Article contents

A Junior ISA is a great way to save for your child’s financial future. Choose a Cash Junior ISA to earn interest or a Stocks and Shares Junior ISA to invest in assets like stocks and bonds for potentially higher returns. When your child turns 18, the money becomes theirs, and the best part? It's completely tax-free.

Saving for your child’s future is a no-brainer, right? If you can afford to put a little extra away each month, it will soon add up and give you peace of mind that they’ll have a financial safety net when they go out into the big bad world, or a solid foundation to continue saving for a big purchase like their own home.

But how should you go about it? Well, opening a Junior ISA is a great option, and here we explain everything you need to know.

A Junior ISA (Junior Individual Savings Account or “JISA”) is a type of long-term, tax-free savings or investment account for children. It was launched to encourage families to save for their children’s futures.

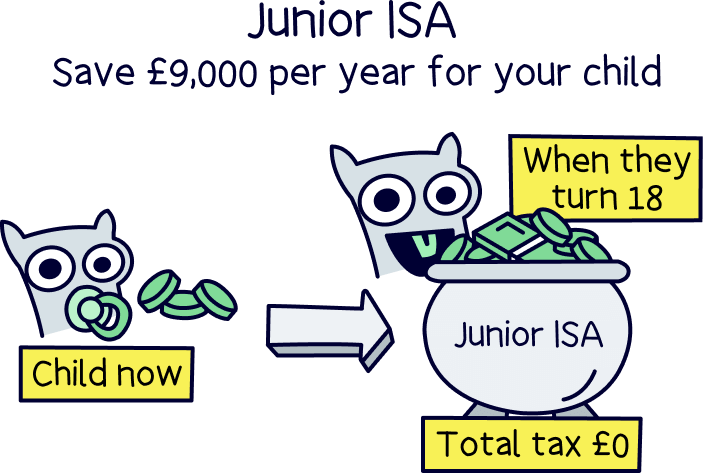

Any money you save or invest in a Junior ISA is essentially locked away until your kid’s 18th birthday, after which point it becomes theirs. We’re thinking of a nice deposit for a home, or a good base to continue saving.

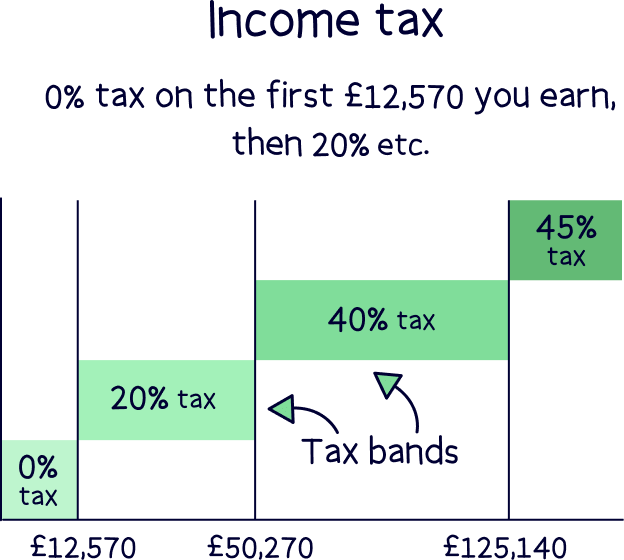

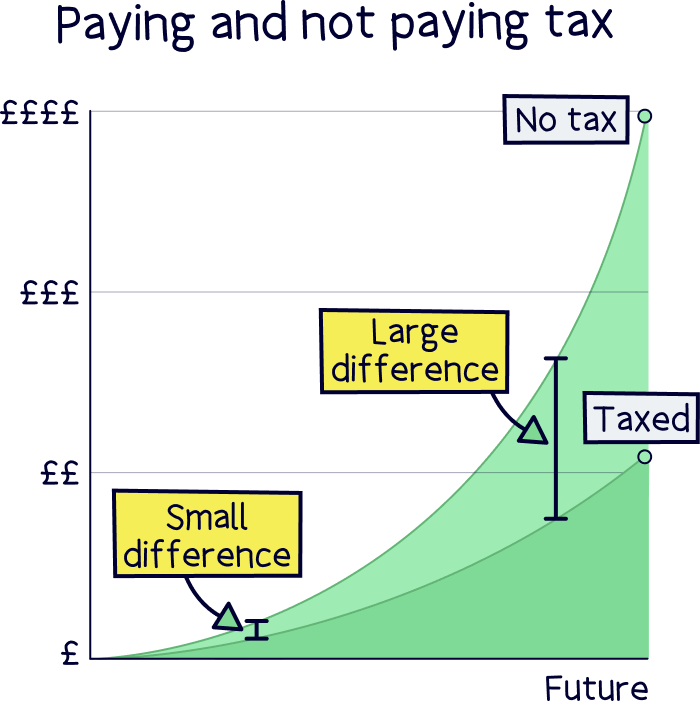

Junior ISAs have got great tax-free benefits, any money you put into one is free from any tax you might have paid if it wasn’t in an ‘ISA wrapper’ (inside an ISA account).

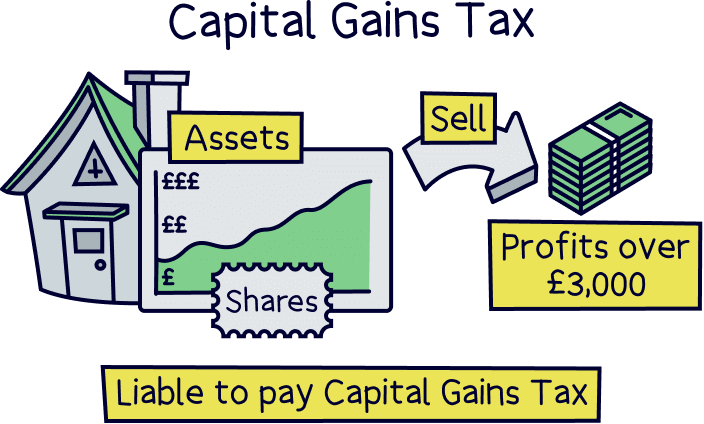

That means you save a lot of cash in Capital Gains Tax, which is paid if you sell any investments within a tax-year (April 6th to April 5th the following year), if profits exceed £3,000 per year.

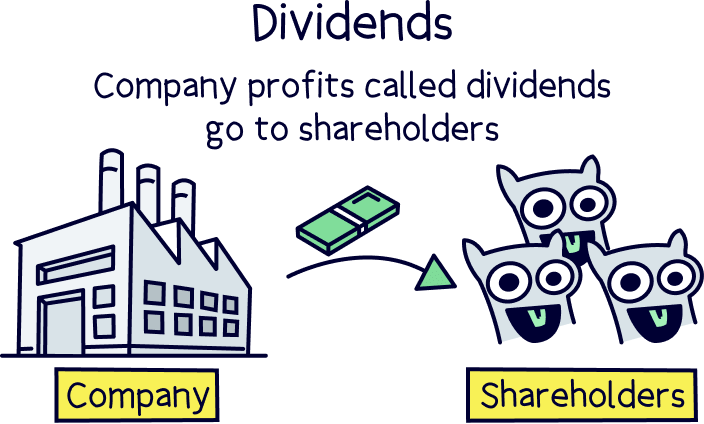

And if any investments you own pay out dividends, you won't have to pay Dividend Tax too. That’s when a business you own (have shares in), pays out its profits to its owners (the shareholders). The limit is £500 per year before you have to pay tax on them if they aren't in an ISA.

There’s also income tax, which is what you would pay on any interest you earn too. That’s the same tax you pay on your earnings, such as a salary.

If the savings in your Junior ISA starts to build up a lot, you might have to pay a fair bit of tax if they weren't in an ISA! That would mean less cash for your kid(s) in future, plus paying tax each year would slow down how quickly the savings grow.

Junior ISAs are pretty great then right?!

To open a Junior ISA, your child has to be under 18 and living in the UK (and a UK resident).

You can only open an ISA on their behalf if you’re their parent or legal guardian and a UK resident.

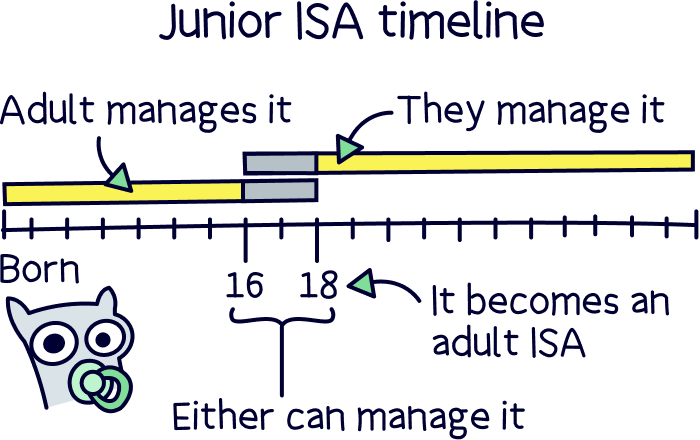

When your child turns sweet 16, they can apply to manage their own Junior ISA — but they can’t withdraw the money until they’re 18.

Anyone can pay money into your child’s ISA, including parents, grandparents, family and friends. The money in the Junior ISA then belongs to your child.

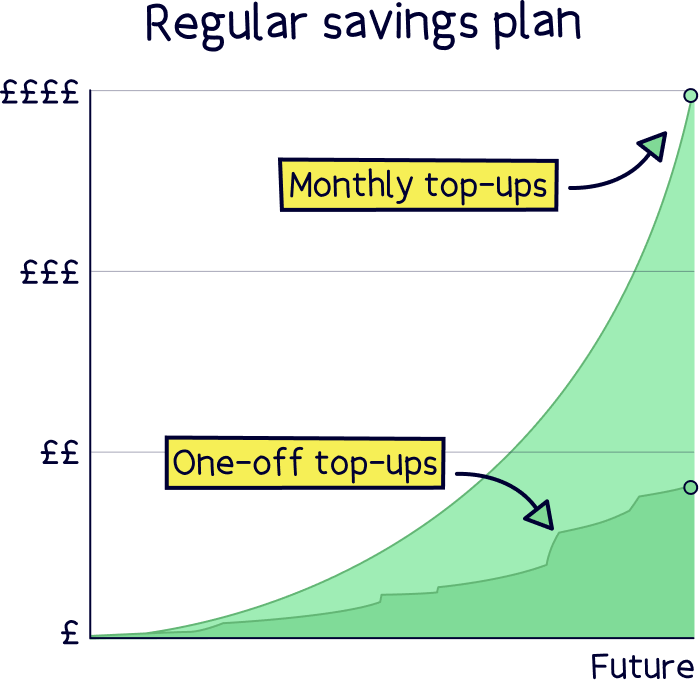

Nuts About Money Tip: to build up your child’s savings quickly, set up a regular payment each month, even small amounts add up over time. Just imagine how much you could save over 18 years!

There are a couple of different types of Junior ISA available. Your child can have a Cash Junior ISA or a Stocks & Shares Junior ISA.

This is like a regular savings account you’ll probably be familiar with – you simply add cash and get interest in return. You won’t pay any tax on the interest at all. And once your child turns 18, it will automatically turn into a regular Cash ISA in their name.

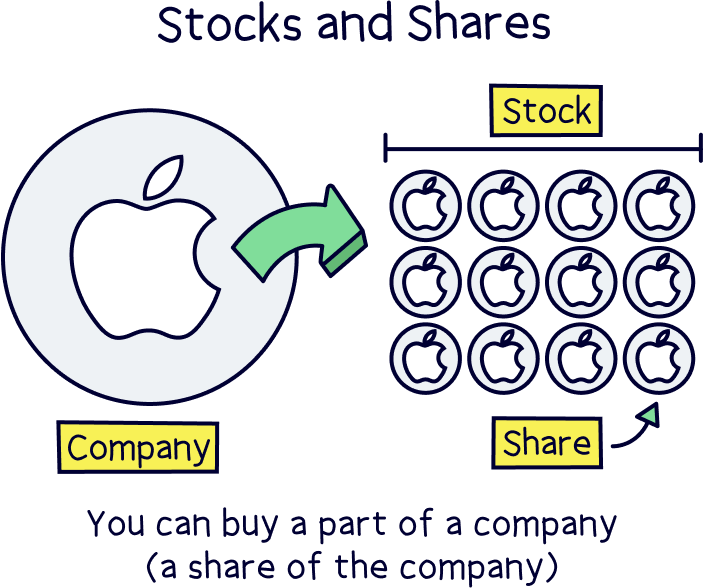

This is where your kids' savings will really grow over time. When you save in a Stocks & Shares Junior ISA, your ISA provider (the company that looks after the ISA) will work with an investment fund (the experts who manage investments) to grow your kids' savings sensibly over time – with the aim of creating a substantial savings pot by the time they’re 18 – with all the money being completely tax-free!

It will then turn into a regular Stocks & Shares ISA when they're 18.

It’s far simpler and safer than it sounds – you don’t actually need to do anything, it’s all handled for you by the experts, and they’ll invest in things such as:

Let’s assume you are opening a Junior ISA for your new born baby, or they’re just a few years old. That means you’ve got years and years of saving and the money growing until they are 18 – when they get the money themselves. Can you guess the best for long term saving?

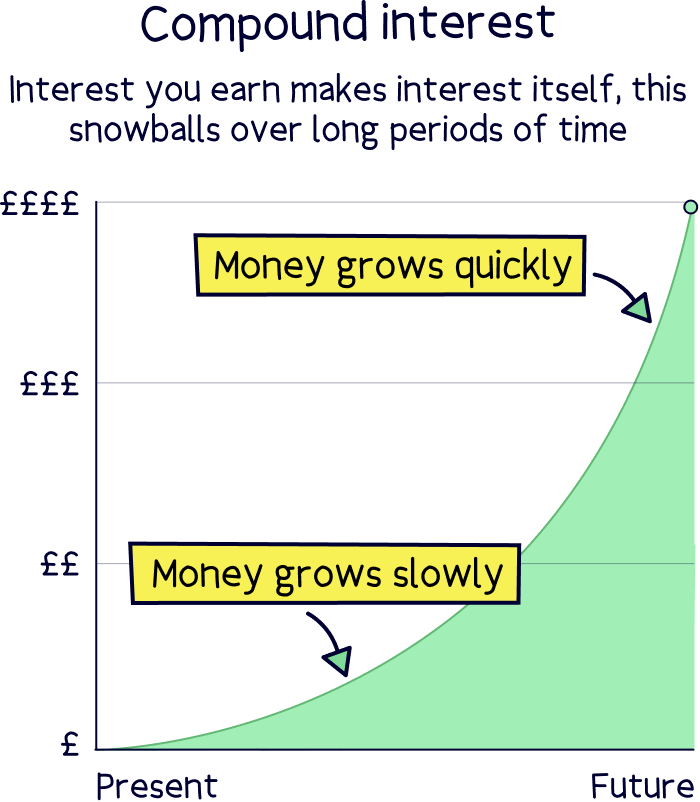

Yep, you guessed it – a Stocks and Shares Junior ISA is by far the best way to save for the future. As a rule of thumb, you could expect your savings to increase by 5-8% per year on average – and the best bit, the interest compounds. This means your interest is used to make more money, and the interest from that makes even more money. You get the idea. Over 18 years this builds up to an impressive amount!

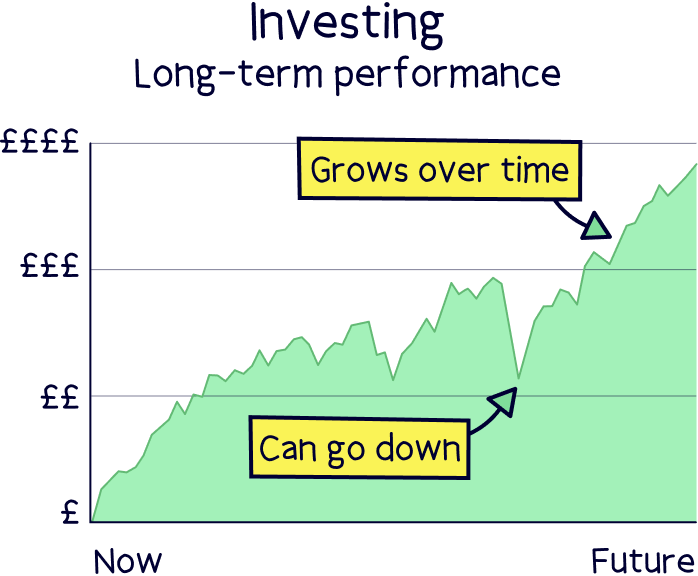

If your child is a lot older, around 15-17, you could consider a Cash Junior ISA. Why? Over a short time frame, saving in a Stocks & Shares Junior ISA could end up losing money depending on how the investments perform.

Although saying that, you could also make a lot of money too. The important thing is to have a long term view, and ideally your child would keep investing for their future after they turn 18, and not immediately spend it all on a fast car!

So, for long term savings go for a Stocks and Shares Junior ISA – your child will end up with a lot more money this way.

For short term savings, 3 years or less, and if you have a view to spend the money immediately when they're 18, you could go for a Cash Junior ISA.

You might have heard of a Child Trust Fund. This was effectively the scheme for long-term saving for your children before a Junior ISA. And was for children born between 2002 and 2011. They effectively have exactly the same benefits as a Junior ISA – so a tax-free savings account, and is your child’s account, which they’ll get when they turn 18.

You can’t open a Child Trust Fund anymore. You’ll need to open a Junior ISA. However if you already have one, you can keep paying into it.

The good news is, whichever type of Junior ISA you choose, it’s super easy to open one. And it usually doesn’t take that long, either. Not sure where to look? Here are our recommendations for each type of Junior ISA...

Moneyfarm tops the list – they’ve got a great investment record, low fees and experts on hand to help.

Beanstalk is a great Junior ISA – it's easy to use, and all works on an app on your phone.

There's simple and easy to understand options, with a choice of two funds and clever tools – perfect to build up your child's savings over time.

It's low cost too, with fees of just 0.50% per year.

Friends and family can contribute too – perfect for birthday and Christmas presents.

Moneyfarm tops the list – they’ve got a great investment record, low fees and experts on hand to help.

Moneyfarm tops the list – they’ve got a great investment record, low fees and experts on hand to help.

Tesco Bank has one of the best Cash Junior ISAs around, currently offering 2.25% per year. Although the rate can sometimes change both up and down – it’s a variable rate. It’s a simple account, which you can manage online or over the phone. What’s not to love!

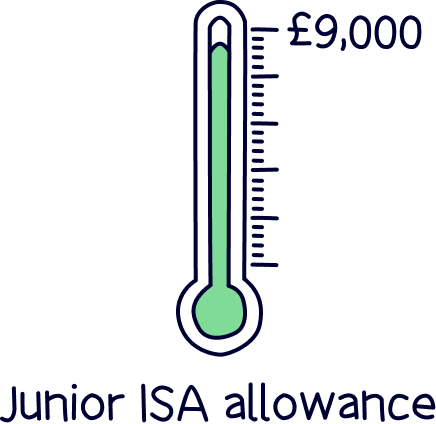

There’s only so much you can put into your child’s ISA each tax year (which runs from April 6 to April 5 the following year). This is called the Junior ISA annual allowance (A.K.A., the ‘annual limit’).

The annual allowance for a JISA is £9,000. That means you can save up to £9,000 each year tax-free.

The allowance resets at the start of the new tax year (April 6th), and you can’t carry over any of your unused allowance from the previous year. It’s a ‘use it or lose it situation’.

Yup! They might have to share everything else, but if you have more than one child, they will have their own Junior ISA allowance. No need to pick favourites!

Nope! It’s completely separate. Your ISA allowance remains at £20,000 per year.

Your child’s Junior ISA allowance is their own personal allowance. If you have your own ISA (which is a very good idea), adding money to your kid’s ISA won’t eat into your own allowance.

Your child can manage their own Junior ISA when they turn 16, but the money remains out of reach until they’re 18.

With many Junior ISA providers, when your child turns the big 1-8, their account is automatically upgraded to an adult ISA and if your child wants to continue saving and/or investing for their future they can, and of course they should!

Once 18, the money is theirs to do with as they please. New car? Gap year? Deposit on a flat? The possibilities are endless of course, but we strongly recommend keeping it invested for the long-term! And, if they can learn all about saving and investing from you, all the better!

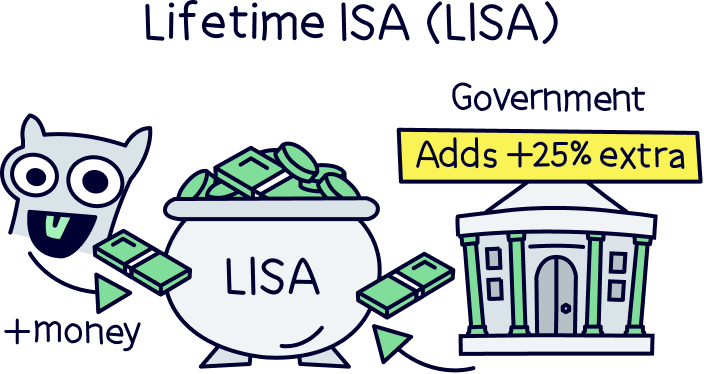

Best of all, at 18 they can open a Lifetime ISA – which acts the same as either a Cash ISA or a Stocks & Shares ISA, but with a 25% government bonus every time they pay in – with an allowance of £4,000 per year. Perfect for young savers beginning to save for their first home (the rules for a Lifetime ISA are you must buy your first home, or save it until you are 60).

Worried you might be stuck with the same Junior ISA provider for 18 years? Or maybe you’ve set one up already and want to transfer a Junior ISA to a new provider?

Well, it’s super easy to transfer a Junior ISA! All you need to do is speak to your new provider (they’re the people who will manage your ISA), and they’ll handle everything for you. It’s often completely free to do too.

By the way, you don’t have to have a Junior ISA in the same place as your adult ISA. It can be anywhere, with any provider. If you’re looking for the best ones, check out the best investment platforms, and our recommendations above.

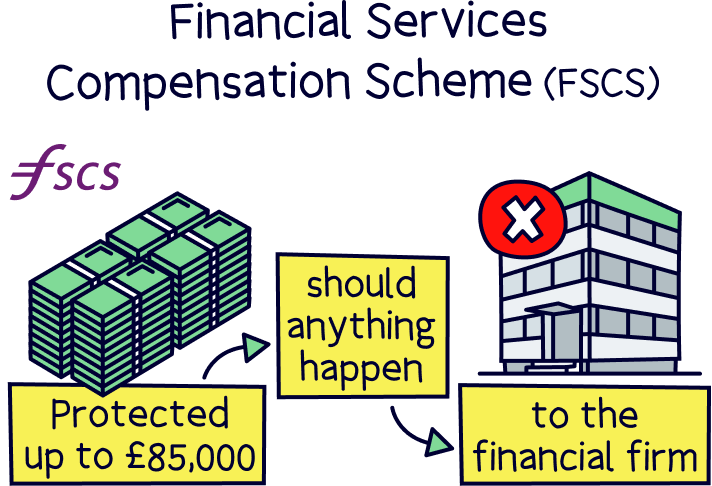

Junior ISAs can be a very safe way to save for the future. They are covered by the Financial Services Compensation Scheme (FSCS) up to a maximum of £85,000. So, in the very unlikely scenario your ISA provider goes bust, you would get your money back.

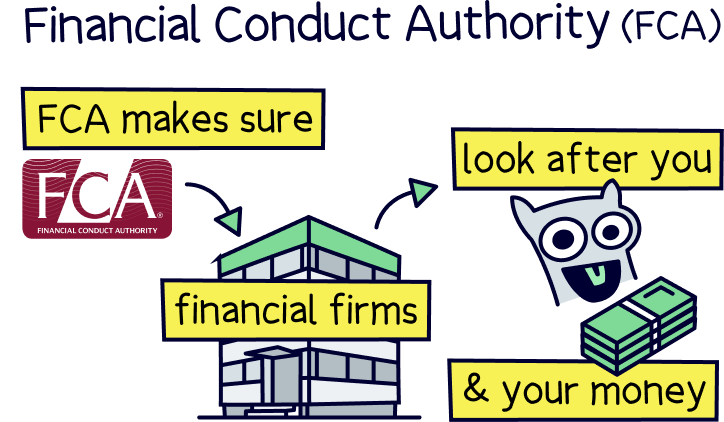

Every provider has to be authorised by the Financial Conduct Authority (FCA) too, which means they’ve been reviewed and approved to look after your money.

Stocks & Shares Junior ISAs might seem a little riskier, because you’re investing your kid’s savings in real businesses on the stock market, rather than a fixed interest rate with a Cash Junior ISA. But that’s typically not the case, investing over a long period of time smooths out any bumps in the road, and is one of the best ways to grow your kids' savings (and yours!).

It’s tough out there for young people at the moment, becoming near impossible to save for a house deposit, let alone just pay the bills – and it’s not looking to change any time soon.

Now, we don’t know what the future will hold. Nobody does. But we do know for sure that opening a Junior ISA for your kid(s) will help give them a huge boost when they become a real adult at 18 (well, kind of a real adult!). A small investment now could become a really large sum in the future – the key is to start saving as early as possible, and keep saving little and often!

Moneyfarm tops the list – they’ve got a great investment record, low fees and experts on hand to help.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Moneyfarm tops the list – they’ve got a great investment record, low fees and experts on hand to help.