Article contents

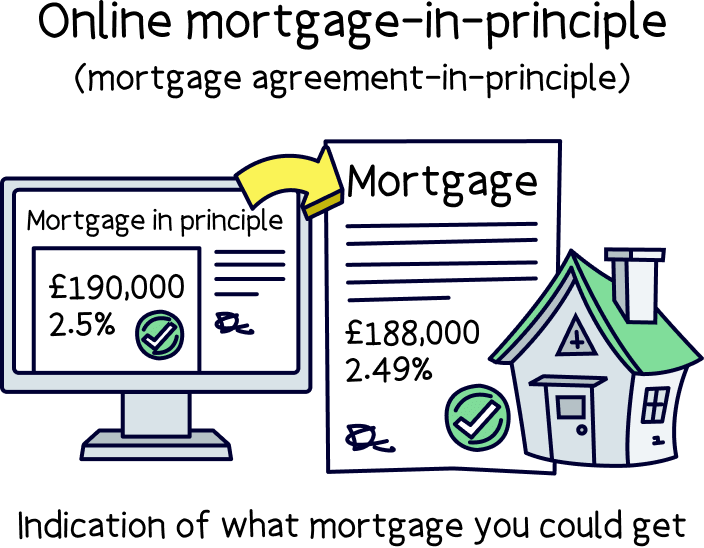

A mortgage agreement in principle is a document from a lender stating how much they might lend you for a mortgage. It shows sellers you’re a serious buyer and helps you budget when house hunting and gives you peace of mind that you can get a mortgage before you’re approved for an actual mortgage.

Refreshing your Rightmove every two seconds? Stoked about finding the house of your dreams? Hold your horses for just a moment. The chances are that first, you’ll want a mortgage agreement in principle. Here, we’ll take a look at exactly what that is, why it can be handy and how to get one.

Ever heard of a mortgage in principle? How about an agreement in principle, decision in principle or mortgage promise? Most of the time, these words are used to describe the exact same thing.

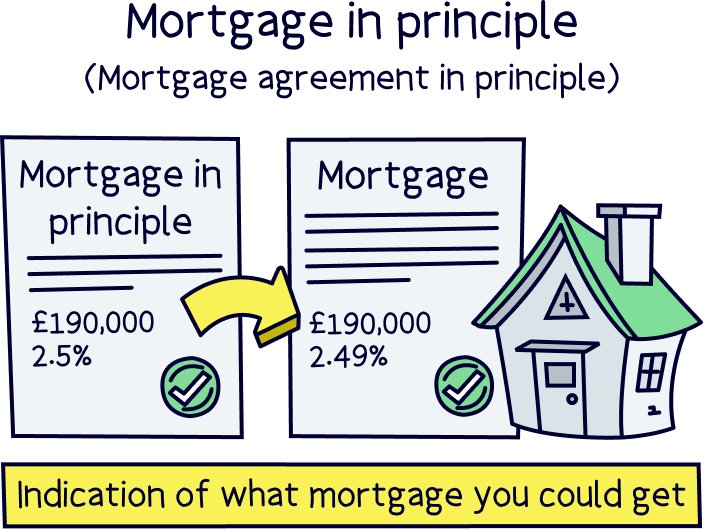

A mortgage agreement in principle is an official document that a lender can give you to show how much they think you could borrow (lenders are the people who give out mortgages). Basically, if a lender gives you one of these documents, it means they think you’re pretty likely to get approved for a mortgage when you apply for one.

Normally, this is the first step towards buying a home and happens before you even start viewing properties.

Tembo will find your best deal, fast, all with award-winning service.

You don’t need a mortgage in principle. But you’ll probably want one. It's a no-brainer, a mortgage in principle is completely free.

Here are the main reasons for getting your hands on one.

Nuts About Money tip: You can get a good idea of monthly repayments based on your deposit and the property value with our mortgage comparison table.

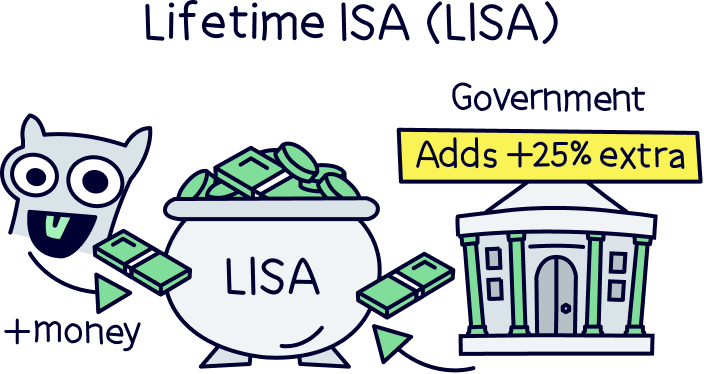

And while we're talking about deposits. Did you know you can get a free 25% on your savings for your first home with a Lifetime ISA? It's a government scheme to help UK people to get on the property ladder. You’re able to save up to £4,000 per tax year (April 6th to April 5th the following year).

Here's where you can find out more about Lifetime ISAs, and what's the best Lifetime ISAs.

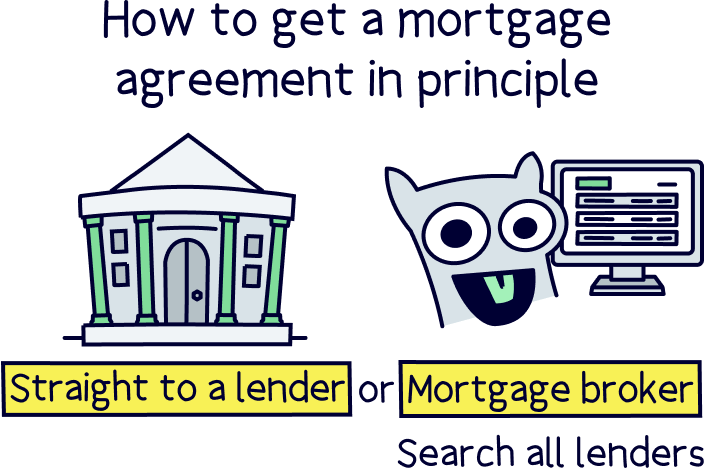

Getting a mortgage in principle is normally pretty quick and easy. You can either:

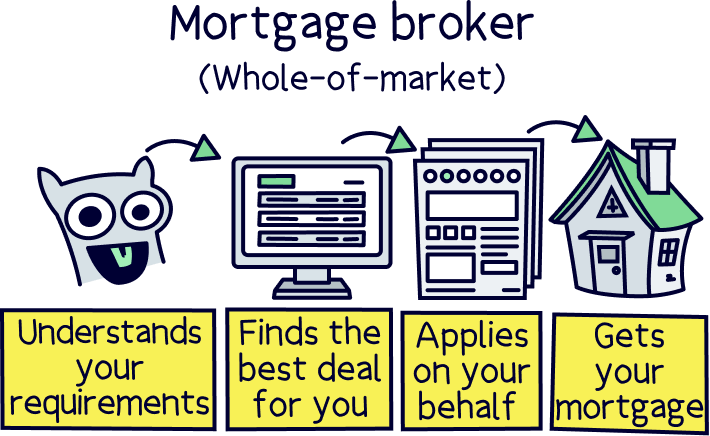

We’d normally recommend using a mortgage broker. That’s because, even though you can apply directly to mortgage lenders, there are over 100 lenders in the UK! So, it can be hard to know which lenders are most likely to say yes. And even harder to know which will be willing to lend you the most money, or to give you the best deal.

On the other hand, an independent mortgage broker will know the ins and outs of the different mortgage lenders and can compare the market to find the best one for you. You’ll have to dig out a few documents for them (things like bank statements and ID) but once that’s done, they’ll often be able to get you a mortgage in principle in as little as an hour. That’s right, you just put your feet up while they sort out the whole application for you!

By the way, some online mortgage brokers will give you a mortgage in principle without actually going to a lender for you. If you’re thinking: ‘huh? I thought only lenders could give out mortgages in principle?!’ then you’re half right, but there is a catch!

The document you get given by a lender is technically called a mortgage agreement in principle. Don’t get us wrong, most people still call it a mortgage in principle for short. But some mortgage brokers (mostly the online ones) take advantage of that and will give you a ‘mortgage in principle’ (without the word ‘agreement’ in it) that hasn’t been okayed by a lender.

These documents can still be handy for showing estate agents and giving you a rough idea of how much you might be able to borrow. But they don’t actually show you whether there’s a lender out there who could be willing to lend you the money. But worth getting all the same!

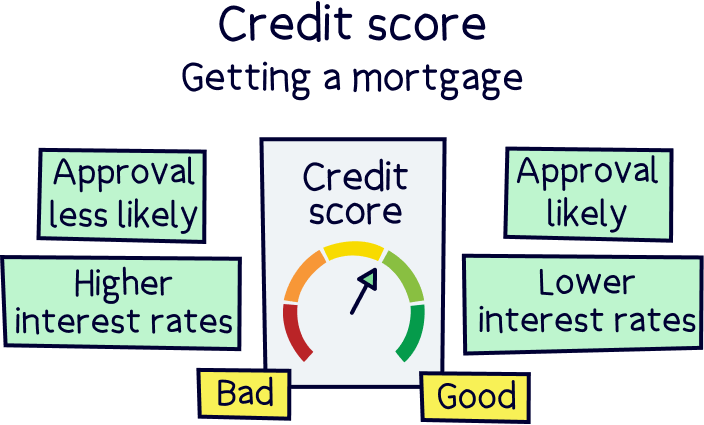

Worried about your credit rating? There’s no need! A mortgage agreement in principle won’t affect your credit score.

If you get a ‘real’ mortgage agreement in principle with a mortgage lender, they’ll run a ‘soft credit check’ when you apply for an agreement in principle. This is just a quick look at your credit history and credit file, which won’t affect your credit score.

If you get a quick mortgage in principle with a mortgage broker, this won’t affect your credit score at all, and often won’t carry out a soft credit check either. It’s just an indication of how much you can borrow to show estate agents you are a serious buyer.

Only when you’re happy you want the mortgage and apply for the mortgage, will they run a ‘hard credit check’ and this will become a record on your credit file. This check will look at data from credit reference agencies, and your overall credit history to make sure you’re in good shape to pay future mortgage payments.

Let’s imagine that you’ve got your mortgage agreement in principle. What happens next?! Well, here’s a quick lowdown.

For a better idea of how long each stage of the process will take, check out our mortgage application timeline.

Let’s put it like this: getting a mortgage agreement in principle is a good sign that you’d get accepted for a mortgage. But it isn’t a guarantee.

A mortgage in principle only shows that, from what a lender knows about you, they think you’d get approved for a mortgage. However, there are a few things that can go wrong between getting your mortgage in principle and getting approved for a full mortgage...

So, in summary, if you got accepted for a mortgage in principle, things are looking pretty good for you. But there’s still a chance you could get rejected later down the line.

Ultimately, the best thing you can do once you have a mortgage in principle is to sit tight, try not to make any big life changes.

There’s one more thing you need to know before you go off and get your hands on that mortgage in principle: mortgages in principle have expiry dates!

Normally, they’ll only last for 60 to 90 days.

If you’re thinking: ‘How am I supposed to find a property to buy within 60 to 90 days?!’ don’t panic.

First things first, before you get a mortgage in principle, it’s useful to do some research on property websites and apps like Rightmove and Zoopla. Take some time to get familiar with what kind of properties are out there and what your deal breakers are. That way, once your mortgage in principle comes through, you’ll have a good idea of what you’re looking for and you’re more likely to find the right fit before it expires.

Secondly, if your mortgage in principle does expire, it’s not the end of the world! Remember that you don’t actually need one to apply for a mortgage. You could just go ahead and put an offer in on a property without one. Or, if your estate agent is bugging you for a valid mortgage in principle, you could just reapply for a new one. What we’re trying to say is that you have options!

Note: You also might be interested in our article How long does a mortgage offer last?

Ready to start your house hunt with your best foot forward? A mortgage in principle could be the answer.

Not only is it a great way to show estate agents and sellers that you’re a serious buyer, but it can also help you to understand what properties you’re going to be able to afford and it can give you that peace of mind you’re after (or at least, as much peace of mind as you can get before you’re approved for an actual mortgage!). If that sounds good to you, just get in touch with a mortgage broker who’ll be able to guide you through every step of the process. Good luck!

Need help finding one of these awesome people? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. Plus, get 50% off their fee with Nuts About Money.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.