Article contents

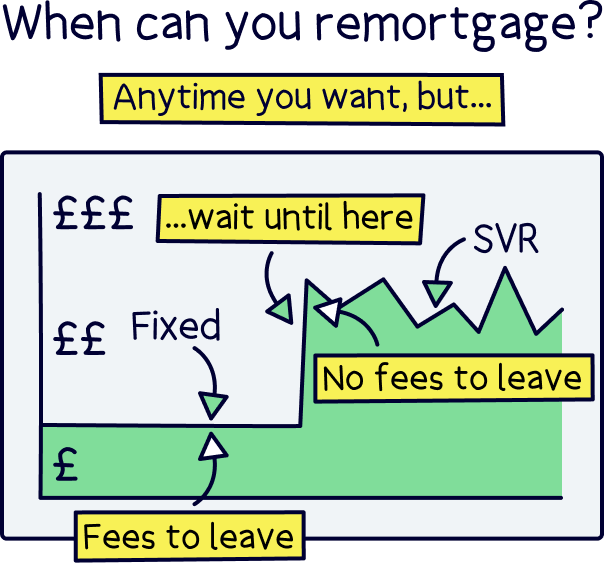

You can technically remortgage whenever you want. However, if you’re on a fixed-rate deal, remortgaging as soon as your fixed-rate period ends will help you avoid hefty price hikes and early repayment charges.

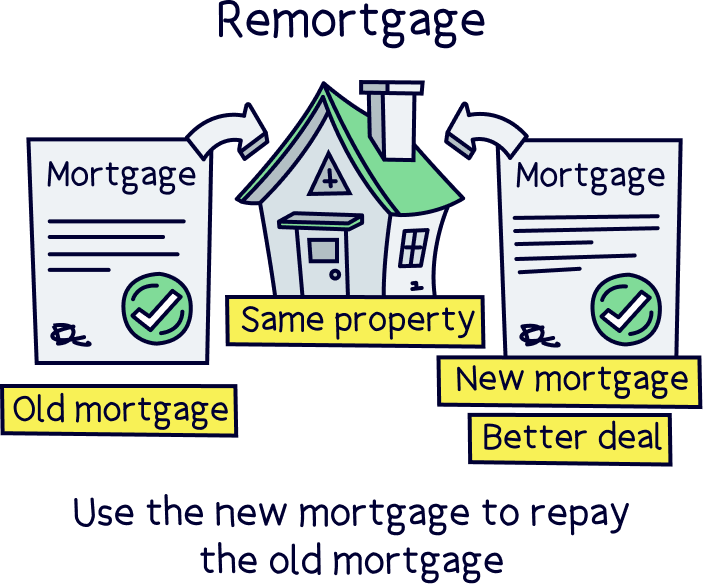

Remortgaging is when you swap your current mortgage deal for a new one. Simple! You’ll often save money (and a lot), or can get some cash out of your home to use however you like.

If you haven’t remortgaged in a while, then chances are you’re paying more than you need to – remortgaging now could save you a ton of money. However, if you remortgaged recently, or you’ve only just taken out your current mortgage, then remortgaging again too soon could land you with hefty fees.

Don’t worry, remortgaging at the right time is a lot easier than you might think. Here, we’ll explain when you can remortgage and, more importantly, when you should.

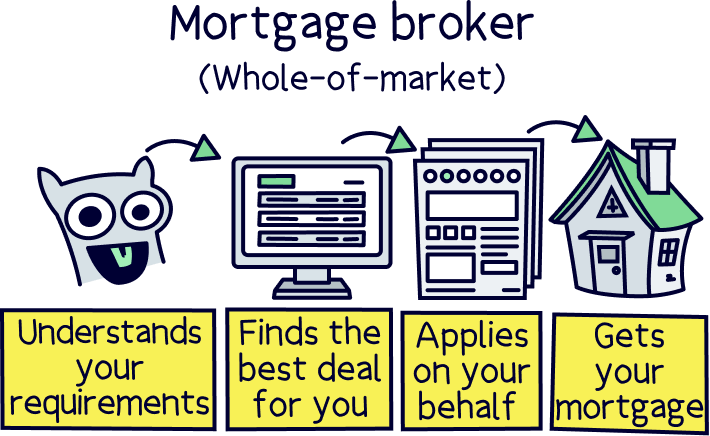

If you’re keen to remortgage – our advice is to speak to a mortgage advisor, they’ll find the best new deal for you and handle all the paperwork too.

Need help finding one of these awesome people? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that? Here's a list of our top mortgage brokers.

Technically, you can remortgage whenever you want. There are no laws stopping you!

However, the best time to remortgage will depend on what kind of mortgage you have. There are two main groups of mortgages:

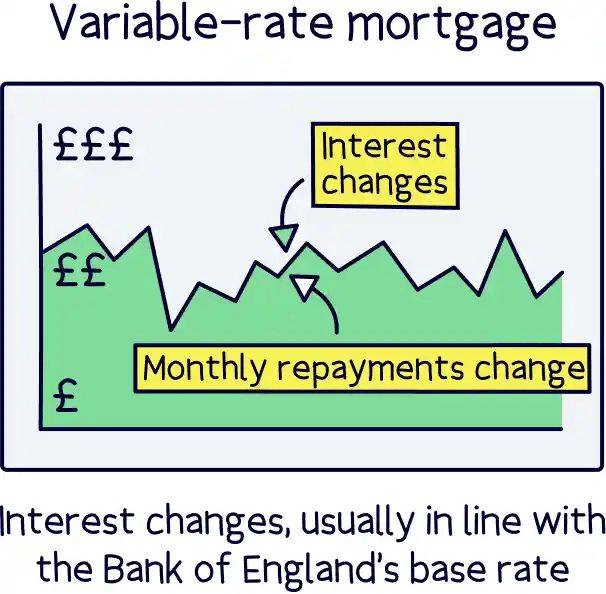

1. Variable-rate mortgages. These are mortgages where the interest you’re charged can go up or down (interest is the fee lenders charge you for the pleasure of borrowing their money). Normally, it will move around roughly in line with the Bank of England’s official borrowing rate (known as the base rate). This means you won’t know how much you’re going to be charged each month.

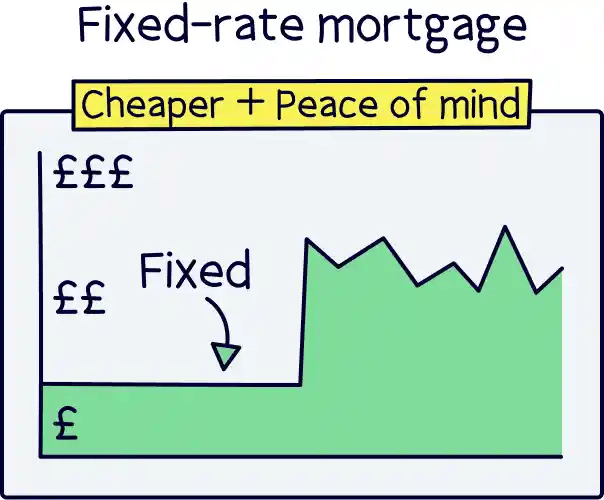

2. Fixed-rate mortgages. These are mortgages where your interest (and therefore your monthly repayments) are set at a fixed price for a certain period of time – often for 2, 3 or 5 years. Think of it a bit like a mobile phone contract where you sign up to a deal and then pay the same amount each month while the deal lasts.

If you’re on a variable-rate mortgage, you can often remortgage at any time without having to pay a penalty fee (although there are a few different kinds of variable-rate mortgages so it’s best to check with your mortgage lender to be sure!).

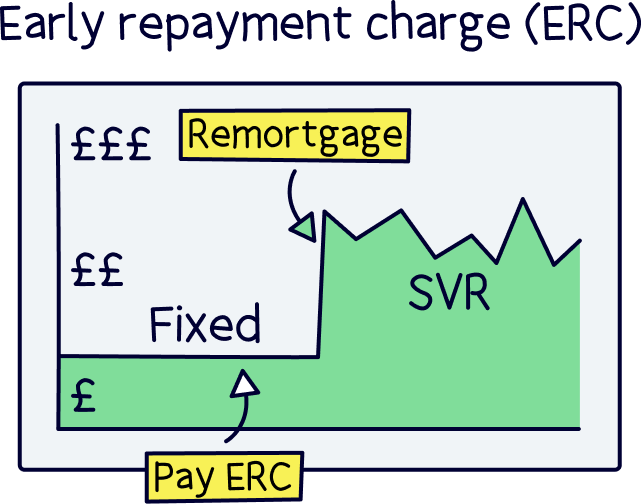

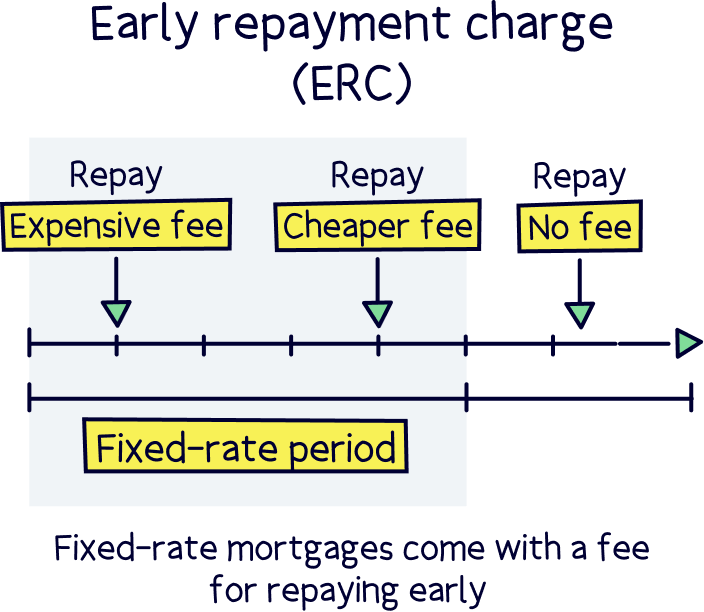

On the other hand, if you signed up for a fixed-rate mortgage (like most people), then you’ll need to time things a bit more carefully. If you want to remortgage early, you’ll normally have to pay an early repayment charge (ERC) which could be thousands of pounds. But if you leave things too long, you’ll be subjected to price hikes which could cause your repayments to go up by hundreds of pounds each month!

Don’t stress, it sounds scary but remortgaging is actually oh-so-easy and it’s not hard to time things right. Let’s take a look at when you should remortgage if you’re on a fixed-rate deal.

Tembo will find your best deal, fast, all with award-winning service.

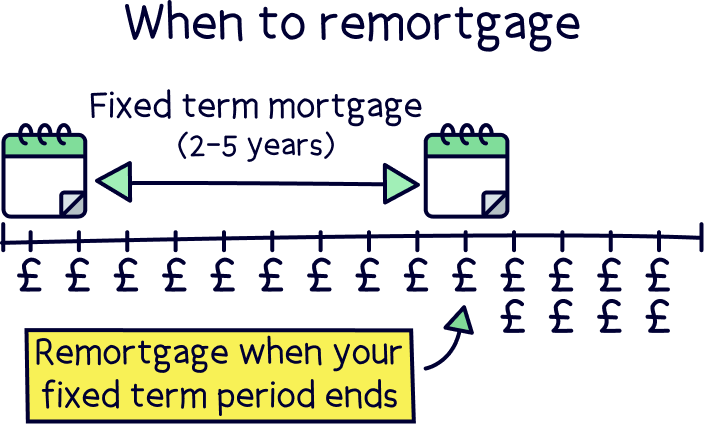

If you’re on a fixed-rate mortgage, the best time to remortgage is immediately after your fixed-rate period ends (that’s the period during which your monthly repayments are fixed at a set cost). And by immediately, we mean the very next day!

To explain why, we’ll need to give you a bit of background about how fixed-rate mortgages work. Here goes!

When you get a fixed-rate mortgage deal, your interest rate will be set at a fixed cost for a certain period of time. This is sometimes called the incentive period because normally, your lender will give you a discounted rate to try and persuade you to choose them. Hooray!

However, as part of the deal, your lender will try to tie you in. In other words, in exchange for lower rates, you have to agree to stay with the lender for the duration of your fixed-rate period. If you don’t, you’ll have to pay that pesky fee (ERC) we told you about. Sounds pretty fair, right?

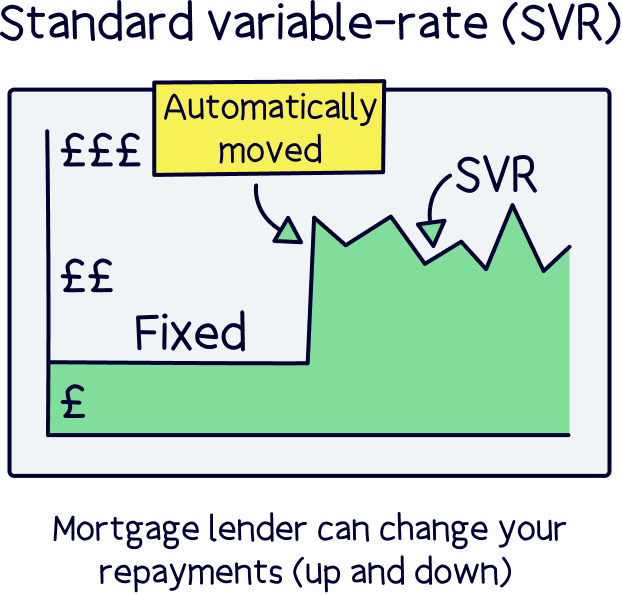

There’s just one catch. As soon as your fixed-rate period ends, your lender will automatically move you onto something called their standard variable rate (SVR). This is one of those variable-rate mortgages we told you about earlier, but it’s the worst kind. Honestly, it totally sucks.

Why? Well, firstly, your monthly repayments will suddenly shoot up. That’s right, your lender’s SVR is likely to be a lot more expensive than what you’re currently paying.

And secondly, your lender can put your rate up (or down) whenever they want. Normally, it will move around roughly in line with the Bank of England’s base rate (except that the rate you pay will be higher). But technically, your lender could change it whenever they fancy. So cheeky!

Your lender is basically hoping that you either don’t notice your rate has gone up, or that you can’t be bothered to remortgage. And it works! According to Experian, around 46% of mortgage holders are on their lender’s SVR (and therefore paying much more than they needed to!).

Don’t worry though. By remortgaging, you can avoid these price hikes and get a lovely fixed-rate mortgage deal all over again and save lots of money.

If you haven’t remortgaged in a while, you’ll want to remortgage as soon as you can so that you don’t stay on your lender’s SVR for even a minute longer than you need to!

But if you’re still in your fixed-rate period, you’ll want to time things so your new mortgage starts when your fixed-rate period ends. That way, you don’t have to pay your lender’s early repayment charge and you don’t have to fall onto your lender’s SVR either – perfect! Don’t worry, it’s really easy to arrange.

You know how we said you should avoid remortgaging until after your fixed-rate period ends? Well, that doesn’t mean you should sit on your bum and do nothing until the very last moment!

Instead, we’d recommend you start looking for a new deal around 6 months before the end of your fixed-rate period.

If you’re wondering why you should bother getting organised so early, it’s mainly because you’ll want to take your time finding the best deal for you. Yes, it can be tempting to just remortgage with the same lender you’re already with. But there are over 100 mortgage lenders in the UK, so the chances are you’ll be able to find a much cheaper mortgage deal by switching, and save even more money.

To make sure you’re getting the best deal, it’s a good idea to get some help from a whole-of-market mortgage broker (also known as a mortgage advisor). They’re experts in mortgages and will be able to compare all the different deals and lenders for you before helping you to choose the best one.

Note: they’re even online these days too. Here’s our best online mortgage brokers.

Plus, they’ll be able to save you a ton of time by sorting out the whole remortgage for you. It’s a win-win!

Not sure where to find a good mortgage advisor? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money.

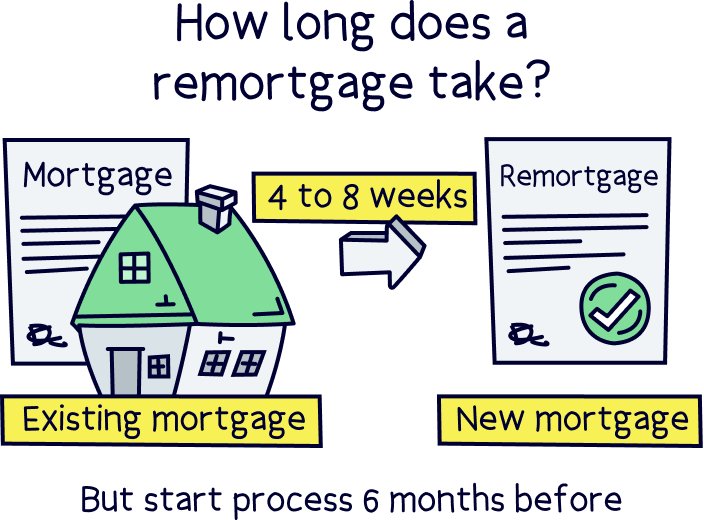

The other reason to start your remortgage early is that it could take a while to go through. The remortgage process with most mortgage lenders takes between 4 and 8 weeks to complete from the date of applying, but everyone is different and it’s impossible to say exactly how long your remortgage will take.

Your lender will need to do similar checks to what they would if you were applying for a mortgage deal on a new house after all (don’t worry though, this is a lot less stressful as you’ve already passed the checks once so there’s no reason you won’t pass again. Plus even if a lender won’t give you a new deal, you won’t lose your current mortgage or anything like that!)

Ultimately, it’s better to be safe than sorry so we’d recommend applying for your new mortgage at least a few months before your fixed-rate period ends. Some mortgage lenders will even let you apply for your remortgage up to 6 months before you want your new mortgage deal to start, so if you want to be super organised then you can.

Don’t worry, your mortgage broker will sort out the remortgage application for you and will make sure your new deal starts right after your fixed-rate period ends. In the meantime, you can just sit back, relax and enjoy those lower monthly repayments when the time comes.

Yes! We wouldn’t usually recommend remortgaging before your fixed-rate mortgage ends as, let’s face it, you probably don’t want to be hit with an early repayment charge (ERC) worth potentially thousands of pounds. But every now and again, there might be a time where it’s worth paying that annoying charge and remortgaging straight away. Here are a couple:

Remember how we said that you can usually get a cheaper deal by switching lenders? Well, sometimes, you can get a much cheaper deal. And we mean much!

If that’s the case, it might be that you can save more money by switching now rather than staying on your current deal until the end of your fixed-rate period – even though you’ll have to pay that pesky fee (ERC).

This is more likely to happen if you’re nearing the end of your fixed-rate mortgage. Basically, your early repayment charge (ERC) will normally be the same percentage as the number of years left on your fixed-rate period. In other words, if you have 2 years left, you’ll often face fees of around 2% of the amount you still have left on your mortgage. But if you have just 1 year left, you’ll usually only have to pay around 1% to leave early.

Don’t get us wrong, even 1% could mean you have to pay thousands of pounds! So usually you’re best off waiting until the end of your fixed-rate period. However, never say never – if you’ve found a way cheaper deal elsewhere, it might just be worth leaving straight away. It’s worth doing the maths anyway (don’t worry, a mortgage broker can do the sums for you!).

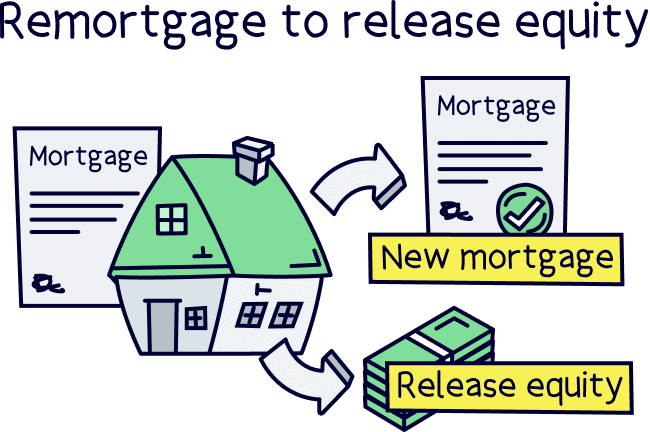

Some people don’t choose to remortgage to access cheaper rates. Instead, they might remortgage to borrow more money. This is called remortgaging to release equity in your home, and it basically involves getting a new, bigger mortgage so that you can get the difference back in cash.

You can use this cash for all sorts of things – you could remortgage to build an extension or for home improvement, or to put your kids through uni, to buy a car, to pay off debts (also called a debt consolidation mortgage). The list goes on!

In an ideal world, if you wanted to remortgage to release equity, you’d wait until the end of your fixed-rate period to avoid having to pay the early repayment charge (ERC). But you might still choose to remortgage sooner and just bite the bullet. It all depends on how badly you need that cash.

Is your fixed-rate mortgage coming to an end? Then now’s the time to start thinking about remortgaging to avoid your lender’s sneaky price hikes, and get a much cheaper rate! The potential savings are huge.

And don’t worry, it’s so much easier than you might think. (In fact you can look at switching deals up to six months before your current deal ends.)

The first step is to find a good mortgage advisor who can compare all the mortgage deals out there and lenders available and help you choose which one to switch to.

If you’re not sure where to find an advisor, check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. Get 50% off their fee with Nuts About Money too.

Then, all you have to do is put your feet up and let them do all the hard work for you! Oh, and enjoy paying those lower monthly bills when the time comes of course!

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.