Article contents

Probably not. Chances are another lender will be able to offer you a better deal, potentially saving you thousands of pounds each year! An independent mortgage broker can help you compare all the options.

Remortgaging can be a great way to reduce your monthly repayments once your fixed-rate mortgage ends. But should you remortgage with your existing lender? Or should you just call it quits and switch lenders altogether? We’ll compare the two to help bring you some clarity.

Picture this: you’re happily paying off your mortgage each month when all of a sudden your monthly repayments skyrocket. Huh?? What went wrong?

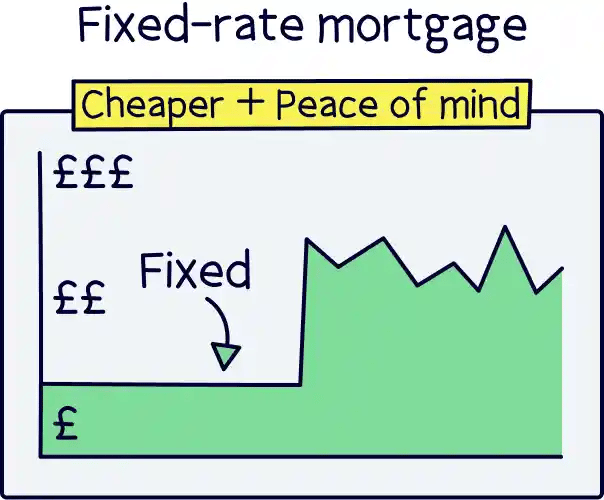

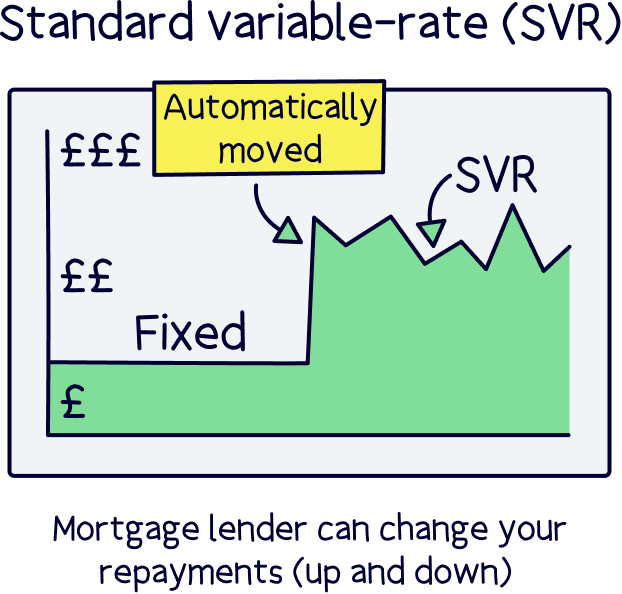

Well, most of us are on something called a fixed-rate mortgage. This is when your monthly repayments are set at a fixed price for a certain period of time.

But when this fixed-rate period ends, your lender will automatically move you onto something called their standard variable rate (SVR). This rate is usually much higher and, worse still, your mortgage lender can change it whenever they want without giving you any warning. It’s pretty sneaky!

To stop that from happening, you’ll need to remortgage. That’s what we call it when you change to a new mortgage, either with your existing lender or with a new one. Either way, you’ll be able to avoid falling onto the SVR and get a much better deal. But by choosing carefully, you may be able to save even more money, potentially getting a better rate than you were on in the first place. Kerching!

Tembo will find your best deal, fast, all with award-winning service.

Yes! Remortgaging with the same lender is pretty easy.

Firstly, they’ve already approved you for a mortgage in the past. And, assuming you’ve been settling your monthly repayments on time, they’re probably pretty confident you’ll continue to do so in the future.

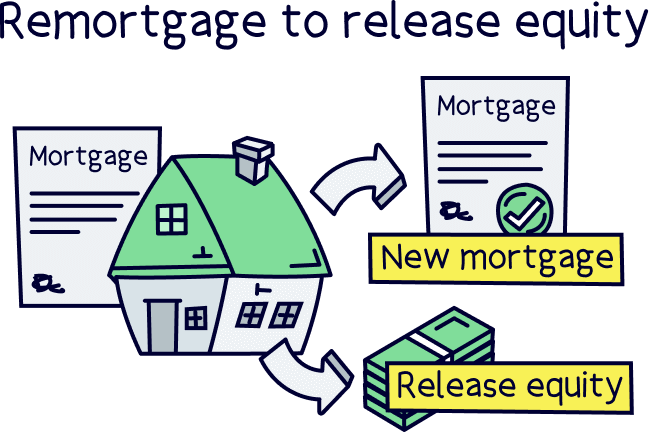

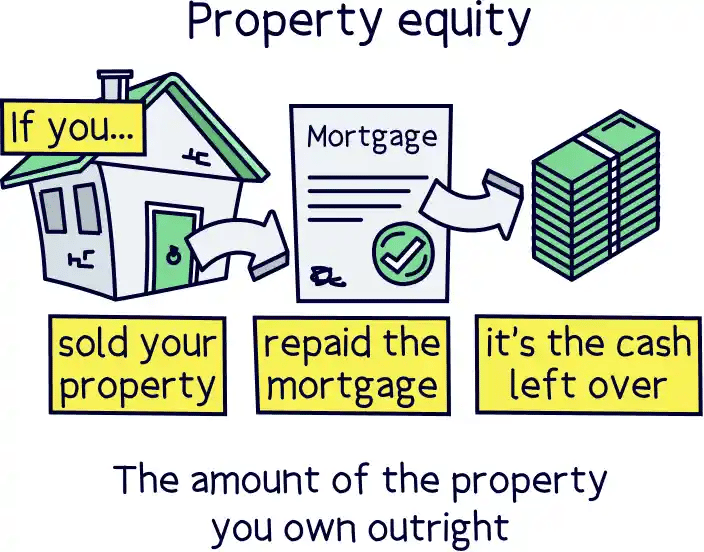

Secondly, mortgages are their bread and butter. They don’t want you to go off searching for another lender, so they might even give you a better deal to encourage you to stay. The only curveball is if you’re hoping to take out a bigger mortgage than your last one, known as remortgaging to release equity. In this case, your lender will want to do some strict checks to make sure you’re going to be able to pay them back.

In short, remortgaging with the same lender is normally as easy as pie. But remortgaging with a new lender is pretty easy too – especially if you get a mortgage broker to sort the whole thing out for you. Better still, by switching lenders, you could save thousands of pounds each year.

With that in mind, let’s take a look at the pros and cons of remortgaging with the same lender.

Here are some of the best things about sticking with your current lender.

Remortgaging with the same lender isn’t all sunshine and roses. Here’s the bad and the ugly.

Nope! At least, not usually.

When you remortgage with the same lender, it’s known as a ‘product transfer.’ In other words, your existing lender is just moving you over to a different mortgage rather than putting in a whole new application. This means you won’t need a solicitor unless you’re making big changes like adding someone else to your mortgage.

If you’re switching lenders, on the other hand, you will need a conveyancing solicitor. But don’t let this put you off! Most lenders will offer you one for free, to encourage you to join them. So, it’s not something you’ll normally need to worry about.

Ultimately, we wouldn’t recommend basing your decision on whether or not you need a solicitor. If switching lenders is going to save you thousands of pounds in the long run, it’s probably going to be worth it!

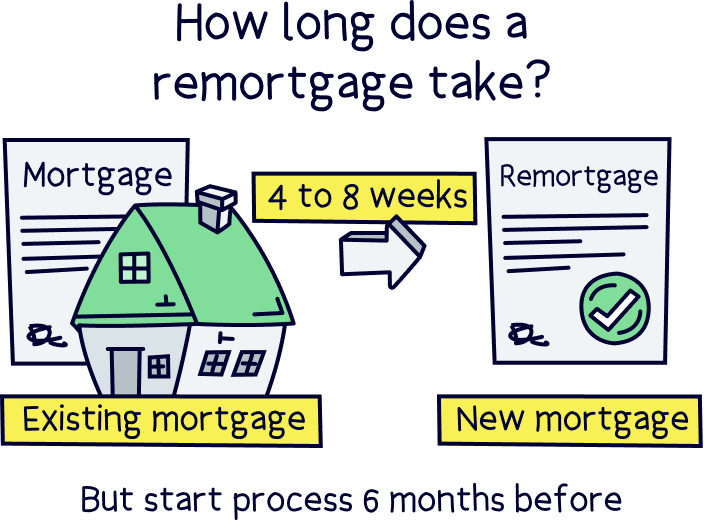

If you remortgage with the same lender, the whole thing can often be sorted in just a few days. However, if you remortgage with a new lender, you’re looking at around a 4 to 8-week wait once you’ve handed in your application.

Normally, we’d recommend thinking about remortgaging around 6 months before your fixed-rate mortgage ends. That way, you’ll have plenty of time to weigh up all the options, pick the best deal and get your remortgage application approved before falling onto that dreaded SVR (that’s the higher rate you’ll get moved onto once your fixed-rate mortgage ends). Check our guide to how long a remortgage takes for our recommended timeline.

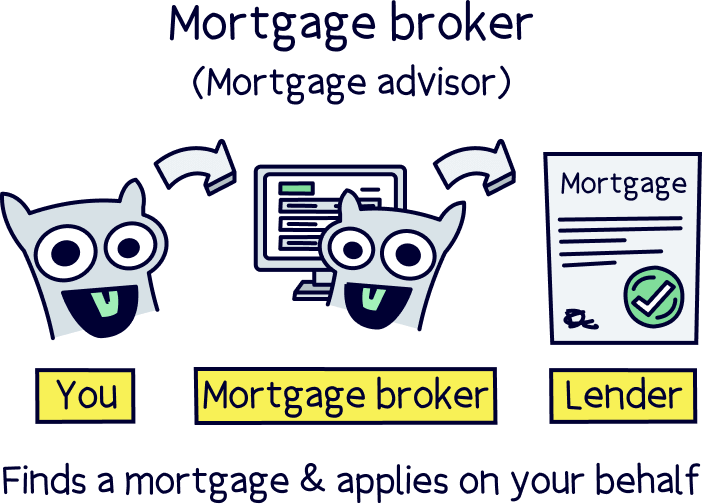

Want a friendly word of advice? Get an independent mortgage broker who can search the whole market involved. Not only will they be able to find all of the juiciest deals, but they’ll sort out the application for you too. Some will even do it for free!

Maybe, but that all depends on what’s going to save you money in the long run. We wouldn’t recommend sticking with the same lender without first comparing what you could get elsewhere.

Let’s put it like this: you might be able to save a few quid here and there by switching mobile phone providers or energy suppliers. But you could save thousands by changing mortgage lenders!

Ultimately, you’ll need to balance out the potential costs of switching (like legal fees and arrangement fees) against the amount you could save on your monthly repayments. Only then can you know for sure which is the best option.

If the idea of doing all that maths is a little daunting, don’t worry. When it’s time to start thinking about remortgaging, just get an independent mortgage broker involved. They’ll be able to search the whole market for the best deals for you and work out how to save you the most money.

Yes, that might mean sticking with the same lender. But it’ll almost always mean switching. At the end of the day, unless you explore all the options, you’ll never know!

When it comes to remortgaging, all that’s left to say is this: don’t take the backseat! It can be tempting to do the easy thing by sticking with the same lender for another few years. But you’ll never know just how much you could save if you don’t at least explore what’s out there. It could be thousands of pounds a year!

Mortgage advisors will make things a breeze by scouring the market to compare mortgages and the best deals for you. Then, whether you end up sticking with the same lender or switching to a new one, one thing’s sure. You can rest safe in the knowledge that you’re doing right by your bank account!

Need help finding one of these awesome people? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.