Article contents

Depending on which credit reference agency you are using, you typically need a score of 721 with Experian, 380 with Equifax and 566 with TransUnion.

Here's all you need to know about credit scores and what credit score you need to buy a house with a mortgage in the UK.

Your credit score is very important to a lender, (that’s a bank or building society for a mortgage.) Your score determines how reliable you are, and if it’s sensible for them to lend you money or not.

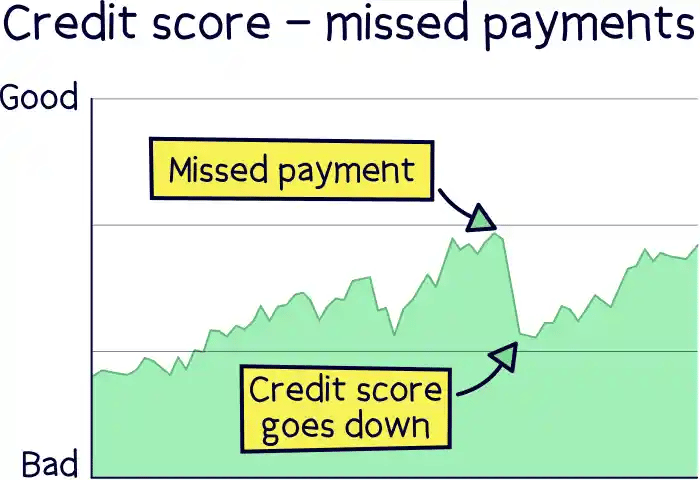

You can’t hide anything from a credit score, it’s like a footprint of your financial history, anything and everything you have done money wise is included. Whether that’s opening or closing bank accounts, applying for mobile phone contracts, loans, credit cards, mortgages or any other type of borrowing, not just if you were accepted or not, and how much borrowing you currently have. Plus if you’ve ever missed a payment.

It also shows where you live and all your address history, and whether you are registered to vote or not (electoral roll).

It’s very in-depth, and for a reason, to help lenders make sensible decisions with their money.

Tembo will find your best deal, fast, all with award-winning service.

If you've made some mistakes with you money before, such as regularly missing payments, or if you’ve never borrowed any money before from a lender, (not your family), your credit score will show this.

No history is not necessarily a good thing. If there’s no history for credit reference agencies to use, then they don’t have the information to give you a good score.

So you may have to play the game a bit sometimes if your score is low, we’ll come back on how to do this at the end of this post.

They’re the guys who gather all your information together and then give you the actual score. There’s three different agencies all with slightly different scoring methods: Experian, Equifax and TransUnion (formerly known as Callcredit).

Although all the credit reference agencies use effectively the same information to produce your credit score, the scores themselves are slightly different. You don’t need to worry about which one your lender will use as you will normally find yourself in the same range across all three.

The official ranges are:

Experian: 0-999: Experian has the highest score range, all the way up to 999. A score of 721-880 is considered fair, and a score of 881-960 is considered good. Above this is excellent.

Equifax: 0-700: Equifax only goes up to 700, with 380-419 considered fair and 420-465 considered good. And above is excellent.

TransUnion: 0-710: TransUnion use a range up to 710, with 566-603 considered fair and 604-627 considered good. And above excellent.

These are just a few of the main ones to give you an idea of what credit reference agencies collect. But it’s pretty much everything to do with your finances and borrowing.

How long you have lived at your current address (and previous addresses): this shows stability in your life, which is more reassuring for a lender.

If you are you on the electoral roll (registered to vote): this proves your name and address to the lender, and they can easily identify you.

Your borrowings (called credit agreements): shows the amount you are borrowing, and the lender, plus all of the repayments. If you’ve missed any repayments, it’s not good.

Your credit utilisation: this means how much you are actually using of the available credit you can use, such as the limit on your credit card. For instance if you are using half of your credit limit, say £500 of £1,000. Then your credit utilisation would be 50%.

The number of credit applications: that's how many times you have applied for credit (e.g. a loan), and the frequency. If you’ve done lots within a short space of time, you may appear like you can’t manage your finances well.

Tip: Look out for errors on your report – There may be errors on your report, such as the wrong address or incorrect borrowing figures or missing payments, these are easily fixable and will increase your score quickly.

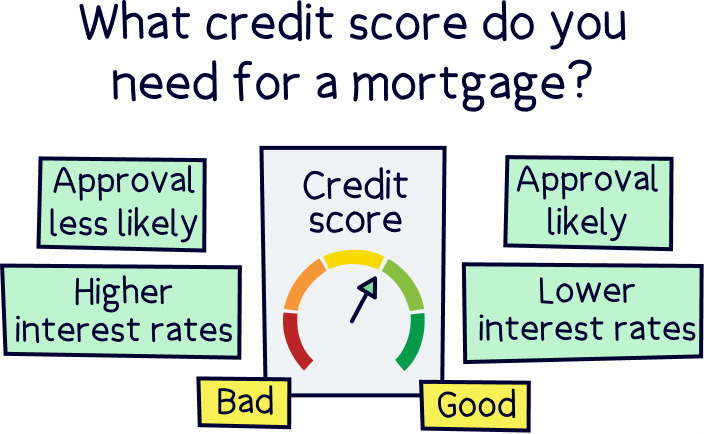

There’s no specific score you need. Luckily! But generally a higher score shows you are more responsible with borrowing money and therefore less risk to a lender. Which means 2 things:

1. You have a higher chance of actually get the mortgage.

2. You might get better interest rates, or at least you won’t be stuck with high interest rates on deals designed for those with bad credit.

If you are in the fair range, you are probably fine. No guarantees though. There’s still a lot of work to do on your credit score. So that’s a score of 721 with Experian, 380 with Equifax and 566 with TransUnion.

Why is there no specific score? Because lenders don’t just use your credit score by itself. It’s just one part of the underwriting process (that’s a lender determining if they will lend to you), they are mainly concerned with if you are able to afford the mortgage repayments and how reliable your income is. So if you’re in a full time job, with a stable income, and don’t expect big life changes soon, you’ll look good to a lender.

Learn more about getting a mortgage with a part-time job.

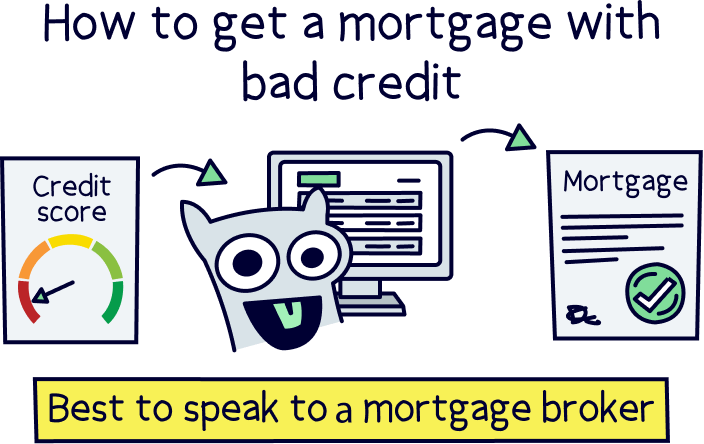

If your score is bad, that’s a rating of ‘poor’ or ‘very poor’, you might still be able to get a mortgage but not with traditional lenders. Specialist lenders will ignore your credit report and lend based on their review of your finances instead. But because of the higher risk to them, the interest rates you’ll get are pretty high. It might be worth seeing if you can improve your credit score first.

Also, if you've ever heard of the credit blacklist, it’s just a myth! You can always improve your score over time.

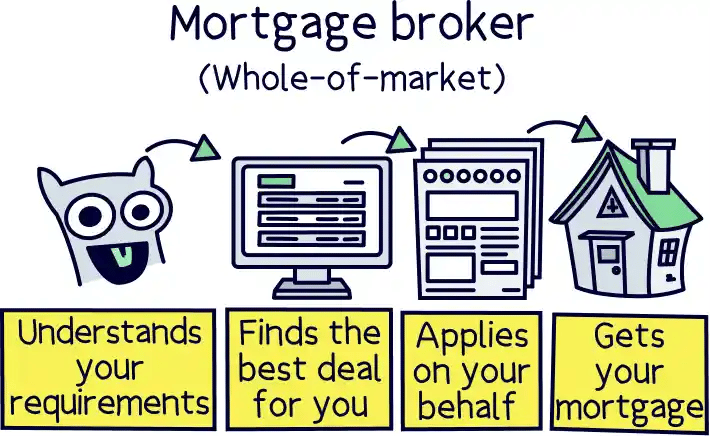

If you’re ready to get a mortgage, and happy with your credit score, we recommend using a mortgage broker to help you get a mortgage. They’ll be able to find you the best mortgage for you and do all the work for you, normally for free too.

Not sure where to find a good mortgage broker? check out Tembo¹, they've got award-winning service, and guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.