Article contents

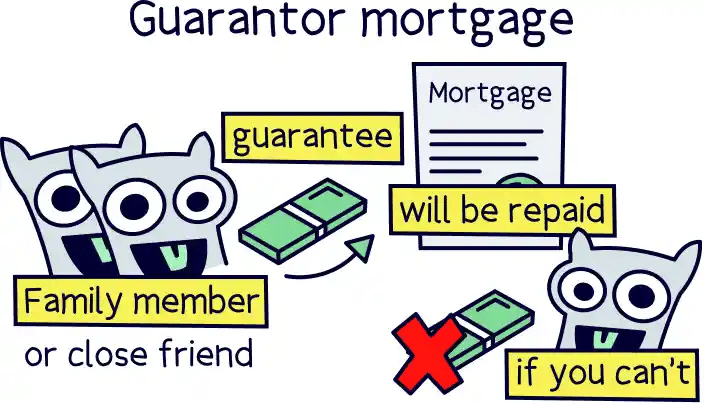

A guarantor mortgage can be a massive help to get on the property ladder. It’s using a family member or close friend to put their name behind your mortgage too (and sometimes their savings and own home). There’s a few out there, and we recommend using a mortgage advisor to find the best one for you.

Perfect for first time buyers, or those who are finding it a bit difficult getting a regular mortgage, such as a low income or a bad credit rating – a guarantor mortgage can be a life line in terms of buying your home. You can also get a guarantor mortgage when you’re switching deals (remortgaging) too.

You can even get a mortgage without any deposit (called a 100% mortgage). We know you were wondering!

Let’s run through all the details about how guarantor mortgages work and how to find the best guarantor mortgage for you.

Guarantor mortgages can be a great way to help you buy a home and get on the property ladder that you otherwise couldn’t do (and be stuck renting or living with your parents forever!).

Using a guarantor mortgage, you can often borrow more than you otherwise could, and it might even be your only option to get a mortgage in the first place. You can also use one to increase your deposit to get a bigger property too (we’ll cover all this in detail below).

Guarantor mortgages are simple really, but let's run through a quick example to make it super clear. Imagine you buy something that has a guarantee – so it will be fixed or replaced if sometimes goes wrong, it’s a pretty good thing right?

Well with mortgage lenders (the people who give out mortgages), in order to lend out money to some people, they want a guarantee that their money will be repaid. They want to know that they’ll still get their monthly repayments every month even if you don’t pay.

Obviously you’re planning to pay the mortgage, but they categorise a lot of people into small categories, and treat them all the same (such as low income earners). We’ll cover who guarantor mortgages are for below.

So, mortgage lenders want someone trustworthy as a backup to act as a ‘mortgage guarantor’, such as a parent, or another close family member, who will accept joint responsibility for the mortgage and put their name to the mortgage repayments too. So they’ll have to pay if you don't.

It’s only a last resort that they will have to pay, such as if you can't pay the mortgage for a few months, then your mortgage lender has the right to get the cash off them.

And often, your mortgage guarantor will have to guarantee their own home as ‘collateral’, or ‘security’, which means the bank can take their home if neither of you make the mortgage repayments.

Don't worry, this is pretty rare and the mortgage lender will make every attempt to get their money back by other means.

However, if you can't make the monthly repayments and there's no way of you paying it, and your mortgage guarantor can't pay it either, then the lender will be forced to sell your property to pay back the mortgage.

If they sell it for less than the total of the mortgage there will still be debt to pay (called negative equity). To recover this debt they have the right to sell your guarantor's property.

So make sure you can definitely afford to make the mortgage repayments every month before you take out the mortgage, and ideally you would have spare cash as a buffer too – just in case you have any unexpected bills.

Nuts About Money tip: if your circumstances change and you think you will struggle to pay the mortgage, speak to your mortgage lender as soon as possible. They will want to help, and there are things that they can do, like extending your mortgage term (the length of the mortgage) – this will reduce the amount of the monthly repayments (although you will pay more interest in the long run as you are borrowing the money for longer).

By the way, a guarantor mortgage is a type of ‘specialist mortgage’ – which simply means they’re not the regular type of mortgage, or ‘normal’ mortgage, and you would often need specialist mortgage advice and a specialist lender (we’ll cover that too).

Not sure where to find one? Check out Tembo¹, they specialise in guarantor mortgages (get 50% off with Nuts About Money).

Tembo will find the best mortgage for you, and help increase your borrowing.

Let’s run through who guarantor mortgages are most suitable for.

Guarantor mortgages are for people who might struggle to get a mortgage, or to borrow as much as they’d like to get their dream home. So, they’re suited for people with:

By the way, you don’t need to make a decision on either a ‘normal’ mortgage or a guarantor mortgage right now. Your best bet is to speak to a specialist mortgage advisor who can help with both, you can review all your options and see which is best for you.

Our recommendation for a mortgage advisor who specialises in guarantor mortgages is Tembo¹.

Although we say ‘guarantor mortgage’, there’s actually a few different types of guarantor mortgages, but in all cases it’s normally a parent or family member helping out.

There’s a few different names for guarantor mortgages these days, as they’re becoming pretty popular now getting on the property ladder is so hard.

Some names include:

However, behind the scenes they all work in the same way, and use one of the below methods:

The first type is where your family member has some savings of their own, and they move these savings into a special savings account with the mortgage lender, and this acts kind of like the deposit on your property. This is technically called ‘savings as security’.

This cash is kept in the guarantor’s savings account until the percentage of your home that you actually own reaches a certain point (called your equity), and then it can be repaid. It can sometimes still earn interest.

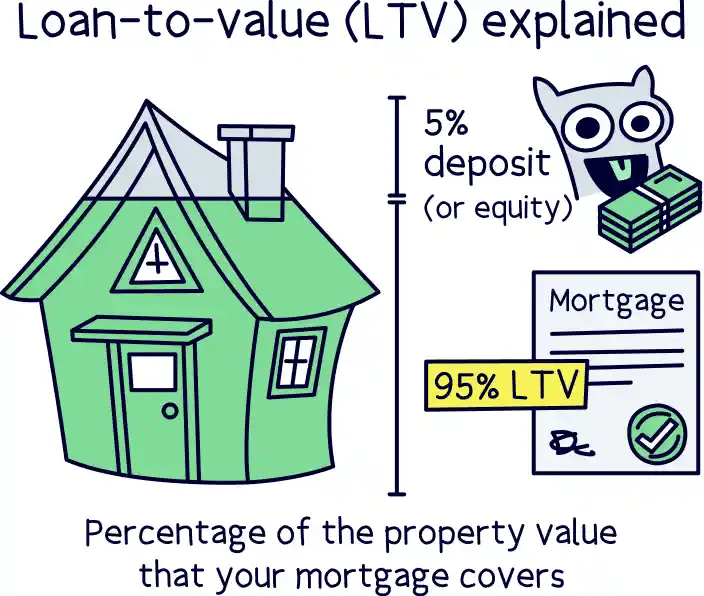

For instance, if you buy a home with a 5% deposit, although you own the whole home, you actually only have 5% cash in the property itself, and the remaining 95% has been paid for with the mortgage. So, effectively the bank owns that portion.

This is also called loan-to-value or LTV. So, with a 5% deposit, you have 95% loan-to-value (the mortgage loan covers 95% of the property's value).

So, with the ‘savings as security’ option, with your family’s money in a guarantor’s savings account, the mortgage lender might only release this cash back to them when your LTV drops down to an agreed point, which could be say, 80% LTV.

You don’t need to actually pay any cash into your mortgage to reduce this, although it will reduce with every mortgage repayment as you’re paying back the loan. It also reduces when house prices increase – your mortgage stays the same amount but the property increases in value, so your loan-to-value reduces.

If your family member owns a high proportion of their own property, so has a lower LTV, for instance 60%, then they can use this as a guarantee for your mortgage, without putting any of their savings on the line either.

What technically happens is a ‘charge’ is put on the guarantor’s property, which means the mortgage lender can take charge of it if you fail to make your mortgage repayments. They can then sell your guarantor’s home to get their money back.

Even if they sell your home, if you’re in negative equity, meaning the property value wasn’t enough to cover the entire mortgage, they can still sell your guarantor’s home.

This is a more modern approach, and if your guarantor has a low LTV on their own home, or owns it outright, the mortgage lender can also put a small additional mortgage on their home, which releases some cash to act as your deposit, or they can switch their mortgage deal to a new deal, called remortgaging, to release cash.

This means you’ll have a much bigger deposit overall, so can get access to better mortgage rates (the larger the deposit the better the interest rate you will get), plus of course, the ability to get a mortgage in the first place if you only have a small deposit.

You’ll likely be making payments towards their new mortgage, but if you don't pay it, they will have to pay it. The mortgage deal on their own home can also be interest only. This is when you don't repay the mortgage but you just pay the interest. Of course the mortgage will have to be repaid eventually, but this can be further down the line.

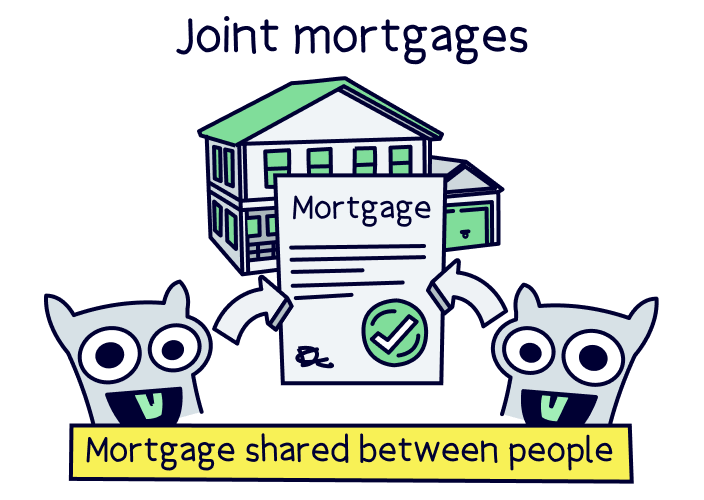

You can also buy a property together with someone (such as a parent), which is called a joint mortgage. You’ll both own the property, so both be on the property deeds (the legal documents saying who owns the property), rather than just you. And both will be legally responsible for making the mortgage repayments.

With a joint mortgage, you can use both of your incomes (e.g. salaries) to determine how much you can borrow for a mortgage, so you can borrow a lot more! You can also use their savings if they have any to put towards your deposit directly (rather than in a separate account).

However, you often can’t get a mortgage that runs past someone's retirement age. So you might not be able to get a mortgage for as long as you’d like (the longer the mortgage, the lower the monthly repayments – but more interest paid overall).

For instance, if your partner on your mortgage (a parent) is 50, they’ll likely retire before they’re 70, and so the most you might be able to get is a 20 year mortgage. The most common length of mortgages is 25-35 for first time buyers.

And if your parent has their own home, they won’t count as a first time buyer in terms of Stamp Duty (the tax on buying a home), which means you also won’t count, and won’t get the first time buyer Stamp Duty relief, which is 0% tax on anything up to £425,000, and would have to pay Stamp Duty on anything above £250,000 (the regular threshold), which is 5% up to £925,000.

But it gets worse, it would technically count as a second home for them, which means you’ll have to pay a 3% Stamp Duty surcharge (extra payment) on your property, and this starts from £0, not the £250,000 lower limit like regular Stamp Duty.

If both of you aren't first time buyers, a joint mortgage can be very expensive. But there is a workaround if you think you might want a joint mortgage…

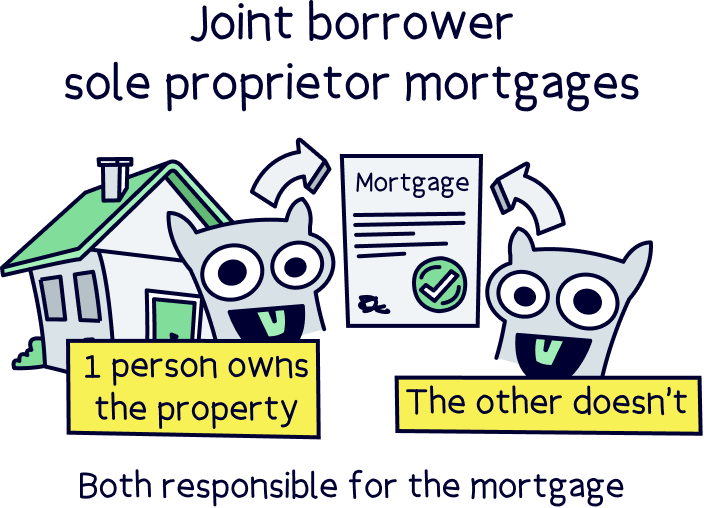

This is a very popular option and a similar concept to joint mortgages, where you can buy a home with someone else, such as a parent or family member, however there’s only one person who actually buys the property (you), and only your name will be on the deeds of the property.

Mortgage lenders are basically being nice with JBSP mortgages, and letting you borrow money so you can buy the home in your own name, but still with all the protection of a joint mortgage (i.e. you are both jointly responsible for the mortgage repayments).

This means your family member doesn’t need to put any savings up or put their own home on the line, but you will still need to pay a deposit when you buy the property, for instance 5% or 10%.

It also means there’s no second home surcharge on Stamp Duty, and you can benefit from all the first time buyer benefits, such as less Stamp Duty (or often none).

You can actually have up to 3 people with a Joint Borrower Sole Proprietor mortgage. So, both of your parents, or other family members.

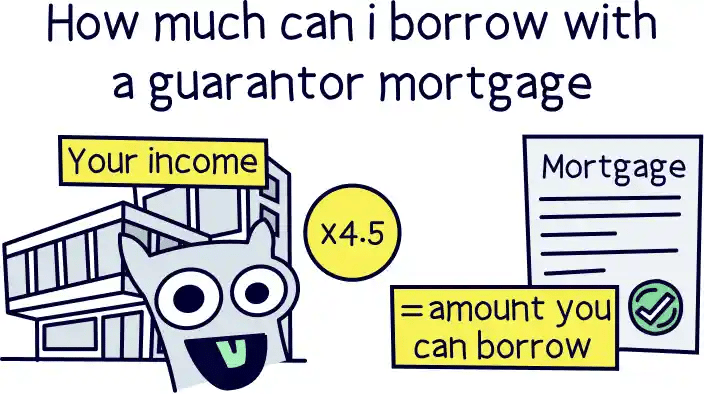

How much you can borrow with a mortgage is typically worked out based on your income, and typically in the region of 4.5 times what you earn.

So, if you earn £25,000 per year, you could borrow somewhere around £112,500.

However, with a guarantor mortgage, you can normally add your mortgage guarantor (often with Joint Borrower Sole Proprietor mortgages) as a ‘booster’ to your income, so, take their income too and add them both together to work out how much you could borrow.

If they also earn £25,000, you can now borrow up to £225,000. But, you’ll still need a deposit, so you can’t necessarily borrow as much as the maximum because you’ll need at least a 5% deposit in cash.

However, bear in mind, that the higher the mortgage amount, the more the monthly mortgage payments will be.

How much you can borrow can get pretty technical, this is just a rough idea, and it depends on which type of guarantor mortgage you want to go for. Some types, such as a family member putting some of their savings aside for you, won’t count towards how much you can borrow, it will just allow you to get the mortgage in the first place.

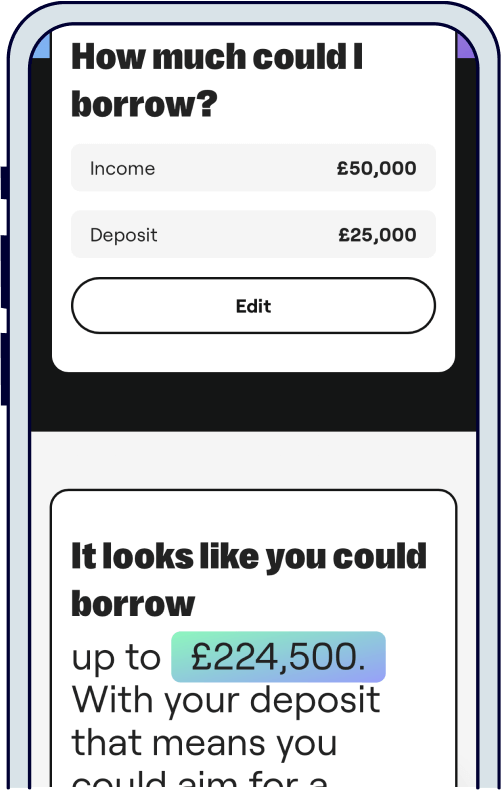

To make things a bit easier (who likes doing maths anyway?), use a mortgage calculator¹ to work out how much you can borrow and get a more accurate figure.

With guarantor mortgages, the interest rate you’ll get is typically a bit higher than a regular mortgage. The interest rate is a percentage of how much you’ll pay each year as a fee to the mortgage lender for borrowing the money.

They’re higher because a mortgage lender is taking on more risk lending to you, as you have a higher chance of not paying the money back. That’s because you could have a lower income, a bad credit rating, or have a smaller deposit so are borrowing more money.

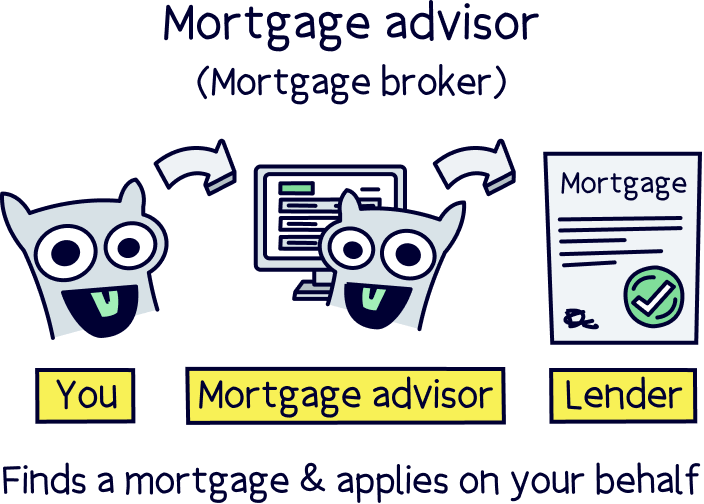

It’s best to use a mortgage advisor to find you the best interest rate (well, actually the cheapest mortgage overall, including all the fees). We’ll cover all of that below.

Typically the only people who can be a guarantor for you are a close family member such as your parents – normally someone trustworthy who has a good income, their own home or some savings. Occasionally, it can be a family friend.

They’ll also need a good credit rating and good credit history. But ultimately, it’s up to the mortgage lender if they’ll be a good fit as your mortgage guarantor.

If it’s a joint mortgage in both of your names, then it can be anyone, as they’ll be jointly responsible for the mortgage too, but not necessarily with a Joint Borrower, Sole Proprietor mortgage.

So, all quite confusing isn’t it? But the best way to get a guarantor mortgage is to speak to a specialist mortgage advisor who’s an expert in this area.

A mortgage advisor is someone who gets to understand a bit about you and the property you’re trying to buy, and then goes out and finds the right mortgage for you.

They’re often worth their weight in gold as they’ll ensure you’re getting the best mortgage deal for you, and getting a bad deal can sometimes mean paying £100s more than you need to every month. It really does pay to use an advisor.

The main factor when choosing the right advisor is to make sure they can search the ‘whole market’, that means they can search every mortgage deal out there. If they can’t, then you can’t be sure you’ll get the best deal.

Our recommendation for a mortgage advisor who specialises in guarantor mortgages is Tembo¹ (get 50% off with Nuts About Money).

Get 50% off the standard fee

Tembo is an all-round amazing mortgage broker, in fact, they're award-winning, and not just online.

They can help with pretty much every mortgage out there, from buying a home to switching deals, and on top of that, have unique options to increase your borrowing such as an Income Boost¹ and Deposit Boost¹.

They'll handle the whole mortgage for you too, and the service is great.

Tembo will find the best mortgage for you, and help increase your borrowing.

There’s a fair few lenders out there now that offer guarantor mortgages to help first time buyers get on the property ladder. So, if you’re still keen to look for a mortgage yourself, rather than use a mortgage advisor, or simply want to learn more first, here’s the best guarantor mortgage lenders:

These are in no particular order, and all have different criteria to determine if you’ll get a mortgage with them or not. Don’t apply to any of them until you’re sure you’ll get a mortgage, as a mortgage application will negatively affect your credit score, which can stop you getting a mortgage from another lender if you get declined.

A mortgage advisor will know all the different criteria and which mortgage lender is the best for you, and ensure you’re in the best position to be accepted for the mortgage.

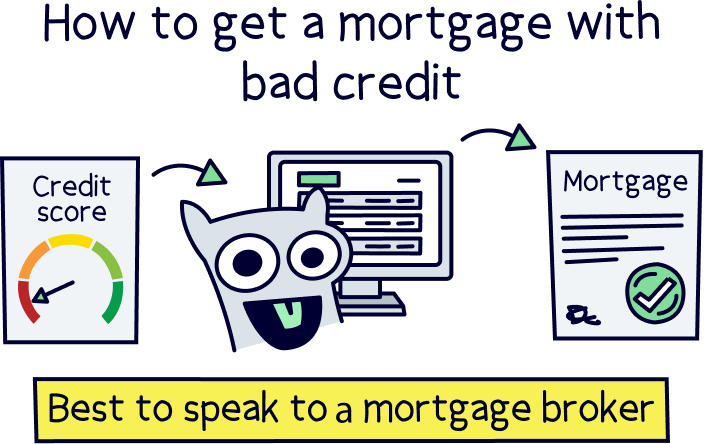

Trying to get a mortgage with bad credit? It can still be done, and a guarantor mortgage is a popular option.

As long as you can pay the mortgage, lenders will generally be happy to include a guarantor on your mortgage to offset your bad credit. There’s no specific ‘bad credit guarantor mortgage’, simply speak to a mortgage advisor to find the best options for you.

It’s a sad topic, but something to consider. If your guarantor dies, you may have to find another guarantor to take on their guarantee (although easier said than done), or you might be able to carry on as normal – it’s all up to the mortgage lender.

If there’s any money left to you from your guarantor’s estate (the total of their money), then your mortgage lender might allow you to pay some of the mortgage off and move to a ‘normal’ mortgage.

And that’s it for guarantor mortgages. Hopefully that’s made things a bit clearer and easier to understand.

There’s several options out there, from using your guarantor (usually a parent) to put up some savings or their home as a guarantee (security), to actually having your guarantor's name on the mortgage too (Joint Borrower, Sole Proprietor mortgage).

Just make sure you’ll be able to make your mortgage payments every month, or you might be affecting your family’s finances too – being a guarantor is a very serious obligation and commitment between both of you. Their savings and/or property is at risk too.

To find the best guarantor mortgage for you, we recommend using a mortgage advisor – they're experts and know the best lenders for your circumstances, and the best type of guarantor mortgage for you.

We recommend checking out Tembo¹ for a guarantor mortgage, they've got award-winning service (get 50% off their fee with Nuts About Money).

Tembo will find the best mortgage for you, and help increase your borrowing.

Tembo will find the best mortgage for you, and help increase your borrowing.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find the best mortgage for you, and help increase your borrowing.