Article contents

The quickest way to remortgage and make sure you’re getting the best possible deal at the same time is to use a mortgage broker. Mortgage brokers are professionals who can sort your whole remortgage out for you, from start to finish.

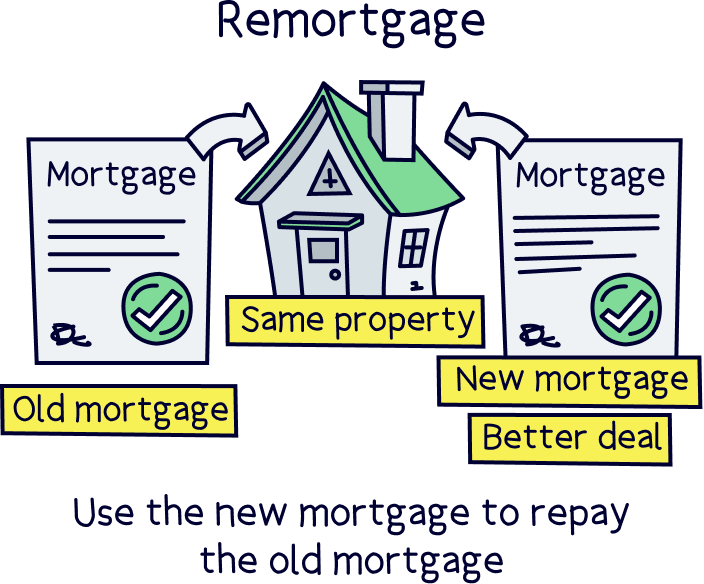

Remortgaging is when you swap your existing mortgage for a new one, either with your current mortgage lender or with a different lender altogether (mortgage lenders are the people who give out mortgages).

Trust us, if you want to avoid paying more than you need to in your monthly mortgage repayments, you’re going to love remortgaging. And you’ll be pleased to know that it’s actually really quick and easy to do! Here, we’ll show you how to remortgage quickly. But first…

If you’re like most people, you probably shop around for the best deal on your mobile phone contract or your energy bills. Remortgaging is exactly the same, but with mortgages. It allows you to switch your current mortgage for a new one, in order to get a better deal and save money on your monthly mortgage payments!

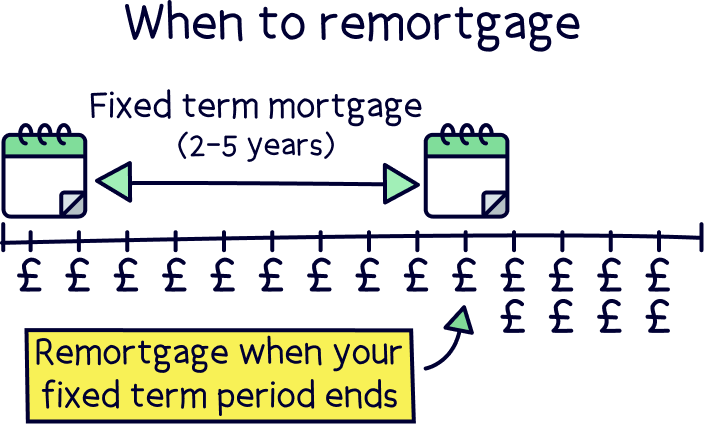

The chances are that when you first got your mortgage, you got a type called a fixed-rate mortgage. Fixed-rate mortgages are ones where your monthly payments are set at a fixed cost for a certain period of time. This is often for 2 to 5 years and is known as your fixed-rate period or, fittingly, your incentive period – because your lender will often give you a nice low rate to incentivise you to pick them!

While you’re in your fixed-rate period, you won’t normally need to remortgage because you’ll be locked into that lovely low rate. And anyway, if you leave during this time, you’ll have to pay a hefty fee known as an early repayment charge. So, you’ll usually be best off staying put!

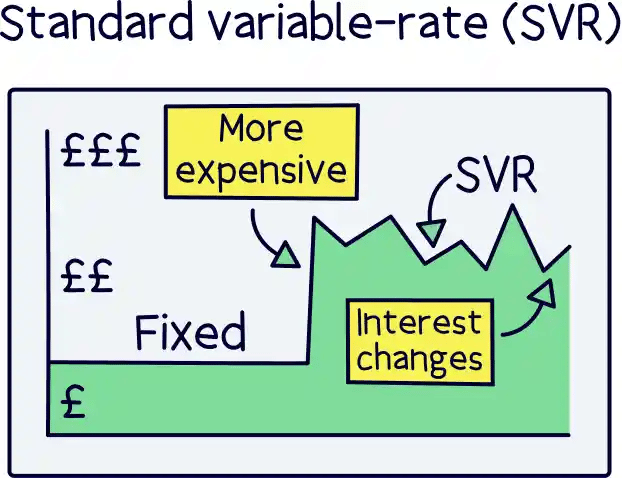

However, when your fixed-rate period comes to an end, your mortgage lender will suddenly hike up your prices, as they’ll automatically put you on something called their standard variable rate (SVR). Not only will this rate be much more expensive, but it can also go up and down without warning. Normally, it will move around roughly at the same time as the Bank of England base rate (that’s the UK’s official borrowing rate). But technically, your mortgage lender can change it whenever they fancy – not good!

Here’s where remortgaging comes in. Switching to a new mortgage means you can avoid falling onto your lender’s dreaded SVR and access way cheaper monthly mortgage repayments. In fact, remortgaging to avoid falling onto a lender’s SVR can save £100s per month.

If you haven’t remortgaged in a few years, the chances are you’re already on your lender’s SVR and paying more than you need to. So, you’ll need to remortgage as soon as possible to reduce your monthly payments again.

Or, if you’re still in your fixed-rate period but it’s coming to an end, make sure you start thinking about remortgaging a few months in advance. That way, you’ll have plenty of time to get a new deal lined up for when your fixed-rate period ends. Simple! Read our when you can remortgage article to learn more.

Of course, not everyone is on a fixed-rate mortgage or wants to go onto a fixed-rate mortgage moving forwards. You may prefer a variable mortgage where your monthly payments can go up or down from month to month (we know, it sounds similar to the SVR, but most variable mortgages are much cheaper and more appealing, we promise!).

However, the same principle nearly always applies as your lender will draw you in with a great deal on your variable mortgage for a set period of time (your incentive period) before automatically moving you onto your lender’s SVR and hiking your prices up. So, remortgaging is still your best friend!

If you're worried about fees to remortgage, don't be! There's not many, and often free.

Your mortgage advisor will explain everything (more on this below).

Tembo will find your best deal, fast, all with award-winning service.

So, now you know why remortgaging is so awesome. But how do you actually do it? Well, there are two super quick ways to remortgage.

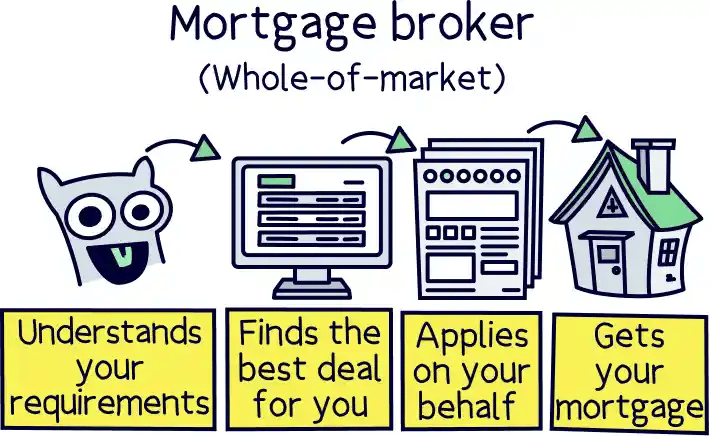

This is our favourite way to remortgage quickly. Mortgage brokers, also known as mortgage advisors, are experts who can help you to get a mortgage – whether you’re remortgaging or getting a mortgage for the very first time!

You don’t have to use one but trust us, we think you’ll want one. Why? Well, because they’ll take the time to get to know you and your unique situation before finding you the best mortgage deals out there and helping you to pick the right one for you.

Plus, once you’ve chosen your mortgage, they’ll sort out the whole application process for you too. That’s right, you just sit there twiddling your thumbs while they do all the hard work, saving you a ton of time. Nice!

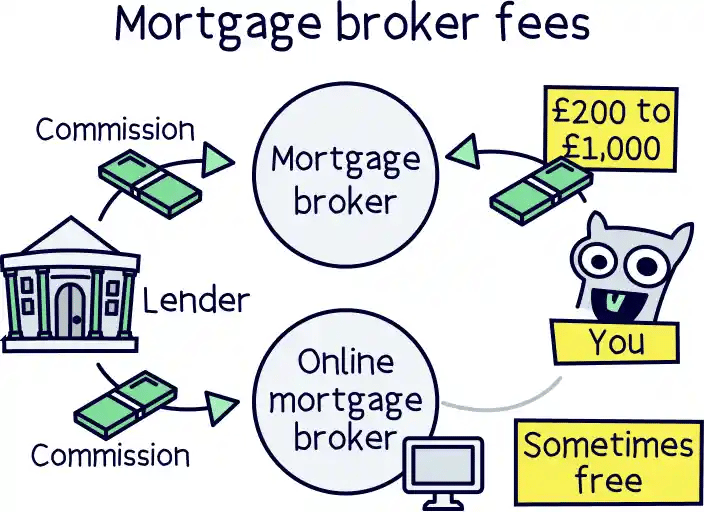

Now, considering how amazing mortgage brokers are, you might assume that they’d be really expensive. But that’s not the case at all. Lots of mortgage brokers are free for you to use as they get paid by the mortgage lender you end up going with, rather than from your own pocket. Hooray!

Some mortgage brokers will charge you a fee. But they’ll still normally save you more money than what you end up spending with them. So, we think they’re worth it!

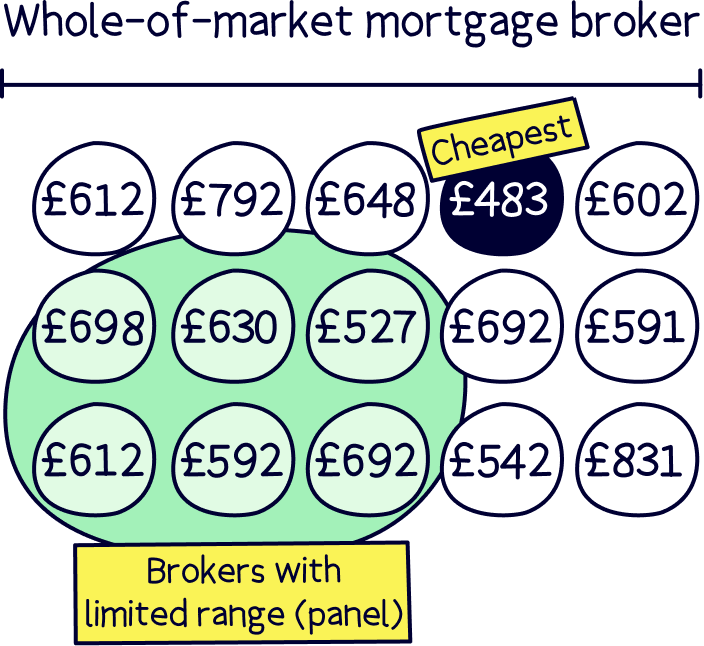

There’s just one thing to watch out for: make sure you use something called a ‘whole-of-market’ mortgage broker. These are mortgage brokers who can compare mortgages from lots of different lenders, instead of being tied to a few lenders that they have to recommend. So, they’re your go-to for finding you the best deals and saving you lots of money!

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

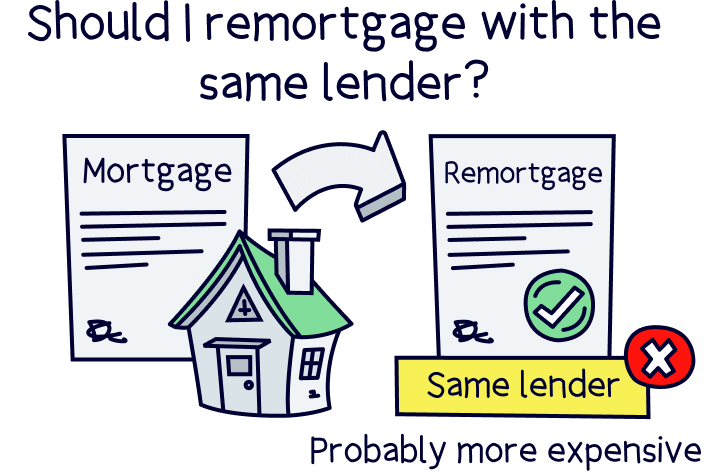

Are you happy with your current mortgage lender? In which case, an even quicker way to remortgage is to do a product transfer. That’s where you switch to a different mortgage with your existing mortgage lender. And it’s really fast and easy.

Let us explain. If you switch to a new mortgage lender, they’ll need to carry out some checks on you before approving you for the remortgage. That will include things like valuing your home (checking to make sure they agree with what it’s worth) and carrying out a credit check (checking to see how good you’ve been with money in the past). Those things can take a bit of time.

However, if you do a product transfer with your existing lender instead, they’ll have all your details saved from last time. That means they can normally just move you over to a new mortgage without having to carry out as many checks. Oh, and they’ll know how good you’ve been at keeping up with your monthly mortgage repayments too – so, assuming you haven’t missed any, they’ll probably be very happy to carry on lending to you!

All sounds very appealing, right? Well, it is. But there’s just one problem: without shopping around, you’ll have no way of knowing whether you could get a better deal elsewhere!

In fact, with over 100 mortgage lenders in the UK, the chances are that at least one of them will be able to give you a much better deal, which you’ll miss out on by doing a product transfer. Let’s put it like this: you might be able to save a bit of money here and there by switching mobile phone providers, but that’s nothing compared to the thousands of pounds you could save by changing mortgage lenders!

That’s why we’d always recommend using a mortgage broker so you at least know what other deals are out there. If your mortgage broker can’t find a better deal, then you can just go ahead with the product transfer and there’s no harm done. But if they can find a better deal for you, you’ll be able to make an informed decision on whether to remortgage with the same lender or to switch to a new one. Makes sense, right?

If you’re on your lender’s dreaded SVR, approaching the end of your incentive period or just keen to find a better deal, follow these simple steps to remortgage quickly. We promise, you’ll barely have to lift a finger and can spend all that time you save doing much more exciting things… Netflix anyone?!

First things first, you’ll want to find one of those superheroes we mentioned earlier called mortgage brokers.

We’ve already banged on a bit about how great they are, but just as a reminder, they’ll help you with your remortgage from start to finish. That includes finding the best deals available to you and filling in your remortgage application for you when the time comes. Lucky you!

Just remember to use a whole-of-market mortgage broker who can compare lots of different mortgages and lots of different lenders to get you the best deal possible.

We recommend you check out Tembo¹, they've got award-winning service, and guarantee to get you the best mortgage deal. Plus, get 50% off their fee with Nuts About Money.

You know how we said that your mortgage broker will go out there and hunt for the best mortgage lenders and deals for you? Well, now’s the time you get to choose between all of those lovely deals they’ve dug out.

Of course, the deals your broker shows you will be the cheapest they’ve found. But there’ll probably still be a few different options – for example, if you’re after a fixed-rate mortgage, they might show you a 2-year fixed-rate deal and a 3-year fixed rate deal, so you can choose between them.

Don’t worry if making the choice sounds a little daunting. Your mortgage broker will give you advice and help you decide which one is best for you. Told you it would be easy!

Now your mortgage broker needs to get your remortgage application ready. Don’t worry, you don’t have to get involved in the application itself as your broker will handle the whole thing for you. But you will need to give them a few details to help, including things like your ID and bank statements.

We know, we know, digging these things out can be a bit of a pain. But guess what? Your mortgage broker can keep all this info saved for your next remortgage! So as long as you use the same broker next time, you won’t have to worry about this again. Get in!

Last but not least, all that’s left is to sit around and let your mortgage broker do the hard work for you. They’ll submit a remortgage application, your lender will carry out some checks and there’ll also be a few legal bits to sort, known as conveyancing.

However, you really don’t have to worry about any of that when you do a remortgage because your broker and lender will usually sort everything out between them. In fact, your new lender will normally even provide you with a solicitor for free (those are the professionals who can help with the legal side of the remortgage).

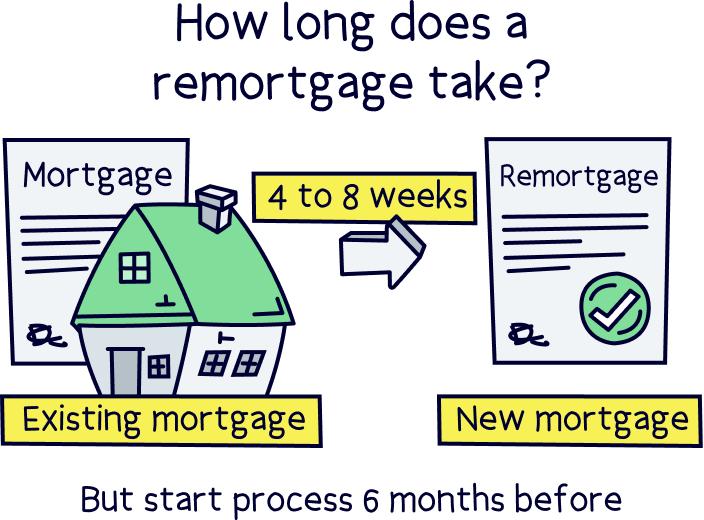

In total, a remortgage typically takes around 4 to 8 weeks to complete from the date of handing in the application. But with one of these awesome people called mortgage brokers by your side, you won’t have to spend more than a couple of hours on it yourself. So, just be patient and you’ll enjoy those lovely lower monthly payments (compared to that stinky SVR) before you know it!

If you haven’t used a mortgage broker before, you might well be thinking: ‘Do I really need one? Can’t I just compare mortgages myself?’

Well, no, you don’t really need one. But you’ll definitely want one. Especially if you’re looking to remortgage quickly!

If you decide to go ahead without a mortgage broker, you can use a comparison site to find decent deals. But you would then need to approach lenders individually to find out whether they’re happy to give you that deal – every lender will have different criteria, so it’s a bit of a minefield trying to understand what each lender is looking for.

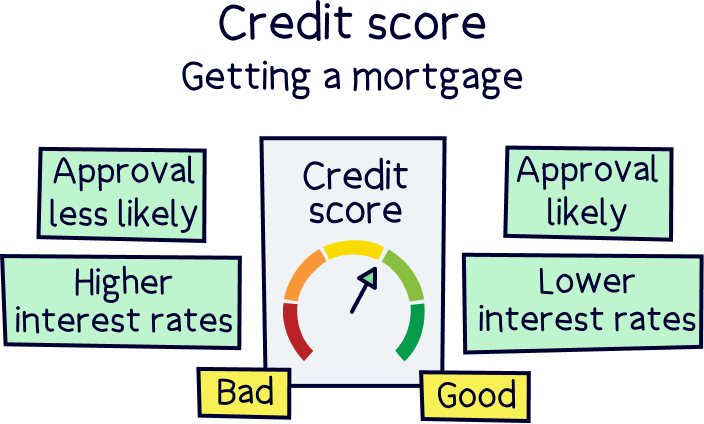

Plus, if you apply to a mortgage lender and they reject you, it could negatively impact your credit score (that’s the score that shows lenders how good you’ve been with money in the past).

On the other hand, a mortgage broker is an expert who knows the ins and outs of the different mortgage lenders. They’ll know which lenders are likely to be able to offer you the best deals given your personal situation, and which ones are most likely to accept you. Not only that, but remember how we said that they’ll sort your whole remortgage application out for you?

That’s right, these experts will take matters into their own hands and make it their business to get you that remortgage you’re after – saving you time, money and making it as likely as possible that you’ll get approved. What’s not to like?!

Nobody likes paying more than they have to, so make sure you avoid your lender’s dreaded SVR by remortgaging when you get to the end of your incentive period. That way, you could reduce your mortgage payments by hundreds of pounds a month!

If you’re ready to grab the bull by the horns and avoid your lender’s SVR, the first step is to get a mortgage broker involved. Not only will they be able to save you money by finding you the best deal. They’ll also be able to save you a ton of time by handling your remortgage from start to finish without you ever lifting a finger. Bliss!

To recap, if you need to find a decent mortgage broker, check out Tembo¹, they've got award-winning service, and guarantee to get you the best mortgage deal. And, you'll get 50% off their fee with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.