Article contents

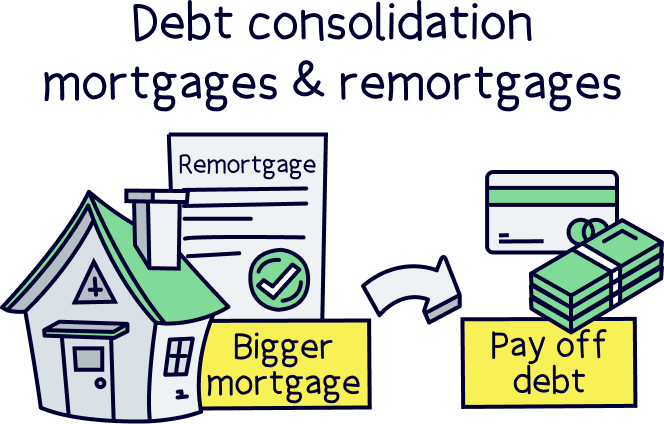

A debt consolidation mortgage is when you take out a new, bigger mortgage on your property to free up equity (cash). Then, you use the cash to pay off other debts.

Are you struggling to pay your debts like so many other people right now? Keeping on top of them can be hard, especially if you have debt in lots of different places.

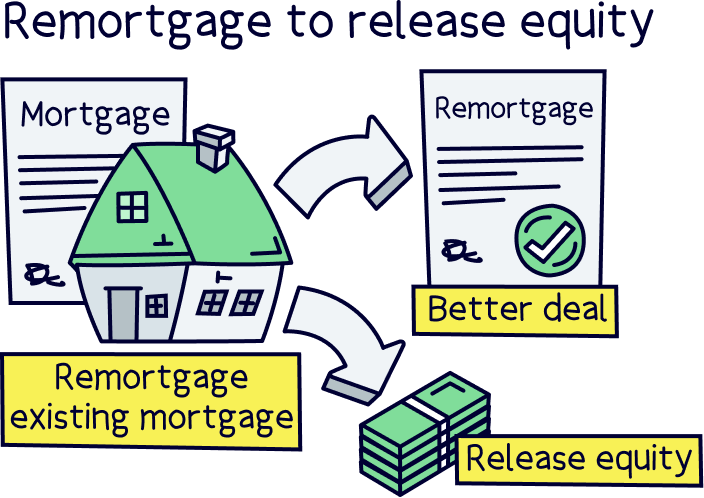

Switching mortgage deals (called remortgaging) could help you pay off your debts by taking out a new, bigger mortgage on your home and getting the difference back in cash.

Here, we’ll look at how it all works and whether it’s right for you.

A debt consolidation mortgage is when you remortgage your property to release equity (cash) and then use the cash to settle your debts.

If you’re thinking ‘Huh? How does that work?’ then don’t worry. Let’s explain.

First things first, equity refers to how much of your property you own outright. In other words, it’s the amount of your home’s value that would go straight into your pocket if you sold it, rather than going towards paying off your mortgage lender (mortgage lenders are the people that give out mortgages).

When you remortgage to release equity, you’re swapping your current mortgage for a new, bigger one. This means your new mortgage will cover more of your home’s value and you’ll get the difference back in cash (that’s the bit we call ‘releasing equity’).

You can use the equity you release for all sorts of things – to build an extension, to pay for a fancy holiday, to buy a new car… the list goes on.

Remortgaging for debt consolidation is exactly the same. It just means you’re using the equity you’ve released to pay off other debts, like loans, credit cards or overdrafts. It’s called ‘debt consolidation’ because you’re ‘consolidating’ all your debts in one place – basically taking out one big loan (your new mortgage) in order to pay off lots of smaller ones.

Tembo will find your best deal, fast, all with award-winning service.

Okay, so we bet you’re wondering why you’d bother taking out what’s essentially a new loan to pay off your existing loans. How exactly is it meant to help?!

Well, the main reason is that interest rates on mortgages tend to be really low compared to interest rates on other loans (interest is the fee a lender will charge you for the pleasure of borrowing their money).

Let’s take a look at an example. An arranged overdraft is a kind of loan where you can keep spending once your bank account hits zero. The interest rates on overdrafts tend to be between 19% and 40% APR, which means you’ll be charged between 19% and 40% of the amount you borrow over a year.

On the other hand, as of April 2021, the average interest rate on UK mortgages was between just 1.52% and 2.58% (Statista), depending on the type of mortgage. So a LOT lower. That means you’ll get charged much less interest each month, which will make your monthly repayments lower and easier to keep on top of.

Just watch out because even though mortgages usually come with lower monthly repayments, they tend to last much longer than your average loan. You could be paying your mortgage off over 25 or even 35 years. This means that even though you’ll be paying less interest each month, you’ll normally end up paying more interest over the whole duration of your mortgage (known as your mortgage term).

Let’s say you have a personal loan of £10,000, borrowed over 5 years at an interest rate of 10%. Your monthly repayments would be £210.36, and the total repayment would be £12,621.35, with £2,621.35 in interest.

If you borrowed an extra £10,000 on your mortgage, say over 25 years at an interest rate of 3%, your monthly repayments would be just £47.21 extra on your mortgage, but you would end up repaying £14,163.26, with £4,163.26 in interest. Quite a bit more than the personal loan!

So, is it a good idea to remortgage for debt consolidation? Well, everyone’s different and ultimately, it’ll probably depend on how well you’re currently handling your debts.

If you’re easily keeping up with the repayments and you’re on track to pay your debts off within the next couple of years, it might not be worth remortgaging for debt consolidation. The same goes if your existing loans have low interest rates, for example, if you’re in the interest-free period of a credit card.

However, if you’re struggling to keep on top of things as they are, a debt consolidation mortgage could make things easier to manage and could help get you out of a sticky situation. Here are the main pros and cons.

Whatever you’re thinking, just be aware that a debt consolidation mortgage isn’t your only option. You could also look at taking out a different kind of loan for debt consolidation. This would work in a similar way to a debt consolidation mortgage, but you might not need to put your house on the line. Check out our guide to loans, overdrafts and credit cards to learn more.

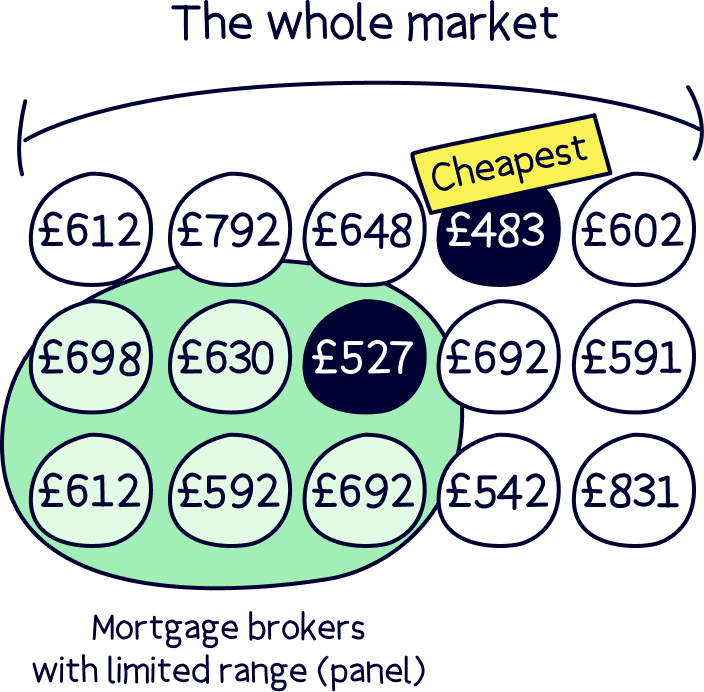

It can be tempting to simply ask your current mortgage lender if they’d consider giving you a bigger mortgage for debt consolidation. However, we’d recommend comparing all the different mortgages and lenders available to you before committing to a new deal. That way, you can be sure you’re getting the best rates.

To do this, it’s best to get a whole-of-market mortgage broker (also known as a mortgage advisor) involved. They’ll be able to compare all the different lenders and mortgages and advise you on which ones would be best for you, based on your own personal circumstances.

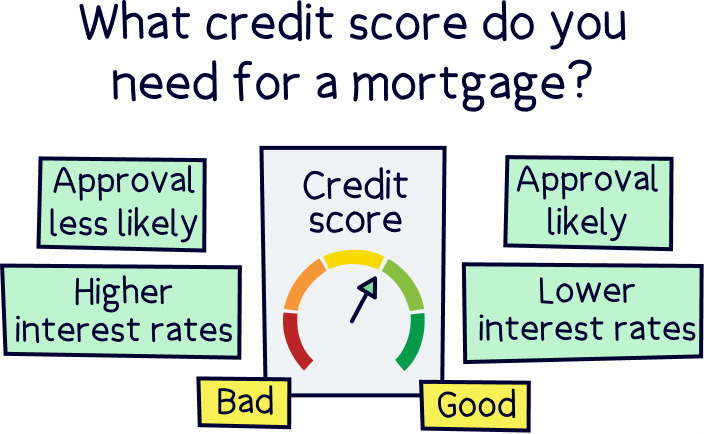

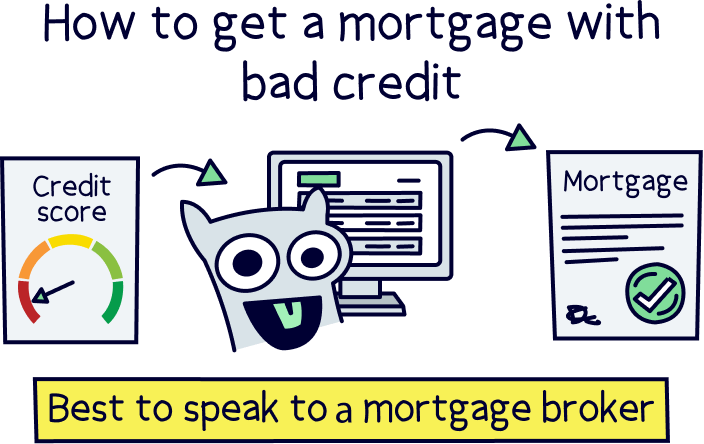

If you’ve managed to pay all your debts on time up till now, you might well have a great credit score as you’ll have a proven track record at paying loans back on time. However, if you’ve missed repayments in the past, your credit score will probably have taken a hit, which could make it hard to get approved for the mortgage.

This can lead to a bit of a vicious circle where you need the mortgage to settle your debts, but you need to settle your debts to get approved for the mortgage. We know, it’s pretty frustrating.

However, if you have a bad credit score, don’t worry. Getting a debt consolidation mortgage is still doable. A mortgage broker will have experience of which lenders are most likely to lend to people with bad credit scores, helping you to find the right lender and stopping you from applying to any lenders who are likely to reject you (if your application gets rejected, this will only make your credit score worse).

In fact, there are even mortgage brokers out there who specialise in helping people to get mortgages with bad credit scores, so you’ll definitely be in safe hands! If you need a little help finding a mortgage broker, use our free find a broker tool to find the right one for you.

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

There are three main kinds of debt consolidation mortgage. They all work in a similar way by helping you borrow more so that you can release equity and settle your debts. But the nitty-gritty details are slightly different. Don’t worry, your mortgage broker will be able to help point you towards the one that’s most suitable for your needs!

Remortgaging for debt consolidation is where you switch over to a whole new mortgage with either the same lender you’re already with or, more often, with a new lender altogether. In other words, you’re ditching your current mortgage for a new, bigger one.

This is a popular way of releasing equity but be careful you don’t throw away a great mortgage with great rates in favour of a less good deal, just so that you can borrow more. Mortgages are a long-term commitment, so you’ll need to make sure you’re getting a deal that’s going to work for you in the long run.

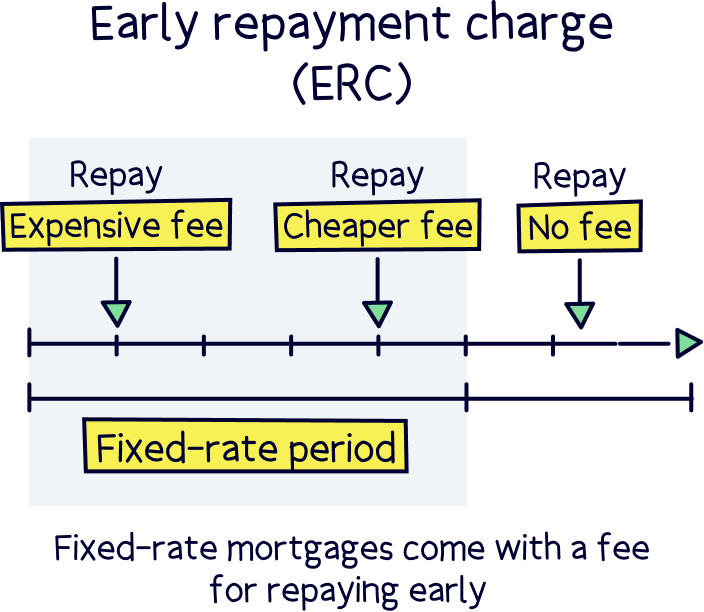

The other thing to watch out for is early repayment charges. Basically, if you’re on a fixed-rate mortgage (which is where your monthly repayments are set at a fixed cost), you might have to pay a fee if you’re leaving your contract early. This could be thousands of pounds so ideally, you’ll want to wait until your fixed-rate period ends to avoid the fee.

Ultimately, taking out a bigger mortgage is always a big step and it’s going to be even more so if you’re already in trouble financially. So, you’ll want to be absolutely certain it’s worth doing. This is something your mortgage broker can help with, so make sure you pick their brains to get some advice.

A further advance is when your existing mortgage lender agrees to lend you more money for debt consolidation on top of what they’re already lending you. In other words, it means you won’t have to get a whole new mortgage to borrow more. You can just add the extra bit of borrowing on top of your current agreement.

It all sounds very easy but bear in mind you will still have some hoops to jump through.

Firstly, your lender will still want to carry out some thorough checks on you. After all, they’re not going to want to lend you more if they don’t think you’re going to be able to pay it back.

Secondly, you’re not necessarily going to be able to access the same deal for the new borrowing as you have for the rest of your mortgage. The extra bit of borrowing could come with higher interest rates and you’ll normally be charged fees for it to go through too.

That’s why we’d always recommend speaking with a whole-of-market mortgage broker, even if you think you want to stick with the same lender. They’ll be able to compare all the mortgage deals out there and let you know what’s cheapest. It might be sticking with your current lender, but it might mean remortgaging instead.

A second charge mortgage is where you use the equity you’ve built up in your home to take out a second mortgage. Yep, that’s right, you’ll end up with two mortgages on the same property!

You can then use the equity released by your new mortgage to pay off your debts.

Just be careful because, just like with your first mortgage, if you don’t pay the second one, your lender could seize your home and sell it to get their money back (don’t panic though, it is a last resort!). Oh, and you’ll end up having to pay two mortgages at the same time, which means two lots of payments to keep up with. However, if you’re taking out a second mortgage for debt consolidation, that’ll probably still be fewer payments to worry about than what you have now.

If you’re wondering ‘How much cash could I release with a debt consolidation mortgage?’ then it all depends on your personal situation. Lenders will look at things like your income and expenses to see how much extra borrowing they think you’ll be able to comfortably pay back.

However, one of the biggest things to factor in is how much equity you own in your property. After all, you can’t release equity you don’t have!

To work out how much equity you own, follow these 3 simple steps.

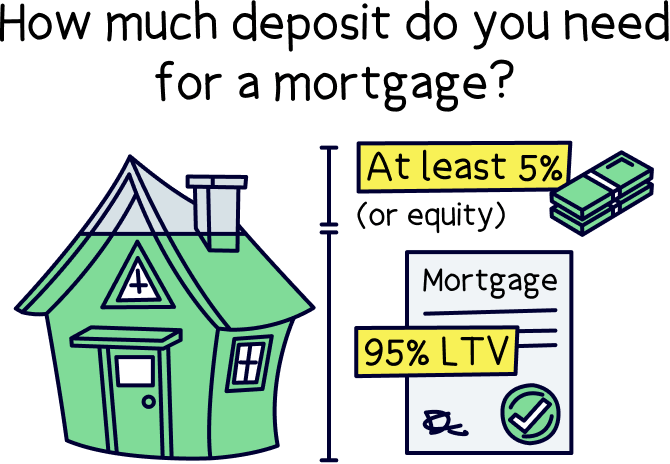

Now you know how much equity you have. That said, you won’t be able to release all your equity when you remortgage.

Most lenders currently will only give you a mortgage for a maximum of 95% of your property’s value, known as a 95% loan-to-value ratio (LTV). That means you’ll need to make sure that you keep at least 5% of your property’s value in equity.

In other words, you’ll need to build up a decent amount of equity before you can release some and pay off your debts.

Not only that, but the higher the LTV (so the higher the percentage of your property’s value you’re covering with a mortgage), the worse the rates you’ll be able to access. And the more equity you release, the bigger your monthly repayments will be and the bigger the risk of falling into negative equity (where you owe your lender more than your property is worth!).

So, even if you can release a ton of equity, that doesn’t mean it’s the right thing to do!

We’d always recommend talking to a mortgage broker about your situation to get some tailored advice about how much equity you can (and should!) release. We’re all different so the chances are it will be about finding that perfect balance between how much equity you own, how much your mortgage lender is happy to let you borrow and how much debt you’re in. Simple!

There are over 100 different mortgage lenders in the UK, and many of them offer debt consolidation mortgages. A few of the best-known include Barclays, HSBC, Nationwide and Natwest.

They all have different criteria, so it’s impossible to say for sure that one is better than another. After all, the best for you might not be the best for someone else. That said, if you’ve had trouble with money in the past, the best debt consolidation mortgage provider for you will probably be one that caters for people who have bad credit (although typically, mortgages for people with bad credit come with higher rates).

Here are just a few mortgage lenders that are particularly flexible when it comes to lending to people who’ve been in trouble financially.

If you think a debt consolidation mortgage could help you get your debts under control, the first step is to find a mortgage broker.

They’ll take the time to truly get to know your circumstances and will be able to advise you on whether a debt consolidation mortgage is definitely the best option for you. If it is, they’ll be able to save you a ton of time and money by finding you the best deal and sorting out your whole application for you.

Hopefully, this has helped you to understand whether a debt consolidation mortgage could help you, and you’ll be on track to pay off those debts before you know it.

To recap, if you need to find a decent mortgage broker. check out Tembo¹, they've got award-winning service, and will find you the best mortgage. You'll also get 50% off their fee with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.