Article contents

Yep, you sure can. As long as you have an income to cover the mortgage repayments and in your later retirement years, you'll be fine.

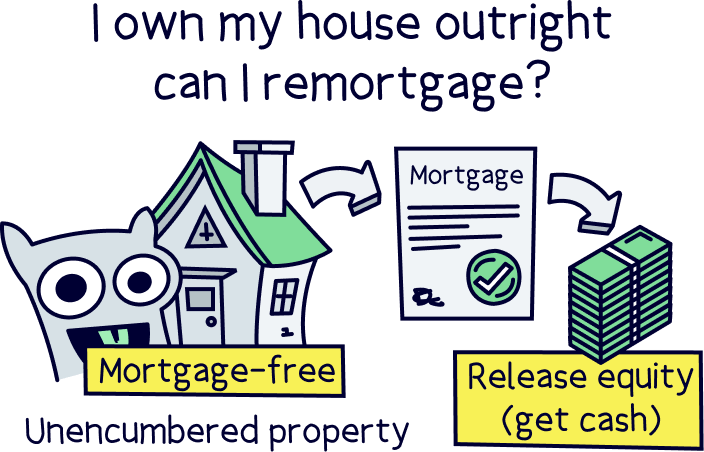

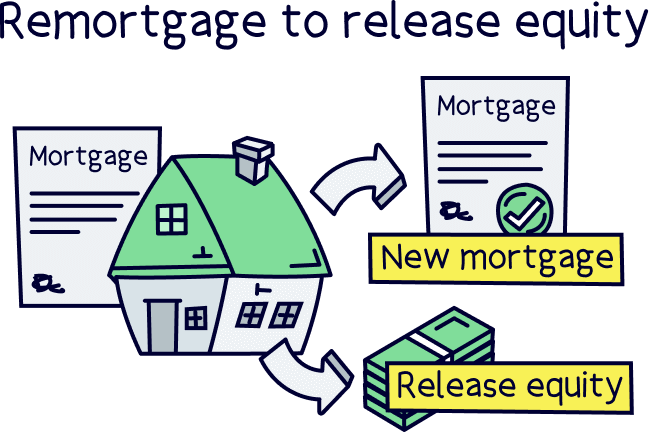

In the fortunate situation to own your house outright? And now want to remortgage? You certainly can do that.

It’s what is known as unencumbered. Well, your property is known as an unencumbered property. It means your house is mortgage-free, no mortgage at all, and it’s not acting as security for any loan. It’s a great feeling and the aspiration of many.

Technically you can’t remortgage your home because you don’t currently have a mortgage on it. You can simply apply for a new mortgage on your home instead.

There’s various reasons why you might do this, the main one being access to lower interest rates compared to a personal loan or credit card, and being able to typically borrow a lot more, depending on the value of your home of course, but personal loans are normally capped at £25,000. But do bear in mind your property is now secured against the loan, and it could be repossessed if you do not keep up repayments.

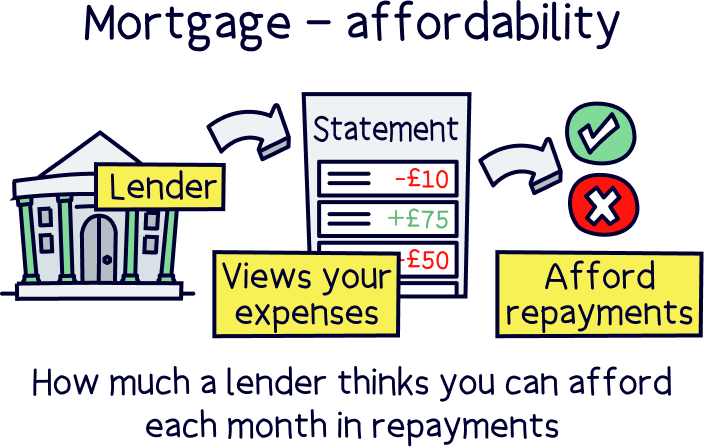

You won’t by default just be able to get a mortgage, you’ll still need to prove to a lender that you are able to repay the mortgage each month. These checks are often:

Affordability: That’s how much you earn, or your total income. You need to be able to afford the monthly repayments. There’s also what other debts you have, such as a personal loan or a credit card and their repayments.

Age: If you are nearing retirement, it may be a bit harder to get the mortgage you want. Typically lenders will only lend to your retirement age.

Adverse credit: If you have CCJs, defaults, late payments, IVA, bankruptcy etc.

The purpose of the mortgage: You may need to specify why you want to remortgage. Typical reasons are buying a partner out, home improvements, buying a car, repaying debt etc. You can also use the money to purchase a buy-to-let property.

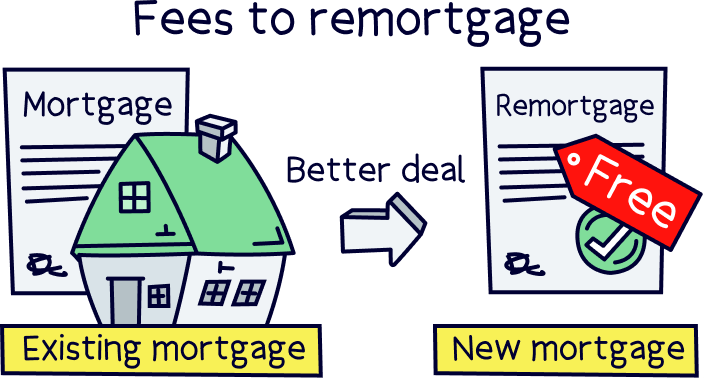

If you're worried about fees to remortgage, don't be! There's not many, if any.

Your broker will explain all.

Tembo will find your best deal, fast, all with award-winning service.

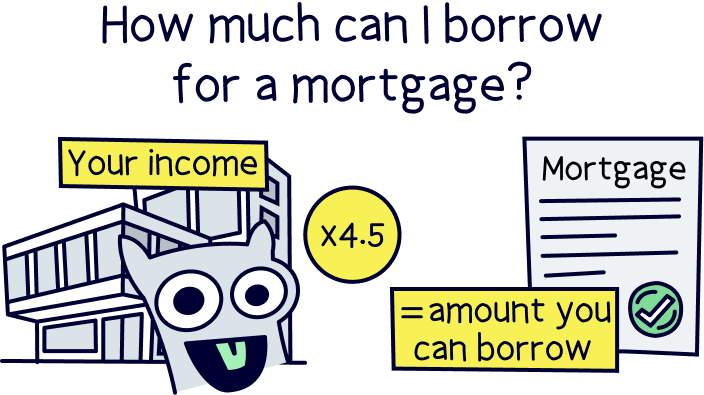

First let’s look at how much you want to borrow. With the figure in mind, we can determine if you are actually able to borrow that amount or not, and then if you are able to afford it.

So take your figure, let’s say £100,000 for ease, and multiply your total income each year by 4.5x. So if you’re earning £30,000 per year, you’ll be able to borrow roughly £135,000. That’s £35,000 over what you are looking to borrow, so it’s looking like you’ll be able to get a mortgage.

If you’re looking to borrow less than £50,000, you may find it more difficult, as the number of lenders in the market are lower, but it’s not impossible. Speak to a mortgage broker for specific advice.

If you’re not sure where to start, check out Tembo¹, they've got award-winning service, and guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

It may have been years since you had a mortgage on your home, or you may never have had one, so may not know it’s current value. But it’s a good idea to try and work out roughly how much it’s worth now so you can get a more accurate quote for a mortgage interest rate.

You can do this by looking at recent sale prices in your area on Zoopla, or you could get a free valuation from an estate agent.

Don’t worry if you’re not completely sure though, your lender will value the house as part of the mortgage application.

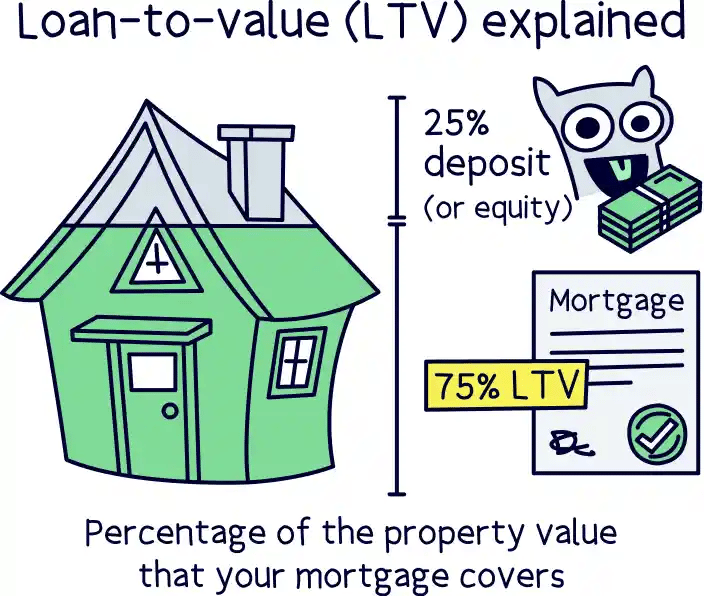

With our scenario of wanting to borrow £100,000, let’s say we estimate our house to be worth £200,000. That means our loan-to-value will be 50%, as simply, we want to borrow 50% of the house value. This also means we’ll have 50% equity left in the house – the bit we’ll still own outright.

If your LTV is high, over 85%, expect fairly high interest rates, but you can still get a mortgage. You may want to consider borrowing less however to get more competitive rates nearer the 60% mark. If you’re already in this range, great.

It’s not possible to borrow more than your house is worth – nice try!

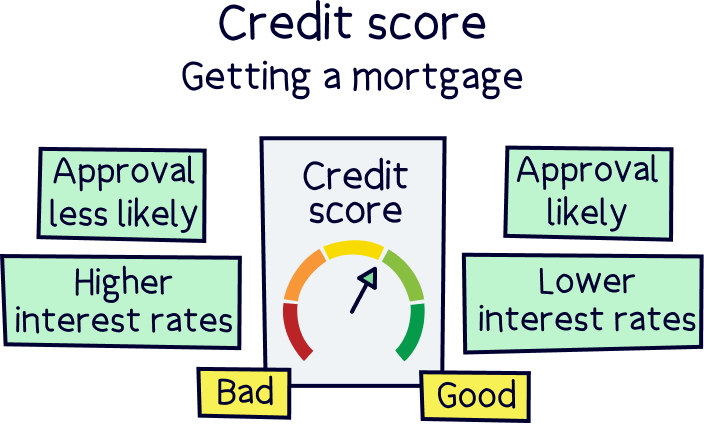

If you’ve not borrowed money for a while, just have a quick check of what your credit score is and make sure you are in good shape to borrow a large amount of money. Here’s a short guide on mortgages and credit scores.

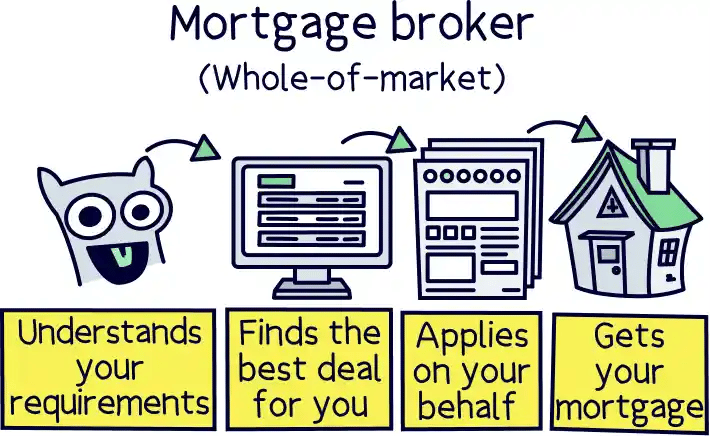

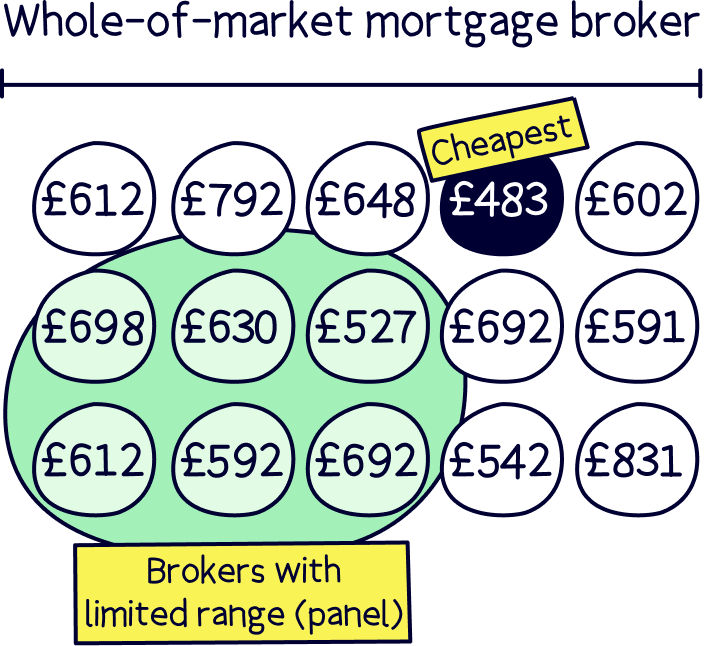

You might be thinking of ‘going alone’, and arranging the mortgage yourself, and you can, but in order to get the best deal for you, it’s really worth speaking to a mortgage advisor, also known as a mortgage broker. There are thousands of mortgages out there with wildly different rates, so it’s worth using an expert who can search the whole market for you and make sure that it’s the right mortgage for you. Make sure you use one that can search the whole market, otherwise you’ll be limiting your options.

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money.

If you are using a mortgage broker, this is the easy bit. When you're ready to apply, they’ll do it all for you. You can just sit back and relax.

Your mortgage will be completed by the lender and you’ll get the money in cash straight to your bank account. Pretty straightforward isn’t it?

If you had bad or adverse credit and want to remortgage your unencumbered property. You can. But your options are going to be very limited, you’re probably going to have to use a specialist lender who will do their own checks on your affordability rather than use a credit score. So if you can comfortably afford repayments, and your LTV is low, you should be ok. It’s best to speak to a mortgage broker who can advise about specialist lenders.

Remortgaging your property is not equity release. They are very different. In this scenario you still own your home and are just borrowing money against it, as a guarantee for future payments.

Equity release, often called lifetime mortgage or a home reversion plan, is where you get a lump sum in cash but are then liable to repay this money when you pass away, which is normally from selling the home or the lender taking possession.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.