Article contents

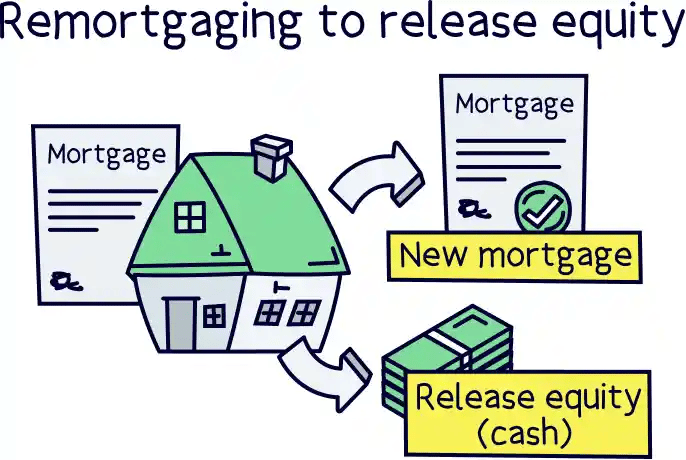

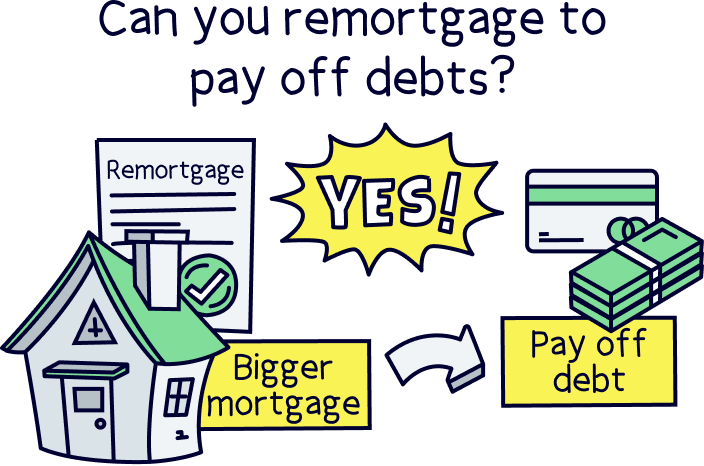

Remortgaging to release equity is when you take out a larger mortgage to unlock some cash that was tied up in your house. You can then use this cash for whatever you want!

Own a property? Want some extra cash in your pocket? You may want to remortgage to release equity. Here, we’ll take a look at what that means, why you might want to do it and how to go about it.

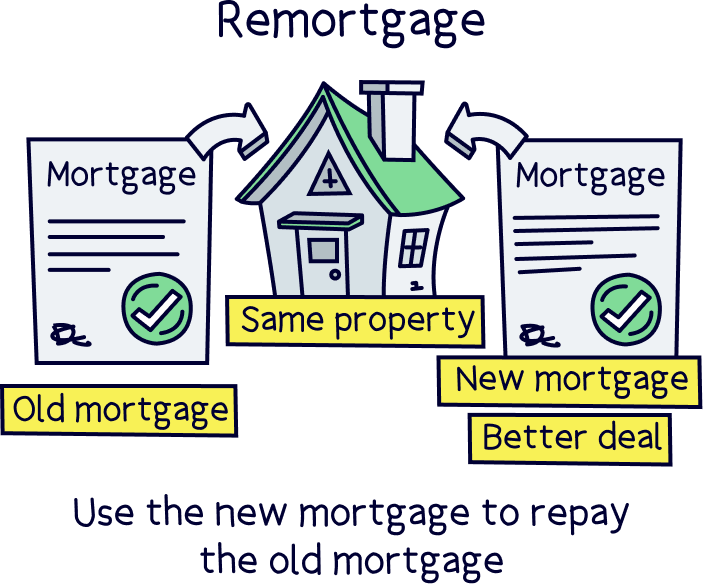

Remortgaging is where you take out a new mortgage on a property you own. If you’re a homeowner, then chances are you’ll want to do this at some point or other – usually to get a better deal, reduce your monthly repayments or shorten the length of your mortgage (known as your mortgage term).

Remortgaging to release equity, on the other hand, is when you remortgage to get some cash. By taking out a new, bigger mortgage that covers more of the value of your property, you reduce the amount of equity you own and get some of the money you once put into the property back in cash.

If you only own one property, things get even better – the cash you get from remortgaging to release equity is tax-free. Kerching!

Confused? Don’t worry, we’ll explain it all below.

Tembo will find your best deal, fast, all with award-winning service.

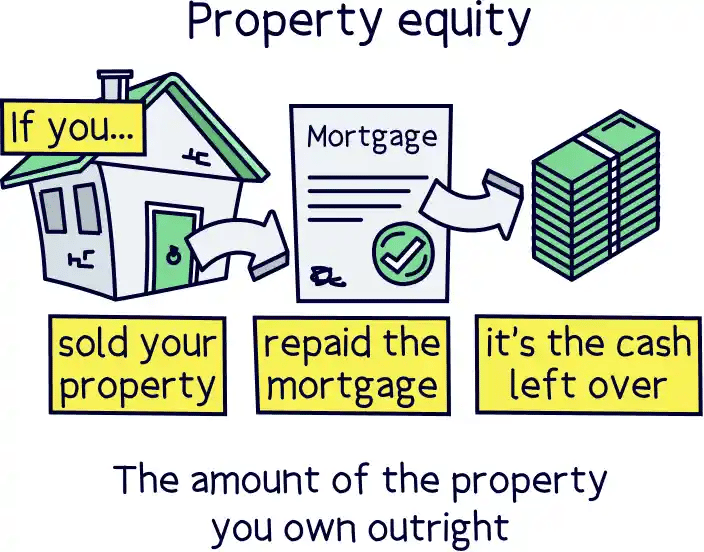

Equity refers to how much of your property you own outright. Basically, even though you do own your house when you buy it, if you haven’t paid off your mortgage, you still owe the mortgage lender a proportion of your house’s value.

Let’s imagine you sell your house and don’t buy a new one. The equity is the amount that will go straight into your pocket. The rest of the property’s value will go back to your mortgage lender in order to pay off the loan.

Most of the time, the equity you have in your property will go up. This is for two reasons:

The more equity you have in your house, the easier it is to remortgage to release it.

The problem with equity is that a proportion of your wealth is tied up in your property. This is essentially money that you own but you can’t spend.

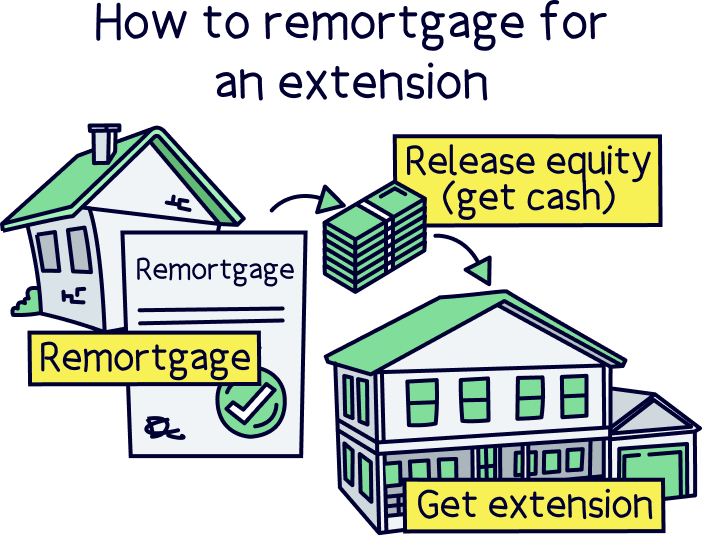

Imagine this, for example: you own a lovely house but you don’t have the spare cash you need to replace your boiler, pay for your child’s uni fees or build an extension. How frustrating!

One thing you could do to get that cash is sell your house. But what if you don’t want to?

That’s where remortgaging comes in.

If you remortgage to release equity, you get to buy whatever it is you’ve set their heart on – without having to sell up.

A lot of people use this as a way to make improvements to their home. For example, they might use the money to knock down walls, build an extension, renovate a bathroom… the list goes on. This can be a really smart thing to do as making home improvements could add value to your house – giving you more equity in the long run! Is it just us with dollar signs in our eyes right now?!

Remortgaging to release equity might sound like the best thing you’ve ever heard of. Especially if you’ve got your eye on something special that you don’t have the cash for.

But watch out: it’s not all sunshine and roses. So, weigh up the pros and cons carefully before making a decision.

If you’re wondering how much cash you could get by releasing equity, the first thing you’ll need to find out is how much equity you actually own!

You can get a rough idea of how much your home is worth by looking at what other, similar properties have sold for in your area. The Land Registry can help you out here, but you can also get some information from sites like Rightmove.

Alternatively, why not just get an estate agent to come over and give you an estimate? Most will do this for free, as they’re hoping that you’ll sell your house and use them as your estate agent. Be careful though: some estate agents will inflate their estimations as a way of getting you to pick them. It’s usually best to get a few estimates so you build up a clearer idea of how much your home is really worth.

Now you’ll need to subtract the amount you still owe your lender (your outstanding mortgage amount) from the amount that your property is worth. That’s how much equity you own. Simple!

Ideally, you’ll want to steer clear of remortgaging to release equity unless you have a decent amount of equity built up in the property. This is because if you dramatically change your loan-to-value ratio (the amount you’ve borrowed in comparison to the equity you own), you could end up paying a lot more interest.

If you own your entire property outright then now’s when you get to act smug. Usually, this will give you access to the very best deals (check out our piece on remortgaging when you own your house outright for the full lowdown).

Some mortgage lenders have calculators available on their websites that can give you an estimate of how much equity you could release. However, it’s always best to speak to a mortgage broker for advice. They’ll be able to give you an idea of what the different lenders are looking for. Plus, they’ll guide you through the whole remortgaging process. What more could you want?!

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

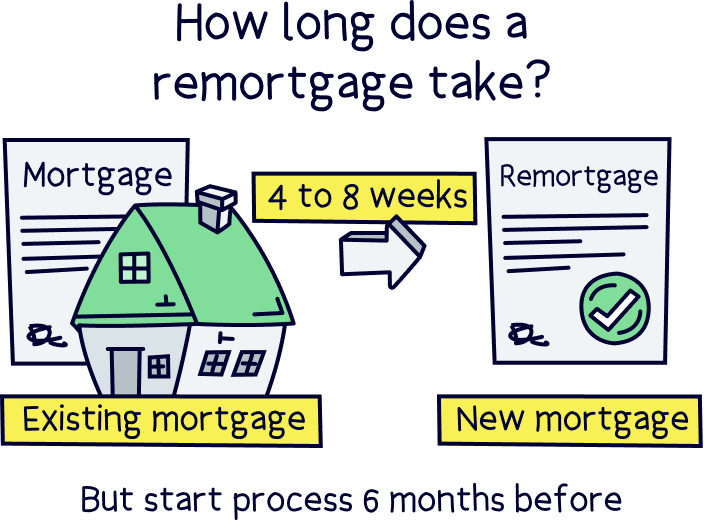

It normally takes around 4 to 8 weeks to get the funds after you’ve submitted an application to remortgage. So, make sure you start the process nice and early, particularly if you need the cash for something specific!

Wondering why it takes so long to remortgage and release equity? Well, your lender will need to check your finances and credit score to work out what kind of deal they’re willing to offer you, just like they did when you first took out your mortgage.

That’s just one reason why getting a mortgage broker involved is the way to go. They can give you a picture of how strong your application is before you go to your lender. That way, you’ll know what to expect and you can avoid wasting time on applications that are likely to get rejected.

Itching to go ahead and remortgage so that you can get your hands on that all-important equity?

The first thing to do is get in touch with an independent mortgage broker. They’ll be able to help you work out how much equity you could (and should!) release, as well as which lenders have the best deals available. Plus, they’ll handle the whole process for you from start to finish.

Trust us, that much-needed cash will be jingling in your pockets in no time!

To recap, if you need to find a decent mortgage broker check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. Plus, get 50% off their fee with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.