Review contents

Wealthify makes investing easy and simple. We love that. Their experts handle everything for you, you don’t need to do a thing. The customer service is great, and the costs are reasonable – although the ethical investment option has higher fees. Overall, 4 stars from us.

Wealthify is one the more established ‘robo advisors’ in the UK – they’ve been around for quite a few years now and are owned by Aviva. A robo advisor is an investment company that uses technology, such as an app, which helps you invest, rather than using a financial advisor.

Wealthify helps you save and invest your money easily and simply. They offer a selection of investment options that you can buy based on your personal circumstances. And you can view your investments whenever you like on their app on your phone, or their website.

Based on your answers to their suitability quiz, they'll build you an Investment Plan with a risk level that's best suited to you. After that, their experts will handle everything – such as changing what you invest in over time. You just sit back and watch your money potentially grow.

You can open a Stocks & Shares ISA, a personal pension, a Junior ISA, or just a General Investment Account (GIA) – we’ll cover these in detail below.

By the way, the app is highly rated – it’s 4.5 stars out of 5 on the Apple App store (as of July 2026).

Let’s dive into the details and see if it’s right for you.

Yep! It’s great for beginners.

It’s designed to be as easy as possible to get started with investing. You don’t need to know anything about investing really. Their experts will handle all of your investments. All you need to do is add your hard earned money.

It's great if you want to learn about investing too. Even though they’ll do everything for you, you can learn where your money is invested and what makes things higher risk or lower risk.

And whenever you want to see your portfolio (that’s how much your investments are worth), you can log in any time and see the total plus the performance of your investments.

Nuts About Money tip: if you can, set up a regular payment every month. Your investment pot will soon add up!

Overall, it’s really simple to use – they take care of everything for you.

To get started, you first need to decide which type of account you want to use, we’ll cover these in detail below, and they’re a Stocks and Shares ISA, Junior ISA, a personal pension, or a General Investment Account (for investing outside of your ISA Allowance).

There’s no Lifetime ISA – which is a great account to help you save for your first home. Here’s where to learn more about these and find the best Lifetime ISAs.

So, once you’ve decided on the account you want, the next step is to figure out the right investment strategy for you.

The investment strategy with Wealthify is called an investment style – it simply means how you want your money to invested, and it ranges from as safe as possible to high risk (there’s always some risk with investing).

The more risk you take with your money, the more money you could make in the future, but you could also lose money too.

Here’s your options:

Designed for people who prefer a steadier approach, with low expectations of potential growth.

Takes a little more risk than Cautious, with the potential for higher growth over time.

A middle-of-the-road option that aims for higher growth than Tentative, while accepting more ups and downs along the way.

Takes more risk than Confident in pursuit of higher long-term growth, but with less volatility than Adventurous.

Designed for people comfortable with bigger ups and downs, in pursuit of the high potential long-term growth.

After that, you’ve got to choose where your money is going to be invested. And for this there’s only 2 options:

Original: this is Wealthify’s standard investment option and is a mix of investments from the UK and overseas.

Ethical: with this option, they try to avoid businesses that damage the environment (e.g. no fossil fuel companies) and are socially responsible (have a positive impact on people).

It’s worth bearing in mind that with Wealthify, the ethical option is expected to make a bit less money over time. This isn’t always the case with other investment platforms, where socially responsible options can have better investment growth (such as Beach¹).

Beach is an easy to use investment app where experts invest your money sensibly over time. Save within an Stocks & Shares ISA and/or pension pot.

This is your standard account, with no tax-free benefits. The good thing with these is you can have as many as you like, so one with any investment platform you like.

When you sell your investments and make a profit, you’ll have to pay Capital Gains Tax on any profit above £3,000 (your Capital Gains Tax allowance).

Learn more about these accounts with our guide: what is a General Investment Account?

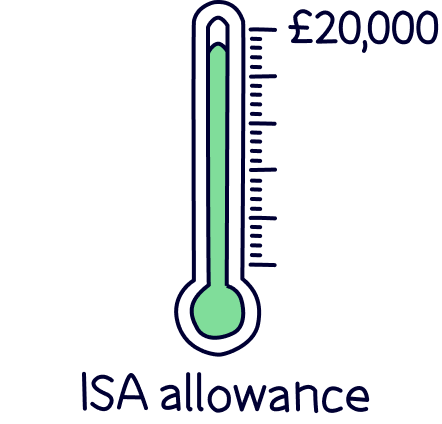

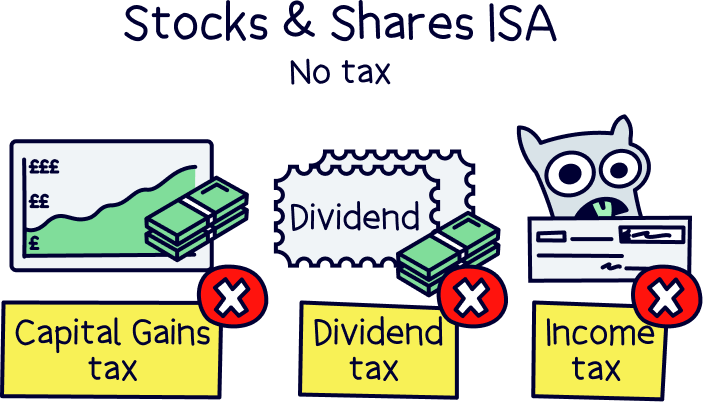

Wealthify calls this an Investment ISA. You can invest up to £20,000 per year and everything you make in the future is completely tax-free!

Note: the £20,000 is actually your total allowance across all of your ISA options, so that includes a Cash ISA and a Lifetime ISA.

That’s no Capital Gains Tax, no Income Tax, and no Dividend tax – which are all types of taxes you could pay on investments.

There's only one downside – once you've used your ISA Allowance, you'll need to wait until it resets to pay into your Stocks & Shares ISA.

That’s where a General Investment Account comes in handy. There are no limits to how much you invest in one of these – but you may be subject to tax on any potential gains you make.

If you want to learn more, here’s our guide to Stocks & Shares ISAs.

By the way, Wealthify's ISA is also a Flexible ISA. This means you can withdraw money and, as long as you pay it back into the ISA during the same tax year, it won't use any more of your ISA allowance.

A personal pension is a great idea to save for your retirement in addition to a workplace pension (that’s one your employer sets up for you, if you’re employed).

All pensions are tax-free, so the same as a Stocks & Shares ISA.However, you also get a bonus of 20% from the government on your personal contributions.

And if you’re a higher rate or additional rate taxpayer, it gets even better, you can claim back some of the money you’ve paid at those rates too (40% and 45%). You would do this on your Self-Assessment tax return (it’s easy to do).

However, there are some limits. You can only pay the total of your income each year or £60,000, whichever is lower (and this is across all of your pensions).

And you won’t be able to touch the money until you’re 55 (57 from 2028). It is for retirement after all. You may also pay Income Tax when you retire depending on how much you withdraw from your pension per year (so exactly the same as if you were earning a salary).

Learn more about personal pensions and view all the best personal pension providers.

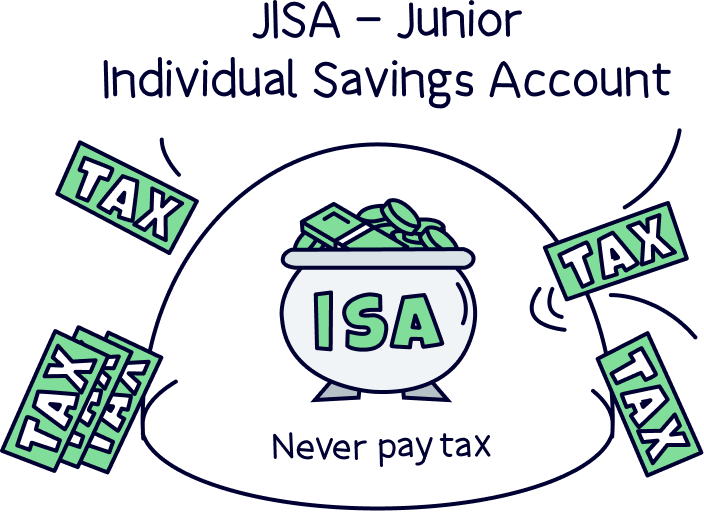

If you’ve got kids – this is a great option to save for their future.

You can set up an account all in their name, which they’ll get access to when they’re 18. And everything they make in the account is completely tax-free!

You can invest up to £9,000 per year. Pretty great right? And this is in addition to your own ISA allowance (£20,000).

Learn more about these with our guide to Junior ISAs.

Let’s get to an important bit, how much does Wealthify actually cost?

First you’ll pay an annual management fee – and this is a fee directly to Wealthify, which is one simple to understand fee, of 0.6% per year (0.6% of the total in your account).

Note: the fee for their pension will reduce to 0.3% on balances over £100,000.

On top of that you’ll also pay a fee for the investments themselves. This varies significantly between which investments you pick.

With the original investment option, the average cost is 0.14% of your total investments per year. With the ethical theme, this goes up to an average of 0.46% – that’s quite a big difference!

So in total with the original option, you’ll pay approximately 0.74% per year, and with the ethical option, you’ll pay approximately 1.06%.

Now let's compare that with similar investment platform options, the 2 most popular, Moneyfarm and Nutmeg.

(also called socially responsible with other platforms).

There’s one big difference when comparing the overall costs. With Moneyfarm and Nutmeg, the more you save the lower the management fee. Whereas with Wealithfy, it’s the same fee however much money you save (0.60%).

Take Moneyfarm for instance, it starts at 0.75% and then when you have £10,000 saved, it reduces to 0.70% on any money saved above that. And if you manage to save £50,000 it reduces to 0.60% (which is the same as Wealthify), and keeps reducing all the way to £500,000, which is 0.35%. (Learn more about Moneyfarm fees with our Moneyfarm review).

With Nutmeg, it’s 0.75% up to £100,000 and then 0.35% on any money above that.

So, if you have a larger portfolio (lots of money), you’ll save money on fees by using Moneyfarm or Nutmeg. Which is great, but don’t make decisions on the fees alone. Look at everything such as customer service, previous investment performance and how easy the platforms are to use.

If you are only looking to invest ethically, Wealthify is quite a bit more expensive. If you do want to help save the planet with your investments, here’s where you can learn more about ethical investing and find our best ethical Stocks and Shares ISAs.

And that’s all the fees you’ll pay with Wealthify, there’s no other hidden fees, and no fees to deposit or withdraw money either.

Note: fees are correct as of 4 August 2026.

Wealthify’s customer service is pretty good.

There’s actually a phone line you can call, open Monday - Friday from 8.00am - 5.30pm. That’s pretty rare for investment platforms, and most modern businesses in general these days!

There’s also a live-chat feature, so you can message them over the app or website rather than phoning them. Or, you could just send a message, and they’ll come back to you via email.

On top of that, there’s an FAQ section on their website which answers pretty much any question you might have.

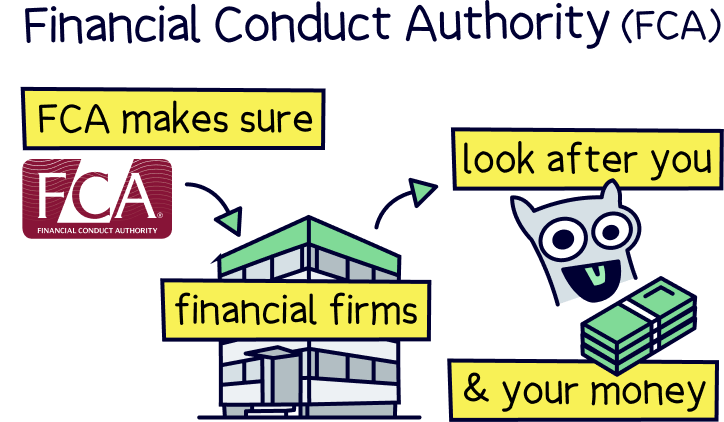

Yep! Wealthify is completely safe.

It’s authorised and regulated by the Financial Conduct Authority (FCA). That means they’ve been reviewed and approved to handle your money.

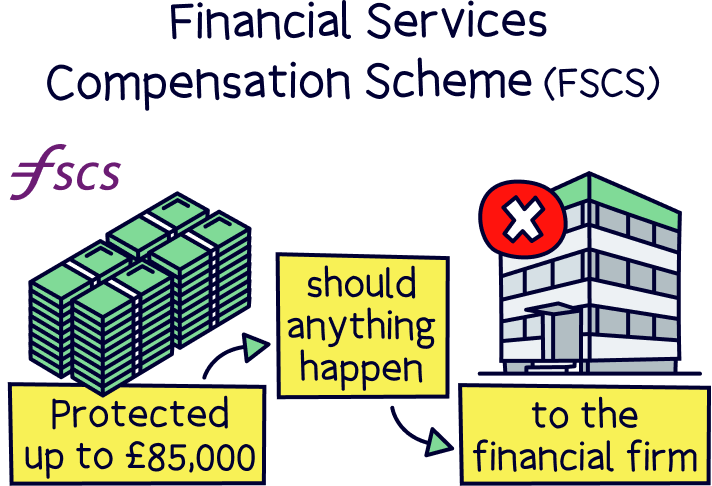

You’re also protected by the Financial Services Compensation Scheme (FSCS), which means if anything goes wrong with Wealthify, such as they go out of business, you’ll get up to £85,000 back.

However, as your money is actually held in the investments themselves, this gives you extra protection, as they’re all in your name, held with financial institutions that Wealthify can’t access. They can only be returned to you.

Wealthify is also owned by Aviva, the large financial services company. You might have heard of them!

Let’s recap and run through the pros and cons of Wealthify.

Customers are big fans of Wealthify!

On the popular reviews website, Trustpilot, as of July 2026, they are rated 4.6 out of over 3,000 reviews. That’s really great for a company in financial services where customer service is often forgotten about (most banks have very low scores).

The customers mention how easy it is to use and get started, and how good the app is, along with great customer service (phone and live-chat).

We’re big fans of anybody who makes investing easier and simpler! And that’s exactly what Wealthify does.

You don’t need to know anything about investing to get started, they take care of everything and their experts look after and aim to grow your money over time.

The customer service is great and you can actually speak to someone on the phone, or live-chat if you like.

The fees are reasonable, and easy to understand. However, with the ethical investment option, it’s slightly on the higher end compared to other options out there (such as Beach¹).

For that reason, we’re knocking it down a star. As we’re big fans of ethical investing here at Nuts About Money.

Overall though, we love Wealthify, and a big 4 stars from us!

If you think Wealthify is for you, or want to learn more, head over to the Wealthify website¹. And remember, as you are investing, your capital (money) is at risk.

Beach is an easy to use investment app where experts invest your money sensibly over time. Save within an Stocks & Shares ISA and/or pension pot.

Beach is an easy to use investment app where experts invest your money sensibly over time. Save within an Stocks & Shares ISA and/or pension pot.

Beach is an easy to use investment app where experts invest your money sensibly over time. Save within an Stocks & Shares ISA and/or pension pot.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things money, with years of combined experience working in the finance industry and writing about money. We understand the ins and outs, how to get the best deals, save money, and how to communicate money in an easy to understand way (we hope you agree).

More than 20 years of combined experience researching and writing about money

Researched and reviewed a wide range of financial services companies, and have a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Beach is an easy to use investment app where experts invest your money sensibly over time. Save within an Stocks & Shares ISA and/or pension pot.