Article contents

Avoid paying a higher interest rate after your fixed rate ends by remortgaging to a new mortgage deal. Use a broker to find the best deal for you.

Fixed rate deal coming to and end? Not quite sure what to do? Here’s how and why you should be remortgaging at the end of your fixed rate.

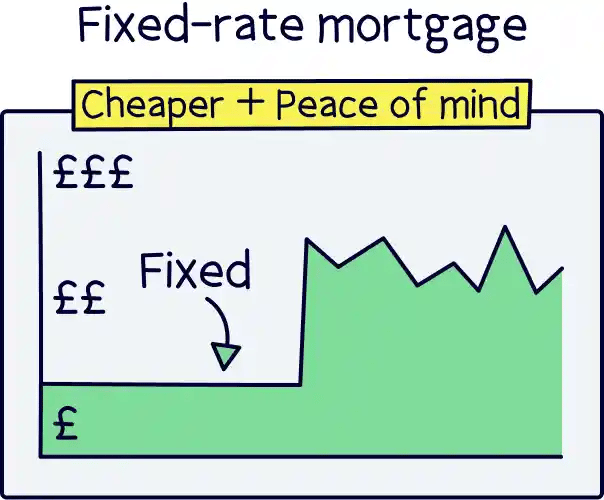

Most mortgages in the UK are fixed rate deals. This means there’s an introductory period, normally 2, 3 or 5 years, at the start of the mortgage which has a fixed interest rate. This means your monthly repayments will be the same throughout this introductory period. Which is usually a very low rate in order to help lenders sell the mortgage (they normally appear top in mortgage comparison tables with lower interest rates).

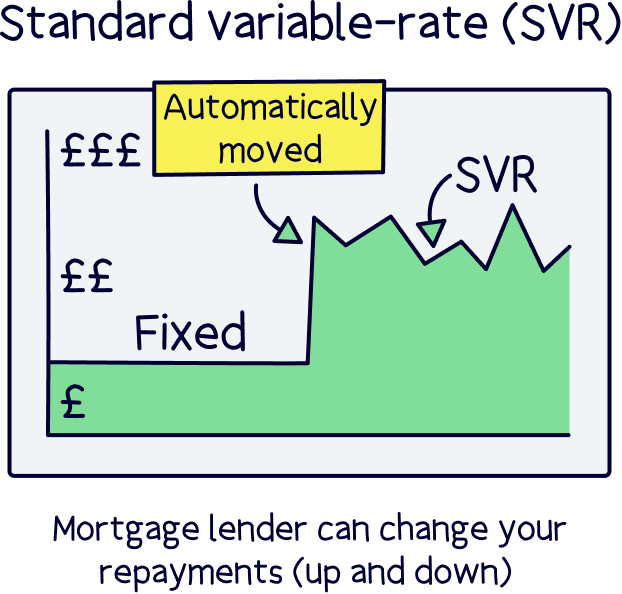

After the initial period with the low rate, the mortgage interest rate will automatically move to a standard variable rate (SVR), for the remainder of the mortgage term (the life of the mortgage), which is typically 25 years, but can be as high as 35 years, and even 40 years recently. We've written a guide to explain more about what happens when a fixed-rate mortgage ends.

The interest you’ll be paying each month could double if you do not remortgage at the end of your fixed rate. That could be a big increase, watch out!

Tembo will find your best deal, fast, all with award-winning service.

So now you know how much the interest rate can be manipulated by the banks, when looking for a new deal you should never look at just the interest rate, you need to factor in all costs associated with it.

There are typically arrangement fees (fees paid to the lender to get the mortgage), and sometimes other more hidden fees. It’s common to find low interest rate mortgages with high arrangement fees to offset the cost to the bank of having the low rate! However you can sometimes find cash back or other incentives, which are great for you, but still might not be the best.

All the fees together and incentives discounted is sometimes called the ‘true cost’, or total cost of the mortgage, and it’s this cost over the fixed term period that you should use to compare mortgages.

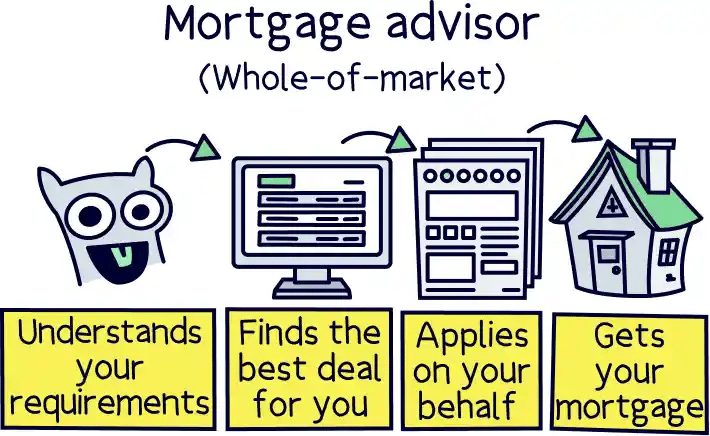

It can get complicated and we do recommend using a mortgage advisor to help you find the best deal. There may be fees for this too, depending on which advisor you use. More on using an advisor below.

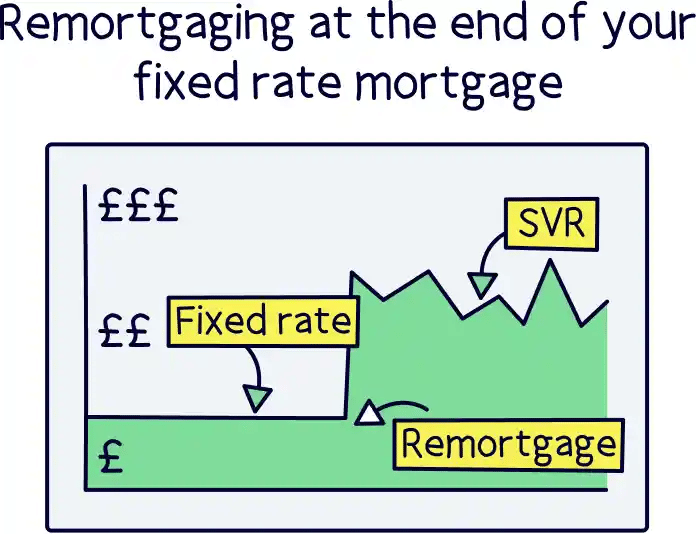

So to avoid paying the higher interest rate on your mortgage, and potentially paying double in interest on the standard variable rate, you should simply just remortgage and find a new deal when the low rate comes to an end.

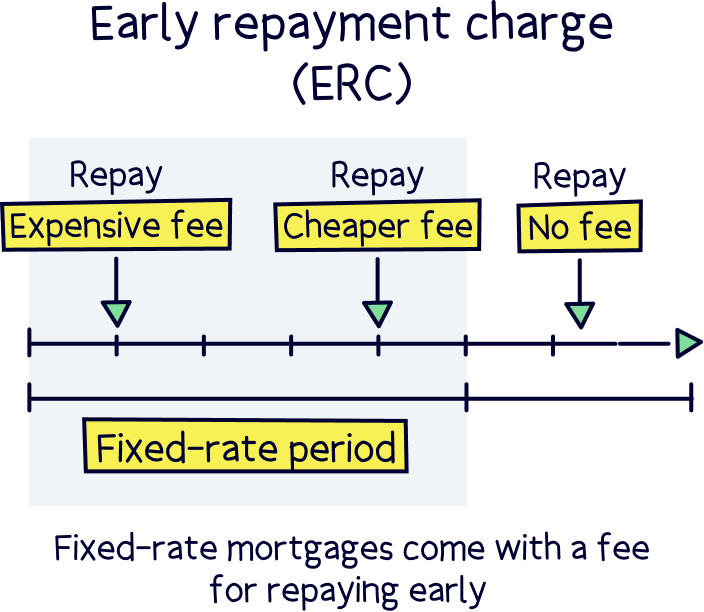

You can’t remortgage before then because you’ll be liable for early repayment charges (ERCs), which are fairly expensive, normally 1-5% of the mortgage depending on how many years are left on the fixed term period. They normally step down as you near the end of the deal, so for instance if you have a 5 year fixed rate, your first year would be 5%, then 4%, 3%, 2% and finally 1% in the last year left of the deal, and then you’ll move onto the standard variable rate for the rest of the mortgage.

The best time to remortgage is around 6 months before the end of the fixed rate period, but don’t worry if you’re less than that now, anytime before the fixed rate ends is a good enough time. And you won’t pay any ERCs remortgaging before the end as you’ll time the new mortgage to start on the very next day your current mortgage deal ends. Well, your mortgage advisor will arrange this for you.

We’ve written a step-by-step guide for the best way to remortgage. But in summary, you need to first dig out all of your documents you have for your current mortgage, and put together a few bits like your address history and salary/income if it’s changed.

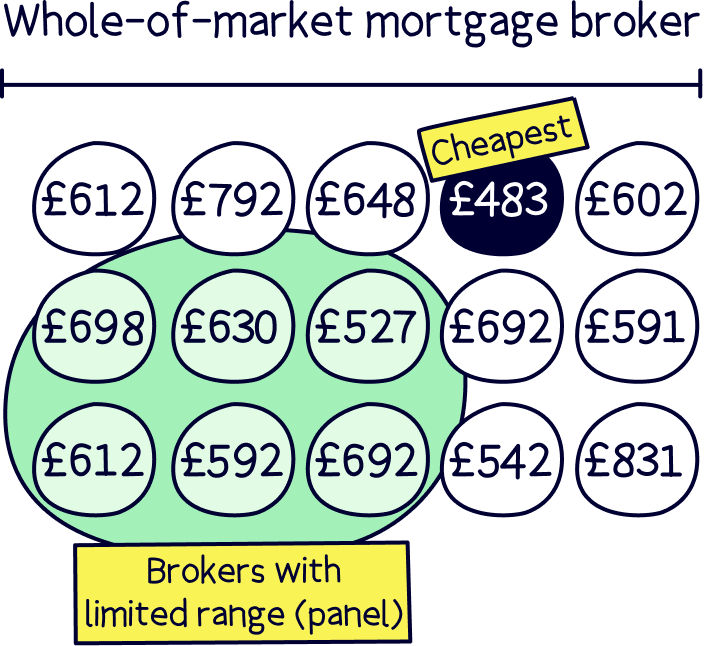

Next is to find a good mortgage broker. You must use one that searches the whole market – this is a key factor, as if a mortgage broker cannot, then you cannot be sure you are getting the best deal and saving the most money!

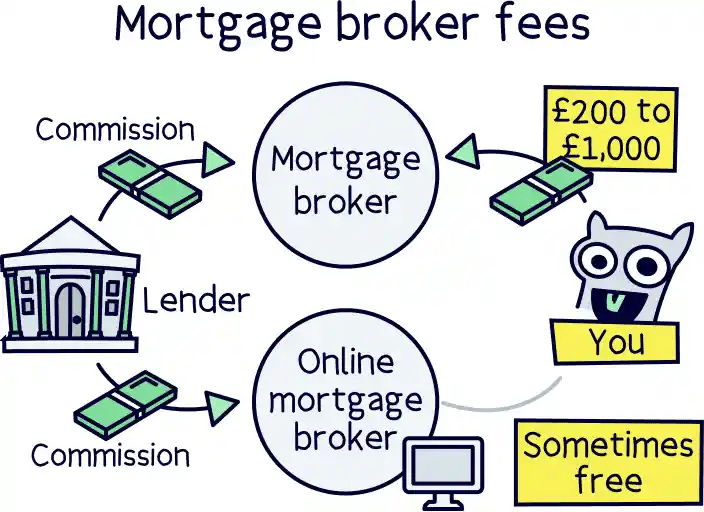

Remortgaging is fairly straightforward for a broker to do too, as you’ve already got a mortgage you have some history and most lenders will be looking for your business! So if a broker begins to quote you quite a bit in fees, we’re talking £500+, then it might be best to shop around. There are a lot of free advisors out there who can search the whole market, but if you’ve found one you like, a reasonable fee would be around a few hundred pounds.

They’re also getting paid a commission from the lender too, the company providing the mortgage, normally a bank or building society – so don’t feel guilty for shopping around for a free or cheaper one!

It’s also worth checking how quickly the mortgage advisor can process your remortgage application too, as if you are nearing the end of your fixed rate deal, you don’t really want to be paying more on your standard variable rate just because your advisor is running behind or has too much work on, or just on holiday!

And that’s all there is to remortgaging at the end of your fixed rate. Your mortgage broker will essentially handle it all for you, apply for you when you’re ready, and arrange for the new mortgage to start the day after your fixed rate deal ends, so you never have to pay that higher standard variable rate!

Not sure where to find a good mortgage advisor? Check out Tembo¹, they've got award-winning service, and guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.