Interest may not be tax-free (like an ISA (below)), but you can save as much as you like. Access your money whenever you like. All available online. Interest rates are AER* variable.

High Interest Vault. Capital at risk. This is an investment product. Not directly FSCS protected. Read Lightyear review.

Capital at risk. Interest earned daily, paid monthly.

When investing, your capital is at risk and you may get back less than invested. Past performance doesn’t guarantee future results. Earn interest on money within your investment account. Read Trading212 review.

Account is with a leading bank through Raisin. More top rates available via the platform.

T&Cs apply. Read Wise review.

Simple Saver account. T&Cs apply. Read Moneybox review.

Interest is completely tax-free, and you can save up to £20,000 per year. Access your money whenever you like. All available online. Interest rates are AER* variable.

Capital at risk. ISA terms apply. Read Lightyear review.

Read Trading 212 review.

T&Cs apply. Read Moneybox review.

T&Cs apply. Read Moneyfarm review.

T&Cs apply. Read Plum review.

All data is sourced by Nuts About Money, or provided directly by the provider. Seen something inaccurate? Get in touch.

Earning a small bit of interest on your savings, or nothing at all? It’s a good idea to move it to a high interest savings account – you could earn £100s per month. And, if you want to access your money instantly (meaning it’s not ‘locked away’ where you can’t touch it), an easy access savings account is likely your best option.

We’ve done the hard work and researched the best easy access savings account in the UK.

There’s a lot of savings accounts out there, and most of them do not pay very well at all (meaning low interest rates), mentioning no names (all the big banks!). However, there are some great ones out there, some that you might not be familiar with, but offer a really great interest rate (how much money you’ll make), are easy to use, and have all the safety and security you want (and more) from a savings account.

When it comes to the best easy access accounts, the interest rate is super important (you might have guessed it). But we’ve also included lots of different factors, to determine the best overall. Here’s our criteria:

We’re just focusing on easy access savings accounts, rather than ‘notice’ savings accounts (where you have to ask for your money and wait a number of days, such as 28 or 90 days), and ‘fixed-term’ savings accounts, where your money is locked away for a set period of time (such as 1 or 2 years), and you won’t be able to access your money during that time (unless you pay very hefty fees).

The easy access accounts we recommend are all ones we recommend to our friends and family too. So you can be confident that whichever of our recommendations you opt for, you’ll be using one of the best savings accounts out there.

Interested in learning more? Here’s our full review methodology and how we test.

They’re pretty much the same – these days the terms are pretty much interchangeable.

Traditionally, with an instant access savings account, you’d typically have a card (cash card), which you can use to withdraw money from a cash machine (ATM), and as many times as you like. However modern instant access accounts don't tend to offer a card anymore.

With an easy access account, you typically wouldn't have a cash card to withdraw money from an ATM, you’d simply send money from your savings account to your regular bank account (e.g. your current account).

There could be a limit on the number of withdrawals you can make too (withdrawal limits are part of our criteria, and all of our recommendations have a high number of withdrawals or unlimited).

Easy access savings accounts are pretty simple really – all you need to do is add money to your account (deposit), and you’ll start earning interest. As simple as that.

And as they’re easy access, you can take your cash out whenever you like, without having to give notice – you’ll be able to transfer it to your bank account straight away.

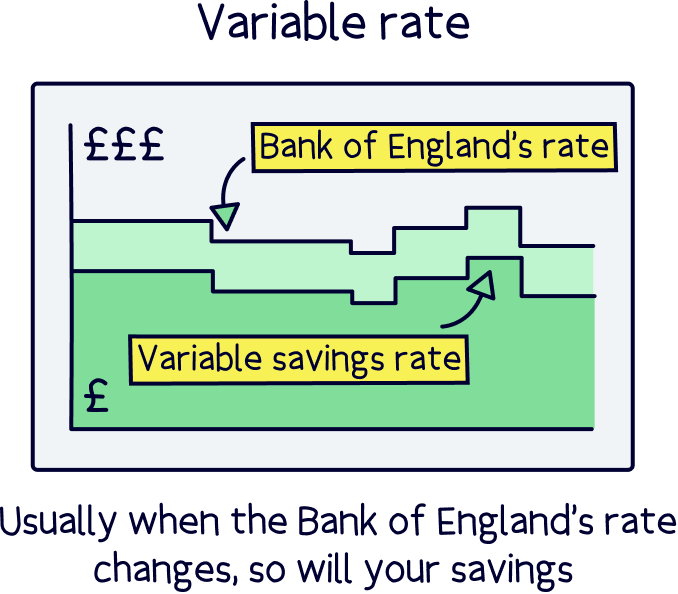

Easy access accounts (and instant access accounts) normally have a variable interest rate. This means the interest rate can go up and down over time, when the savings account provider decides to change it. Normally this is in line with the Bank of England base rate (the interest rate the banks get paid to deposit their customers' money with the Bank of England).

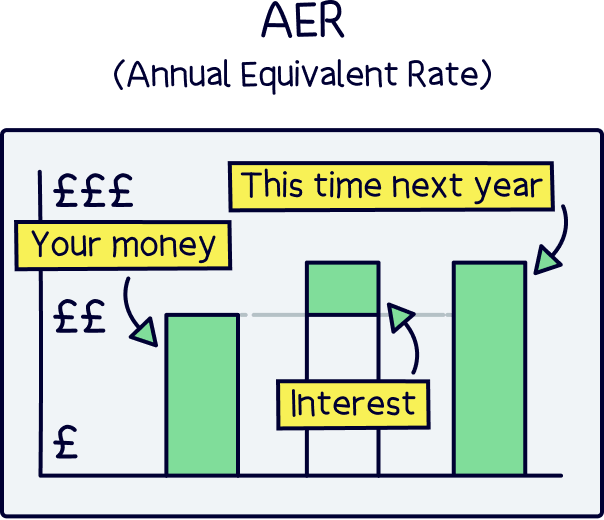

‘AER’, or Annual Equivalent Rate, is often used to measure the interest rate on a savings account. It means how much you’ll make (as a percentage) this time next year.

So, if the interest rate is 5% AER, you’ll earn 5% of your money this time next year. Simple right?

To work it out is a bit complicated, and it takes into account compound interest – which is your interest you get, making more interest. For instance, if you earn interest monthly, the monthly interest you make, will begin to make interest the next month, and this snowballs over and over (called compounding).

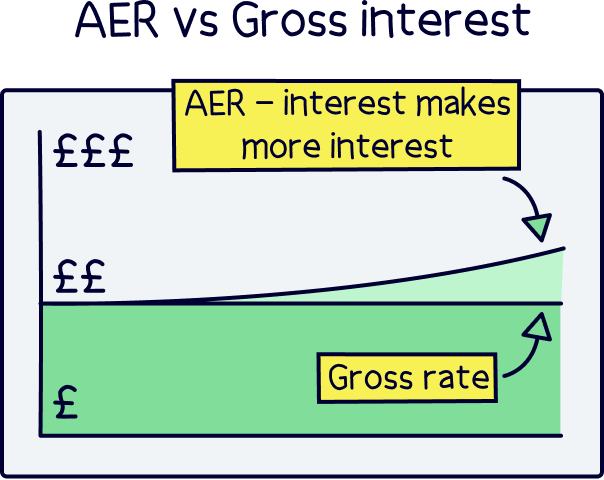

The alternative measure for savings accounts is the ‘gross rate’, and this is simply how much the account pays without taking compound interest into account.

Nuts About Money tip: if you want to compare easy access accounts yourself, always use AER, or always use the gross rate – don’t compare the two against each other, otherwise it won’t be a fair comparison (AER would normally show higher).

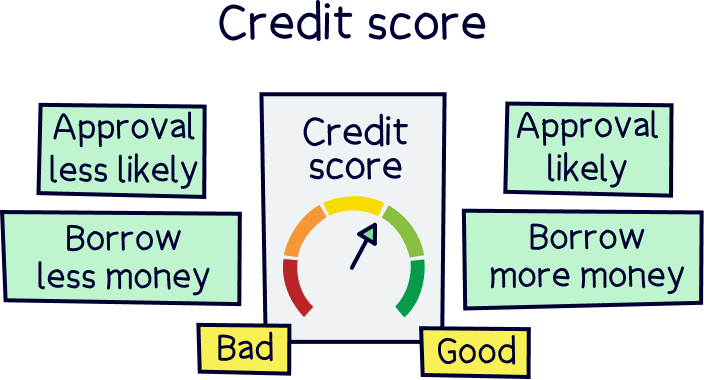

A credit check is where you’ll be checked to see if you’re worthy of borrowing money from a bank, and is often represented as a credit score. If you have a low credit score, which can happen if you don’t repay your debts on time, you likely won’t be able to borrow money.

With savings accounts, as you’re not borrowing money (getting credit), there’s typically not any credit checks involved.

You’ll likely still need to prove who you are, such as taking a photo of your driving licence or passport, and a few banks may carry out a ‘soft’ credit check (which just checks who you are), and they use this in order to verify your identity (this doesn’t leave any marks on your credit report).

This means opening a savings account does not impact your credit score – it also means it won’t improve your credit score either (in case you were thinking of opening a savings account to improve your score).

With an easy access savings account, you can normally start saving with as little as £1. However, it does depend on the savings account. With some, you’ll need a minimum deposit of £50, £100 or more (£1,000+).

All of our recommendations above have a very low minimum deposit (£1).

With some savings accounts, you’ll get a bonus when you open an account, which is typically a higher interest rate for the first 12 months.

These can be great initially, but typically the interest rate after 12 months is pretty bad. The bank is really relying on you not switching after 12 months, either forgetting about it, or not realising that you can move your money wherever you like. Loyalty doesn't pay!

These savings accounts can also have restrictions, such as not withdrawing money for a certain amount of time after you open the account.

We don’t typically recommend these accounts as you’ll need to switch again after 12 months, or whenever the bonus period ends, and there’s a risk you might forget – plus all the extra admin and time looking for another account again.

It’s often best to go for a high interest savings account without a bonus (unless the bonus is very good, and we mean very good!).

Getting an easy access savings account, or a different type of account is completely up to you and your financial circumstances, but, if you think you might want the cash again soon, or simply want the option to withdraw your money whenever you like, then an easy access savings account is a great idea.

If you are planning to save for the long-term (for instance, a few years, or longer), and not concerned about getting your cash back anytime soon, then you could opt for a longer term savings option (covered below).

A notice account is a savings account where you have to give ‘notice’ to get your cash back out. These can have a higher interest rate than an easy access account (but not always). They normally come in 28 days, 90 days, 180 days or 1 year, but can be any time frame.

This could be a fixed-term savings account (for instance 5 years), where you might get a higher interest rate, but will need to lock your cash away (getting a slightly higher interest rate probably isn't worth locking your money away for many years).

Typically these have a higher minimum deposit, such as £1,000, and would require your money to be deposited as a lump sum (all at once), rather than regular deposits (for example every month).

Note: fixed rate savings accounts can also be called fixed rate bonds.

A regular savings account is a savings account where, you guessed it, you save regularly.

You’re normally required to pay in every month, and in return you might get a higher interest rate for a set period of time (e.g. the first 12 months).

However, they’re not great for long term saving as the rate drops after the bonus period (e.g. 12 months), and there can be a limit on the number of withdrawals you're allowed every year. Often, a modern easy access account can be a better choice.

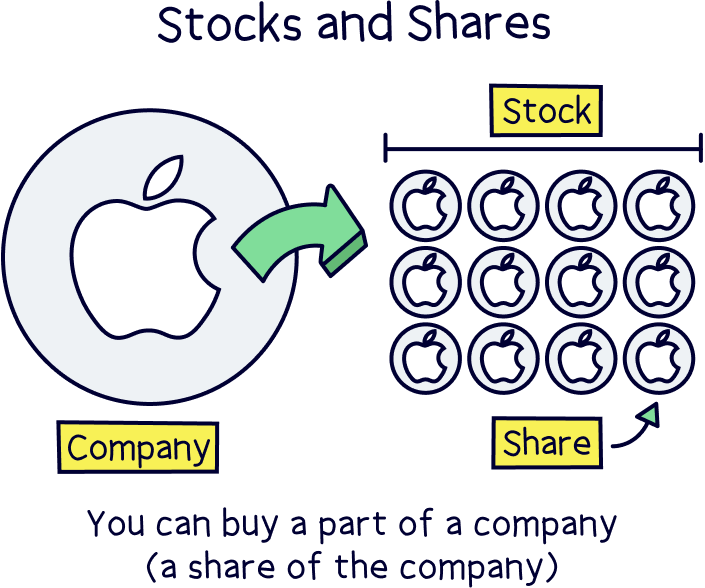

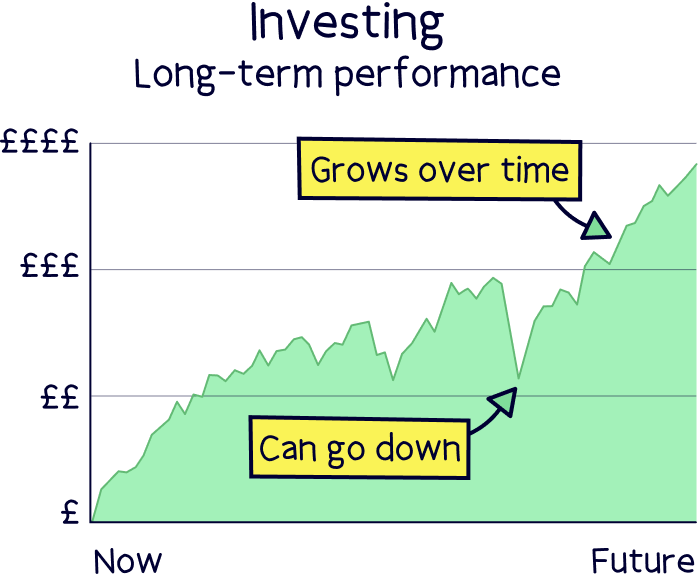

You could opt to invest your money instead. Typically this is one of the best ways to grow your money over time, and you’ll often make more money than simply earning interest with cash.

Investing is where your money is put into things like growing companies, with the view they’ll grow over time to be worth more money. And it can include things like property and bonds (loans to governments and big companies).

When letting the experts handle things, this can be a great option for long term growth – they’ll use sensible, tried and tested investment strategies, that reduce the risk of losing money, and aim to grow your money significantly over time in a safe way.

Note: when investing, your money can go up and down over time, but over time, typically outperforms savings accounts (even the best ones).

This is pretty much exactly the same as how your pension grows over time too.

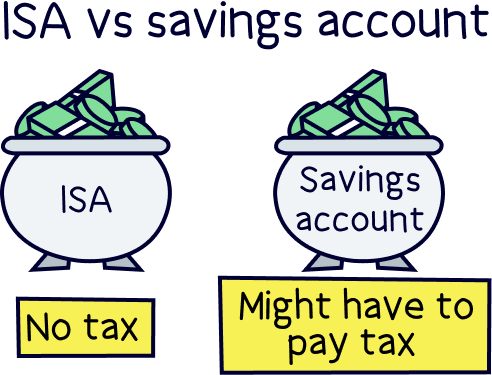

You’ll also be able to save tax-free, within a Stock and Shares ISA – meaning your money can grow even faster over time (as you won’t be paying any tax on your money).

If this sounds interesting to you, check out the best investment platforms – where you’ll find our recommended options for investing with experts.

Yep! Well, we say instantly, normally within a day or less. With an easy access account, you’ll have to withdraw it to your bank account, and this can take a bit of time – it’s all up to the banks. Normally, it’s around 2 hours, but it could be a day, or sometimes even longer.

So, if you do need the money, it’s often best to take the cash out a short while beforehand, just to be sure.

In the UK, we all have a Personal Savings Allowance (PSA). This is how much we can earn each year in interest, before we have to pay tax (on the interest). How much interest you can earn depends on your income (e.g. your salary), and how much Income Tax you pay.

The maximum amount you can earn in interest without paying tax is £1,000 per year – and you’ll get this if you are a basic rate taxpayer (earn less than £50,270 per year). If you earn over £50,270 per year, but under £125,140, you’ll be able to earn £500 per year in interest before paying tax. And, if you earn over £125,140, you’ll have to pay tax on all of your interest.

Here’s a quick summary:

If you earn more interest than your Personal Savings Allowance, you’ll pay Income Tax on the amount above it. The rate you’ll pay is the same as your regular income (e.g. your salary).

So, if you pay 20% Income Tax (earn less than £50,270), and you make £1,500 in interest (and this doesn’t take you over £50,270 per year), you’ll pay 20% interest on anything over £1,000. In this case, you’ll pay 20% tax on £500, which is £100.

Nuts About Money tip: if you’ve got loads of cash in savings and might have to pay tax, (and don’t want to invest your money in the long term, for instance in a managed Stocks and Share ISA), you could consider a Cash ISA. This is where the interest you make is completely tax-free (you can save up to £20,000 per year). The drawback is interest rates on Cash ISAs are typically a bit lower than regular savings accounts.

For low income earners (earning less than £17,570 per year), there’s also something called the starting rate for savings. This is how much you can earn in interest before you need to pay tax on it – meaning you could earn £5,000 in interest per year tax-free.

If you earn less than £12,570 per year, you’ll be able to earn £5,000 in interest before paying tax. If you earn more than £12,570 (but under £17,570), your allowance reduces by every £1 over it.

So, if you earn £13,570, your £5,000 starting rate will reduce by £1,000 (as you are earning £1,000 more than £12,570). This means you can earn £4,000 per year in interest before paying tax. This keeps going until £17,570, which is £5,000 more than £12,270. Make sense?

It’s perfectly safe to use an easy access savings account, and often a great idea.

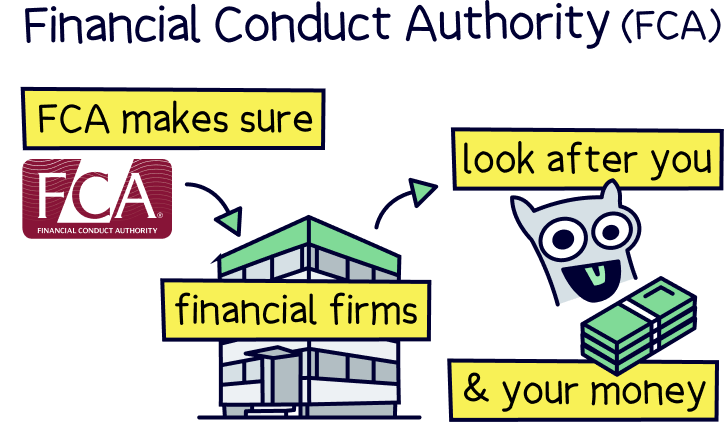

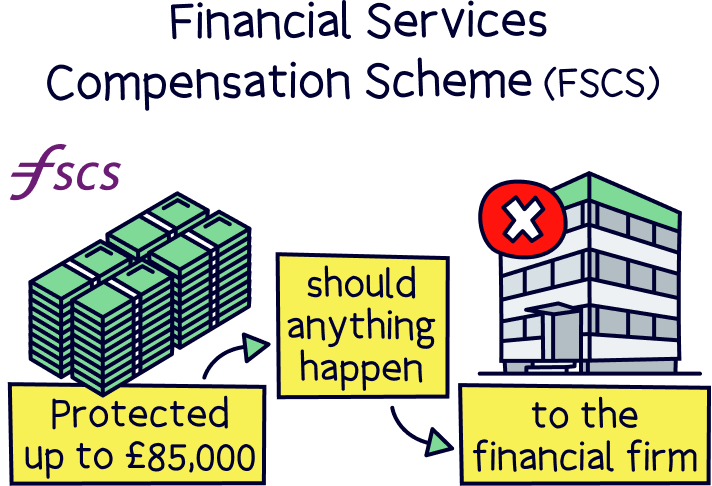

In the UK, all financial services companies have to be authorised by the Financial Conduct Authority (FCA). They’re the people who make sure finance companies (such as banks) are looking after you and your money.

This also means that your money is protected by the Financial Services Compensation Scheme (FSCS). That means your money is protected up to £85,000 should the company your savings account is with go out of business (fail).

If you’re over 50, don’t worry, there’s no need to look for special accounts just for you. You can use any savings account you like – all of our recommended options above can be used by anyone of any age, as long as they’re over 18 (or a children’s savings accounts for under 18s).

It’s very rare to find an account exclusively for over 50s (or 60s), that pays a higher interest rate.

The same goes for over 60s, you don’t need to worry about your age when it comes to opening a savings account – you can still get the best one, just like everyone else!

Let’s run through a recap, and the pros and cons of easy access savings accounts:

There we have it for the best easy access accounts.

Simple really isn’t it? All you need to do is add your money, and you’ll start earning interest. You’ll be able to withdraw your cash whenever you like, and add more money in, whenever you like too.

Easy access accounts are great for getting your cash to work for you (earn interest), but also have the cash there whenever you need it (such as a deposit for a mortgage, or buying a new car).

The interest rates are normally pretty good (with the best savings accounts) – although if you’re saving for the long term, and don’t need access to your money any time soon, you could consider a fixed term savings account (lock your money away typically for a higher interest rate), or invest your money, where experts aim to grow your money sensibly over time using tried and tested strategies. Check out the best investment platforms if this sounds interesting to you.

If you’re ready to get started, we’ve done the hard work and researched the best easy access savings accounts – not only looking at the best interest rate, but how easy it is to set up and use, and the number of withdrawals, among other things.

Click the following link best easy access savings accounts and you'll be taken to the tables above.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things savings, with many years of combined experience writing and talking about savings (and ISAs). Some of our team were top financial advisors. We understand the ins and outs of planning your finances well, how to communicate savings in an easy to understand way (we hope you agree), and of course, how to get the best savings rate for you.

More than 20 years of combined experience researching and writing about savings

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of savings companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Save and invest with Lightyear – get a top savings rate, withdraw money instantly, there’s no minimum deposit and the app is great.