Article contents

Yep! Don't worry, you definitely can. If you can afford the mortgage repayments, and prove your income, there's nothing to worry about.

Do you work on a fixed-term contract? Can you regularly be found tearing your hair out and weeping over your finances, wishing you could get a mortgage? Well, we’re here to make your day: you can!

If you’re like most people working on a fixed-term contract, chances are you’ve been going nuts thinking you’ll never be able to get a mortgage. But guess what? Fixed-term contractors get mortgages every day!

Here’s all you need to know.

Tembo will find your best deal, fast, all with award-winning service.

Okay, so we know we said that lots of fixed-term contractors get mortgages. And it’s true! But just to be on the safe side, let’s make sure we’re both on the same page…

When we talk about someone working on a fixed-term contract, we’re talking about two main groups of people:

If you’re an employed fixed-term contractor, your employer takes off PAYE tax and National Insurance from your payslip, just like they would for someone on a permanent contract. The only real difference is that your job will last for a fixed amount of time.

There are lots of different reasons you might be employed on a fixed-term contract like this – maybe you’re covering for someone who’s on maternity leave, or maybe your employer just needs an extra pair of hands for a few months. Either way, it usually means you won’t be sticking around forever.

If you’re a self-employed fixed-term contractor, you work for yourself. So, you’ll (usually) invoice the company you’re contracting for and receive the full amount. Normally, you’ll be registered as self-employed or you’ll be the director of your own limited company.

Depending on your situation (things like how long you’ve been contracting for and whether you run a limited company with someone else), you might be able to be treated as ‘employed’ instead of ‘self-employed’. But this is all a little complicated so we’d recommend chatting to a mortgage broker to get some advice on your specific circumstances. More on that later!

Let’s imagine your friend comes up to you one day and wants to borrow some money. Would you say yes? Let’s face it, if you’re a good friend, you probably would. But you’d probably also want to know whether they’d be able to repay you. Are we right?

Getting a mortgage is pretty much like that. When you apply for one, you’re basically asking a mortgage lender ‘can I borrow some money?’. Before they say ‘yes’ or ‘no,’ they’ll want to work out how likely you are to be able to pay it back.

Because you’re not on a permanent contract, they might see you as a little bit risky. Don’t worry, that’s not a judgment on you! It just means they might worry about where your next job is going to come from once your contract runs out – and ultimately, whether you’re going to be able to afford your mortgage repayments long-term.

Have you consistently earned a living through fixed-term contracts? Go you! This will help to show mortgage lenders that you’re going to be able to keep up your repayments. Many will want to see that you’ve been contracting for at least 12 months.

If you’ve only just started working as a contractor, don’t worry. Some lenders will still consider you if you’ve been working in the same industry consistently for at least a couple of years.

Hopefully, you don’t have any major gaps in employment. Some mortgage lenders won’t lend to anyone who’s had an employment break in the last 12 months. But if you have had some gaps, don’t stress out about it too much. Some lenders are more flexible and anyway, they don’t all agree on what counts as a gap (one might count just a single week, while another might accept a break of four weeks between contracts). So, it’s all about finding the right lender for you.

How many months do you have left on your current contract? If your answer is six months or more, then crack out the champagne – this is what most mortgage lenders will be looking for. That way, they know that you have some stability in the near future.

Having said that, every lender is different. Some will be happy to lend to you if you have just three months left on your contract, while others will set 12 months as the minimum requirement.

Even if you’re nearing the end of your contract, all is not lost. Think about how you could show you have some consistent work lined up. Maybe you could get a letter showing that your contract is going to be renewed. Or maybe you could provide proof that you have another contract lined up for afterwards. Every lender is different so there’s always hope!

Do you work in tech, finance, consulting or design? Lucky you. Working in a highly-skilled role means you’re going to find it easier to get a mortgage than people who work in lower-skilled environments like warehouses or call centres (sorry!).

This might seem really unfair, but professional occupations are statistically more stable than low or unskilled jobs. Don’t forget, mortgage lenders are obsessed with risk!

In the same way, in-demand roles that can work year-round (like teachers and doctors) will often find it easier to get a mortgage, even if they’re on a zero-hours contract. It makes sense really – they’re less likely to be out of work than seasonal workers who are employed on a short-term basis.

Just remember that a mortgage lender will take all aspects into account when deciding whether or not to lend to you. If you work in a lower-skilled role but you’ve had consistent work for many years, you’re still going to be more appealing than a teacher who’s had big gaps in employment.

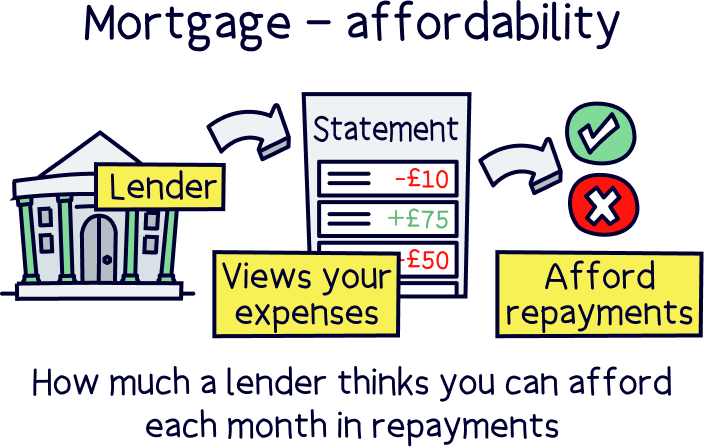

Quick, call off next week’s shopping spree! Affordability is all about how much ‘spare cash’ you have after paying your bills and other outgoings. So, it’s best to curb your spending now to make sure your finances are in good shape.

Think about it: it doesn’t matter how much you earn if you don’t have any left over to pay your mortgage with!

Your mortgage lender will want to see your earnings and outgoings to work out whether you have enough disposable income to afford mortgage repayments. We hate to break it to you, but that might mean airing your dirty laundry and sharing your bank statements. Gulp!

Most mortgage lenders who offer mortgages to contractors will want to work out your average salary based on how much you’ve earned over the last few years (assuming you’ve worked as a fixed-term contractor for that long). But if your income varies a lot, some will take the lowest figure while some will be happy to go on the most recent figures, especially if you’re growing steadily.

Some lenders will even be willing to calculate your income by taking your day rate and multiplying it by the number of days you usually work each week. They’ll then use this figure to work out how much you can be expected to earn each year (before you get your hopes up, be aware that they’ll usually take off six to 10 weeks’ potential earnings to account for any holidays and gaps between contracts. Nice try!). This can be a total lifeline if you’ve only just started contracting.

When’s the last time you settled your water bill? Have you paid off those credit cards?

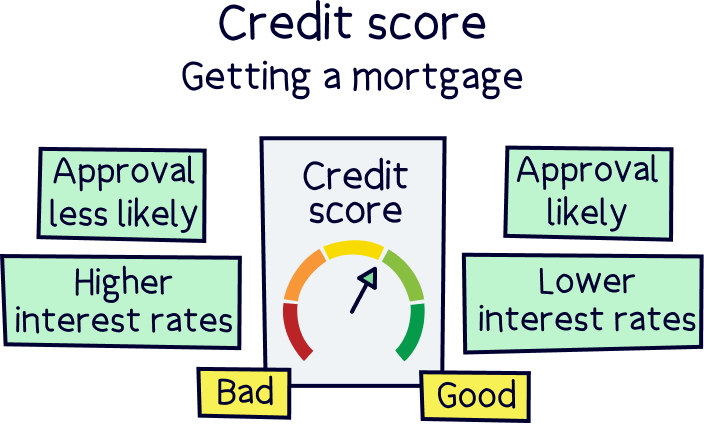

Most lenders will use your credit score to estimate how likely you are to repay their loan. Your credit score is a number that reflects your credit history – in other words, it shows lenders whether or not you’ve repaid debts in the past.

Most lenders won’t offer you a mortgage if you don’t have a good credit history. So, try to get yours looking as awesome as possible before you apply.

Yep, that means paying down the balance of any credit cards and getting yourself up-to-date with bills. And we’re sorry to say that that car you were hoping to get on finance will just have to wait – you’ll want to avoid applying for any credit before your mortgage application goes through.

Strange as it sounds, you’ll also want to make sure your address is up-to-date on any old accounts, like mobile phone contracts or old credit cards. You might think it’s silly, but you don’t want to get rejected for a mortgage because of something as petty as this – trust us!

To check how your credit history is looking, just head over to Experian, Equifax and TransUnion. These three companies provide the information that’s used to work out your credit score, using something called a ‘credit report.’ They’re legally obliged to give you access to this report for free (thank you GDPR!) so make the most of it.

If you’re on a fixed-term contract and you have poor credit, this can really limit your options. So, you might want to take some time to improve your credit score before trying for a mortgage. That said, it’s always worth talking to a mortgage broker, who’ll be able to advise you on what your chances are given your individual situation.

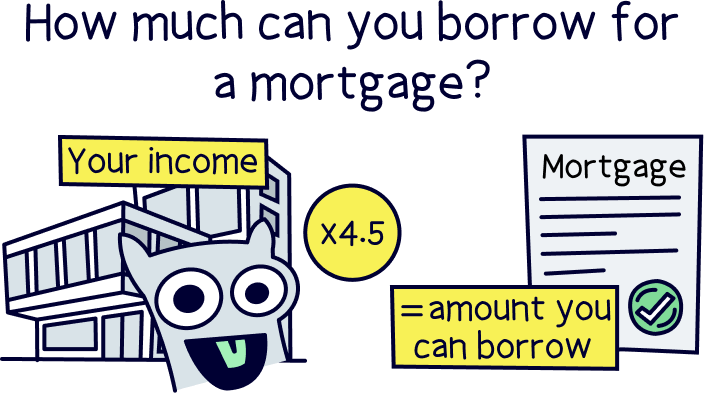

As a general rule of thumb, mortgage lenders will consider letting you borrow between 4.5x your yearly income.

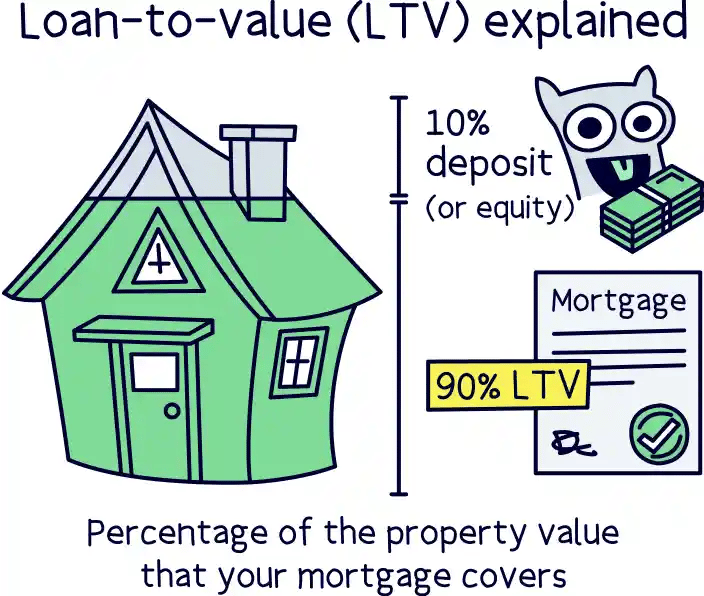

But don’t celebrate just yet! You’ll also need to chip in a percentage of the value of the house as a deposit. This relationship between the amount you’re borrowing and the amount you’re paying upfront is called the loan-to-value (LTV) ratio.

Most people are able to get an LTV of 80-90%. That means you’ll be borrowing 80-90% of the house’s value and using a deposit of 10-20%.

Having said that, it always helps to put down as big a deposit as possible. Aside from anything else, this shows that you’re fully committed to your purchase, which means you’ll usually have more options to choose from and get access to better deals (and who doesn’t love a deal?!).

It’s quite rare to get offered an LTV of 95% on a fixed-term contract but it’s not impossible. If this is what you’re looking for, talk to a mortgage broker to find out whether it’s realistic for you.

We know that finances aren’t fun, but now’s the time to quit putting them off and get them sorted! Start by paying off any unpaid credit card charges and bills so that your credit history is in the best shape possible. Then, make sure that your accounts are up-to-date and accurate.

You’ll also want to gather all the documents you need for the application. Depending on your situation, this might include utility bills, P60 forms (if you’re employed), tax returns (if you’re self-employed), proof of identity and bank statements. Let’s be honest, the last thing you want is to get sent foraging for documents when you’re halfway through your application. Plus, any mistakes could cause delays and may even make you less likely to be approved. No-one wants that!

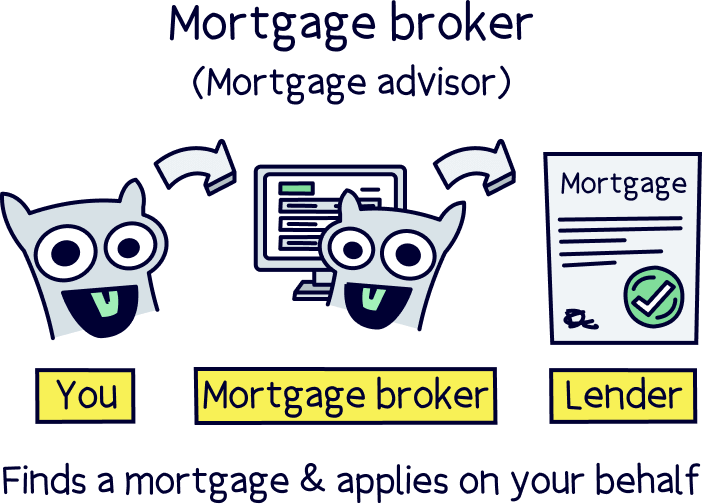

Why spend hours searching for the right deal and the perfect mortgage lender when you could get someone else to sort it all for you?

A mortgage broker will be able to tell you what the different lenders are looking for, where you should apply and how to get the best deals. Plus, they’ll even do the whole application on your behalf so you can enjoy twiddling your thumbs while someone else does the work (or better still, go get yourself a cuppa!).

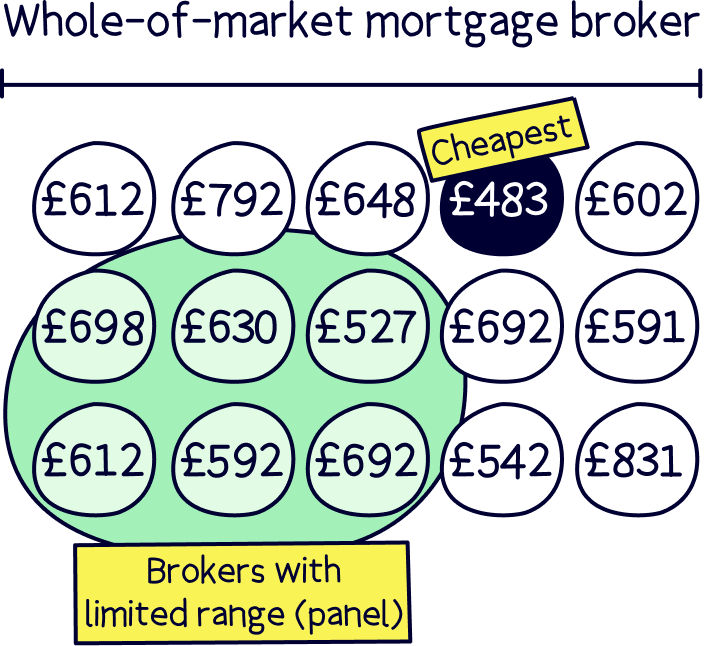

Just make sure that you opt for a mortgage broker who’s able to search the whole market, otherwise you’ll find your options limited.

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

Been accepted for a mortgage? Congrats! All that’s left is for your lender to process your application, which can take between around 18 and 40 days.

Meanwhile, you can whip your solicitors into shape and draw up moodboards for how you’re going to decorate. Before you know it, you’ll be unloading those cardboard boxes, ordering a Chinese takeaway and popping open the bubbly. You deserve it!

It’s impossible to say which mortgage lender would be best for you without taking a deep dive into your personal finances, employment situation and credit history (no offence, but that’s just not us!).

That said, these three mortgage lenders are known for being particularly flexible with contractors:

Remember that everybody’s different so there’s no way to know which mortgage lender will be best for you – these are only three lenders out of around 100 in the UK!

We’d always recommend using an independent mortgage broker, who’ll be able to advise you on the best lender for your circumstances. Plus, they’ll have access to a whole range of specialist lenders that you may not be able to approach yourself.

So, what do you think? Too early to crack open the bubbly?

As you can see, getting a mortgage as a fixed-term contractor is totally doable. In fact, there are tons of options available to you, no matter what kind of contracting you do.

If you’re still not sure whether you’ll be able to get a mortgage, why not get in touch with a mortgage advisor? They’ll be fully up-to-date with what the different mortgage lenders are offering and will be able to tell you what your chances are.

Not sure where to find a good mortgage broker? Check out Tembo¹, they've got award-winning service, and guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money.

Good luck! (you don’t need it, trust us.)

Yes! If you’ve been approved for a mortgage as a fixed-term contractor, you should be able to remortgage. In fact, it’s generally expected that you will when your fixed-rate mortgage comes to an end. Before we go on, we’d better explain: a fixed-rate mortgage is when your interest rates are fixed for a certain length of time. Nothing to do with being on a fixed-term contract, as similar as it sounds!

If you’ve recently changed from a permanent role to a fixed-term contract, or if your income has dropped, you may have fewer options when it comes to remortgage lenders. Always talk to an independent mortgage broker to make sure you get the best deal.

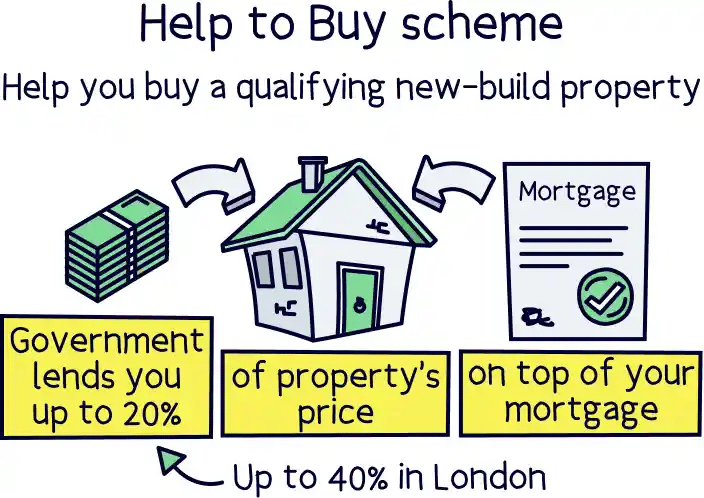

Yes, you can use the government’s Help to Buy scheme on a fixed-term contract. Just bear in mind that lenders will still have to assess your eligibility as they would if you were applying for a regular mortgage.

There are quite a lot of differences between the lenders that offer Help to Buy mortgages, so a broker will be able to help you find the best one for you.

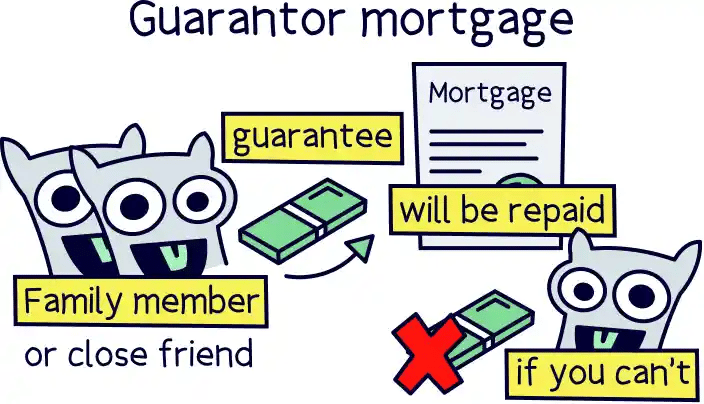

Yes. Roping in a guarantor can be a lifesaver if you’re struggling to get lenders to accept your employment status. It can also help if you have bad credit or you’re finding it hard to save for a deposit.

With a guarantor mortgage, you’ll need a guarantor who’s willing to make the repayments if you can’t.

Just beware: usually, your guarantor will have to use their own home as ‘security.’ In other words, if neither of you can make the repayments, their property will be at risk. So, it’s a big decision to make!

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.