Article contents

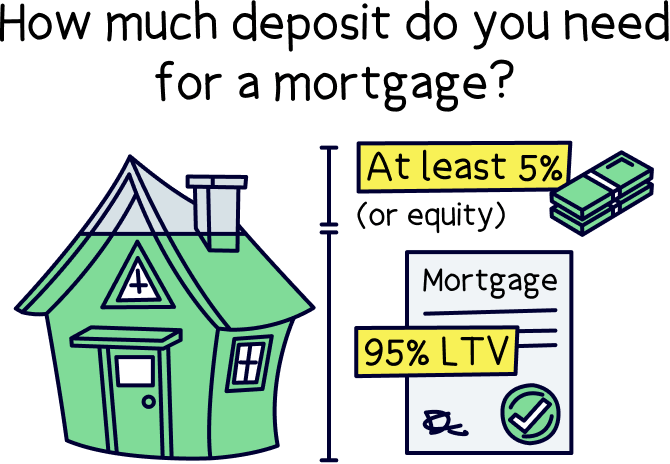

Most lenders will want you to pay a deposit that’s at least 5% of the value of the house you’re buying. For example, if you’re buying a £200,000 house, you’ll normally need a deposit of at least £10,000 (5% of 200,000 is 10,000).

Got your sights on buying a house? Wondering how many extra shifts at work you’ll need to save a deposit big enough? You’re in the right place!

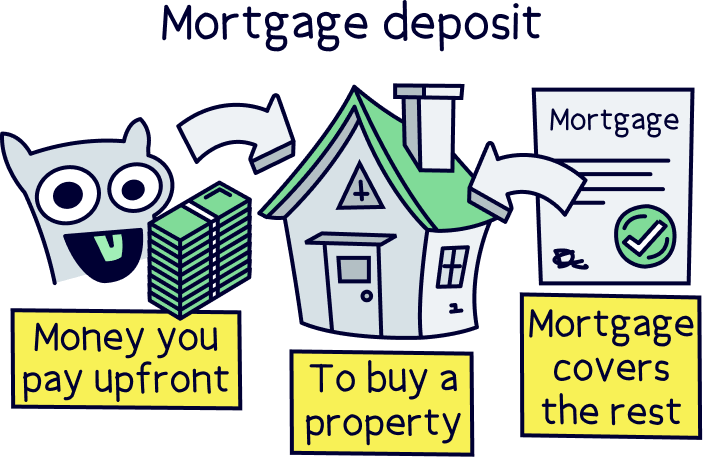

A mortgage deposit is a sum of money that you pay upfront when you buy a property. In other words, it’s the part of your property’s price that isn’t covered by your mortgage. Here, we’ll look at how much deposit you need to buy a house, to help you on your way to becoming a homeowner.

Every mortgage lender is different (mortgage lenders are the people that give out mortgages). So, they’ll all have different requirements when it comes to how big a mortgage they’ll give you and how much of a deposit they’ll want you to pay.

That said, most lenders won’t let you borrow more than 95% of the value of the house you’re buying. That means you’ll need to pay at least 5% as a deposit.

This is known as a 95% loan-to-value ratio (LTV) as they’re loaning you 95% of the house’s value. The rest, you’ll need to fork out yourself.

Struggling to get your head around what that means? Let’s look at an example.

Say you want to buy a house worth £200,000. Most lenders will let you borrow a maximum of £190,000 (95% of 200,000 is 190,000). That means you’ll need to pay at least the remaining £10,000 as a deposit.

Now let’s imagine you’re buying a house that costs £500,000. In this case, you’ll need to save for a minimum deposit of around £25,000. This is because your lender will still normally only give you a mortgage for 95% of the property price, which in this case comes to £475,000. Your deposit will need to make up the difference.

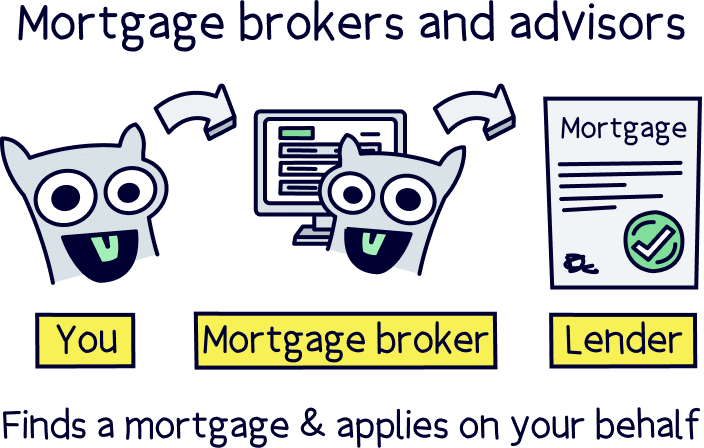

If you have at least a 5% deposit, we recommend you get in touch with a mortgage broker (also known as a mortgage advisor). They’re these amazing people who know all about mortgages and can help you get the best deal – we’ll tell you more about them in a bit.

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage. You'll also get 50% off their fee with Nuts About Money. How great is that?

Okay, okay, so we know we said that you only need to save 5% of your house’s value for a deposit. But that doesn’t mean you should only save up 5%. Ultimately, the more deposit you can put down the better.

Want to know why? Here’s the lowdown.

This one might sound obvious, but the more you borrow, the bigger your monthly repayments will be.

Firstly, if you borrow more, you’ll have more to pay back (that’s the obvious bit!). But secondly, borrowing more also means paying more interest – that’s a fee lenders charge you for the pleasure of borrowing their money.

Your interest will be calculated as a percentage of the amount of money you owe your lender each year. If you pay a bigger deposit, you’ll owe your lender less which means you’ll have less interest to pay.

Not all lenders will want to give out mortgages that are as big as 95%. In fact, a lot of lenders in the UK stopped offering low-deposit mortgages when the Covid-19 pandemic hit, as they were worried about people getting mortgages that they wouldn’t be able to afford to pay back.

Things are a bit better now as the government created something called the mortgage guarantee scheme. The scheme aims to protect lenders who offer 95% mortgages in order to encourage more lenders to do so. It’s set to last until the end of 2022.

However, not all lenders are part of the scheme and many will only lend you around 90% of your house’s value. This means there’ll be more lenders to choose from if you can pay at least a 10% deposit.

So, why is it a good thing to have a bigger choice of lenders?

Well, the more choice you have, the more likely it is you’ll be able to find a cheaper deal. Get in!

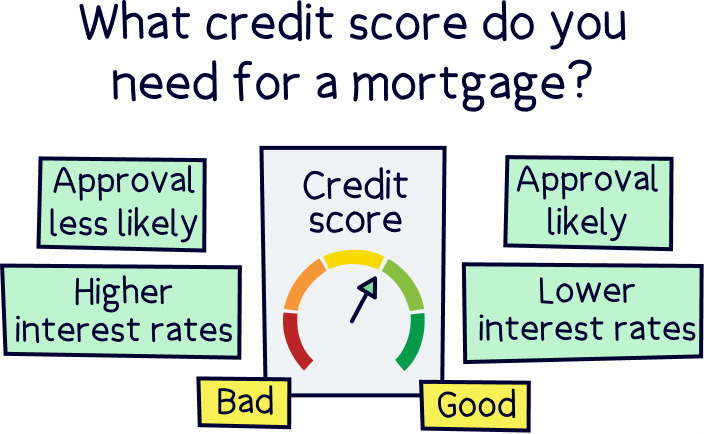

On top of that, the more lenders there are to choose from, the more likely it is that there’ll be one who’s happy to lend to you. This is especially the case if you’re self-employed or you have a bad credit score (a score lenders use to see how good you’ve been with money in the past), as you’ll usually have a smaller pool of lenders to choose from already.

We all want to get the cheapest rates possible, right? Well, lenders tend to reserve their best rates for people who pay bigger deposits. This is all to do with your lender’s risk.

Basically, if you consistently don’t pay your mortgage each month, your lender might want to seize your house and sell it so that they can get their money back (don’t worry, this is the absolute last resort!). If your mortgage covers less of your home’s value, it’s more likely your lender will be able to sell your home for enough to get their full loan back.

In a nutshell, a big deposit is safer from your lender’s point of view, so will come with better rates.

The size of your deposit isn’t the only thing that lenders will look at when they’re deciding whether or not to give you a mortgage. They’ll also look at things like your income, expenses, credit score and job.

When they’re umming and ahhing about whether or not to accept you, lenders will balance up all of these factors, including your deposit, to decide how likely you are to be able to meet your monthly repayments – this is known as affordability.

Putting down a bigger deposit will help give them confidence you can afford the repayments because the repayments will be lower. But it could be particularly helpful if your application’s not as strong as it could be on other fronts.

Remember how we said that lenders might be less happy to lend to you if you’re self-employed or you have a bad credit score? A bigger deposit might help to ease their worries and make it easier for you to get approved in cases where you might otherwise struggle.

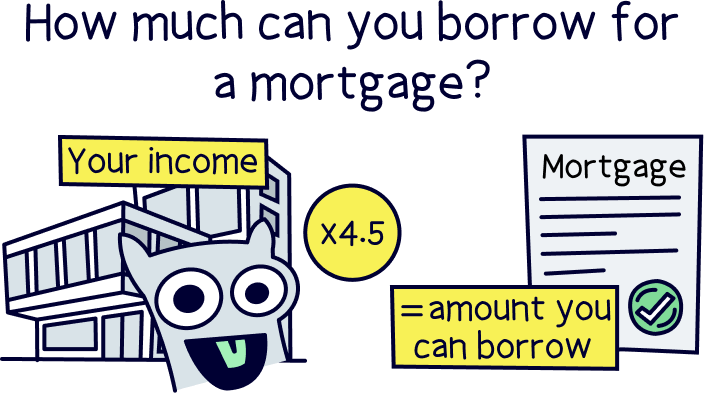

Lenders will normally only let you borrow around 4.5 x your yearly income. This is all to do with that ‘affordability’ thing we just told you about. Lenders won’t want to let you borrow more than that because they’ll be worried you won’t earn enough to keep up with your monthly repayments.]

Say you earn £20,000 per year. You’ll normally be able to borrow around £90,000 (4.5 x 20,000 = 90,000). With a 5% deposit, that means you’d be able to buy a house worth a maximum of £95,000 (technically it’s just under, but we’re rounding up for ease).

However, say you put down £10,000 as a deposit instead. You could now afford a property that’s worth £100,000 (£90,000 + £10,000 = £100,000). This is because you’re topping up the loan from your lender (£90,000) with more money.

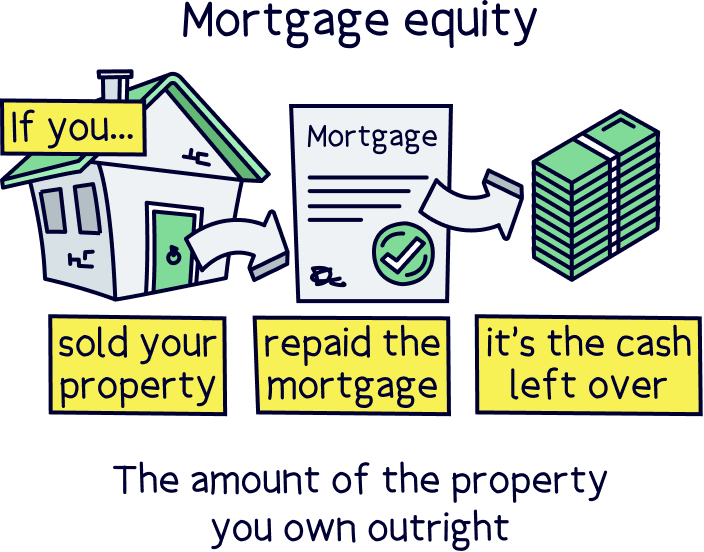

The amount of your home that you own outright is called your equity. Think of it as the value of your home that would go straight back into your pocket if you sold it, rather than towards paying off your mortgage lender.

The smaller your deposit, the less equity you’ll have in your property. This could be a problem if house prices in your area go down as you could end up with negative equity.

Negative equity is when you owe your mortgage lender more than your property is worth. It can make things really hard if you want to sell or remortgage in future (remortgaging is when you swap your current mortgage for a new one and can save you a lot of money in the long run).

Tembo will find your best deal, fast, all with award-winning service.

Theoretically, yes, you can get a 100% mortgage. But in practice, this isn’t really a thing at the moment (and they’ve always been pretty rare anyway!).

Let’s start at the very beginning.

A 100% mortgage is a mortgage where your lender agrees to lend you the whole value of your property. That means you don’t have to pay a deposit at all. Sounds pretty dreamy, right?!

Although technically any kind of mortgage could be a 100% mortgage, the only ones available tend to be guarantor mortgages. That’s where you get someone else (normally a family member) to promise to pay your mortgage repayments if you can’t.

Usually, they’ll have to put forward some savings or their own home as security. That means that, in the worst-case scenario that neither of you can keep up with the repayments, their savings or property could get taken. So, becoming someone’s guarantor on a 100% mortgage is a pretty big deal and not something your family member should jump into without thinking about carefully.

100% mortgages can also be problematic because if your home goes down in value even just a little bit, you’ll immediately be in negative equity (remember, that’s when you owe your lender more than the value of your house). This isn’t a situation you want to be in as it can make it really hard to move house or remortgage in the future.

To cut a long story short, there are very few 100% mortgages out there so it’s pretty unlikely you’d be able to get your hands on one. And even if you could, it’s not really something we’d recommend as the risks are high!

If you’ve been saving but you’re not sure you’ve got enough money for a deposit, don’t worry. The easiest way to get an idea is to look at house prices in your area using an app like Rightmove or Zoopla. Then, ask yourself whether you’ve managed to save 5% of the purchase price.

If you have, the chances are you have a big enough deposit. Congrats! Now’s the time to get in touch with one of those awesome people called mortgage brokers that we told you about earlier.

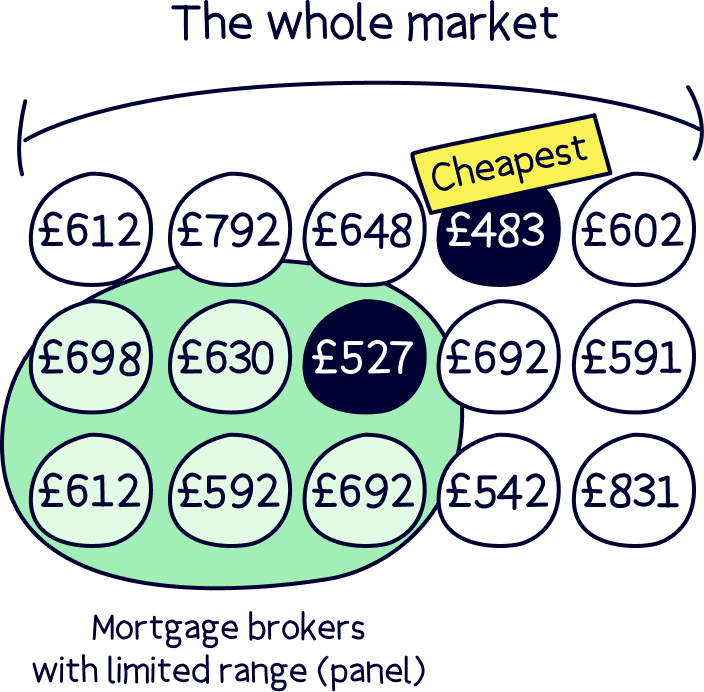

A mortgage broker will be able to take a look at your situation and give you advice about how to get a mortgage, how much of a deposit you should pay and where the cheapest deals are.

If you go for a whole-of-market mortgage broker (which we’d always advise you to do) they’ll be able to compare all the different mortgages from all the different lenders before helping you to choose the best one for you. Oh, and when you’ve found the perfect house to buy, they’ll even sort out the whole mortgage application for you.

That’s right, you just sit back and twiddle your thumbs while they toil away on your behalf. Easy!

Need help finding one of these superheroes?! Check out Tembo¹, they've got award-winning service, and will find your best deal. Plus, you'll get 50% off their fee with Nuts About Money.

Yes! Let’s face it, saving for a deposit isn’t easy. If you’re struggling, you’ll be pleased to hear there is some help available.

If you’re a first-time buyer, we have some good news. You might be able to qualify for a Help to Buy Equity Loan. This is where, on top of your mortgage, you can get a loan from the government of up to 20% of your property’s purchase price (or, if you’re buying in London, up to 40%).

This scheme is specially designed for people who are struggling to get a mortgage because they can’t save up a deposit big enough. Woohoo!

Just bear in mind that to qualify, you’ll have to buy a new-build property from a developer that’s registered with the scheme (and new-build properties tend to be more expensive to buy which is a bit of a pain!). Your new home will also need to be below a certain price, but the exact amount will vary depending on where you’re buying.

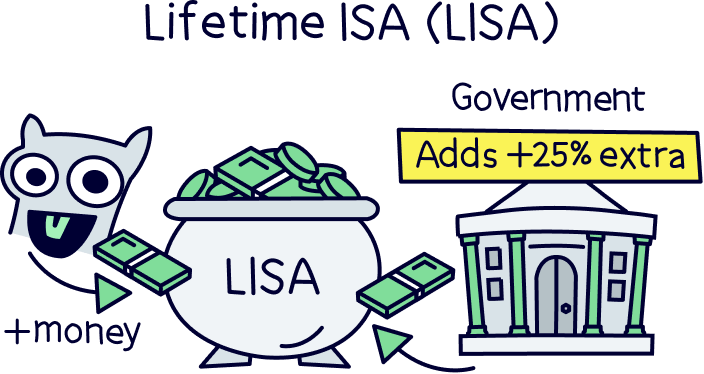

A Lifetime ISA is the best kind of bank account. It’s a savings account where the government boosts any savings you put in there to help you buy your first home (or to tide you over later in life).

You can put £4,000 into your account each year and the government will then add a sum worth 25% of the amount you put in. Kerching!

To qualify for the help, you’ll need to make your first payment into the account before you’re 40 and you won’t be able to add to it anymore after you turn 50.

You’ll also only benefit from the government bonus if you use the money for what it’s designed for. If you use it for anything else, you’ll have to pay a hefty 25% withdrawal charge – which means you’ll actually lose more than the bonus you get! In other words, use the money carefully.

This one isn’t a government scheme, but it is a great way to boost your savings and affordability. A joint mortgage involves teaming up with someone else (usually a friend or family member) to buy a home together.

By teaming up together you could combine your savings to afford a much bigger deposit. Plus, you’d be likely to qualify for a bigger mortgage as your lender would take into account both your incomes when considering how much you can afford to borrow.

Remember how we said that you’ll normally be able to borrow around 4.5 x your yearly income? Well, if you’re getting a joint mortgage, you’ll be able to add both your salaries together and then multiply that number by 4.5.

Say, for example, that you earn £20,000 per year and your friend or family member earns £20,000 per year too. Together, you earn £40,000, which means you could probably borrow £180,000 (40,000 x 4.5 = 180,000). This is double the £90,000 you could borrow alone.

If you’ve been squirrelling money away for a mortgage, the first thing to do is chat with a mortgage broker.

They’ll look at your deposit as well as a whole load of other details (like your income and expenses) to tell you how much you can borrow and where the best deals are. Plus they’ll make life super easy by sorting out your mortgage application for you.

Not sure where to find a great broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage. Plus, you'll get 50% off their fee with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.