Article contents

Getting a mortgage with a new job can be challenging, but it’s definitely possible. If you can hold off for at least three months, your application will be stronger. Mortgage lenders will want to see proof of income and greater job stability.

Been offered a new job? Congratulations! Lying awake at night wondering whether you can get a mortgage now? We’re here to help.

Whether you’re umming and ah-ing about whether to accept that job offer, or you’re toying with the idea of starting your job hunt, we’ll take a look at the ins and outs of getting a mortgage with a new job.

In short, it’s not as scary as you might think and you do have options. We’ll break it all down for you below.

If you were lending someone money, you’d want to be sure they were going to be able to pay it back, right?

Mortgage lenders (people who give out mortgages) are exactly the same. They don’t want to give anyone a mortgage who’s not going to be able to pay the mortgage back. So, when you put in a mortgage application, they’ll spend a long time trying to work out what their chances are of getting their loan repaid. Makes sense, right?

But where does a new job come into this?

Well, if you’ve recently changed jobs, a mortgage lender will see you as more risky than someone who’s been in the same job for ages. Why? It mostly comes down to 3 things:

Don’t worry, we’re not trying to scare you! It’s just that if a company has to make job cuts, often they’ll let go of the newest employees first. You know, ‘last one in, first one out’ and all that! This means you’re more likely to be made redundant than someone who’s been in the same job for years.

Are you still on your probation period? We hate to break it to you if you are, but this means your employer could end your contract at any moment, with barely any notice. If that happens, how are you going to pay your mortgage?

Just as that’s probably a terrifying thought for you, it’s also pretty scary for those mortgage lenders who are desperate not to lose their money.

As part of the mortgage application process, lots of lenders will want you to provide them with payslips from the last few months (or longer!). If you haven’t been in your job for that long, that’s going to be just a little bit tricky.

Don’t worry though, some lenders will accept a letter from your employer confirming your salary instead, so all is not lost – we’ll get to this later.

So, the big question on everyone’s brain: ‘How long do you really need to be employed to get a mortgage??’

Let’s start with the short answer. In the UK, most mortgage lenders will want to see that you’ve been in your current job for at least 3 months.

Now for the long answer. In reality, every mortgage lender is different. Some lenders will be happy to lend to you if you’ve been in your job for 3 months or less, while others will only lend to people who’ve been in employment for more than 3 years!

It’s definitely going to be harder to get a mortgage if you’ve recently changed jobs, so if you can wait a while before applying, that’s ideal. That said, getting a mortgage with a new job is possible. At the end of the day, it’s all about finding a lender whose criteria matches your situation.

We’d always recommend getting an independent mortgage broker onboard, who’ll be able to tell you what your options are and which lenders are most likely to accept you. On top of that, they’ll sort out the application for you and make the whole process of getting a mortgage way easier!

Not sure where to find a good mortgage broker? Check out our recommended mortgage brokers.

If you want an idea of mortgage costs view our mortgage comparison table and to work out what your monthly repayments would be visit our mortgage repayment calculator.

If you’ve just changed jobs and you’re holding out for a mortgage, here are some of the things that mortgage lenders will look at when they’re deciding whether or not to say ‘yes.’

Have you passed your probation period? Crack open the champagne!

Although you’re still more risky to mortgage lenders than someone who’s been in their job for years and years, at least your employer can’t fire you at a moment’s notice. That definitely counts for something!

If you’re still on your probation period, you might be best off waiting for the green light from your employer before you apply for a mortgage. But if that’s not possible, don’t panic. It’s not the only thing that lenders will look at, as you’ll see below.

One thing that mortgage lenders always look at when they’re deciding whether or not to accept someone for a mortgage is ‘affordability.’ In other words, they’ll try to work out whether they think you’ll be able to afford the monthly repayments. If you’ve got a pay rise, that means you’re more likely to be able to pay them back.

If, on the other hand, you’ve taken a pay cut, your ‘affordability’ and the amount your lender will be happy to offer you, will go down. This might mean you need to look for a cheaper property, or if you’re already partway through the house buying process, you’ll need to check that your lender is still happy to offer you the same amount.

When it comes to proving your income, most lenders will want to see at least a few months’ payslips. So if you can, wait until you’ve been in your job for at least a few months before applying. If not, don’t panic. Some lenders will accept a signed letter from your employer confirming your salary.

Are you still getting paid in the same way as you were before? If you’ve taken a salary cut but your new job includes commission, overtime or bonus payments, your total income may not be so different after all. So, you’ll need to try and show mortgage lenders how much you could really earn.

If you’ve been in your job for a few months, your payslips should do the talking for you. But if not, try to think of how else you could prove your extra income. Perhaps you could get written confirmation of guaranteed bonuses or a letter detailing what commission you can earn. It might just make all the difference!

Your affordability isn’t just about how much you earn. It’s also about how much you spend! In the eyes of the mortgage lender, there’s no point in earning tons of money if you spend it all on the latest gadgets or trendy footwear.

Your lender will want to check that your outgoings (such as your living expenses) still leave enough money to pay back your mortgage. Some lenders will even ask for bank statements so that they can check your expenses for themselves. So try and reduce your spending for a few months– especially if you’ve taken a pay cut. That means no big purchases until your house sale has gone through.

Have you got a car on finance? A student loan? Credit card debts? These factors are all things that your lender will take into account when they’re deciding whether or not to lend to you.

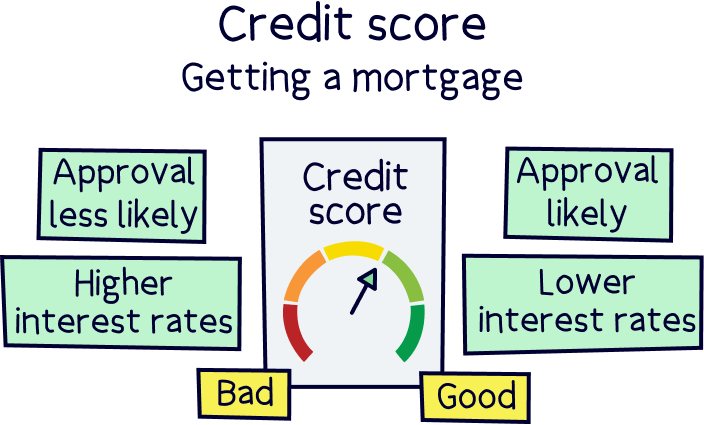

Normally, they’ll do this by checking your credit score – a figure that shows lenders your credit history (or in other words, a figure that shows how good you are at paying debts back).

If you want to see what your credit history looks like, head over to Experian, Equifax and TransUnion. These organisations provide the information that’s used to calculate your credit score in something called a ‘credit report.’ They have to give you access to it for free by law.

Sadly, if your credit score is not in good shape, it’s unlikely that lenders will offer you a mortgage. Especially if you have a new job on top of it all! So, if your credit report’s looking a bit peaky, now’s the time to spruce it up a bit.

That means settling any unpaid bills, paying off your credit cards and avoiding any big purchases until you’ve been accepted for a mortgage and it’s all gone through. And yes, that means putting off that fancy holiday you’ve been dreaming of too. Sorry!

Is your new job in the same industry or field as your last one? If your answer’s yes, you’ll have made potential lenders very happy. Basically, if your new job is in a sector or role that you’re experienced in, chances are you’ll be good at it. From a mortgage lender’s standpoint, that means you’re less likely to get fired and more likely to pass your probation period. Get in!

If you’ve launched yourself into a completely new field, don’t panic – lenders will be looking at all the factors we’ve mentioned so far. Plus, every mortgage lender’s criteria is different. Don’t forget to get in touch with a mortgage broker to find out if there are lenders out there that can work with your circumstances. Again, here's a list of our recommended mortgage brokers.

Tembo will find your best deal, fast, all with award-winning service.

If you’re self-employed, it’s going to be that little bit more tricky to get a mortgage because you’re unlikely to have payslips that prove your monthly salary. Many lenders need at least one or two year’s worth of accounts as proof of income before they’ll consider self-employed workers, while others need three years of accounts or even more!

Now add to that the fact that you’ve only just gone self-employed. Is it going to make it trickier to get a mortgage? Absolutely. Is it going to make things impossible? No!

The best thing you can do is talk to a mortgage broker to find out what your options are, and before that, check out our guide on self-employed mortgages. A broker may be able to find you a deal with a lender who has more flexible lending criteria, such as one that specialises in lending to the self-employed.

Everything we’ve mentioned above (like your credit score, your salary and whether you have experience working in the same industry) will also come into play if you’re self-employed. So, performing well in those areas can only help. Plus, if you’re a self-employed fixed-term contract worker, lenders may also look at how long your contracts are. Check out our guide to getting a mortgage on a fixed-term contract to find out more.

If you can wait until you’ve been in your new job for a few months before you start house hunting, or if you can change careers after moving into your new home, your life’s going to be a hell of a lot easier. But we all know that’s not always how life works!

So, what happens if you switch jobs while buying a house??

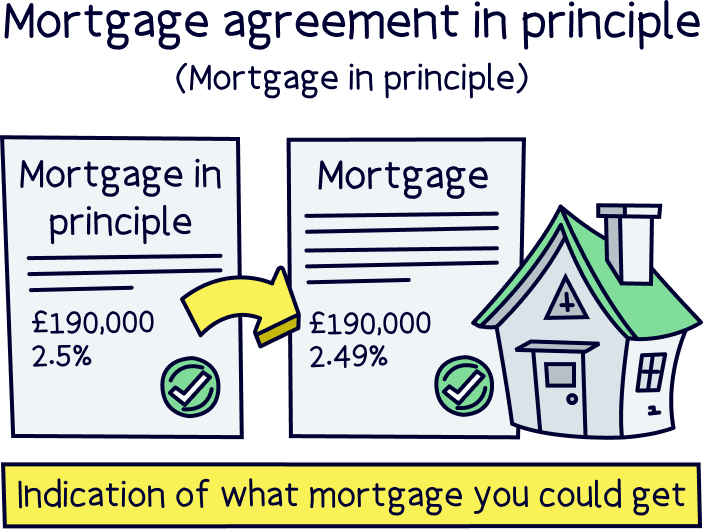

Let’s look at the worst-case scenarios first. If you switch jobs after getting a mortgage in principle, your lender might not be willing to honour the agreement when you come to take out the mortgage. A mortgage in principle is basically a document that says how much a lender is willing to loan you, providing their checks go through okay – it’s based on your circumstances at the time, so if those circumstances change, that might invalidate the offer.

Note: here's how to get a mortgage agreement in principle.

Similarly, if you change jobs once you’ve been accepted for a mortgage, your lender could withdraw their agreement completely, or they could decide to offer you a smaller loan.

Now for the better news: some mortgage providers might just be happy to just continue as if nothing’s changed.

The decision is likely to come down to factors like whether your affordability will stay the same, whether you’ve stayed in the same industry and whether you’ve moved up or down a rung in your career.

Talk to your mortgage broker before accepting a new job offer if you’re in the middle of a house purchase. They’ll be able to advise you on what to do next, and they may even be able to give you the inside scoop on how your lender has reacted to similar situations in the past.

Until your house purchase has gone through, you have to tell your lender if you’ve changed jobs. But once you’ve moved in and your mortgage is up and running, you don’t have to keep them updated anymore.

That means no sniffing through your bank statements, no snooping at your payslips and no questions asked if you go ahead and switch jobs. Freedom!

BUT (yes, there’s always a but!): if changing jobs means you’re going to struggle to make your monthly repayments, that’s a different question. Missing mortgage payments can make it really hard to get another mortgage or other loans in the future, so you’re best off being upfront with your provider to see if there’s anything they can do to help.

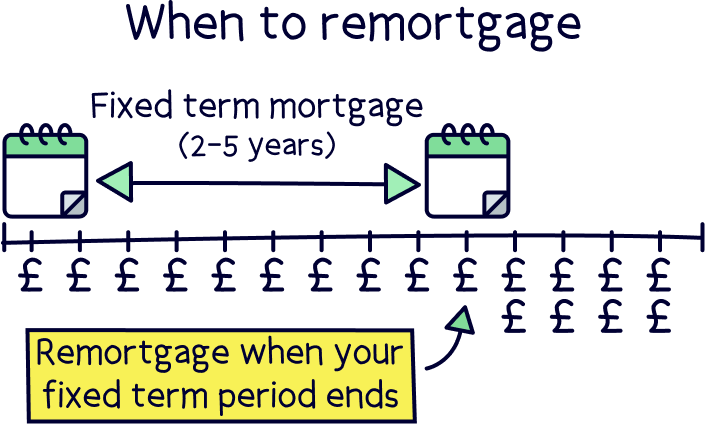

The other thing to bear in mind is remortgaging. If you’re on a fixed-rate mortgage, that means the interest you pay on your loan is fixed at a certain rate (usually for 2 or 5 years). Once that time passes, you’ll want to remortgage your property to stop the interest rates from increasing (our piece on what happens when your fixed-rate mortgage ends has the full lowdown).

The reason we bring this up is that switching jobs when you’re coming close to remortgaging can make it harder to get a good deal on your remortgage – just like how it can make it hard to get a mortgage in the first place. Especially if your salary goes down! So, keep an eye out for the end of your fixed-rate mortgage and bear that in mind if you’re planning a job move anytime soon.

At the end of the day, nothing’s impossible. Yes, getting a mortgage is easier if you’ve been in your job for at least a few months, but there are other routes you can take. Chat with a mortgage broker before you go any further, to see what they say about your specific circumstances.

Fingers crossed, you’ll be unpacking boxes in your dream home before you know it!

As a reminder, if you need to find a decent mortgage broker check out our top mortgage brokers. You can also see the latest interest rates with our mortgage comparison tool.

For more information about mortgages visit our mortgage home page.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.