Article contents

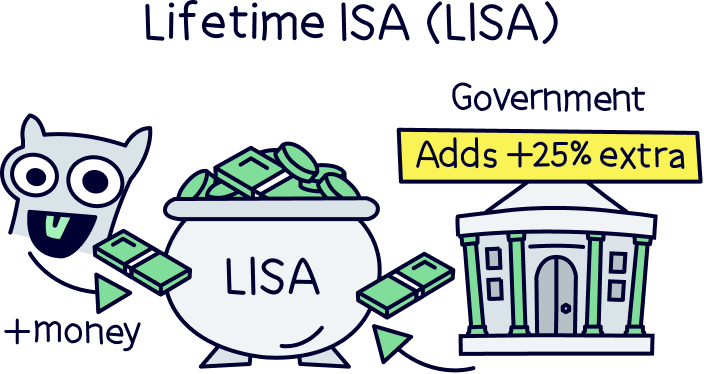

Saving for your first home can seem like an impossible task. But with a Lifetime ISA, you can hit your savings goal a lot quicker thanks to a 25% government bonus on money you put in each year. The limit on a LISA is £4,000 per year (which is part of your overall ISA limit of £20,000). You could use a LISA for later in life too.

You might know that an ISA is an Individual Savings Account (and if you want to know more, check out our ISA guide). But what is a Lifetime ISA?

Well, if we told you that for every £1 you save the Government would give you a 25% bonus, would you be interested?

We see you nodding! Let’s dive in and learn more about who can open a Lifetime ISA, how they work, the different types, and the all-important rules.

There are only two ways to use your Lifetime ISA – there’s always a catch isn’t there?!

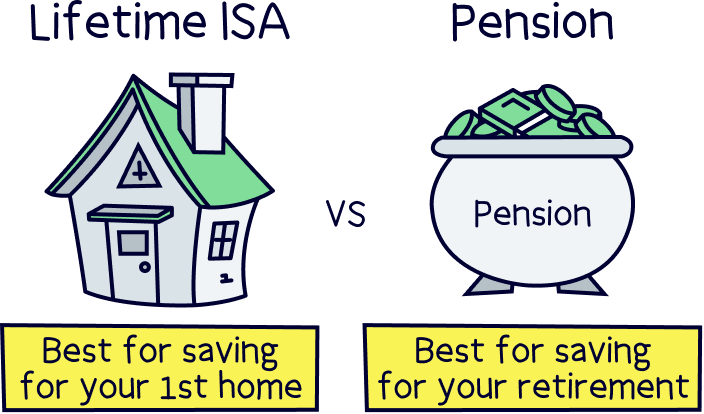

You can either put it towards the purchase of your first home, or you can use it to save for later in life (over 60) – but it’s not intended as a replacement to a pension.

You’ll be pleased to hear you can use your Lifetime ISA as a deposit on your first home! But there are a few rules:

If you’re buying a home with your partner (and you’re both eligible for a Lifetime ISA), you can get a Lifetime ISA each – doubling the amount of money you get free from the Government, and making it easier to buy your dream home quicker.

Check out Moneybox, it has one of the best interest rates, is simple to set up and use and has excellent customer service.

A LISA can act as a bonus to your pension savings if you want to save even more cash for later in life. But it’s not a replacement for a pension (here's our comparison of a Lifetime ISA vs pension).

A pension has more benefits, which are:

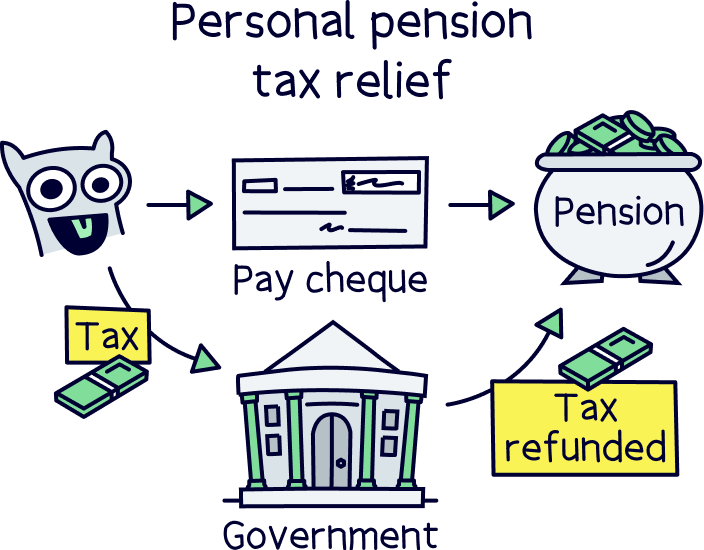

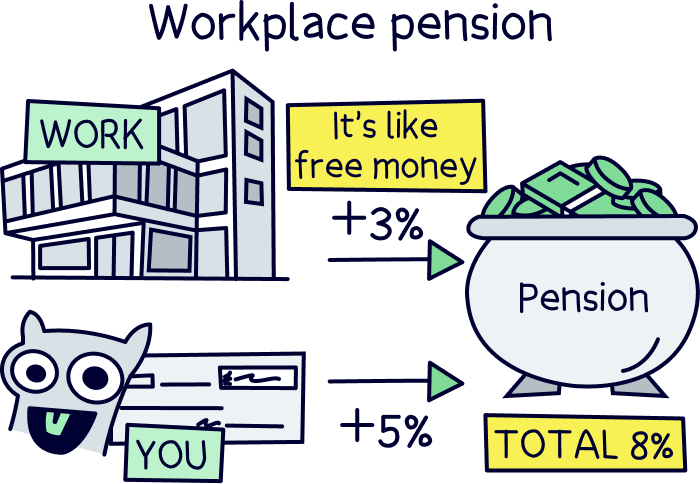

How is it the same? Well you’ll normally be making contributions to your pension from your salary before you pay tax on your salary, which means you don’t pay tax on your pension contributions, you get 20% ‘tax relief’.

Whereas with a LISA, your contributions aren’t taken from your salary, you add it in yourself on money you’ve actually already paid tax on from your salary.

Let’s say you are paying £80 into your LISA, a 25% bonus on £80 is £20, making a total of £100. With a pension, you’ll have £100 taken from your salary before you pay 20% tax, which means you’re getting that 20% for free – and 20% of £100 is £80. So, exactly the same!

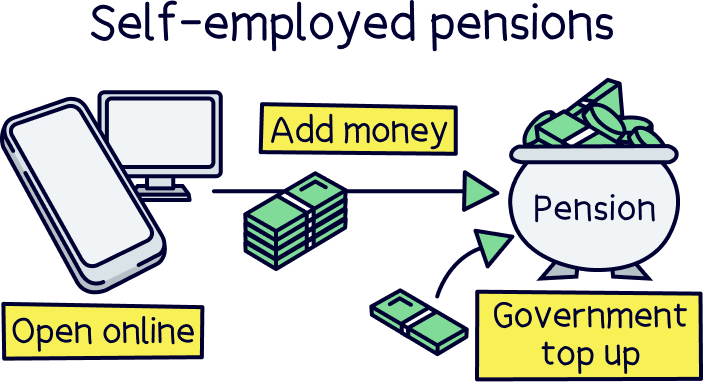

If you are self-employed, a LISA can appear to be an easy way to save for retirement, as you don’t have an employer to set up and manage a pension for you.

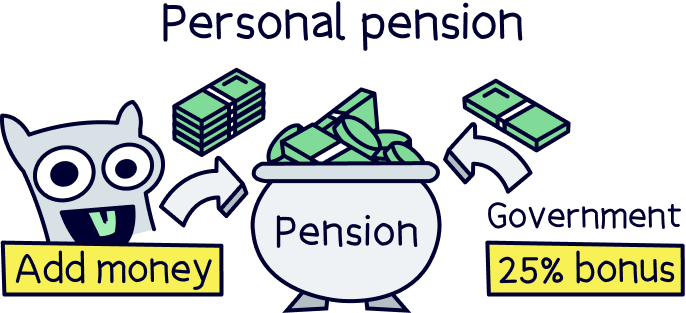

However, these days, pensions for the self-employed are super easy to set up by yourself, and you also get a 25% government bonus on your contributions too, automatically applied.

Plus, the fees charged by ISA providers and the investment funds (the experts who manage your money) can be cheaper with a pension than a LISA. Your pension is also managed by experts who specifically work on growing your money over time ready for your retirement, so you can be nice and comfortable when you retire.

We strongly recommend setting up a pension rather than a LISA if you are self-employed, and recommend reading our guide on self-employed pensions too.

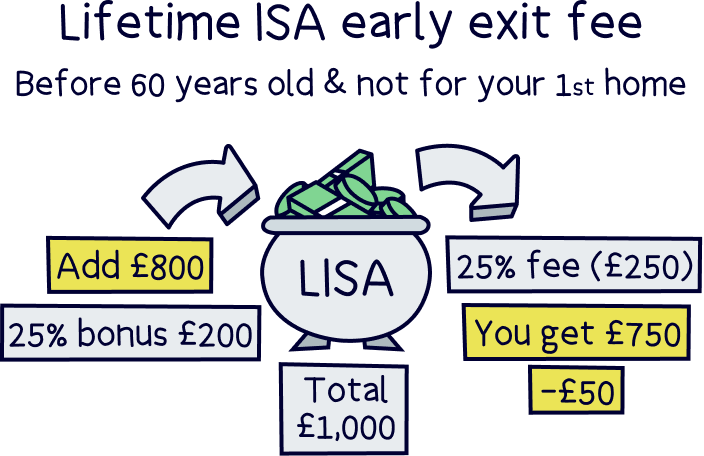

If you take your cash out for any other reason than to buy your first home, or before you are 60, you’ll need to pay a withdrawal charge. Think carefully before you do. The charge is set at 25% of the amount withdrawn, hefty!

You might be thinking, “well I’ll just be losing the government bonus”, which is 25%, but you’ll actually be charged more than you put in. Let’s take a look at an example:

With this in mind, you should only open a Lifetime ISA to help buy your first home or to boost your savings for retirement. If you’re saving for any other reason, check out one of these ISAs instead.

However, as part of the Lifetime ISA rules, if you fall terminally ill, you can withdraw cash from your Lifetime ISA provider without having to pay the government penalty (25%). Even after you’ve received a Lifetime ISA bonus (or a few bonus payments), and earned interest or investment growth.

To open a Lifetime ISA, you have to be:

Heads up: If you’re a Brit abroad, you can only open a LISA if you’re a Crown employee (a member of the UK armed forces, a civil servant, or a diplomat).

Lifetime ISAs are pretty similar to other types of ISA — you can save or invest your money, and you don’t have to pay any tax on the money your savings / investments make. Which is great, as tax can have a huge impact on the speed at which your money grows.

So far, so simple. But there are a few key differences worth noting when it comes to LISAs:

This means if you’re able to save the full £4,000 into your Lifetime ISA in the tax year, you’ll have £5,000 (plus any interest or returns on investment earned) to put towards your first property purchase or later in life. Sweet!

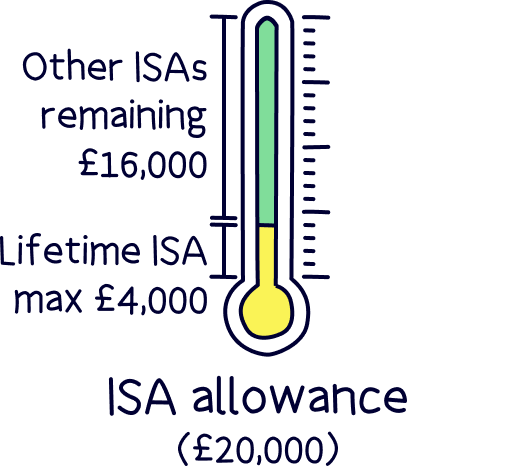

The ISA allowance is the amount you can save or invest without paying any tax. It’s currently £20,000.

You’re limited to what you can put into a Lifetime ISA each tax year (£4,000), and that number is linked to your overall annual ISA allowance.

So, for example, if you save the full £4,000 into your Lifetime ISA, the most you can pay into your other ISAs is £16,000.

You can only open and pay into one of each type of ISA each tax year. The 2 main types of ISAs are Cash ISAs and Stocks & Shares ISAs.

There's 2 types of Lifetime ISA, you can choose to save (Cash Lifetime ISA) or invest (Stocks and Shares ISA) your money with a Lifetime ISA.

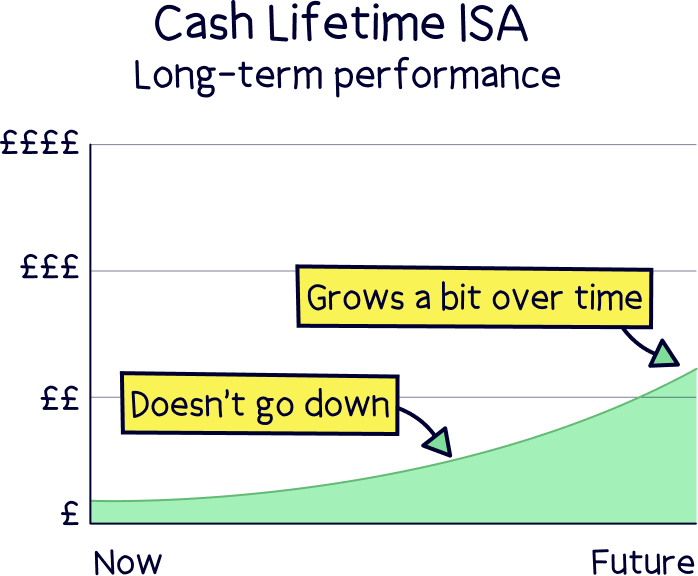

This type of ISA lets you save cash and earn interest tax-free. All you need to do is start saving! And, you’ll magically get the 25% government bonus every month. The company running your ISA will handle everything for you (called Lifetime ISA providers).

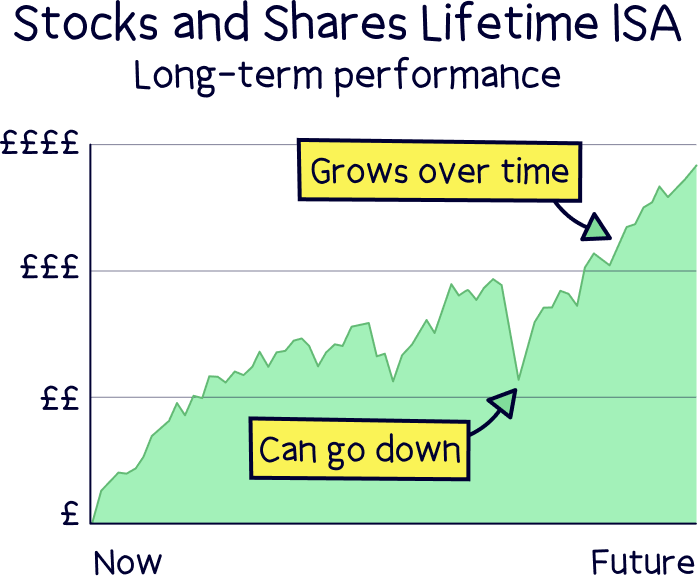

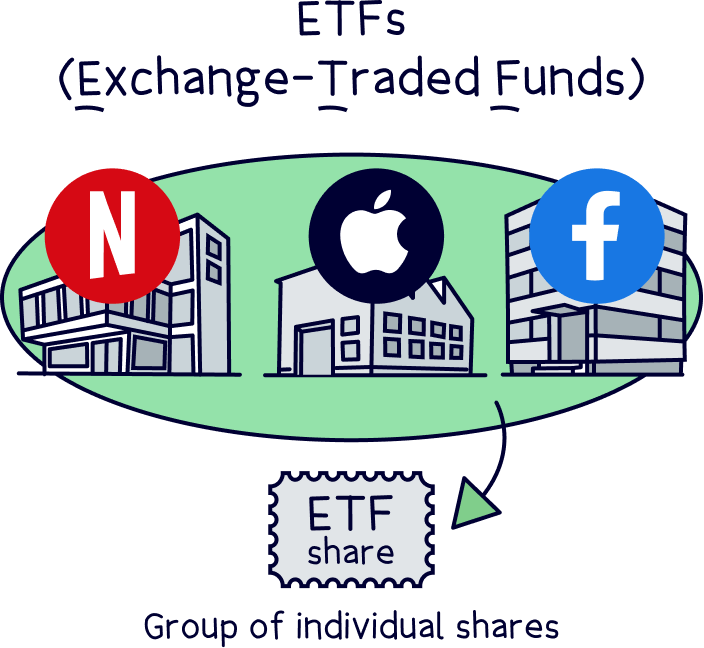

This type of ISA grows your money over the medium-to-long term (and can grow quite large!). Your ISA provider (the company managing your ISA), will work with an investment fund who will invest your money in things like stocks & shares, funds, and bonds. Don’t fear – your money is in expert hands, plus everything is handled for you too – you just put your feet up and watch your money grow.

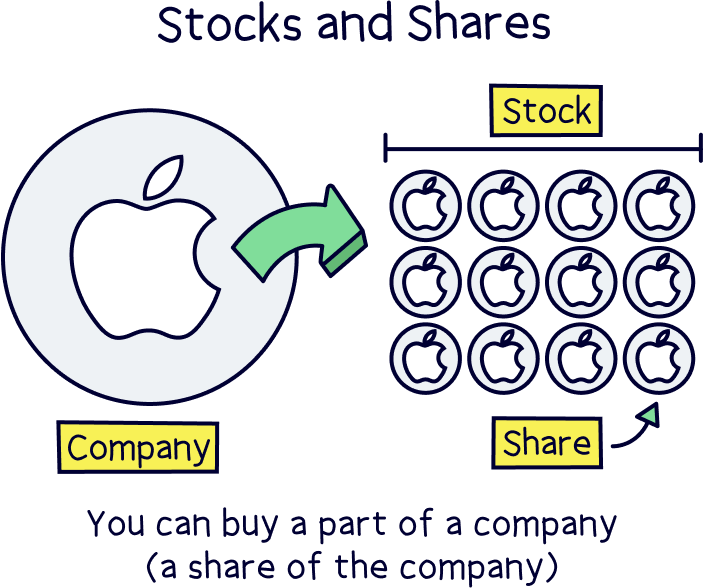

Stocks and shares, eh? Tell me more…

When you invest in a Stocks & Shares Lifetime ISA, your ISA provider (the company that looks after the ISA) will work with an investment fund(s) who will manage your investments, such as buying and selling shares, to grow your money over time. All you need to do is sit back and relax.

If you start investing early, it’s almost certain that your Stocks & Shares Lifetime ISA will outperform a Lifetime Cash ISA over time. And, all the money you start making from the investments will be completely tax-free. However, this is only a good idea if you plan to have your account for a long time, otherwise, simply go with a Cash Lifetime ISA.

Nuts About Money tip: if you think a Stock and Shares Lifetime ISA is for you, scroll down or click to see our Lifetime ISA recommendations.

You can indeed, but you can only open one Lifetime ISA in a tax year, and you can only pay into one Lifetime ISA each tax year.

So, you could open a Lifetime Cash ISA this tax year, pay into it, then open a Stocks & Shares Lifetime ISA next tax year, and pay into that. But you couldn’t split your money between the two in the same year.

With that in mind, you might be better off picking one type and sticking with it – if you think you’ll use the cash soon to buy a home, you could go with a Cash Lifetime ISA and just collect the 25% bonus.

However, if you’re not planning to buy a home for a while, such as 3-5 years or more, or want to use a LISA to save a bit extra for your retirement, you could go with a Stocks and Shares Lifetime ISA, so you can collect the 25% bonus, and grow your money over time too (as your money will be invested sensibly by experts over time), with a rough estimate of 7% increase per year over time.

Note: You can open up different types of ISA that aren’t Lifetime ISAs in the same year. For example, you can also open a standard Cash ISA or a Stocks & Shares ISA.

Opening a Lifetime ISA is super simple. So long as you’re eligible (18-40, UK resident), all you need to do is decide you if want a Cash Lifetime ISA (for short-term saving) or a Stocks and Shares Lifetime ISA (for long-term saving).

Next, all you do is pick your preferred Lifetime ISA provider – they’re the people who manage everything for you. Not sure where to look? Don’t worry we’re to help you choose too.

Top rate

Saving for your first home? Moneybox could be for you.

Moneybox is the go-to place for Lifetime ISAs – it’s easy to use, and you’ll be able to manage everything on a great mobile app.

You can either pick from saving cash (Cash Lifetime ISA), and benefit from a great savings rate. And there’s no fee for saving cash.

Or, you can make your own investments (Stocks and Shares Lifetime ISA), and pick from a range of investment options (including individual US shares such as Apple and Amazon). Fees will apply.

Moneybox will handle everything behind the scenes, and collect your 25% government bonus and automatically add it to your account.

Overall, it’s low cost overall, and the customer service is excellent.

Note: don’t wait to get started, as you’ll need to wait 12 months before you can use your LISA to buy a home – all you need to do is add £1.

Top rate

Tembo is one of the best Lifetime ISAs out there – it’s got one of the best interest rates out there, and it’s easy to use, with a great app on your phone, packed with tools to help you save more.

They’ll also transfer your existing Lifetime ISA over if you have one too (they’ll handle everything).

There’s two options, a Cash LISA (with the top interest rate), or a Stocks and Shares LISA, where you can simply let the experts handle things, and aim to grow your money more over time).

They'll also be able to help you with the mortgage when the time comes to buy your first home – and help you borrow more if you need to.

The customer service is top notch too.

Check out Moneybox, it has one of the best interest rates, is simple to set up and use and has excellent customer service.

Cheapest Stocks and Shares Lifetime ISA

Lifetime ISAs: fees are reduced to 0.25% per year, and free to buy investment funds

Hargreaves Lansdown (HL) is the most popular investment platform in the UK, it’s used by over 1.8 million people, saving over £130 billion. It’s very trustworthy, and safe to use.

They offer a great Stocks and Shares Lifetime ISA – which offers the full range of investment options, but also has reduced costs just for the LISA (compared to other types of investment accounts), making it one of the best LISA options out there (fees are reduced to 0.25% per year, and free to buy investment funds).

It’s great for making your own investments, or you can pick ready-made choices where you can leave it to the experts.

AJ Bell is well established, with a good reputation.

It's one of the cheapest traditional stock brokers out there (charging a low annual fee).

There's a huge range of investment options – pretty much every investment out there (including both funds and shares).

The customer service is great too.

Overall, it's one of the best options.

Check out Moneybox, it has one of the best interest rates, is simple to set up and use and has excellent customer service.

A Lifetime ISA can be a massive boost to your savings if you’re a first time buyer – you can put your savings towards buying your first home – with a 25% bonus on your Lifetime ISA savings (up to £1,000 per year as your Lifetime ISA limit is £4,000 per tax year).

But you’ll need to be sure you want to buy a home, as you won’t be able to withdraw money after you start saving with your Lifetime ISA provider (well, you can, but you’ll have to pay a very hefty charge of 25% of the total, unless you have a terminal illness). Or, you can wait until you are 60 to withdraw, and use it to enjoy later life.

It’s a great way to build up a large amount of money for your house deposit in a relatively short period of time, whether you choose a Cash LISA or a Stocks & Shares LISA.

If you want to see our top picks, scroll up or click to see our best Lifetime ISAs.

Once set up, your savings will grow inside your account, you’ll also pay nothing in tax too! So, if you’re saving for a few years or more, it could be worth saving in an expert-managed Stocks and Shares Lifetime ISA and benefit from potentially higher investment growth.

And don’t forget, you have to have your LISA open for 12 months before you can use it for your first home – so you better get opening one soon! You’ll be in your own home in no time. You can normally open one with a first payment of just £1 too.

You can also use a LISA to save for later in life, for when you’re over 60, but we recommend you don’t use it as an alternative to a pension, just as a little extra for when you retire. A private pension has far better benefits to help grow your money for retirement, and an equivalent to the 25% bonus too.

Check out Moneybox, it has one of the best interest rates, is simple to set up and use and has excellent customer service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things savings, with many years of combined experience writing and talking about savings (and ISAs). Some of our team were top financial advisors. We understand the ins and outs of planning your finances well, how to communicate savings in an easy to understand way (we hope you agree), and of course, how to get the best savings rate for you.

More than 20 years of combined experience researching and writing about savings

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of savings companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Check out Moneybox, it has one of the best interest rates, is simple to set up and use and has excellent customer service.