Article contents

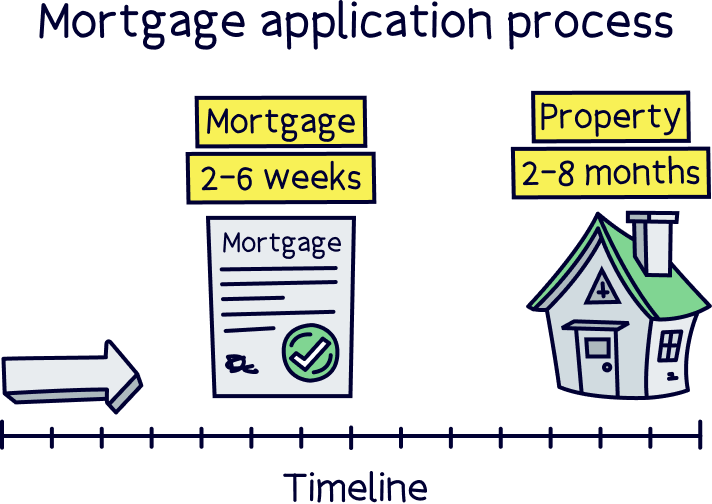

The UK mortgage application process takes around 2-6 weeks, but there are lots of other steps. First you’ll need to get a mortgage in principle, then apply for the mortgage and get a property valuation. Once you’ve received your mortgage offer you can exchange contracts and finally ‘complete’ where the house sale goes through.

Set your heart on buying a home? You probably want to get things moving as quickly as possible. But when it comes to getting a mortgage, there’s a ton of waiting involved. Our mortgage application process timeline will give you a realistic idea of what you can expect.

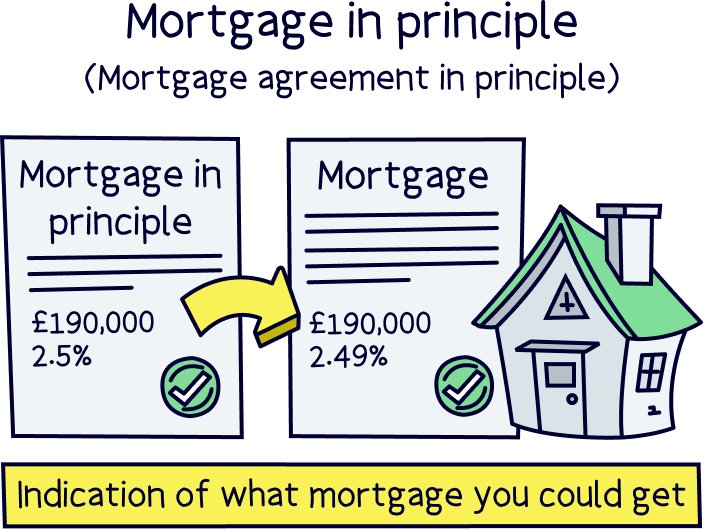

For most buyers, the first step to buying a home is getting a mortgage in principle. This part often comes before you actually view any houses!

A mortgage in principle, also known as a ‘mortgage agreement in principle,’ is an official document from a mortgage lender confirming that, from what they know about you so far, they think you’d get accepted for a mortgage. It also says how big that mortgage would be.

Although you don’t have to get a mortgage in principle to go house hunting, it helps to have one. That’s because...

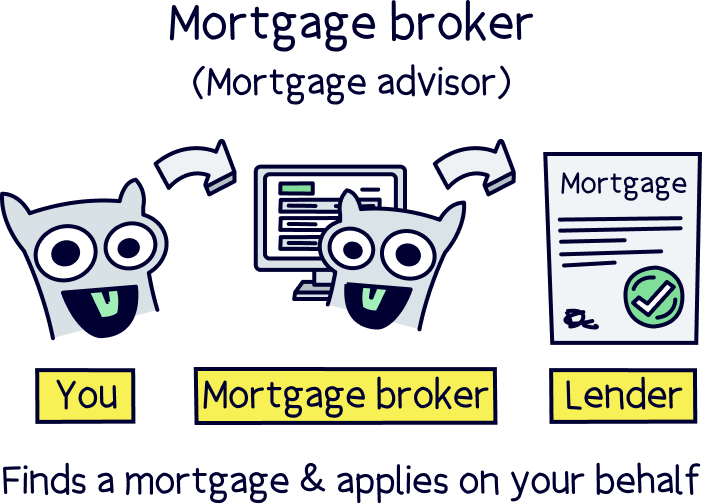

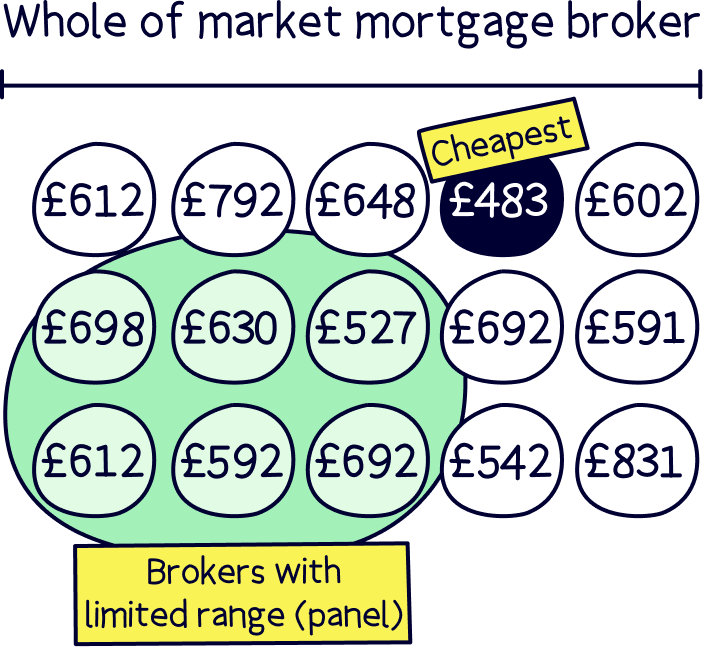

The easiest way to get a mortgage in principle is to use an independent mortgage broker. They’ll be able to search the whole market for the best lender for you, and they’ll even sort out the application!

We highly recommend using a mortgage advisor. Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. Or view all our recommended mortgage brokers.

You’ll need to dig out some documents and info, like bank statements and previous addresses, but once you’ve found the info they need, they could get you a mortgage in principle in as little as 1 hour!

Nuts About Money tip: view current mortgage rates with our mortgage comparison.

Tembo will find your best deal, fast, all with award-winning service.

Now’s when you get to trawl the newest listings on Rightmove and snoop around all the prettiest houses in your budget! In other words, it’s time to find your dream home and put an offer in on it.

It’s hard to put a timescale on this as every person and every house hunt is different. After all, some people fall in love with the first property they see, while others view hundreds before finding the right one. It’s all about getting that feeling!

That said, most mortgage-in-principles will only last for 60-90 days. So, ideally, you’d make an offer on a property within that time. It helps if you’ve been keeping an eye on apps like Rightmove, and your local estate agents window before this, so you have a clear idea of what you want and you’re ready to act when the right property comes along.

If you can’t find a property you like within that time, don’t panic! The worst thing you can do is buy something just because you’re feeling some time pressure.

If your mortgage in principle expires, it’s not the end of the world. You can simply apply for a new one. Or, you could get an offer accepted without one and go straight in with the full mortgage application instead. You have options!

Once you’ve had an offer accepted on a property, it’s time to go ahead and apply for a mortgage.

If we assume you worked with a mortgage broker to get a mortgage in principle, this is super quick and easy. All you’ll have to do is let them know you’re ready to turn your mortgage in principle into an actual mortgage offer. They’ll already have all your details to hand, so you can just leave them to it!

If you didn’t get a mortgage in principle in the first place, that’s okay. You can just apply for a full mortgage offer straight away. We’d still recommend that you find a 'whole-of-market' mortgage broker as they’ll be able to recommend the best lender and deal for you. Plus, they’ll fill in the application and handle the whole process from start to finish. Not only does this give you the best possible chance of being approved for a mortgage, but it means you’ll have a whole lot less stress to deal with too!

Not sure what mortgage broker to use? Here's a couple of our favourites, or view all our recommended mortgage brokers.

Get 50% off the standard fee

Tembo is an all-round amazing mortgage broker, in fact, they're award-winning, and not just online.

They can help with pretty much every mortgage out there, from buying a home to switching deals, and on top of that, have unique options to increase your borrowing such as an Income Boost¹ and Deposit Boost¹.

They'll handle the whole mortgage for you too, and the service is great.

Habito will find the best mortgage for you, all for free, and with great service. But better than that, if you’re buying a home, they’ll handle the whole process for you – that’s the legal work and survey, and everything else. It’s a huge stress and time saver, and comes at a great price.

Habito is run by Monzo, which is a very large and successful modern bank (often called a mobile bank).

Tembo will find your best deal, fast, all with award-winning service.

If you want to know more about applying for a mortgage check out our guide to how long a mortgage application takes for the full lowdown, and what happens after a mortgage is issued for what comes next.

A mortgage valuation is when your mortgage lender checks how much they think the property you’re buying is worth. Basically, they want to make sure they’re not lending you too much money. Makes sense, right?!

The process of making these checks is called a ‘valuation survey.’ Sometimes your lender will send someone into the property you’re buying to carry out the survey in-person. Or, sometimes they’ll simply just get someone to drive past and look at it from the outside, which is known as a ‘kerbside valuation.’

Nowadays though, they’ll often just do a ‘desktop valuation.’ This is where the whole thing is carried out on a computer, using data such as recent sold prices. Yep, that’s right. They don’t even look at the property in real life!

Usually, your mortgage valuation will be done and dusted around 1-2 weeks after you hand in your application. You might be asked to pay a fee for it (this could be anywhere from £150 to £1,500) but other than that, you’ll just need to sit back, relax and wait for the results to come in.

That said, you’ll probably also want to get your own, more detailed survey carried out on the property in the meantime. This should flag up any costly issues that you didn’t spot initially, like damp or structural issues, so spending money on a survey can be worth it in the long run. Plus, if you find major issues, you can always ask the seller for a discount on the agreed price!

Nuts About Money tip: Just make sure you use a qualified and registered surveyor – you can find one online with the Royal Institution of Chartered Surveyors (RICS) or Residential Property Surveyors Association (RPSA).

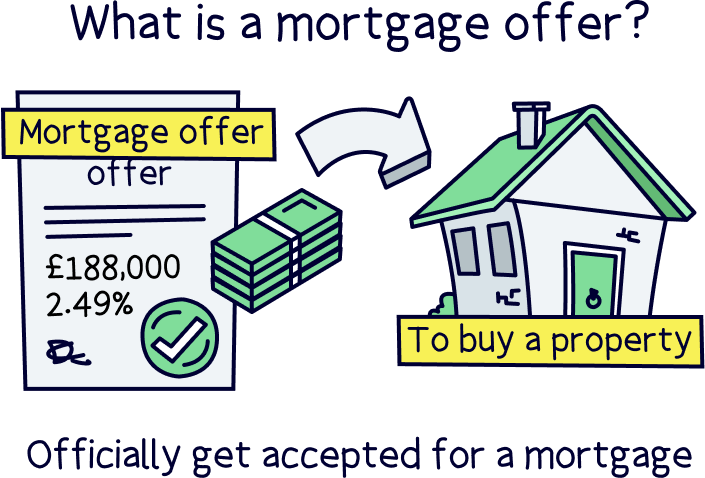

This is the part where you get to jump up and down excitedly about getting a mortgage offer!

After your mortgage valuation is out of the way, your lender will have everything they need to make a final decision. Then, after an agonising wait of around 2-20 days, you’ll (hopefully!) get the news you’ve been waiting for. Phew!

Just bear in mind that this isn’t the end of the journey quite yet. Even though you’ve now been approved for a mortgage, your lender could still technically change their mind if your circumstances change before your house purchase goes through. So, sit tight and try to act normal! (In other words, avoid changing jobs or taking out any other loans for the time being.)

Note: if you change jobs, read our getting a mortgage with a new job article.

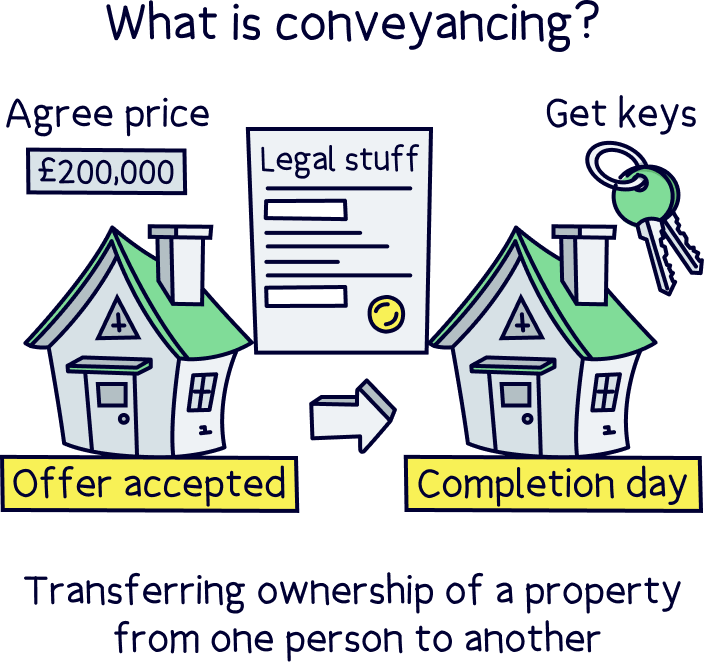

Exchanging contracts is the moment where you’re legally committed to buying the property (and the seller is legally committed to selling it to you). Basically, it’s when you finally get to breathe a massive sigh of relief – up until now, the seller could have pulled out of the house sale at any moment, but now you’ve reached safety!

From your mortgage lender’s point of view, you could exchange contracts anytime after your mortgage offer comes in. That said, most people will still need to wait around 1-2 months before they exchange.

Well, while your lender’s been sorting out everything to do with your mortgage, your conveyancing solicitor will also have been hard at work gathering all the legal documents you need for the house purchase to go through. This involves a lot of back and forth with the seller’s solicitors, so it can take a while!

Check out our piece on how long conveyancing takes to get a better idea of the process.

Ultimately, you’ll need both your mortgage lender and your solicitor to be happy before you can go ahead and exchange contracts. It can feel like a bit of a marathon, but you’ll get there in the end!

Okay, so there have been a few causes for celebration already in this process. But now’s the time to crack open your fanciest bottle of bubbly… in your new home!

That’s right, ‘completing’ is the moment where the whole house sale goes through and you get the keys to your very own pad. Congratulations!

This usually happens around 1-2 weeks after you exchange contracts, but if you’re in a rush, it could happen the very same day. Or, it could happen a number of weeks after. It all depends on what you agree with the seller.

If you’re part of a chain (where there are multiple buyers and sellers all buying from one another) then you may have to wait longer as you’ll need every party to be ready at the same time. On top of this, some lenders require you to leave at least 5 working days between exchanging and completing.

Ultimately, a gap between the two is no bad thing as it gives you the chance to start packing those boxes up, ready for moving day. How exciting is that?!

Every house sale is different, so it’s impossible to say exactly how long yours will take. But one thing’s certain. No matter how long you have to wait, it’ll all be worth it once you’re sitting on the floor of your brand new pad with a takeaway on your lap and boxes all around you waiting to be unpacked!

If you’re ready to start the process, the first step is to chat to an independent mortgage broker who can hold your hand at every step.

As a reminder, if you need to find a decent mortgage broker check out our top mortgage brokers. You can also see the latest interest rates with our mortgage comparison tool.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.