Article contents

The annual ISA allowance for the 2026-2027 tax year is £20,000, which means you can put a maximum of £20,000 into your ISAs this tax year (April 6th to April 5th).

Got an ISA? Wondering how much money you’re allowed to put in it? There’s a limit to how much you can put in your ISAs and this limit can change from year to year.

Here, we’ll look at the ISA limit for 2026/27 and what that means for you.

An ISA is a pretty awesome type of savings account that helps you to save and grow your money tax-free. But there’s only so much tax-free money the government is happy to let you hide away from the taxman (after all, our taxes are what keeps the country running!).

For that reason, the government puts a limit on the amount of money you can pay into your ISA each year. And when we say ‘year,’ we’re talking about tax years (tax years run from the 6th April to the 5th April the following year, instead of running from the 1st January to the 31st December).

Your ISA limit, known as your ISA allowance, can change from year to year. However, the ISA allowance for the tax year 2026-2027 will be the same as what it was for the tax year 2025-2026.

At the moment, you can put £20,000 into an ISA each year, and that’s set to stay the same up until the end of the 2026-2027 tax year. It may go up after that but nobody knows for sure yet!

However, there are a few exceptions…

A Cash ISA, which is an account where you put your cash inside, and earn interest in return, just like a savings account with your bank, doesn’t have any specific limits.

So you can put up to £20,000 per year into one, or spread your £20,000 ISA allowance out across other types of ISAs and your Cash ISA. It’s simple.

Stocks and Shares ISAs work just the same as a Cash ISA, there’s no set limit for these types of ISAs. You can put up to £20,000 in each tax year. A Stocks & Shares ISA is an account where you can invest your money and everything you make is completely tax-free, forever!

If you invest your money outside of a Stocks and Shares ISA, you may find you’ll have to pay Capital Gains Tax on your profits above £3,000 (if you sold them).

You’d also have to pay Dividend Tax, which is a tax if a business you own (have shares in) pays out their profits to the owners (shareholders). But only if the dividends went above your £500 dividend allowance.

Plus if you earn any interest, you’d have to pay income tax (which is the same as your earnings, such as a salary).

Beach is an easy to use investment app where experts invest your money sensibly over time. Save within an Stocks & Shares ISA and/or pension pot.

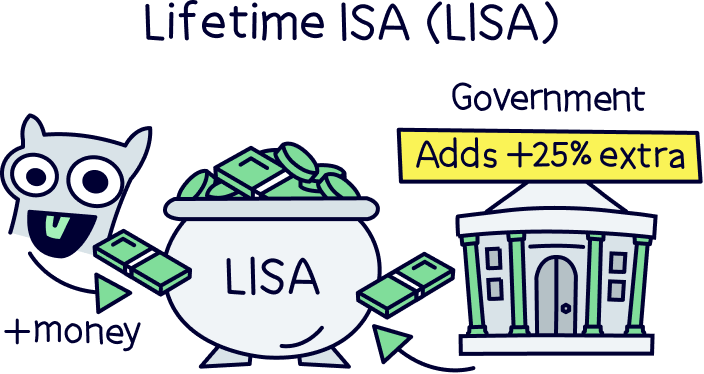

A Lifetime ISA, or LISA, is a type of ISA that helps you save to buy your first home or to tide you over later on in life. It’s particularly great because the government will add 25% to whatever you pay in! So, if you pay in £10, the government will add £2.50. Kerching!

You just have to make sure you don’t touch the money unless you’re buying your first home or you’re over 60 (or if you develop a terminal illness but let’s hope not!). Otherwise, you’ll have to give that juicy bonus back.

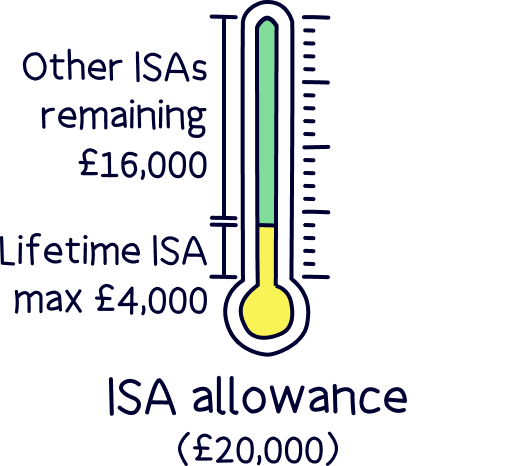

It’s worth mentioning that there’s a lower ISA allowance for lifetime ISAs. You can only pay in £4,000 each year (although you’ll still have £16,000 of your overall ISA allowance left to pay into another type of ISA if you want – £4,000 + £16,000 = £20,000).

If you're interested in getting a Lifetime ISA, check out Moneybox¹, their app is easy to use and their service is excellent.

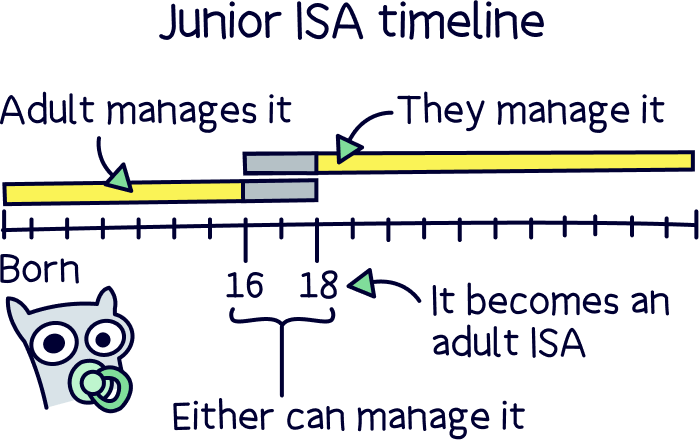

A Junior ISA, or JISA, is a type of ISA that lets you put money aside for a child under the age of 18.

Normally, you can’t open an ISA with someone else or on behalf of someone else, but junior ISAs are different. If you’re a parent or guardian, you can open one up and pay into it for your child. Any money that goes into it will officially be theirs and not yours – they’ll be able to access it once they’re 18 years old.

Anyway, the ISA limit for junior ISAs is also lower than the standard allowance. You can only pay in £9,000 per year. However, this doesn’t count towards your yearly ISA allowance – instead, you can pay £9,000 into a junior ISA on top of £20,000 into your own ISAs.

An Innovative Finance ISA, IFISA, is an account where you loan money directly to other people, called peer-to-peer lending. You cut out the large companies and banks who typically lend money, and so can often earn a higher rate of interest when loaning money directly to someone else.

There’s no specific limit for Innovative Finance ISAs, so you can put in up to £20,000 (your total ISA limit), or shared across other types of ISAs.

It’s not the cheeriest of topics, but have you ever thought about what will happen to your ISA when you die? Well, you’ll probably be pleased to hear that you can pass it on to whoever you want in your will.

At the same time, if you have a spouse or partner, they can apply to have their ISA limit increased so that they can inherit your ISA without having to go over their allowance and without having to pay tax on it. So, say you have an ISA worth £40,000. Your partner or spouse will get their normal yearly ISA allowance of £20,000, plus an extra inherited ISA allowance (also known as an additional permitted subscription or APS) of £40,000.

The weird thing about this is that your partner or spouse can get this extra allowance regardless of whether you left your ISA to them or not. In other words, your friend, parents or child might inherit your ISA if you put it in your will, but your spouse or partner will still be the one to get that lovely extra allowance. However, they’ll only be able to benefit from the extra allowance if they have more than £20,000 of their own money to put in their ISA.

We've got a whole article on Inheritance Tax on ISAs too.

In recent years, ISA providers have been able to offer flexible ISAs. This is when you can put money into your ISA, such as a Cash ISA, or Stocks and Shares ISA, and then take money back out, and then put it back in again, in the same tax year. And if you do that, it won’t affect your ISA allowance. Pretty handy right?

If an ISA is not flexible, then if you take cash out, it would simply have been ignored as part of the ISA rules on the limits, and if you then re-added it, it would count as putting ‘new’ money into your account and so count towards your ISA limit.

It’s often not a great idea to take money out of your ISAs anyway, so you can keep earning those tax-free benefits, but if you do need to, at least with a flexible ISA, it's, well, more flexible.

If you have more than 1 ISA, you might be wondering: ‘Does the ISA allowance mean I can pay £20,000 into each of my ISAs?’

We’re sorry to break it to you, but the answer is no. The £20,000 allowance is per person, not per ISA, which means if you want to pay into more than 1 ISA, you’ll need to split that £20,000 allowance across all the ISAs you want to contribute to that tax year. For example, you might decide to pay £7,000 into a cash ISA and £13,000 into a Stocks & Shares ISA (£7,000 + £13,000 = £20,000).

So, the good news is that you can put £20,000 of your savings into an ISA each year without having to pay any tax on the returns (money) it makes. Nice! This is your annual ISA allowance.

The not so good news? Well, if you have a lot of savings to squirrel away, it would have been nice if the ISA limit was increased a little instead of staying the same for years. But hey ho, it is what it is and ISAs are still pretty awesome.

In fact, if you don’t have one (or you’re thinking about getting another one), check out our recommendations for the best investment platforms out there at the moment. You'll be up and running and growing your money in no time!

Beach is an easy to use investment app where experts invest your money sensibly over time. Save within an Stocks & Shares ISA and/or pension pot.

Beach is an easy to use investment app where experts invest your money sensibly over time. Save within an Stocks & Shares ISA and/or pension pot.

Beach is an easy to use investment app where experts invest your money sensibly over time. Save within an Stocks & Shares ISA and/or pension pot.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Beach is an easy to use investment app where experts invest your money sensibly over time. Save within an Stocks & Shares ISA and/or pension pot.