Article contents

The Bank of England base rate, officially called bank rate, is currently 3.75%, and it's the interest rate banks get charged when they borrow money from the Bank of England. It’s also the interest rate banks receive if they save their money with the Bank of England. The rate is used to control inflation (the price of goods and services rising over time), which helps keep the country financially stable.

The Bank of England base rate isn’t as complicated as it sounds. Here's everything you need to know and how it affects your money.

Heads up, it’s officially known as the ‘bank rate’, and it’s set by the Bank of England – who are responsible for managing money in England, such as printing new bank notes, and keeping the country financially stable.

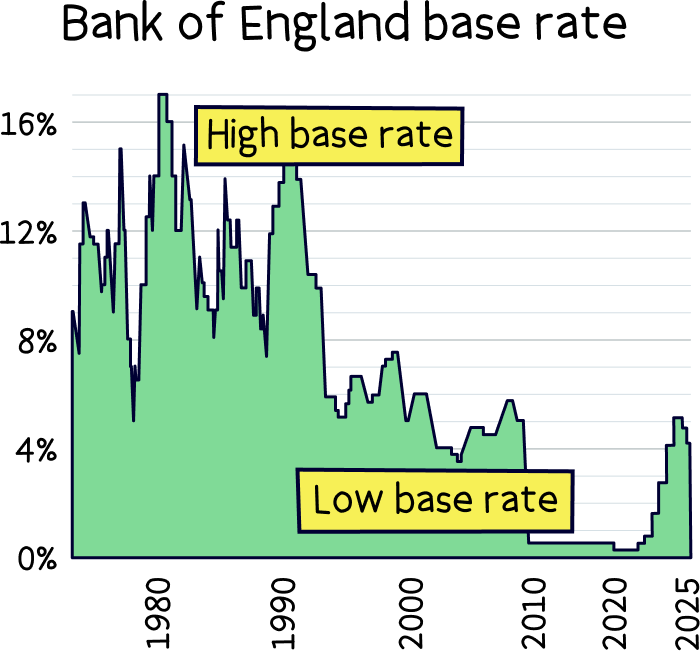

The current Bank of England base rate is 3.75% (changed in December 2025).

It was much lower at 0.10% at the beginning of the Coronavirus pandemic, and has been as high as 17% in 1979. But what does this rate actually mean..?

The base rate is an interest rate, just like you’d get if you went into your bank and asked for a loan, or opened a savings account – it’s a cost of borrowing money, or a reward for saving money.

However, the Bank of England interest rate is slightly different to what we’d get from a high street bank…

Believe it or not, the banks borrow money too, from the Bank of England, and they pay interest on this, which is always the Bank of England base rate. They also keep some of their money with the Bank of England, just like your savings with the bank, and in return they get interest, which is the Bank of England base rate too.

This can affect you when you borrow or save money with your bank. As they’re either borrowing money or storing their money with the Bank of England, to offer you things like loans and savings accounts, and they’ll be paying or receiving the base rate as interest (more on this below).

So why does the bank rate actually exist? Well, the purpose of the base rate is to keep inflation ‘low and stable’...

Why is this important? Inflation is a fancy word for the cost of living increasing – that’s the cost of everything you buy regularly such as food, clothes, energy, petrol, services etc.

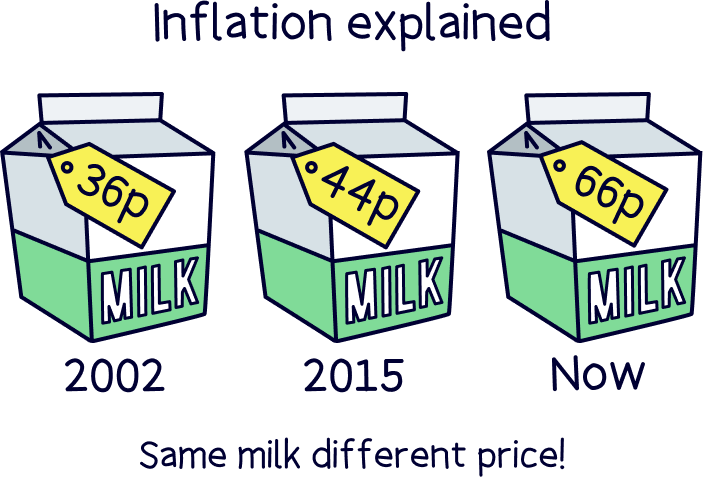

For example, in the year 2002 a pint of milk cost 36p, and now it costs 66p – that’s nearly double the price! It's the same amount of milk, inflation has just increased it!

It’s measured as a percentage, and represents the average of these costs increasing each year.

Note: The Bank of England has a target of keeping inflation at 2% increase per year, in order to keep the country stable.

Inflation can have a huge impact on you and your money, if inflation rises a lot over a short period of time, the cost of living can get very expensive, very quickly – particularly as wages don’t tend to rise in line with them. It means your money will buy a lot less, your money will quickly be devalued.

This makes people spend less because things become expensive, and when people start spending less, it begins to harm the whole economy, and businesses begin to struggle with lower sales and potentially could go out of business, causing unemployment, and even less spending, and a spiral begins causing a devastating impact on the country as a whole. Sorry to be a downer!

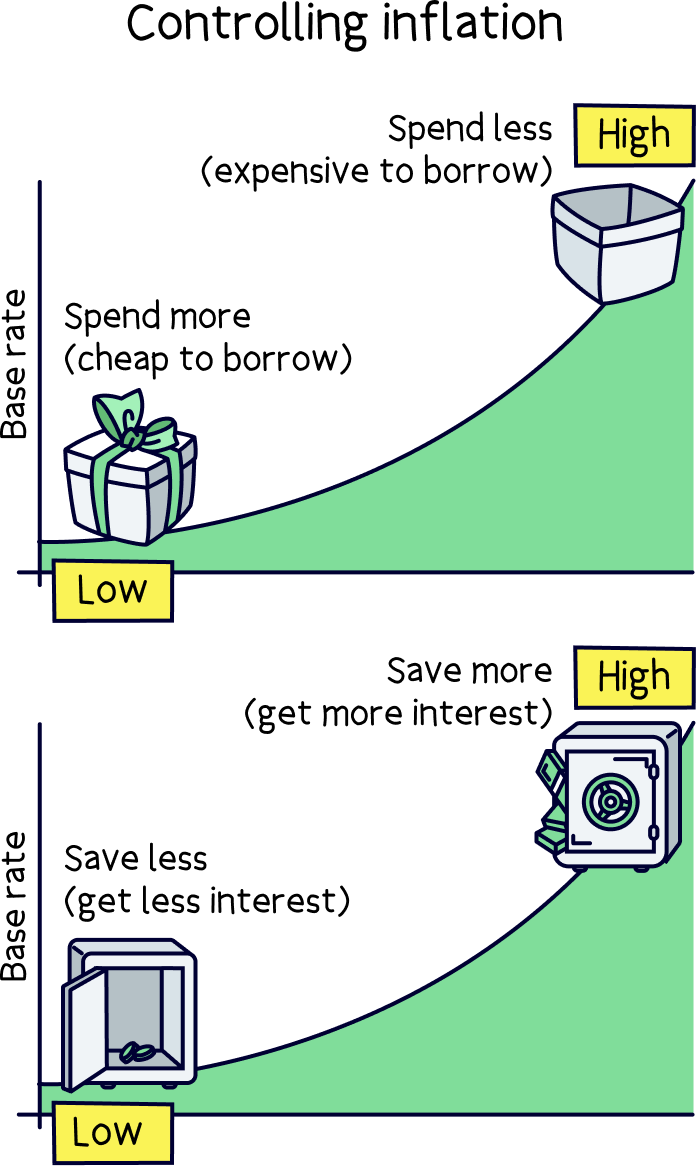

To stop this from happening, the Bank of England has to control inflation, and they do this with the Bank of England base rate. When it’s lower, the cost of borrowing money is lower and people begin to borrow money to buy things, have more spare cash to spend, and save less as they’re not getting much interest in return (because interest rates on their savings are very low).

When the base rate is higher, borrowing money becomes more expensive, and people tend to borrow less, have less money to spend, but also get more interest on their savings, so tend to save more.

Confusing right? Let’s explain more...

When banks borrow money from the Bank of England, they use this money to give their customers things like loans and mortgages – with a nice profit on top for them of course.

Let's assume the base rate is 4.25%, and let's take mortgages as an example.

A bank's standard mortgage might have an interest rate of 6.25%, with the bank borrowing money from the Bank of England at 4.25%. If the Bank of England put the rate up from 4.25% to 4.50%, your mortgage would usually go up by the same amount, so an increase of 0.25% too, making your mortgage interest rate now 6.50% – it might not seem much but could be £100s extra per month.

Note: you can normally get a fixed-rate mortgage deal, where the interest rate is fixed for a set period of time, normally 2, 3 or 5 years, so it’s not impacted by increases in the base rate, and it’s often a good thing to do. Need a new mortgage soon? We strongly recommend using a mortgage advisor to find you the best mortgage deal and even apply on your behalf.

It also affects your savings too if you keep them with a bank. Your bank will be keeping some of the money with the Bank of England and earning interest at the base rate set.

Savings rate example: If the Bank of England base rate is 4.25% and the bank gives you an interest rate of 2.25% on your savings they are making 2% of your money every year as a hidden fee. Very cheeky but it works, there's a reason why banks are so profitable!

Anyway, when the base rate increases, the banks are earning more money from the increase, and often they’ll pass this onto their customers to keep them happy (there's usually a bit of a delay to pocket a bit more free money, again very cheeky).

Let’s say the base rate increases to 4.50% from 4.25% (so a 0.25% increase), you might see the interest rate on your savings account increase by the difference, 0.25% too. Although it’s not guaranteed and up to the banks themselves to pass on any increases (if you have a fixed-rate savings account, you won’t get this increase).

The Bank of England has a Monetary Policy Committee (MPC), who sets the bank rate. It’s a group of 9 people who know a thing or two about economics, such as the Governor and the deputies of the Bank of England. And they’ll vote roughly every 6 weeks on what the base rate should be after considering what’s happening with inflation, and if there are new Government policies.

Hopefully this wasn't too complicated. So the Bank of England base rate (bank rate), is simply the rate at which banks can borrow money from the Bank of England, and it’s also the interest rate banks can get if they keep their money with the Bank of England.

It’s used to control inflation, which is the cost of living, with the aim of keeping everyone’s money and ultimately the country stable, which ultimately helps you plan better for the future.

Speak to a mortgage advisor, they'll know what's best for you. Here's where to find the best advisor for you.

Speak to a mortgage advisor, they'll know what's best for you. Here's where to find the best advisor for you.

Speak to a mortgage advisor, they'll know what's best for you. Here's where to find the best advisor for you.

Speak to a mortgage advisor, they'll know what's best for you. Here's where to find the best advisor for you.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Speak to a mortgage advisor, they'll know what's best for you. Here's where to find the best advisor for you.