Article contents

Teaming up to buy a house with a partner, family member or friend could be a great way to get on the property ladder for the first time or to afford that dream property you’ve got your eye on.

Thinking about getting a mortgage with someone else? Whether you’re toying with the idea of buying a home with your partner, or you’re umming and ahhing about whether or not to team up with friends or family, here's everything you need to know about joint mortgages.

First things first, a joint mortgage is a mortgage that’s shared between two or more people. In other words, while a standard mortgage is a loan that lets you buy a property by yourself, a joint mortgage is a loan that lets you buy a property with someone else.

So, why would you want one?

Well, by teaming up with someone else, you’ll probably be able to get a bigger mortgage than you could on your own (we’ll take a look at why in a bit). Plus, if you’ve both been saving, you can put down a bigger deposit by pooling your savings, helping you to afford your dream property and potentially get a lower interest rate on your mortgage.

Nuts About Money tip: get an idea of monthly mortgage repayments by comparing current mortgage rates with our mortgage comparison table.

Note: be careful because when you get a mortgage with someone else, you’ll be jointly responsible for paying your monthly mortgage repayments. In other words, if the person you’re getting a mortgage with doesn’t pay their share, you will have to pay it!

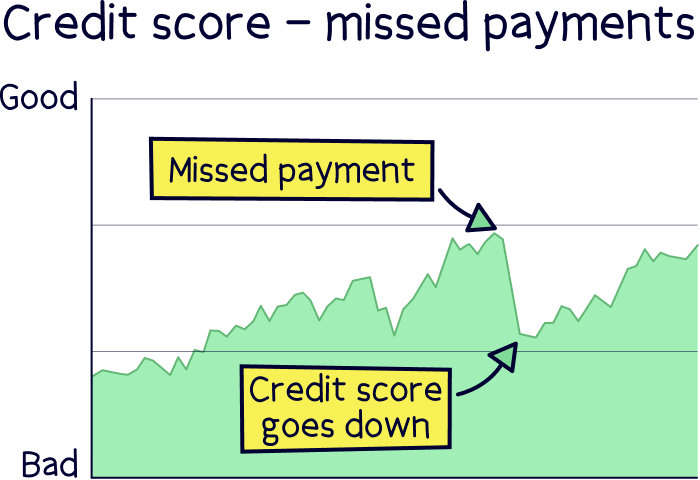

Not only that, but getting a mortgage together will link you financially. Basically, if they get into any financial trouble, it might show up on your credit score (a score that’s used to show how good you are with money). This means that lenders (the people that give out mortgages) might be less happy to give you another mortgage or loan in the future.

All this to say that you shouldn’t just get a joint mortgage with any random person you meet in the street. Instead, you’ll need to do it with someone you trust. Which brings us onto…

Tembo will find the best joint mortgage deal, fast, all with award-winning service.

Most people who take out joint mortgages are couples (married couples, civil partners or just… couples!). However, any singletons out there will be relieved to hear that you don’t have to be in a relationship to get a joint mortgage. In fact, anyone can submit a joint mortgage application.

A few examples of people who might get a joint mortgage are:

Many lenders will only let you have two people on a joint mortgage, but if you want to take out a mortgage as a group, that’s totally doable too. Some lenders will let you have three or even four people on there.

That said, just because anyone can apply for a joint mortgage, that doesn’t mean you’ll definitely be able to get one.

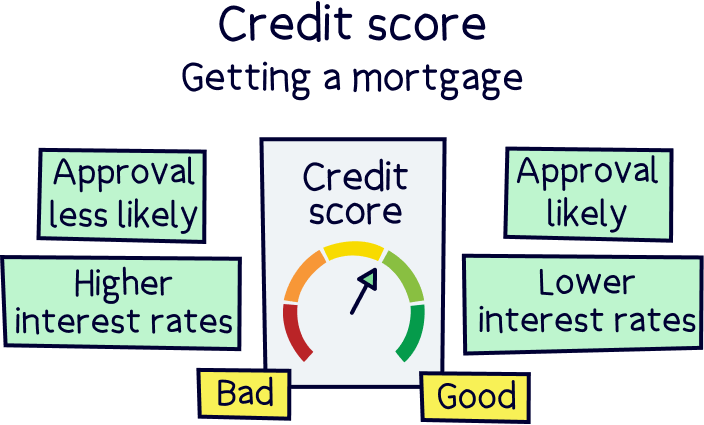

First, you’ll want to make sure that nobody you’re applying with has a bad credit score. If they do, it means they’ve probably had trouble with money in the past. And that will normally mean that most lenders won’t be willing to lend to them.

Second, we hate to break it to you, but if you or someone you’re applying with is above a certain age, you’re probably going to struggle to get approved for a joint mortgage. We know age is just a number. But unfortunately, lenders have maximum age limits (normally between 70 and 75) because, at this point, you’re likely to retire and won't have a salary to pay the mortgage.

Basically, you’ll want to make sure that everyone you’re applying with is going to be below your lender’s age limit by the time your mortgage finishes to give yourself the best possible chance of getting approved.

This doesn’t necessarily mean abandoning the idea of getting a mortgage with someone older completely. You could just take out a shorter mortgage so that it’s finished before anyone passes the age limit. Or, if a parent or grandparent is trying to help you get on the property ladder, you could look at making them a guarantor instead, which is where they help you get a mortgage by agreeing to be responsible for making the monthly repayments if you can’t (explained below).

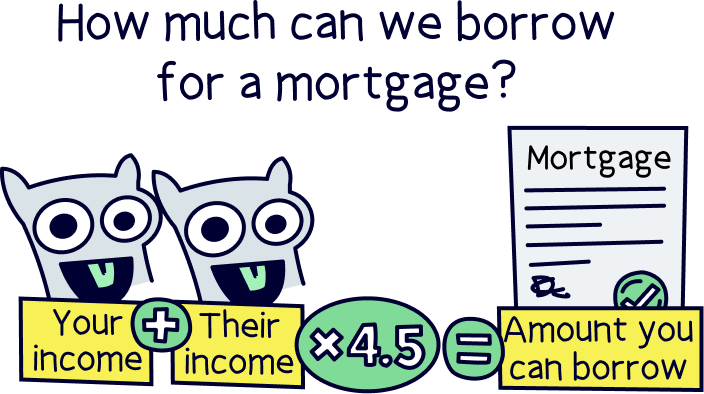

Okay, so here’s the good news. Normally, you’ll be able to borrow more if you apply for a joint mortgage than you will if you get a mortgage alone.

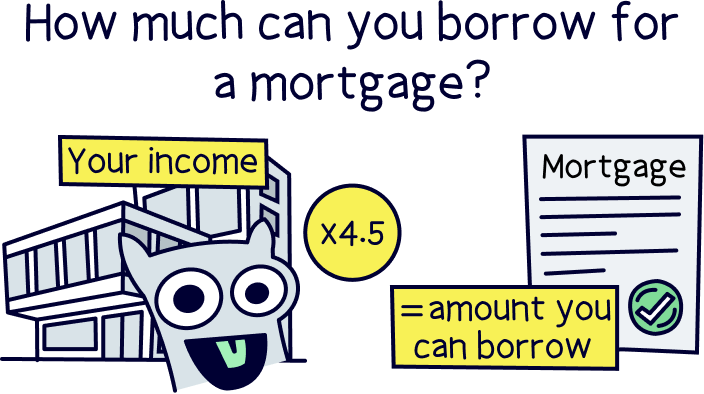

Why? Well, one of the main things lenders will look at when they’re deciding how much to lend to you is your salary. Most lenders will let you borrow around 4.5 times your yearly income.

But if you get a mortgage with someone else, you’ll be able to combine your salaries to borrow more.

Confused? Let’s say you earn £20,000 per year. That means on your own, you’d probably be able to borrow around £90,000 (£20,000 x 4.5 = £90,000).

Now let’s imagine your friend or partner also earns £20,000 per year. That means you jointly earn £40,000 each year. Together, you’d probably be able to borrow around £180,000 (£40,000 x 4.5 = £180,000). Not bad, eh?

However, if there are more than two of you getting a joint mortgage, lenders will typically only look at the income of the two highest earners. So, sadly, you won’t be able to add together all of your incomes to get one massive mortgage (you will be able to pitch in together for the deposit and the mortgage repayments though).

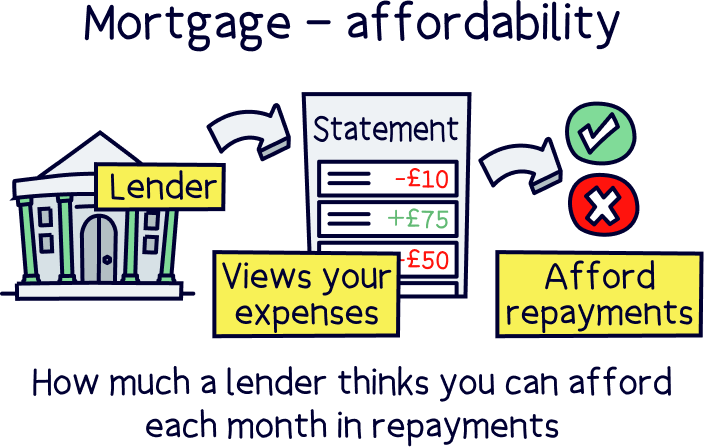

Plus, bear in mind that your income isn’t the only thing that lenders will look at. They’ll also check things like how expensive your bills are and what else you spend your money on each month before coming to a decision about how much to let you borrow. This is all about making sure you’ll be able to afford your monthly repayments.

So, try to reduce your spending before submitting your joint mortgage application. Things like expensive clothes or a new car and try not to take out any loans until after you’ve been approved.

Right, now for the scary bit. When you take out a joint mortgage with someone, you’re jointly responsible for paying the mortgage back. That means that if one of you can’t afford to pay the mortgage, the rest of you will need to pay up. Eek!

You’re also jointly responsible for making any decisions about your mortgage and the property. In other words, if you want to make any changes, like remortgaging or selling up, you’ll all have to agree. Don’t worry, that doesn’t mean that joint mortgages aren’t a good idea. It just means you’ll need to really trust whoever you get a mortgage with.

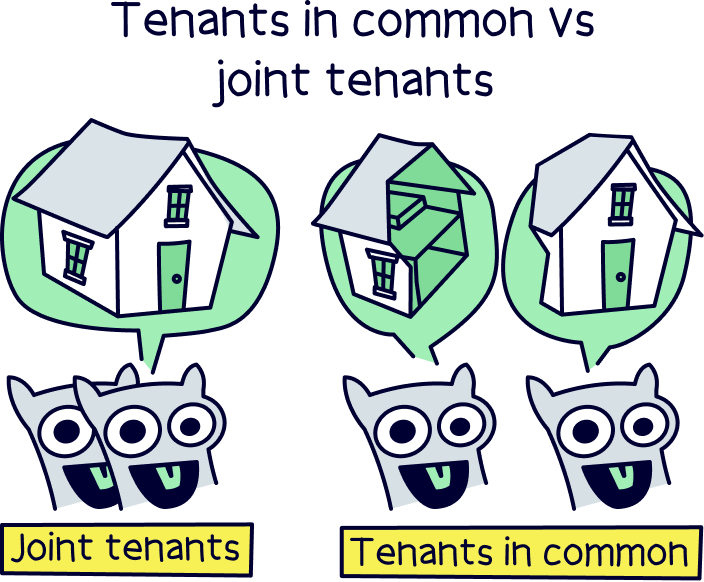

There are two main ways that you can jointly own a property:

Joint tenancy is where everyone who owns the property jointly owns 100% of it. Basically, the law will see you all as a single owner, and you’ll all have equal rights on everything to do with the property.

Here are the main things to bear in mind if you’re considering joint tenancy.

This is the kind of joint ownership that’s normally chosen by long-term partners or married couples.

Taking out a mortgage as tenants in common means that everyone who owns the property has their own individual shares in it, rather than owning the whole thing jointly.

For example, if there are two of you, instead of you both owning 100%, you could take 50% each. Or, you could split the shares differently, such as giving one of you 55% and the other 45%. This way, if you sold the property, one of you would get 55% of the profits and the other would get 45%.

Here are the main things to bear in mind if you’re thinking about becoming tenants in common.

This kind of joint ownership protects you a bit more financially, as it means if you pay more for the property (like putting down more of the deposit than your partner), you could take more shares and get more of the profits when it’s sold. So, it’s often chosen by people who’re buying a property with short-term partners, friends or family members.

Joint ownership mortgages can help you to get on the property ladder for the first time. They can also be a great way to team up with someone else to buy that dream property you just couldn’t afford alone! But they’re not for everyone.

So, should you get one? Only you can answer that question for sure, but these pros and cons might help.

Are you considering getting a joint mortgage so that your parents (or relatives) can help you get on the property ladder? Are you going to be the only one actually living in the property?

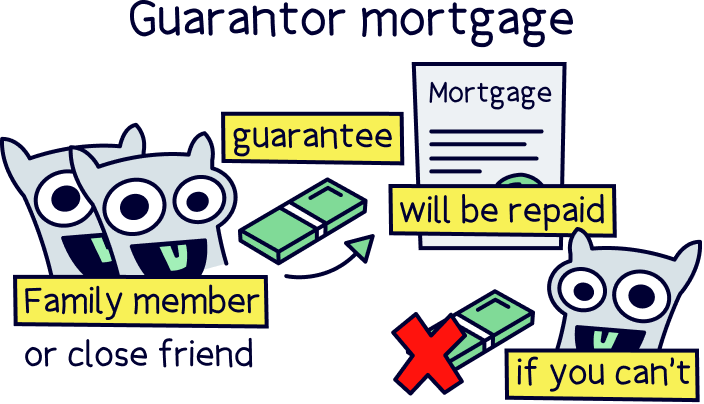

In this case, a joint mortgage isn’t your only option. A guarantor mortgage is where a friend or family member helps you to get a mortgage by agreeing to keep up with your monthly mortgage repayments if you can’t.

Imagine that your lender is umming and ahhing about whether or not to give you a mortgage. Maybe you’re self-employed (which means you don’t have a regular salary coming into your bank account). Or maybe you’re hoping to get a student mortgage and you haven’t yet had time to build up a decent credit score. By getting a friend or family member to act as guarantor, you can ease the lender’s worries as you’ll have someone (usually older, more experienced and in a better financial position) agreeing to pay your mortgage if you can’t.

So, which is better? Well, it depends on what you want.

The main difference is that, with a guarantor mortgage, your guarantor won’t actually own any of the property. So, even though they have to pay up if you stop paying your mortgage, they won’t get any of the potential profits if your property gets sold. On the other hand, with a joint mortgage, you’ll jointly own the property and will both get a share of the potential profits when it gets sold.

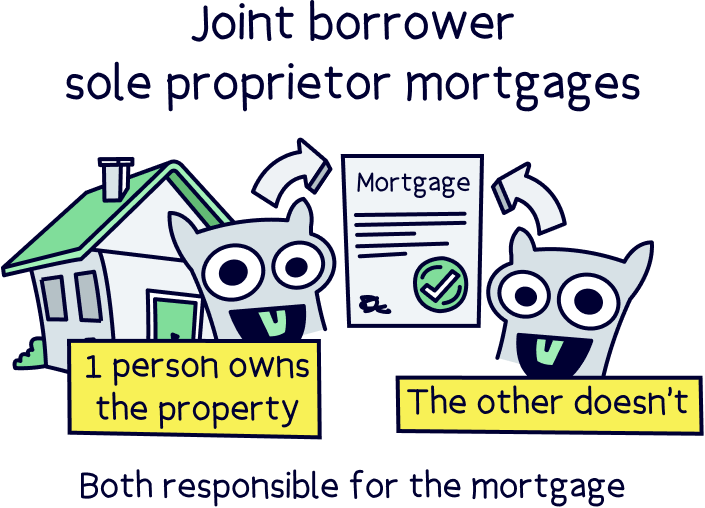

To make things even more complicated, there’s also something called a joint borrower sole proprietor mortgage. Just like a guarantor mortgage, with a joint borrower sole proprietor mortgage, your parent or family member won’t own any of the property. But like a joint mortgage, they’re responsible for contributing to your mortgage repayments from the outset. This is different from a guarantor mortgage where your parent or family member is essentially just a plan B, there if things go wrong.

Before you take the plunge and get a joint mortgage, it’s important to consider what you would do if you separated.

It’s not exactly fun to think about, but what happens if you buy a home with a partner and end up going through a breakup or divorce? Or if you pitch in with friends, what happens if one of you decides they want to move out and buy a home on their own?

Ultimately, it pays to think ahead and have an action plan. Here are some of the options open to you if you decide to split with the person (or people) you have a joint mortgage with.

Okay, so this one’s probably the easiest solution if you decide to bring your joint mortgage to an end. By selling your property, you can use the money from the sale to pay off your mortgage and then split any profits between you.

Remember how we were banging on about the differences between buying a property as joint tenants versus tenants in common? Well, how the money from the property sale is split will depend on which of those you chose.

If you’re joint tenants, any profits will normally be split evenly between you. But if you’re tenants in common, the profits will be split based on how many shares you each decided to take when you bought your home. In other words, if you own 60% of the property and your partner owns 40%, you’ll take 60% of the profits when it’s sold.

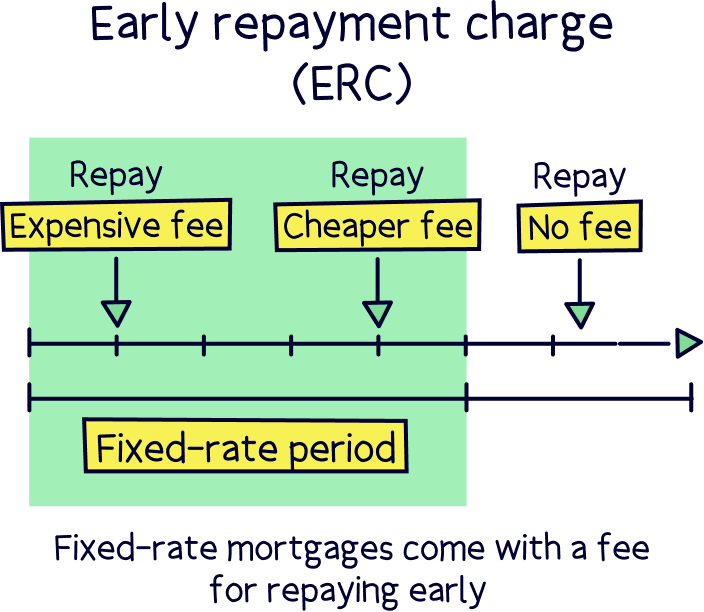

Just watch out because if you’re still in the introductory period of a fixed-term mortgage, you might have to pay an early repayment charge for leaving early. Depending on how early you’re leaving your mortgage (and how big your mortgage is), this could add up to thousands of pounds.

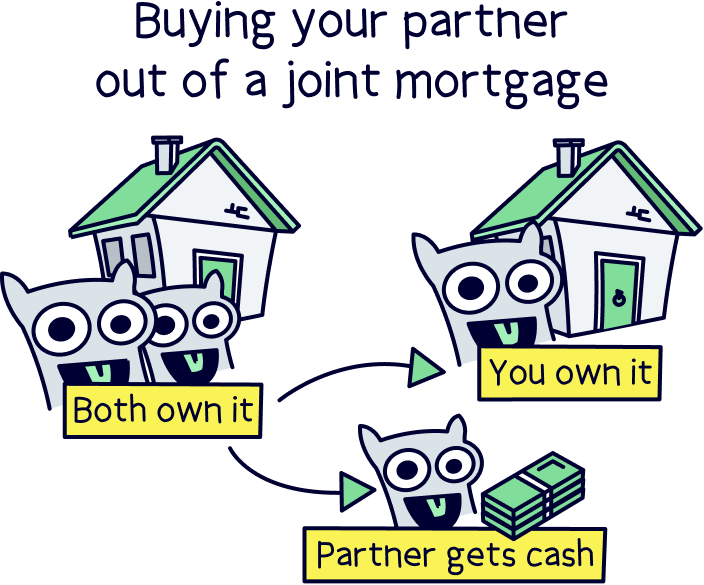

If you want to carry on living in your home, you could consider buying your partner out. Or, if they want to continue living there, they could consider buying you out.

Buying someone out of a property is what it’s called when one of you takes ownership over the other person’s share of the home and you become solely responsible for paying the mortgage. To do this, you’ll need to work out the value of your partner’s share of the property and literally buy it off them.

Let’s face it: not many of us have the cash lying around to be able to afford to do that. So, you’ll probably need to remortgage your property to release equity (cash). You can then use the funds released to pay for your partner’s share.

However, for this to work, you’ll need to prove to your lender that you can afford the mortgage repayments on your own. Check out our guide to buying a partner out of a joint mortgage for the full lowdown.

Just because one of you has decided to move out of the property, that doesn’t mean you can’t continue to jointly own it.

As long as, between you, you carry on paying the mortgage, it makes no difference whether or not you’re both living there. Ultimately, when the property gets sold, you’ll still both get a share of the profits.

Leaving the mortgage how it is could be a good solution if you both still want to own a property but you just don’t want to live there together. It can also be a good compromise if you own your property with a long-term partner and you’re going through a breakup or divorce, especially if there are children involved. This way, one of you can carry on living there with your children.

Alternatively, if you want to buy your partner out but you can’t afford to do so completely, your partner could continue to own a small stake in the property – as long as they agree, of course! You could then continue saving and buy your partner out fully later down the line. Or, they could just continue to own a small percentage of the property indefinitely and then get a small percentage of the profits when you eventually sell it.

Do you live in England or Wales? Are you bringing your joint mortgage to an end because you’re going through a divorce?

If so, you may be eligible for a Mesher or Martin order. These are court orders that allow a spouse to continue living in the property for a set period of time. Depending on the type of order, it means that the home can’t be sold until a specific event happens. This might be after a certain number of years, until the couple’s youngest child turns 18 or anything else that the court rules.

If this sounds good to you, you’re best off chatting to a solicitor to see if you can start the process.

Fancy applying for a joint mortgage? Well, the process is exactly the same as applying for a mortgage on your own. The only difference is you’ll need to do it with someone else!

It might sound obvious, but this means you’ll have to decide a lot of things together: what kind of mortgages you’re interested in, what lenders are best for you, how many years you want your mortgage to last for (known as your mortgage term)… we could go on!

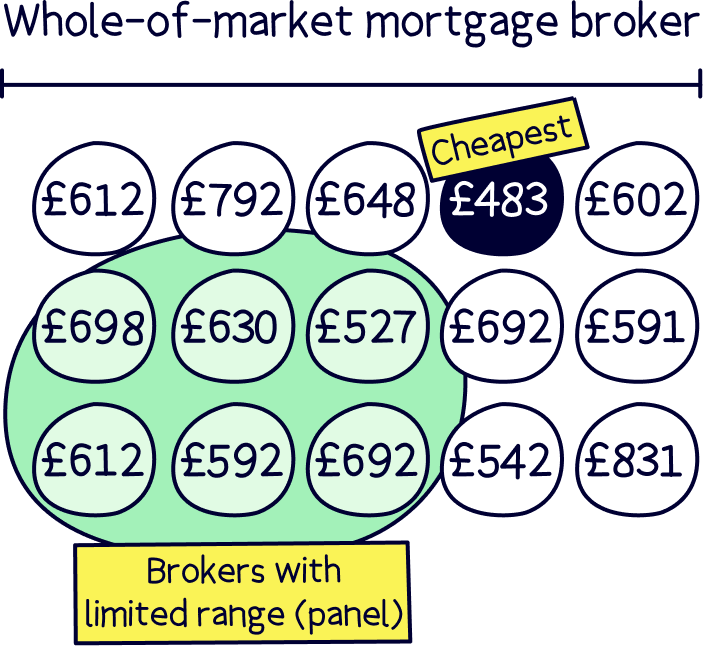

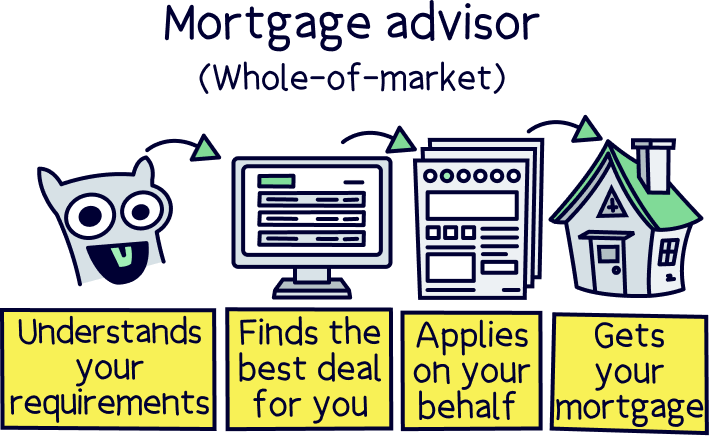

We’d recommend talking to a ‘whole-of-market’ mortgage broker (also known as a mortgage advisor) as they’ll be able to search through all the different mortgages being offered by lots of different lenders, to help you find the best deal for you.

They’ll be able to give you tailored advice about how best to protect yourself going into a joint mortgage too.

Not sure where to find a good mortgage broker? We've listed a couple below or check out our recommended mortgage brokers.

Get 50% off the standard fee

Tembo is an all-round amazing mortgage broker, in fact, they're award-winning, and not just online.

They can help with pretty much every mortgage out there, from buying a home to switching deals, and on top of that, have unique options to increase your borrowing such as an Income Boost¹ and Deposit Boost¹.

They'll handle the whole mortgage for you too, and the service is great.

Habito will find the best mortgage for you, all for free, and with great service. But better than that, if you’re buying a home, they’ll handle the whole process for you – that’s the legal work and survey, and everything else. It’s a huge stress and time saver, and comes at a great price.

Habito is run by Monzo, which is a very large and successful modern bank (often called a mobile bank).

Tembo will find the best joint mortgage deal, fast, all with award-winning service.

It’s also a good idea to get a deed of trust drawn up by your conveyancing solicitor when you start the process of buying that dream home (your conveyancing solicitor is the solicitor you hire to sort out all the legal stuff for you). A deed of trust is a legal agreement that will lay out exactly what should happen if the worst occurs and you split, disagree or one of you stops paying your share of the mortgage repayments.

It might sound like overkill now, but it’s a great way to give yourself that all-important peace of mind, just in case. That way, you can relax and focus on enjoying your new home, without having to give any of that boring stuff another thought.

So, what do you think? Time to start property hunting with your partner, friend or favourite family member?!

If pooling your resources to get onto the property ladder – or to be able to afford your dream home – sounds like bliss to you, what are you waiting for? The first step is to find that special person (or people) to buy a property with and then get a great mortgage broker to help with your joint mortgage application. Before you know it, you’ll be sat on the floor of your new pad with a bottle of bubbly on the go and boxes all around you. Good luck!

Tembo will find the best joint mortgage deal, fast, all with award-winning service.

Tembo will find the best joint mortgage deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find the best joint mortgage deal, fast, all with award-winning service.