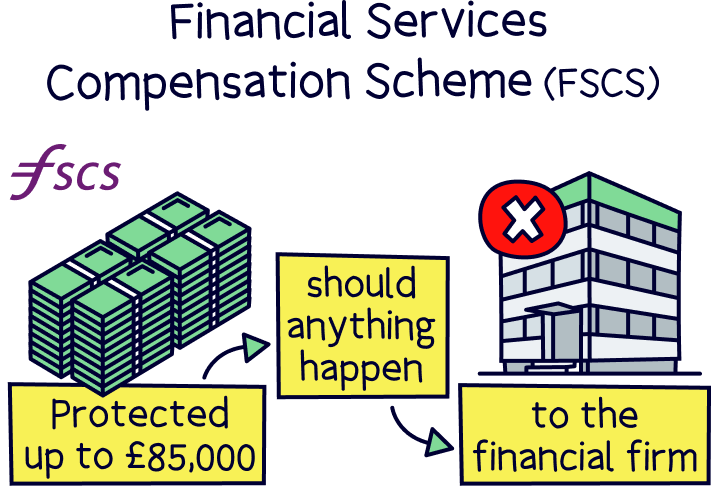

Importantly, Stocks and Shares ISAs, as well as Cash ISAs, are protected by something called the Financial Services Compensation Scheme (FSCS). In the unlikely event your ISA provider happens to go out of business, you’re covered to the sum of £85,000 per ISA provider. And usually your money is actually stored with a large bank or financial institution, not the ISA provider itself, to give you even more protection.

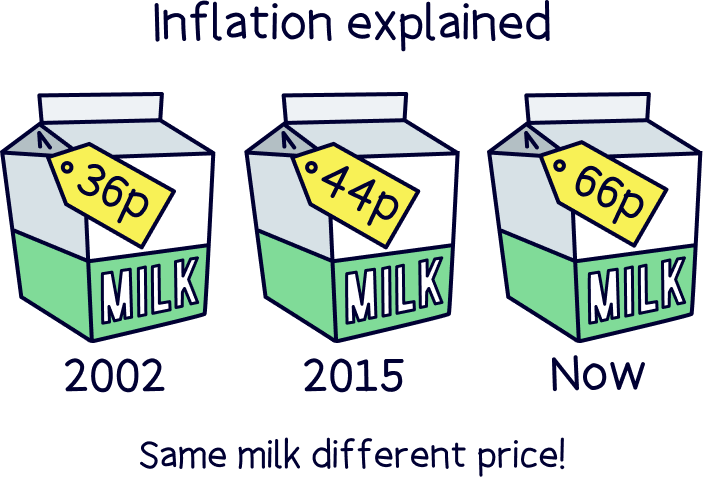

Inflation – which is a fancy word for the cost of living increasing – so your food shopping, energy bills, petrol, basically everything you’ll buy often, increasing in price.

For example, in 2002, a pint of milk cost 36p and it's now 66p – that’s nearly double the price, for the same milk carton.

Inflation is measured as a percentage, and it represents a rough approximation of the total cost of living increasing over a year.

Now let’s apply that to a Cash ISA and a Stocks and Shares ISA...

The average return from investing with experts is typically higher than the rate of inflation, and so you'll be staying ahead of inflation. You won’t get that every year, there'll be ups and downs, but on average over time you’ll be making money.

But with a Cash ISA, it's typically lower than inflation, which means your money is actually going down in value (in terms of what you can buy with your money).

We know, we know, it’s a confusing topic. But all you need to know is, inflation is bad for your savings, and you want your savings, and wages to be above inflation, or at the very least keep in line with it, or you’ll effectively be getting poorer, even though you are saving hard!

So, in terms of inflation, one of the best ways to beat it over time is with an expert-managed Stocks and Shares ISA, as on average your money growing each year is far higher than a Cash ISA. But a Cash ISA is still better than keeping your savings under your bed, as you then wouldn’t be getting any interest on your savings at all.

You can see why we love Stocks and Shares ISAs so much. And, that’s not even factoring in the tax-free savings! That’s an extra bonus.

Ok, so it’s pretty clear that Stocks and Shares ISAs offer much better returns than Cash ISAs. But Cash ISAs are still a great place to keep savings that you might need in the near future, while still gaining interest on them, all tax free.

For the medium-to-long term, a Stocks and Shares ISA is the way to go.

Let’s compare Cash ISAs and Stocks and Shares ISAs in a head-to-head battle.

Why choose one when you can have everything? That’s another great thing about ISAs – you’re allowed to open both! (Actually there’s also a Lifetime ISA you can open too, more on that below).

You’ve got a yearly ISA allowance of £20,000 per year, to do with as you like, so you could put £12,000 in a Stocks and Shares ISA, and the remaining £8,000 in a Cash ISA, for example. That’s if you’re a great saver and able to save £20,000 of course!

Nuts About Money tip: have some savings available for the short-term, while investing for the long-term with the rest of your money.

So, put simply: yes, you can do a bit of saving and a bit of investing – all through ISAs.

Back to Lifetime ISAs. If you’re saving for a house, you might also want to put your savings into a Lifetime ISA, and get a 25% bonus from the Government each year. You get a £4,000 allowance for these, which is part of your total £20,000 allowance. Here's where you can find out more about Lifetime ISAs.

There’s no time like the present – get started saving and investing!

A Stocks and Shares ISA (when left to the professionals) can help you combat rising inflation and provide a much better place to grow your money over time than a Cash ISA.

For medium-to-long term growth, Stocks and Shares ISAs are the way forward, and all managed by experts, protecting your money and growing it safely. There’s nothing to fear.

There are lots of great ISA providers to choose from, both with expert-managed and self-managed ISAs, so however hands-on or hands-off you want to be, there’s a right ISA provider for you.

Cash ISAs are also a good option too if you just want to put some cash away in a savings account for emergencies, or if you want to save some money for the short-term.

Whichever type of ISA you choose (and remember, you can have both to cover your short-term savings and long-term investing!), everything you earn from your ISA is completely tax-free.

To find out how much your Cash ISA, or Stocks and Shares ISA could be worth in the future check out our ISA calculator.

If you want to learn even more about investing, we've got a great guide to investing for beginners, and check out the best Stocks and Share ISAs, or search all of our resources on our investing home page.

Check out the best Stocks & Shares ISAs managed by experts.

Check out the best Stocks & Shares ISAs managed by experts.

Check out the best Stocks & Shares ISAs managed by experts.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Check out the best Stocks & Shares ISAs managed by experts.