Review contents

Tembo is a great service. They’ll help you get on the property ladder with unique options to increase the amount you can borrow and boost your deposit – and they’ll search every mortgage out there to get the best one for you. Plus, they can help you save for your deposit with a market leading interest rate on a Lifetime ISA.

Getting on the property ladder can be incredibly hard these days. Tembo makes it much easier for you to buy your dream home.

How? On the surface, they’re a mortgage broker (that’s someone who gets a mortgage for you), but they also have options to increase your deposit, and the amount you can borrow – which makes it much easier to buy your first home (or a bigger place).

Of course, if you don’t need extra help to buy your home, they can simply sort the mortgage, and guarantee to get the best mortgage for you. They can also help you switch to a great new deal if you’ve got a mortgage already (called remortgaging). And buy-to-let investors are welcome too!

They aren’t just an online mortgage broker either, they’ll actually get to know your personal circumstances over the phone too – it’s the best of both worlds – real experts alongside technology (website), making everything easy and straightforward.

Tip: if you just want to see the latest interest rates for mortgages check out our mortgage comparison.

You can do it in your own time (such as while you're watching TV), and then have a chat with your professional mortgage advisor to discuss any questions you might have.

We’ll cover those options more in-depth below, but if you’re in a hurry, learn more on the Tembo website¹.

By the way, you'll also get 50% off their fee with Nuts About Money (saving £100s).

Tembo also offers a Lifetime ISA to help you save for your first home, where you can get a massive 25% bonus from the government, on everything you save, and a market leading interest rate. Here’s where to learn more about the Tembo Lifetime ISA¹.

Overall, Tembo is a great service, and has great options to help you buy a home. They’re really helping to simplify the complicated mortgage process – they’ve even been voted the UK’s Best Mortgage Broker in the British Bank Awards.

Let’s dive in a bit more.

Yes! It’s perfect for first time buyers. They’re experts in all the various problems first time buyers face, such as small deposits and lower incomes – they’ve got unique options to help with these, so you could still end up buying the home of your dreams much sooner than you think!

They even offer a Lifetime ISA to help save for your first home in the first place (more on that below).

We’ll cover how your income affects your mortgage below, but for a quick overview of your options, Tembo has a service called Income Boost¹, which increases your income for a mortgage, with the help of friends and family. And then there’s Deposit Boost¹, which is where your friends or family can use their property to add to your deposit.

Don’t worry, if you don’t have friends or family who might help, there’s lots more options, which they’ll run through with you, and we’ve listed some of them below.

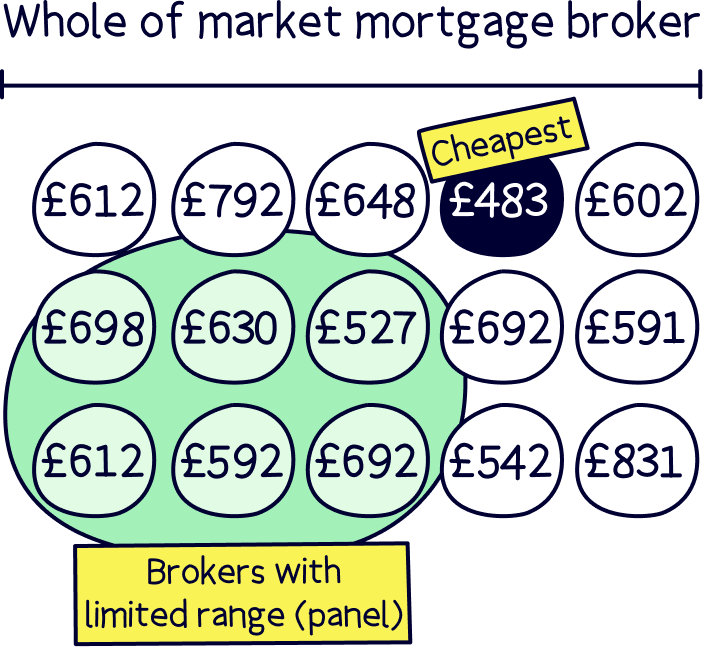

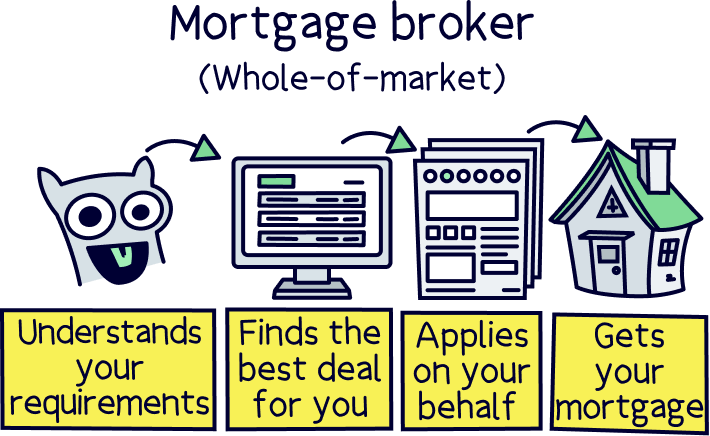

They’ll also apply and sort the whole mortgage for you too, even if you don’t want to use these additional services. And, you’ll be guaranteed to be on the best mortgage for you – as they search the whole market (search every mortgage possible by mortgage brokers – that's over 100 lenders) to find the right one for you.

We highly recommend using a good mortgage broker for your mortgage, it doesn’t have to be Tembo. The difference between a bad mortgage deal and a good deal can be £100s a month – if you do it yourself, or use a mortgage broker who can’t search the whole market, you can’t be sure you’ll end up on the best deal. A good broker really is worth their weight in gold!

Learn more about how Tembo works for first time buyers on the Tembo website¹. And if you want to view all the best options for mortgage brokers, check out the best mortgage brokers.

If you like the sound of Tembo, get 50% off the standard fee – you could save £100s.

Tembo’s Lifetime ISA is pretty great – in fact it comes out top of our best Lifetime ISAs…

That’s because it’s got a great rate on your cash savings, and it’s super easy to use – just add your money and you’re away. It all works on a great mobile app, and it’s packed with tools to help you save more too.

Nuts About Money tip: you can transfer your existing LISA (if you have one), so you can get that top interest rate too. Tembo will handle the whole transfer process for you.

If you’re not sure what a LISA is, you’ll likely want one… A Lifetime ISA (LISA), is a government scheme to help you save for your first home. You’ll get a massive 25% from the government on everything you save, and you’re able to save up to £4,000 per tax year (April 6th to April 5th the following year).

You can use the money you save to buy your first home for up to £450,000.

If you haven’t got one yet, it’s worth opening one now, as you’ll need to have it open for at least 12 months before you can use it – just add a little until you’re ready to save more.

There’s a few more bits and bobs to Lifetime ISAs, but we won’t bore you with the details here, learn more, and get started on the Tembo website¹, or check out our guide to Lifetime ISAs.

Put simply, Tembo does everything possible to help you get on to the property ladder. They’re your partner with the financing side of buying your home, all you really need to do is find the home of your dreams.

That means they’ll find the right mortgage for you, from various different types of mortgages, but also use the various different government schemes and sources to either increase your deposit, or boost your income to a level where you can get the mortgage.

The 2 main options are (we’ll run through the other options below too):

This is to increase the amount of cash you can use for your deposit. A higher deposit can be the difference between getting a property or not, and reduces the interest rate you pay on the mortgage too.

For instance, if you have a 5% deposit, you’ll likely not be able to get a good (cheaper) mortgage, or one at all, but if you can boost that to 10% or more with help, you’ll be in much better shape.

Or, you might be looking at a home you've fallen in love with, can borrow enough and can afford the monthly repayments, but don’t quite have enough saved for a deposit to get the mortgage. That’s where Tembo can help.

Deposit Boost is where a family member or even a good friend can use their own home to get a small mortgage loan on their property, which acts as your deposit – technically they are ‘releasing cash’ from their home.

Important: they'll ultimately be responsible for the payments and the loan, but you’ll be paying it back each month. If you don't pay, they will have to pay it.

Sound interesting? Here’s where to learn more about Deposit Boost¹.

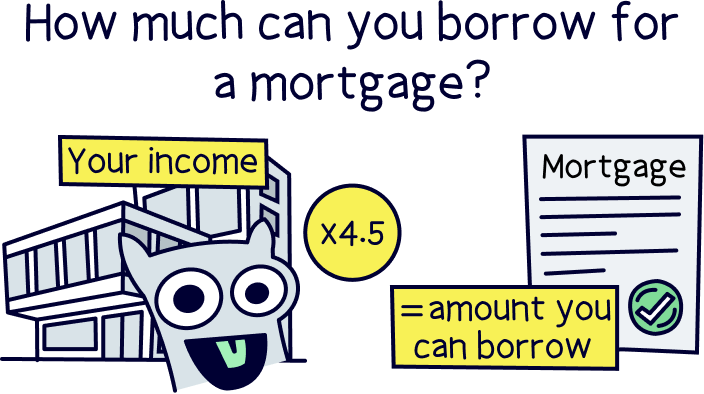

Income Boost is a great option if you have a good deposit, but don't earn enough to get a ‘normal’ mortgage to cover the property price.

Very roughly, you can borrow 4.5x your salary for a mortgage.

How does it work? You can add a friend or family member’s income (e.g. their salary) to your mortgage and so increase how much you can borrow. These are a special type of mortgage, called a Joint Borrower Sole Proprietor (JBSP) mortgage – which simply means there’s more than one person borrowing the money (technically), but only one person owns the home.

Here’s where to learn more about Income Boost¹.

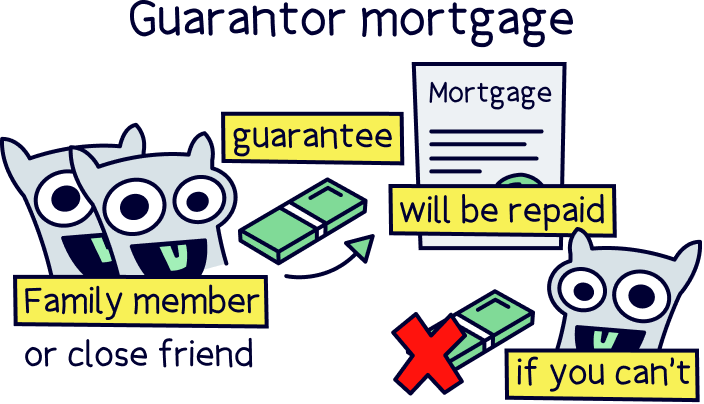

You might have heard of guarantor mortgages called something different, such as family assisted mortgages – and these are where your family is helping you out to get on the property ladder, either by using their savings or house as a guarantee for your mortgage, or their own income to increase your borrowing.

Important: if you don’t pay your monthly repayments, your guarantor will have to.

Tembo’s Deposit Boost¹ and Income Boost¹ can also be classed as guarantor mortgages.

There’s also the option of using the Shared Ownership scheme, which is buying between 25%-75% of a property, and paying rent on the rest. A housing association will own the rest (the property developer), and act as your landlord. You'll never own the actual property, just the right to live there.

Although these might sound like a good option, we don’t recommend this here at Nuts About Money. Even though you only own part of the property (the lease), you will have to pay 100% of all the regular extra charges in full (like the service charge), and these can grow extortionately high after you move in, and recur every year. It’s also incredibly difficult to buy the remaining share of the property and re-sell the property in future.

An equity loan can be a great option to boost your budget. With these, you can increase your deposit with a second mortgage on the property. They’re very similar to the Government’s Help to Buy scheme, which has now been phased out.

The lender (the company who gives you the loan) will own part of the property too, so if you sell in future and the price has gone up, you’ll pay part of the profit to the lender when you repay the loan.

You can borrow up to £100,000 from a range of different companies that offer this service, and Tembo¹ will find the best one for you.

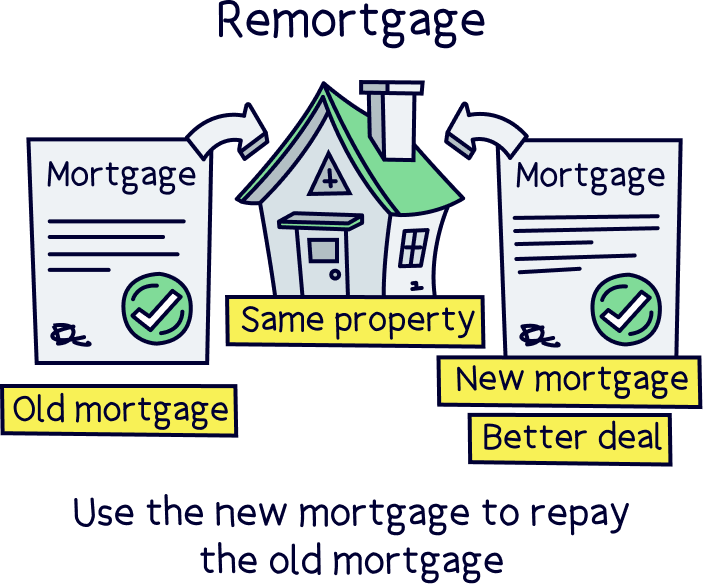

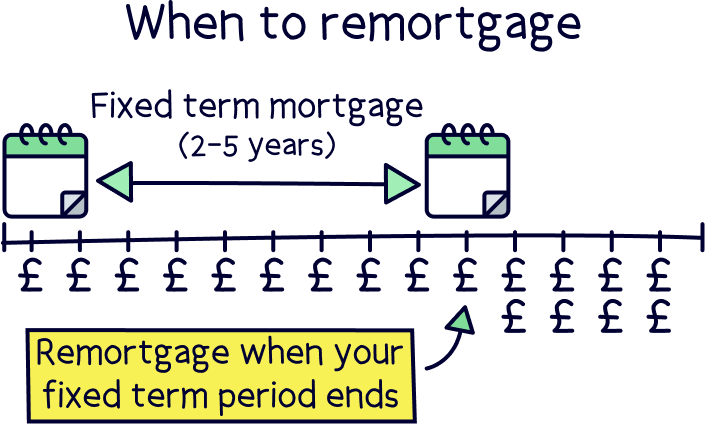

If you’ve already got a mortgage, often you’ll want to switch to a new deal when the fixed rate period of your mortgage ends, which is the lower rate (incentive) at the beginning of the mortgage. This is normally fixed for either 2 or 5 years.

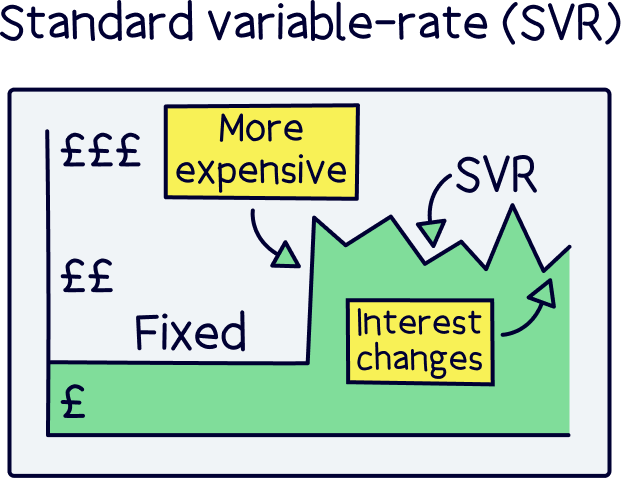

After the fixed-rate period ends, your mortgage rate normally increases as you move onto the mortgage lenders Standard Variable Rate (SVR). This is the lenders 'standard’ rate, and can change over time (up and down). It’s normally a lot more expensive. Switching deals is called remortgaging.

You can also remortgage to borrow more cash if you want to build an extension, or use the cash for anything you like – be sensible please!

For the latest remortgage rates, visit our remortgage comparison table. Here’s where to learn more about remortgaging with Tembo¹.

The customer support is awesome.

The guys at Tembo really know their stuff, and they’re super friendly and helpful too.

When you first get started, you’ll need to use their website, where there’s live-chat, so you can ask any questions you might have on their website and get a quick response.

After that, you’ll be assigned a mortgage advisor who’s with you from start to finish and you’re able to speak to them over the phone – or email, or live-chat, the choice is yours. They’ll update you whenever there’s progress on your mortgage too, so you’re always in the loop.

If you're just curious, their website is also full of information about the types of mortgages that might be right for you.

Unfortunately Tembo isn’t free. They charge for the mortgage advice. The typical fee is £499, and if you get extra help by taking out an Income Boost, or Deposit Boost, it's normally around £749, but it can increase to £999 for very complex cases.

And as you're reading this (Nuts About Money), you'll get 50% off the fee – making it very reasonable. All you need to do is get started on the Tembo website¹.

This is in-line with most mortgage brokers across the UK, so don’t let it put you off, and the customer service is really excellent. Plus, you’ll be sure you’re getting the right mortgage for you, and they’ll handle the whole application for you too. Not to mention the extra services they provide to get you on the property ladder!

We always recommend getting mortgage advice – finding the best mortgage for you can potentially mean the difference of £1,000s per year, so it really does pay for itself.

Yep! Tembo is perfectly safe to use for your mortgage. They’re authorised and regulated by the Financial Conduct Authority (FCA) – which means they’ve been reviewed and approved to give mortgage advice, and arrange finance for your home.

It also means you’re protected too, and can claim compensation if the mortgage advice you received meant you didn’t get the right mortgage for you. This is part of the Financial Services Compensation Scheme (FSCS).

Customers really love Tembo. On the popular reviews website Trustpilot, it’s got an excellent score of 4.9 out of 5 from over 2,000 reviews.

That’s really, really good, well even more than good, excellent! Especially for a company in financial services where scores tend to be very low (as the customer service is often very poor). In fact, the highest score on Trustpilot among the top mortgage brokers.

Most of the reviews for Tembo are about the amazing customer service and helping people get onto the property ladder when they otherwise couldn’t, and finding the best mortgage deal overall.

Here’s a quick recap and the pros and cons of Tembo:

We’re huge fans of Tembo – getting on the property ladder is seriously difficult, and anyone helping people to get on the ladder deserves a big round of applause!

The options to increase your borrowing and deposit are really great (Income Boost¹ and Deposit Boost¹). For a lot of people, these might be your only options to buy a home.

Plus, you can be sure you’re getting the best mortgage deal, as they search every mortgage lender possible (over 100 lenders) to find the best one for you. Potentially saving £100s per month.

And best of all, the service is epic. They’re with you every step of the way, and advising the right options to get you that dream home.

The only downside is there’s a fee, but can you really expect all of that for free? (although 50% off with Nuts About Money).

Overall, we think it’s awesome. It’s 5 stars from us. Learn more and get started on the Tembo website¹.

Yep! And it's a pretty good one – you'll save £100s.

For mortgage advice: you'll get 50% off their fee with Nuts About Money. That's a saving of up to £499.

All you need to is get started on the Tembo website¹.

If you like the sound of Tembo, get 50% off the standard fee – you could save £100s.

If you like the sound of Tembo, get 50% off the standard fee – you could save £100s.

If you like the sound of Tembo, get 50% off the standard fee – you could save £100s.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things money, with years of combined experience working in the finance industry and writing about money. We understand the ins and outs, how to get the best deals, save money, and how to communicate money in an easy to understand way (we hope you agree).

More than 20 years of combined experience researching and writing about money

Researched and reviewed a wide range of financial services companies, and have a transparent review process

We follow a strict editorial code to ensure you get the best information possible

If you like the sound of Tembo, get 50% off the standard fee – you could save £100s.