Article contents

If you only have a minor credit issue, you might be able to get a competitive mortgage from a high street bank. If the issue is more serious, you’ll normally have to turn to specialist lenders who offer bad credit mortgages.

You might think that if you have bad credit, you’re never going to be able to get a mortgage. But guess what? Getting a mortgage with bad credit is totally possible. Here’s all you need to know.

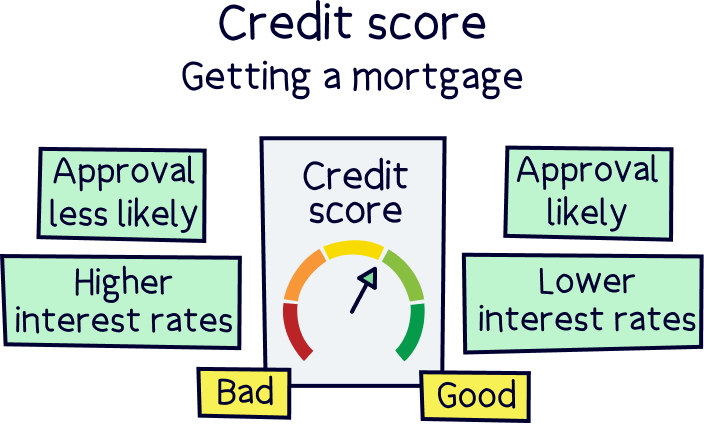

If you have bad credit, this normally means you have a problem with your credit history. Your credit history is an overview of everything you’ve done up until now money-wise, kind of like a footprint of your financial history. It’s used to calculate your credit score, which is a number mortgage lenders use to see how good you’ve been with money in the past (lenders are the people who give out mortgages).

If you’ve had issues with money – for example, you’ve failed to pay your bills on time – this will show up in your credit history. And, normally, it will translate into a bad credit score.

It can be harder to borrow with a bad credit score as, if you’ve had money troubles before, it’s more likely that it could happen again. But that’s no reason to panic! Here’s why...

Tembo will find your best deal, fast, all with award-winning service.

Yes! Contrary to what you may think, you can get a mortgage with bad credit.

There are over 100 mortgage lenders in the UK, and while some of them will refuse to lend to people with bad credit altogether, others will be much more flexible. Some mortgage lenders actually specialise in lending to people who have bad credit and even offer something called bad credit mortgages.

‘Huh? What’s a bad credit mortgage?’ we hear you ask.

A bad credit mortgage is a mortgage designed especially for people with bad credit. Hooray! There’s just one problem: they can be pretty expensive.

This is all to do with risk. If you’ve had trouble with money in the past, mortgage lenders will worry that it will happen again and you won’t be able to keep up with your monthly mortgage repayments. Basically, they’re charging you higher rates to make up for the extra risk.

Don’t get us wrong: if you’re struggling to get a mortgage because of your credit score, a bad credit mortgage could be a bit of a lifesaver. However, depending on the issue and how bad your credit score is, you might not actually need to get a bad credit mortgage. Instead, you may be able to get a standard mortgage from a high street bank, which is likely to be cheaper.

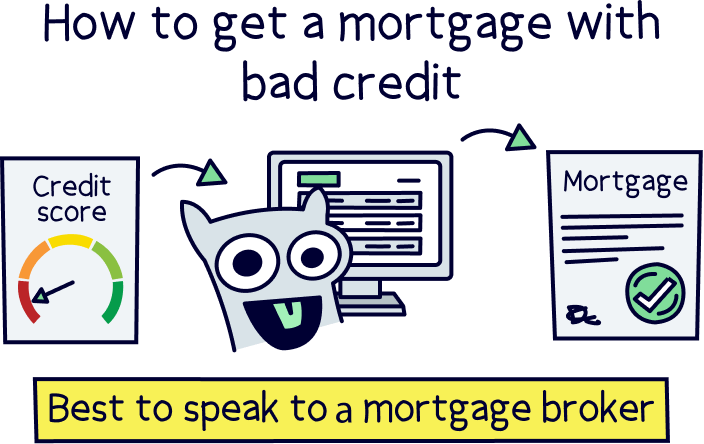

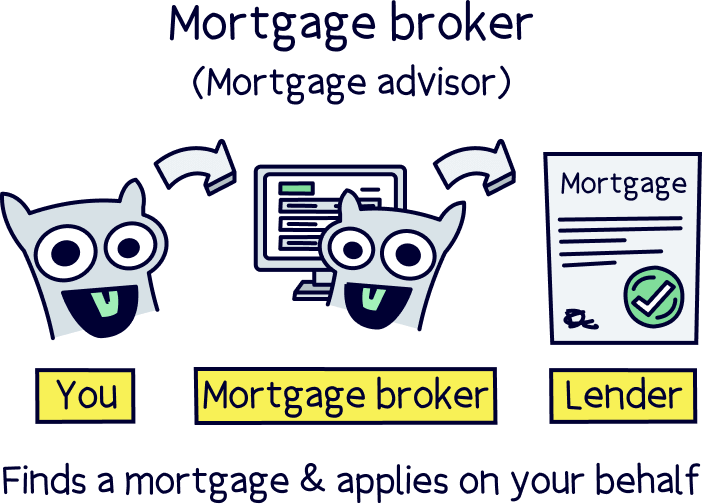

To find out what your options are, you’re best off speaking with a whole-of-market mortgage broker (also known as a mortgage advisor). They’ll be able to compare all the different mortgages available to you from all the different lenders to find you the best deal. Plus, they’ll sort your application out from start to finish.

If you’re not sure where to start, check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

Okay, okay, so we know we said that it’s possible to get a mortgage with bad credit. And it is! But even bad credit mortgage lenders will want to do some checks before deciding whether or not they’re happy to give you a mortgage. Here are the main things they’ll look at.

Of course, credit history is just one aspect of what lenders will look at when they’re umming and ahhing about whether or not to give you a mortgage. They’ll also need to weigh up all the other things that lenders normally check, such as your income, expenses, job and deposit.

The stronger you perform in all these other checks, the more likely you are to be able to persuade a lender that they should give you that mortgage you’re after!

So, what can you do to make it more likely that a lender will accept you for a mortgage, despite your bad credit? Just follow these simple steps.

If you have a bad credit score, the first thing to do is find out why. This can be done by checking something called your credit report.

A credit report is a statement that lays out your credit history. It’s what’s used to calculate your credit score, and lenders will use the info on there to help them decide whether or not to give you a mortgage. So, safe to say you’ll want to know what’s on there!

There are 4 main companies that provide credit reports, known as credit reference agencies. They’re called Experian, Equifax, TransUnion (which used to be Callcredit) and Crediva. To get hold of your reports, you’ll just need to get in touch with each company or use CheckMyFile, which will get them all for you in one go. That way, you can see what the issues are and, hopefully, work out how to resolve them!

Now you know what the issues are with your credit, you can spend some time trying to improve it!

That means getting up-to-date with any late payments and paying off any outstanding credit cards. And yes, sadly, it also means avoiding taking out any more loans for the time being. That car on finance that you’ve had your eye on might just have to wait, but it will be worth it for your dream home!

There’ll probably also be some quick wins on your credit report. For example, did you know that you can harm your credit score by changing addresses frequently, or even just old mobile phone contracts that are still showing up?!

By making sure your address is up-to-date on any old accounts and signing up to vote (so that you appear on a database called the electoral roll), you can quickly get your credit score looking as awesome as possible.

Remember those super helpful guys known as mortgage brokers or advisors that we mentioned earlier? Well, we’d always recommend getting one involved if you want a mortgage. But we’d really recommend it if you want to get a mortgage with bad credit.

A mortgage broker will actually take the time to sit down with you and learn all about your personal circumstances – including your credit situation – before giving you tailored info and advice. It’s best to choose a ‘whole-of-market’ broker, as they’ll also be able to compare all the different deals and lenders available to you to make sure you’re choosing the best (and cheapest!) one for you.

Mortgage brokers are experts in mortgages, so they’ll have a much clearer idea than you would about which lenders are most likely to give you a mortgage. This is important because, if you apply for a mortgage and get rejected, it could harm your credit score even more, making it even harder for you to get a mortgage.

By sorting out the whole application for you, your broker will give you the best possible chance of getting approved (and finding the best deal!). That way, you can avoid doing further damage to your credit score and, fingers crossed, get the keys to your very own home before you know it. Get in!

Not sure where to find a mortgage broker? Check out Tembo¹, they've got award-winning service, will find you the best deal, and you'll get 50% off their fee with Nuts About Money.

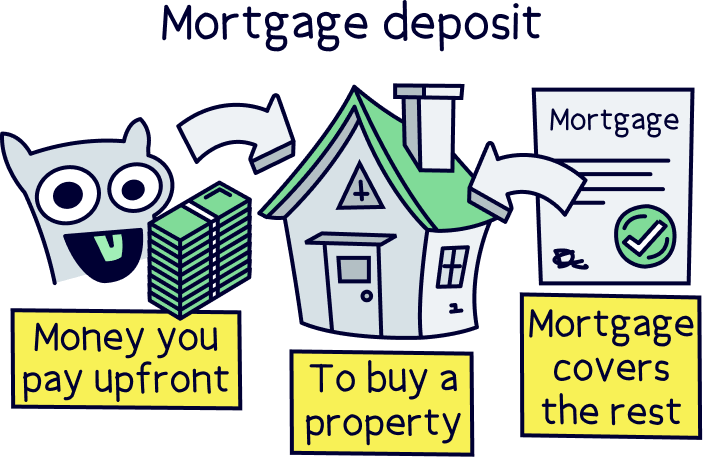

Let’s imagine you don’t have any credit issues. In this case, most lenders in the UK will want you to pay a deposit of at least 5% of your property’s value. In other words, the maximum mortgage you can normally get will be for 95% of what you’re paying for your home.

Here’s an example for you. Say you’re buying a property for £200,000. In this case, most lenders will let you borrow a maximum of £190,000 (95% of 200,000 = 190,000), meaning you’d have to fork out a deposit of at least £10,000 (5% of 200,000 = 10,000).

If you only have a minor issue with your credit, you might still be able to get away with a 5% or 10% deposit. However, if you have more serious issues, you’ll often need to put forward a lot more.

For example, if you’ve been bankrupt or you’ve had a previous home repossessed (where your lender takes ownership of your property, usually because you can’t afford to keep up with the repayments), you could need a deposit of up to 25%. The same goes if you’ve had an Individual Voluntary Arrangement (IVA), which is an alternative to bankruptcy.

If you’re really struggling to convince a lender to give you a mortgage, you might even need to pay a deposit of 50%. In this case, you’d still need to pass certain checks, but you’d be much more likely to get approved as you’d be making yourself a lot less risky to mortgage lenders.

A mortgage broker will be able to give you a better idea of exactly how much deposit you’ll need for a mortgage, given your unique circumstances.

There are many different issues that can lead to bad credit, and they’re all treated slightly differently by lenders. With that in mind, here are the main issues and how lenders often feel about them.

Not all issues with your credit are to do with money troubles. No credit history is a great example of that.

If you have no credit history, it means there’s no info on your credit report. So, lenders won’t have anything to go off when they’re deciding whether or not to give you a mortgage.

You might end up with no credit history because you’ve only just moved to the UK. Or, maybe you’ve simply always lived with your parents.

A specialist mortgage broker will often be able to help you find a mortgage, but it’s best if you try and build up your credit history first. There are some really easy ways to get started. For example, you can open up a UK bank account if you don’t already have one, or you could register to vote so you show up on the electoral roll.

There are lots of different things that can lead to a low credit score. In fact, similarly to no credit history, many of these factors aren’t to do with money issues at all.

You might have a low credit score because you’ve never borrowed money before. This means you won’t have a track record for paying back money on time, which will make you more of a risk to lenders. Alternatively, you may simply have no address history.

By taking out a small form of credit, like a mobile phone contract, or getting a credit card and paying it off on time and in full each month, you can quickly start to get your credit score into better shape. And, hopefully, this will help you to get a decent mortgage deal.

Many lenders will be happy to give mortgages to people who’ve missed payments before, although they all tend to treat late payments slightly differently.

Normally, lenders will be happier to give you a mortgage if you’ve only missed a payment once, as opposed to having missed many payments over time. However, let’s imagine that you missed a payment 6 months ago and still haven’t caught up. Some lenders won’t take it too seriously as they’ll just count it as one late payment. But others will look at it more harshly, seeing it as 6 months’ worth of late payments.

Similarly, lenders will treat your application differently depending on what kind of payment you’ve missed. For example, lenders often won’t mind too much if you’ve missed a credit card payment, but they’ll be much more worried if you’ve missed a mortgage repayment. After all, if they’re going to be giving you a mortgage, they’ll want to be sure that paying it will be your top priority.

A default is what it’s called when a lender closes your account due to missed payments. This could be an account with your bank, your electricity supplier, your mobile phone company… the list goes on.

Meanwhile, a CCJ is a county court judgment and happens if someone takes you to court for not paying money you owe. Both these issues tend to be treated pretty seriously by mortgage lenders.

If the issue occurred a while back, you might be able to qualify for a standard mortgage with one of the big banks. However, there’ll still be specialist lenders who’ll be willing to give you a mortgage if the issue happened more recently. Many lenders will need you to pay back CCJs first though!

These are the most severe issues that you can have in your credit history.

Repossession is when your lender takes ownership of your property because you’ve stopped paying what you owe. And bankruptcy is when you’re legally declared as unable to pay your debts.

It can be harder to get a mortgage with these issues in your credit history, but it’s still possible – especially if they occurred a while back. A specialist mortgage broker will be able to lay out your options for you.

A payday loan is a special kind of loan that’s designed to tide you over until payday.

If you have a payday loan in your credit history, this will be a red flag for lenders. In fact, most UK lenders will point blank refuse to give you a mortgage if you’ve had a payday loan recently as they’ll see it as a sign that you weren’t able to manage your finances properly.

If you’ve had a payday loan, your best bet is to get in touch with a mortgage broker to see what your options are.

The best bad credit mortgage lender for you will depend on all sorts of things, including the severity of the issue that’s showing up in your credit history.

Only have a minor issue? You might be able to qualify for a competitive mortgage with a big bank. Halifax, the Royal Bank of Scotland and Santander are all examples of lenders that don’t have specially designed bad credit mortgages but will consider applicants with bad credit scores, bankruptcies and CCJs on a case-by-case basis.

Got multiple issues in your credit history? Or issues that occurred recently? In this case, you might need to look at lenders who offer specially designed mortgages for people with bad credit. Here are some examples.

So, just because you’ve got bad credit, that doesn’t mean you have to despair. You still have every chance of being able to get a mortgage on that dream property you’ve had your eye on!

If you’re ready to get started, why not find a mortgage advisor sooner rather than later? They’ll be able to guide you through the whole process, from finding you the best deals to sorting out your whole application for you. That’s right, you just sit there feeling smug while they work their butt off for you. Easy!

As a reminder, if you need to find a decent mortgage broker, check out Tembo¹, they've got award-winning service, and will guarantee to find you the best deal. You'll also get 50% off their fee with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.