Article contents

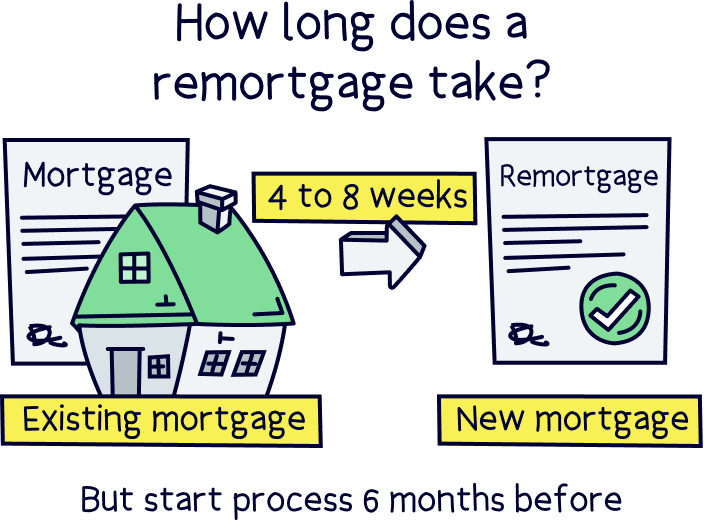

Remortgaging is easy, but not necessarily quick, allow 4 to 8 weeks for a remortgage to complete after you've applied. We recommend starting 6 months before your fixed rate ends just to be sure!

So, you got accepted for a mortgage and moved into your dream home. Happy days! But the story doesn’t end there. If you want to avoid paying over the odds on your mortgage long-term, you’ll have to think about remortgaging at some point or other.

That’s what we’re here for. We've laid out exactly how long a remortgage takes and when you should start thinking about one. Enjoy!

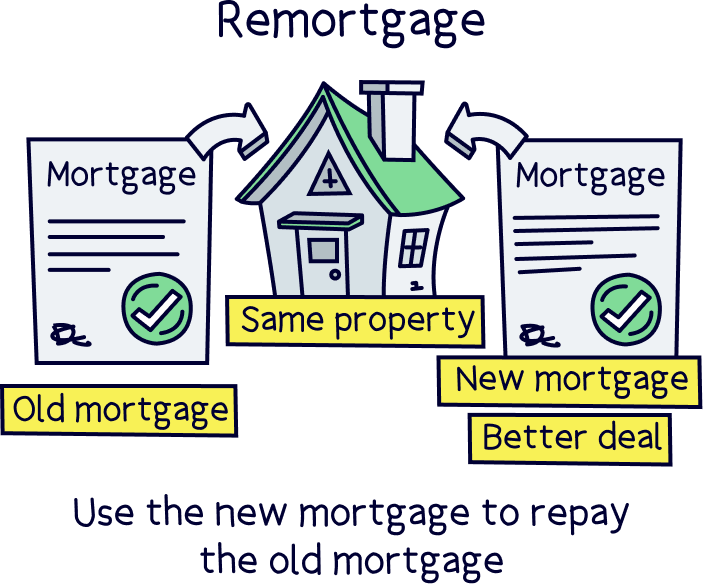

First things first: what exactly is a remortgage? In a nutshell, it’s when you change the mortgage you have on your property, either by switching to a new mortgage lender or by changing to a new deal with your current lender.

It sounds complicated but it’s pretty simple and so worth it – trust us!

Here are a couple of reasons why you might want to remortgage.

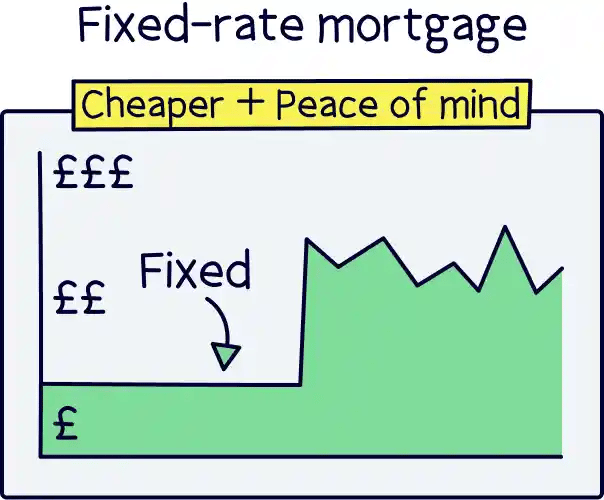

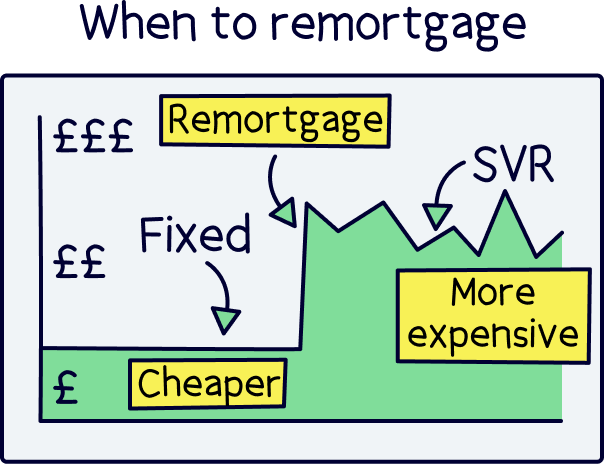

If you’re like most people, you’re currently on a fixed-rate mortgage. Don’t worry, that’s not as mind-boggling as you might think. It just means that the interest rates you pay on your mortgage are fixed for a certain amount of time (usually 2 or 5 years). So, you’ll be used to knowing exactly how much you’re going to be charged each month.

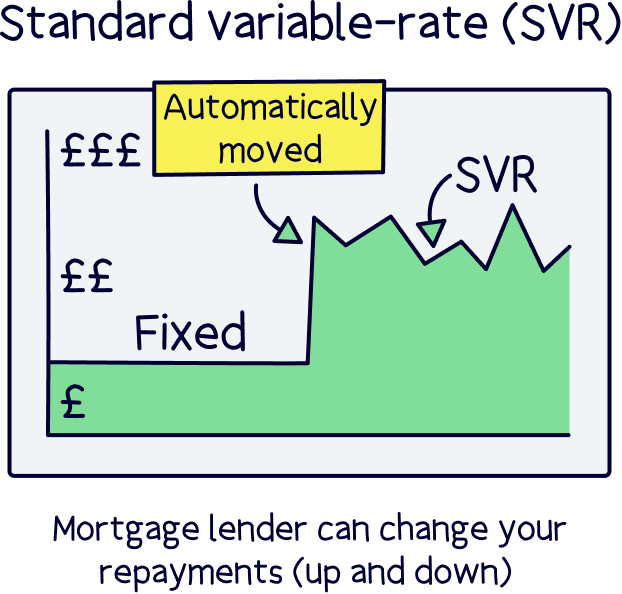

But when your fixed-rate mortgage ends, your mortgage lender will automatically charge you their normal rate (known as their standard variable rate, or SVR). This can go up or down without any notice. Worse still, it’s likely to be a lot higher than what you’re currently on, so it means your monthly repayments will go up – you could end up paying thousands of pounds more each year. And no-one wants that!

This is where remortgaging comes in. Just like how you might shop around for a better deal on your energy bills or your insurance at the end of a contract, you can shop around for a better deal on your mortgage too.

And because mortgage lenders will be trying to attract new customers, you could end up on an even better deal than what you were on in the first place. Drinks are on you!

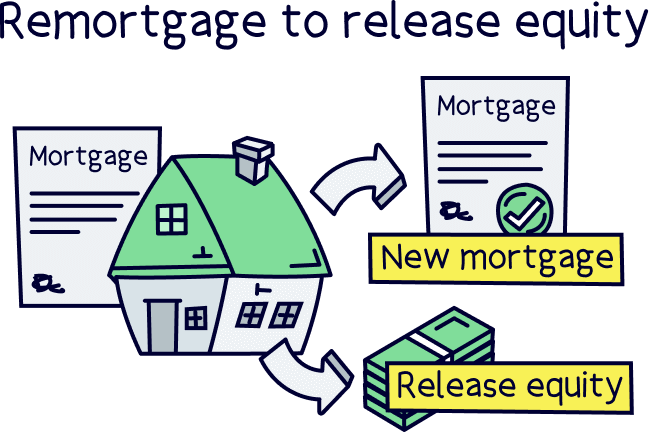

Need some cash to carry out some renovation work? Or maybe you’re after some funds for something completely non-house-related, like a car or a wedding?

When you switch to a new mortgage, you may be able to borrow a bit more against the value of your house, to release some equity. In other words, you might be able to take out a bigger mortgage, meaning you get some tax-free cash out of it. Kerching!

If you’re one of those lucky people who doesn’t currently have a mortgage on their house (known as an unencumbered property) then this could also be a great option for you. By remortgaging your house, you release funds that you can use in whatever way you want… sounds tempting, right?

Just remember that taking out a bigger mortgage means you’ll owe your mortgage provider more money, which will usually increase your monthly costs. So, it’s not a decision to be taken lightly.

Tembo will find your best deal, fast, all with award-winning service.

Just remember that taking out a bigger mortgage means you’ll owe your mortgage provider more money, which will usually increase your monthly costs. So, it’s not a decision to be taken lightly.

It normally takes around 4 to 8 weeks for a remortgage to go through after you’ve applied.

But no two people are the same so it’s impossible to say for sure. Here are some factors that could influence how long it takes.

Have you just changed jobs? Or recently become self-employed? We don’t want to rain on your parade, but that’s not always good news when it comes to remortgaging (congrats on the big life change though!).

A remortgage is treated as a whole new mortgage application, so lenders will want to start from scratch and be absolutely sure you can afford the monthly repayments.

That normally means taking a look at a good few months of payslips… If you’ve just changed jobs or you no longer have a regular monthly income, that’s obviously going to be tricky! And surprise, surprise, this could cause the process to take longer. So, give yourself a bit of extra leeway.

If you’re switching to a new lender for your remortgage, they’ll want to work out how much your house is worth – known as a valuation. This is just the same as when you first applied for a mortgage.

Think about it: if you don’t keep up your remortgage repayments, your lender will need to repossess your home – in other words, they’ll need to take ownership of your property. Then, they’ll try to make their money back by selling it themselves. They can’t very well do this if they lend you more than the house is worth!

Often, lenders just do the valuation on the computer, called a ‘desktop valuation.’ It’s super quick and they’ll sort it all out themselves, so you don’t have to lift a finger.

Where things could take a little longer is if they decide that your house is worth less than what you’ve borrowed. This is rare, but it normally means they won’t give you the full loan you’ve applied for. If that happens (and trust us, it doesn’t happen often), don’t panic! You can just remortgage with your current lender instead of switching, known as a product transfer.

Remember all the legal stuff you had to go through when you first bought your home? Well, there’s also some legal work involved when you remortgage (sorry!!).

The good news is that this time round, it will be pretty easy. The conveyancing solicitor will need to confirm that you are who you say you are and that your house definitely belongs to you (plus a couple of other little bits). And guess what? Most remortgage lenders will offer you free legal services if you use their recommended solicitors – so at least you might not have to pay those legal fees again!

Did you use a mortgage broker when you first got a mortgage? If that’s a yes then now’s the time for a fist pump. They’ll normally have your information already stored, so if you use the same broker again, that’ll help to speed things up.

That said, if you’re sticking with the same mortgage lender, you won’t have to deal with any legal work at all. They’ll be able to treat your remortgage as a product transfer, which means they can use all the legal information they got from you last time.

Just remember, as tempting as it might be to cut out the legal faff, your current lender might not be able to get you the best deal. So, don’t be a couch potato – many people change mobile phone providers just to save £100 or so. By changing mortgage lenders, you might be able to save thousands of pounds! That’s definitely worth it in our books.

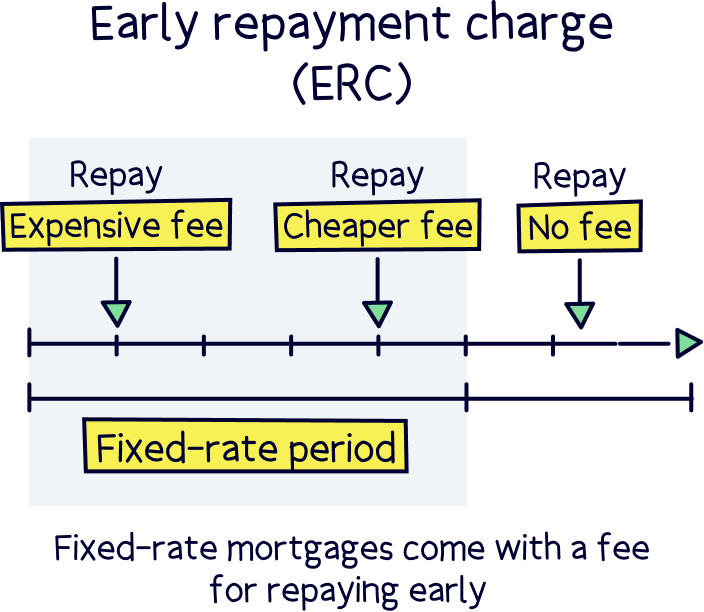

Okay, so here’s the important bit. You want to make sure your new mortgage starts right when your fixed-rate mortgage comes to an end. This way, you avoid falling onto your lender’s SVR (you know, those higher interest rates we talked about before?).

We know what you’re thinking: ‘Why can’t I just transfer over to my new mortgage now?’

Well, most mortgage lenders have early repayment charges. That means they’ll often charge you high fees for leaving early (we’re talking potentially thousands of pounds). Instead, by leaving at the moment your deal ends, you can avoid those fees and avoid paying those higher interest rates. It’s a win-win!

Just beware: you’ll usually still have to pay some fees when you remortgage. These might include product fees, legal fees and valuation fees. So, make sure you weigh up these costs against the savings you’ll make by remortgaging, to check whether it’s worth it. A mortgage broker can work this all out for you, so make sure you get one involved. More on this below!

You don’t want to end up paying those higher interest rates we talked about… right? So, you’re going to need to leave enough time to complete your remortgage before you fall onto your lender’s dreaded SVR.

Follow this timescale and it’ll be a breeze, we promise.

Forward-planning never harmed anyone. To give you the best chance of coming out the other side of this as cool as a cucumber, we’d recommend looking to remortgage as early as 6 months before your fixed-rate deal ends.

So, if you’re on a 2-year fixed-rate mortgage, set a reminder on your phone for 18 months in. That way, you’ll have plenty of time to get your finances in shape before submitting your application. That’s right, it’s time to pay off those debts, improve your credit score and stop overspending.

If you don’t have 6 months to play with, don’t worry. Just start the process as soon as you can so you don’t get burned!

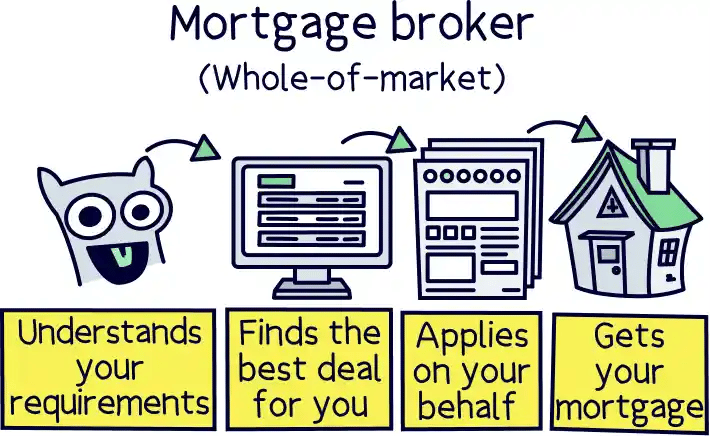

We bet you’re great at lots of things. But if you’re like most people, the ins and outs of individual mortgage lenders is not your strong suit. That’s why in our opinion, you should work with an independent mortgage broker (also known as a lifesaver) to get the best deals.

They’ll know all about the different lenders and what they can offer. Better still, they’ll be able to look at your finances (and your wishlist) before recommending the best mortgage lender for your circumstances. Plus, some of the bigger ones are free, so what’s there to lose?

If you’re not sure where to start, check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

You’ll want to submit your remortgage application around 2 to 3 months before your fixed-rate period ends (you know, so you don’t fall onto that SVR we keep banging on about!).

But there’s no harm in doing it earlier if you want to be super organised – some mortgage lenders will let you hold a mortgage offer for up to 6 months. This can be especially handy if interest rates are low and you want to bag a deal straight away.

If you follow our previous step and get a mortgage broker involved, now’s the time to act smug: they’ll sort the whole thing for you so you won’t have to worry about the application at all!

That’s right, you just sit back, relax and make your way through Netflix’s whole back catalogue while your mortgage broker gets to work. It’s that simple!

Got your application in with time to spare? Go you! But don’t get too excited just yet. There’s still a lot of waiting to do.

Before your remortgage can go through, your lender will need to carry out a credit check (where they check whether you have a good track record for paying back money) and get your property valued (which they’ll often just do on the computer as a ‘desktop valuation’). There’s also the legal stuff to sort. Usually, you won’t have to think about any of this as your new lender will take care of it all – even down to providing you with a solicitor, which most lenders will do for free!

The conveyancing alone (aka: the legal stuff) usually takes around 4 weeks on a remortgage, but it’s best to leave a bit longer if you can in case there are any holdups. Ultimately, you could be waiting up to two months for the whole thing to go through. So, put the kettle on!

This is the part where you pat yourself on the back, treat your partner to a fancy meal and enjoy the potentially massive savings of having remortgaged instead of falling onto your lender’s SVR.

If you’ve taken out a bigger remortgage to release some equity then you may as well go the whole hog and fork out on some caviar (or something equally as posh). You’ll usually get the tax-free cash in your account around 4 to 8 weeks after submitting your application.

Right: get out your diary (or your smartphone if that’s how you roll) and put a big red circle around the date 6 months before your fixed-rate mortgage comes to an end.

Then, when the time comes, you know what to do! Don’t let yourself pay over the odds on your lender’s SVR. Instead, get a mortgage broker involved and see if you can make a saving. When you’re sunning yourself in Barbados (or, much more sensibly, saving for your kids’ futures!), you can thank us.

Not sure where to find a great broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.