A mortgage broker will find you the best mortgage deal and handle all the paperwork too - here's our top picks.

It’s an award-winning mortgage broker with awesome service. They'll find your best deal.

Let the experts compare mortgages to find the best mortgage deal for you – you could save £100s.

Get 50% off

Tembo is an all-round amazing mortgage broker, in fact, they're award-winning, and not just online.

They can help with pretty much every mortgage out there, from buying a home to switching deals, and on top of that, have unique options to increase your borrowing such as an Income Boost¹ and Deposit Boost¹.

They'll handle the whole mortgage for you too, and the service is great.

• Guaranteed the best mortgage deal

• Increase your borrowing

• Boost your deposit

• Awesome service

• Online and over the phone

• Apply and handle all the paperwork for you

• It’s not free (but 50% off with Nuts About Money)

Get FREE advice

Habito makes mortgages and buying a home much easier – it's all online.

They’ll find the best mortgage for you, all for free, and all in your own time.

But better than that, if you’re buying a home, they’ll handle the whole process for you – that’s the legal work and survey, and everything else. It’s a huge stress and time saver, and comes at a great price.

The customer service is great too.

• Completely free mortgage advice

• Searches the whole market

• Excellent customer service

• Can help with every step of buying a home

• You have to start the process online (can't call straight away)

Unbiased help you find the right mortgage broker for you from your local area. Their advisors are all rated 5*, fully qualified and search the whole-market (every mortgage deal).

• Free to use (but fees charged from advisors)

• Find a mortgage broker in your local area

• Best option if you want face-to-face advice

• Advisors are vetted and typically great

• Fees can vary depending on your chosen advisor

• Can’t get a mortgage online

L&C are becoming a bit outdated for modern times – it’s effectively a big call centre.

They’ll find you the right mortgage, and for free, but it’s all phone based and time-consuming with scheduled meetings.

The customer service is very inconsistent too. There’s better options out there.

• Free

• Searches every mortgage out there

• All phone based

• Very salesy

• Customer service is inconsistent (depends on your advisor)

Thinking about getting your mortgage online? Good choice. It’s more convenient and lets you work on your schedule rather than the mortgage broker’s.

We’ve reviewed the best online mortgage brokers in the UK, to help you find the right broker for you – using a great one can really help find the right mortgage deal, potentially saving £100s per month.

There’s a few online mortgage brokers out there (also called mortgage advisors), but they’re not all equal!

Using an online mortgage broker is a great idea – you can pretty much handle everything online, instead of trying to book appointments over the phone or in person with a mortgage advisor.

Online mortgage advisors allow you to work to your own schedule – you decide when you want to speak to them, provide your details, and apply for your mortgage – it’s all up to you. Technology can be a wonderful thing!

They’re also typically much faster to give you an indication of how much you can borrow (called a mortgage-in-principle), and a real mortgage quote so you know how much you might be paying per month. Plus they are often quicker with the whole mortgage application process and getting the actual mortgage too.

Nuts About Money tip: get an idea of monthly mortgage repayments by comparing current mortgage rates with our mortgage comparison table.

The customer service is often great too. And the best bit, some of them are completely free to use, saving you hundreds of pounds! What’s not to love?!

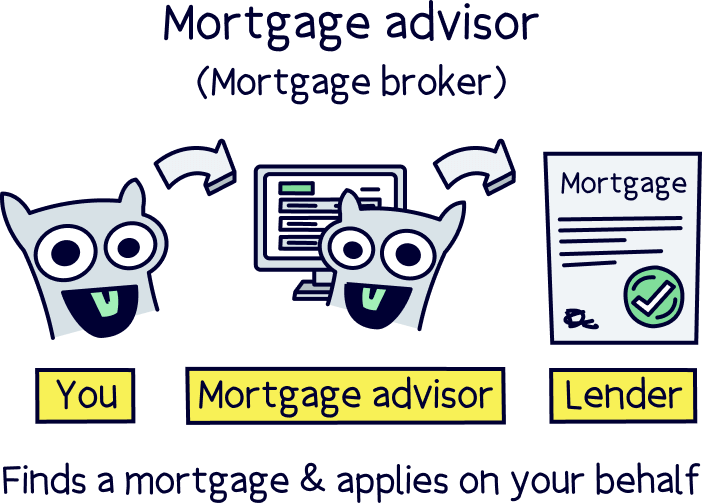

By the way, a mortgage advisor and mortgage broker just means the same thing. It's simply an individual or a company that gives mortgage advice.

If you’re buying your first home, first of all, congrats! Getting on the property ladder is a huge achievement in today's world. We’re going to guess that you don’t know too much about getting a mortgage – and that’s fine! That’s why we’re here.

For first time buyers, we recommend using Tembo¹ – they're experts at not only finding you the right mortgage deal, but they also help with increasing your borrowing and boosting your deposit – making it much easier to get a mortgage and buy your dream home (plus get 50% off their standard fee with Nuts About Money).

Here’s our Tembo review to learn more.

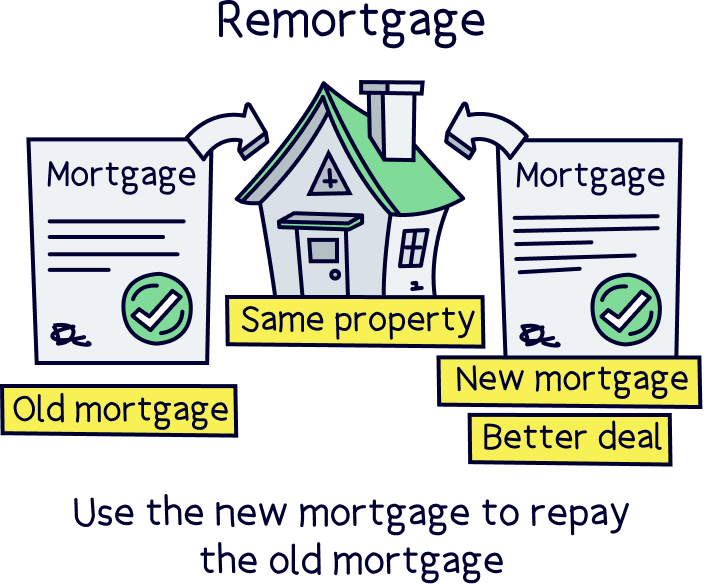

If you’re looking to switch to a new mortgage deal (remortgage) you should still use a mortgage broker to find the best new deal for you – which a good mortgage broker will do.

Again, we recommend using Tembo¹ for remortgaging, they'll guarantee to have you on the best new deal, and in no time at all – so you won't end up paying any more than you need to. Again, you can save 50% with Nuts About Money. Alternatively, check out our top mortgage brokers.

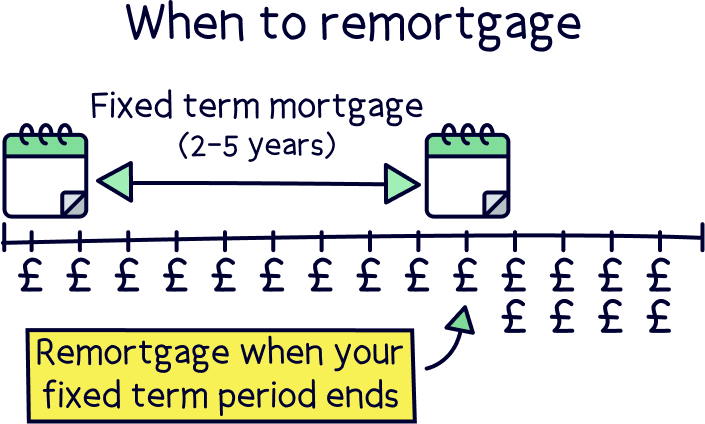

By the way, we highly recommend you remortgage when your original fixed term period ends (the fixed term period is the initial rate a lender will give you to take out the mortgage. It's normally a cheaper deal for 2 or 5 years).

When you remortgage and switch deals, you’ll avoid paying a higher interest rate than you have to and potentially saving £100s per month on your mortgage repayments.

Nuts About Money tip: Find out how much your monthly repayments will be with our mortgage repayment calculator.

Note: it doesn’t make a difference if you are remortgaging or buying a home, finding the best mortgage deal is a similar process and still hard to do yourself – a mortgage broker will find you the best deal and handle all the paperwork for you too.

Again, using a mortgage broker is a great idea, they’ll find your perfect mortgage, we cover why more in-depth below, but in summary, it’s a lot of work to find your own mortgage, especially to find the right deal for you. A mortgage broker can handle everything for you, and if you use an online broker, it’s much easier and can be low cost if you use the right one!

Nuts About Money tip: see the latest interest rates with our mortgage comparison tool.

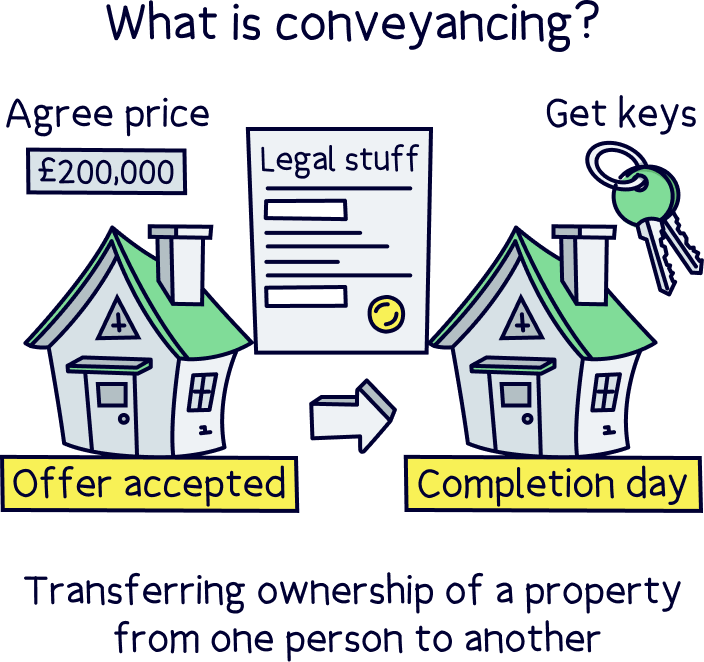

When you buy a home, there’s not just the mortgage to think about, there’s lots of legal work to take care of, such as exchanging contracts (the official thing to say you’ve bought the home), transferring large sums of money (when the mortgage completes) and updating the land registry with your details (saying that you’re the new owner!). So you’ll need a conveyancer or a solicitor (legal people) to do these for you.

You’ll also often need a building survey, which is to make sure the property you are buying is in good condition and suitable to buy – you might be surprised how many homes have issues! This needs to be done by a qualified surveyor and normally arranged by you.

By the way, with Habito¹, they can take care of everything for you:

Habito's fee for all of these services combined is pretty much the same as hiring all these people yourself. To cap it all off, you will need to research and find these professionals yourself. It's a full-time job!

Not having to manage all of this is a real game changer! It's hard to manage everything and can be pretty stressful, especially if you’ve not done it before. Why not just have someone do it for you?! Here’s our Habito review if you want to learn more.

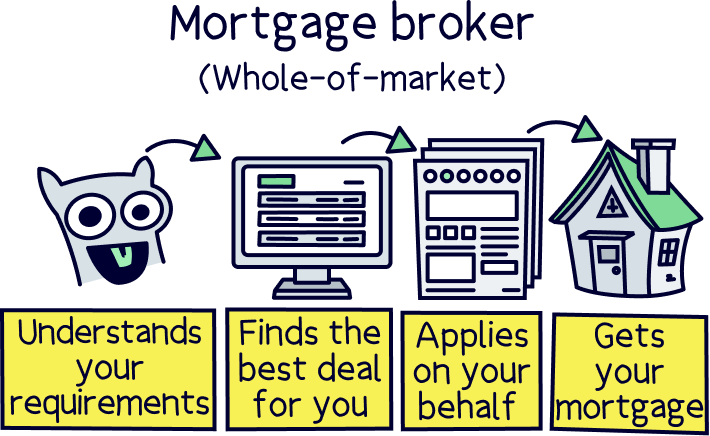

You don’t actually need to use a mortgage broker to get a mortgage. However it helps… A LOT!

Think of mortgage brokers as a comparison site for mortgages. Except not only do they find the right mortgage deal for you, and get you a real mortgage offer, they handle the whole mortgage application process too. They’re with you every step of the way until the mortgage completes.

Pretty great right? Not just perfect for first time buyers, but everyone looking to move home, or just switch their mortgage deal to reduce monthly mortgage payments before they go onto the expensive lender’s standard variable rate).

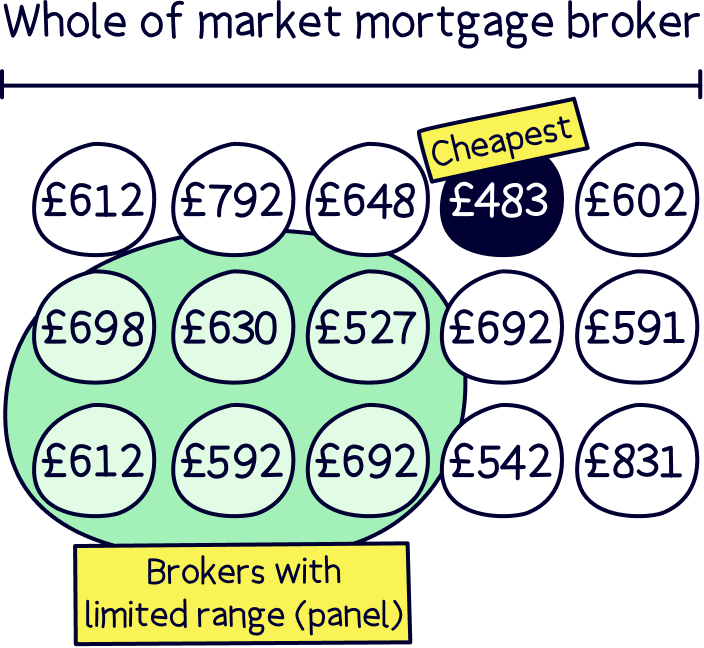

There’s just one thing – make sure you use a good mortgage broker, one that can search the whole market…

The best brokers are able to search every mortgage deal out there to find the right one for you. There's over 20,000 mortgages, so it’s quite a feat to do yourself! All of these mortgages combined are called ‘the whole market’, or sometimes the ‘mortgage market’.

Of course, they don’t do it manually, they have software they use, but they’ll review the results and make sure it’s a good fit for you and your personal circumstances. Each mortgage is quite different, and each mortgage lender has different criteria they use to assess customers and determine if they’ll give you a mortgage or not – and a mortgage broker should know all these little details and which mortgages you'll likely be accepted for.

Having said that, not every mortgage broker can search every mortgage deal out there – some mortgage advisors are restricted to a few mortgage lenders (sometimes they will be called their 'panel'), and it definitely pays to do your research here.

The number one rule is do not use a mortgage broker who cannot search the whole market!

Why not? Well, you could end up getting a mortgage that’s a lot more expensive than it needs to be, simply because the broker can’t search them all. And that means you could end up paying £1,000s more in interest payments every year and extra fees.

Tip: You can get an estimate with our mortgage comparison tool.

It’s not worth the risk, even if the advisor seems nice, or is recommended by your estate agent (who will probably get commission for recommending them).

The best online mortgage brokers we’ve listed above, all search the whole market.

You don’t have to use an online mortgage broker if you don’t want to. But we recommend it if you’re happy using websites on your computer or your phone.

We recommend them because it means everything runs to your schedule, rather than the advisor's schedule. The process can be long and you can do little bits here and there when you have some time, rather than having long phone calls with a broker, or a super-long email chain with information going back and forth.

Simply create an online account with an online broker and then when you have a spare 10 minutes or so, answer some questions about who you are and what sort of mortgage you’re after, and what property you’re looking to buy (you could even do it at work, just don’t tell the boss we said!).

But better than that, you can often speak to your mortgage advisor over live-chat (online chat through their website) too, so you can even have conversations that suit your schedule too – and you don’t have to speak to anyone on the phone (if you don't want to).

Once you’ve got the mortgage recommendation (that’s the best mortgage that your advisor has found for you from all the mortgage options), they’ll go ahead and handle all the paperwork to apply to the lender for you too. How good is that?

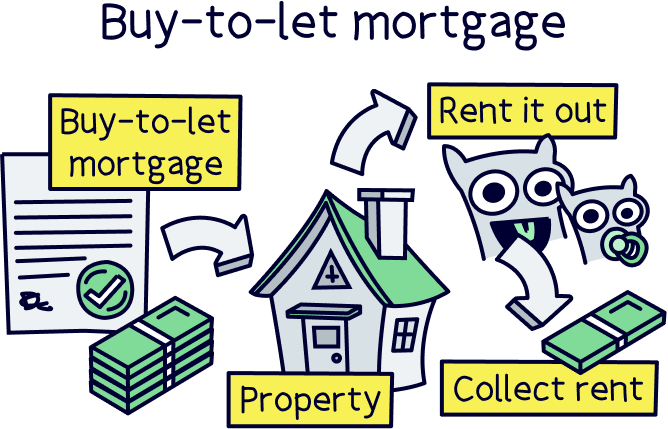

Note: even if you’re looking for a buy-to-let mortgage, online mortgage brokers can still help find the right mortgage deal for you. Even if you’re a portfolio landlord (with multiple properties), you’ll get expert advice and a better deal.

The customer service when getting a mortgage online is normally very good. Just because you’re using an online mortgage broker don’t think the service will be bad!

You tend to speak to your mortgage advisor over live-chat on their website and they also have a customer services team who you can speak to before you get assigned a mortgage advisor, who can answer any questions you have about the service and even mortgages in general.

The response times are way faster than a traditional mortgage broker, who is often working by themselves and can only respond to customers one at a time when they have spare time, and if they’re on holiday you could be waiting weeks!

With an online service, you’ll get a pretty quick reply – because there’s a team of experts waiting for questions to come in. Modern online mortgage brokers tend to have efficient processes in place to help give the best service possible.

And by the way, if you prefer to speak to someone over the phone you can, you just need to ask. They will also reply to emails too.

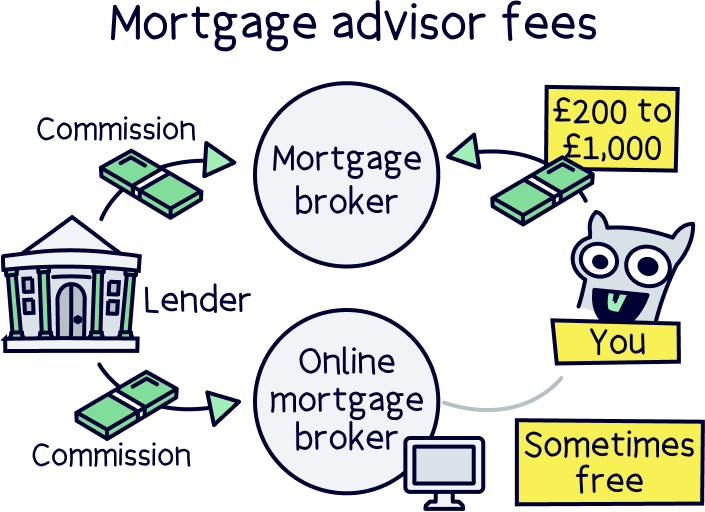

As with all mortgage brokers, they make money (commission) from the lender (the company that gives you the mortgage).

With online mortgages, as it’s online based, they don’t actually need to do as much work as your traditional mortgage advisor – they’ll still find the best mortgage for you of course, but they don’t need to book phone calls and have lengthy conversations over the phone.

Which means they can work with more customers at the same time, and as a result, can make enough money from the lender without charging you a fee too (or a reasonable fee for the service they provide). Pretty clever right?

Traditional mortgage brokers handle fewer customers, and therefore have to charge you a higher fee in order to make enough money.

Our recommended free online mortgage broker is Habito¹,

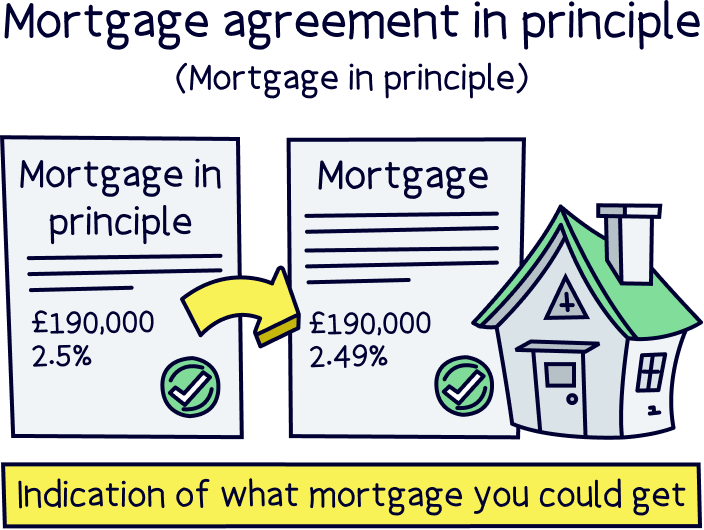

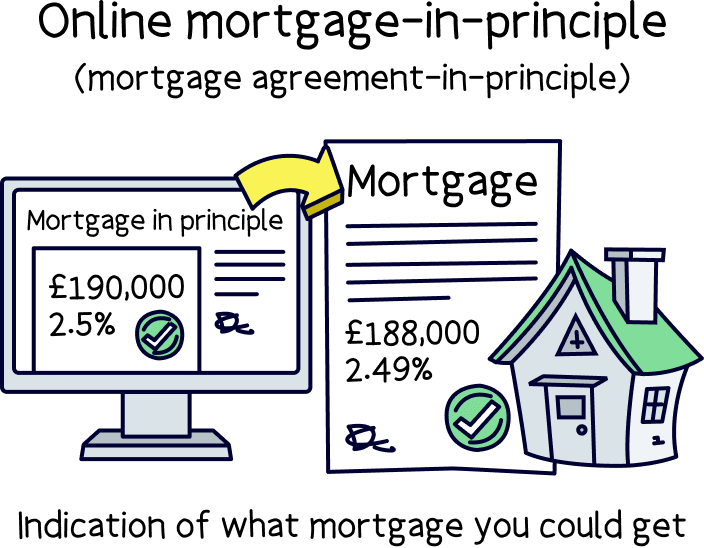

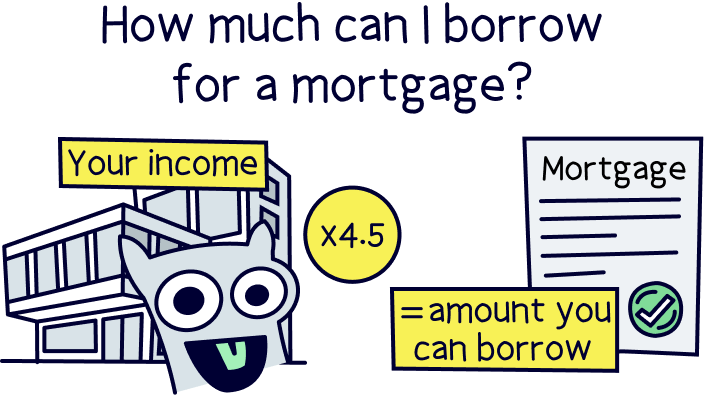

A mortgage-in-principle, or often called a ‘mortgage agreement-in-principle’, is an indication of what a real mortgage could look like – so effectively, it says how much you can borrow, and then what a typical interest rate might be for you based on your individual circumstances.

Determining how much you can borrow for a mortgage is based on your income, so your salary if you’re employed – and how much profit you make if you’re self-employed.

As a rough guide, you could multiply your income by 4.5 to work out how much you can borrow.

This figure would then often be reduced based on your bills and how much spare cash you have left each month – the lender needs to work out if you have a good buffer so that if anything happens you can still pay the mortgage.

A mortgage-in-principle will give you a good idea how much you can actually borrow.

If you need to borrow more than this Tembo¹ can help.

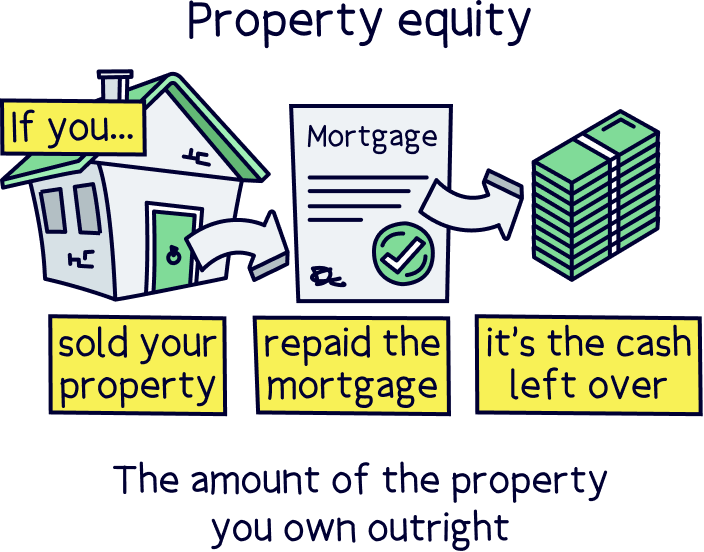

The interest rate will often depend on how much deposit you have, which is the cash you’re putting up yourself to buy your new home.

Or if you’re remortgaging, which is where you already have a mortgage and switching to a new deal, it’s called equity – which is the amount of the property you own yourself.

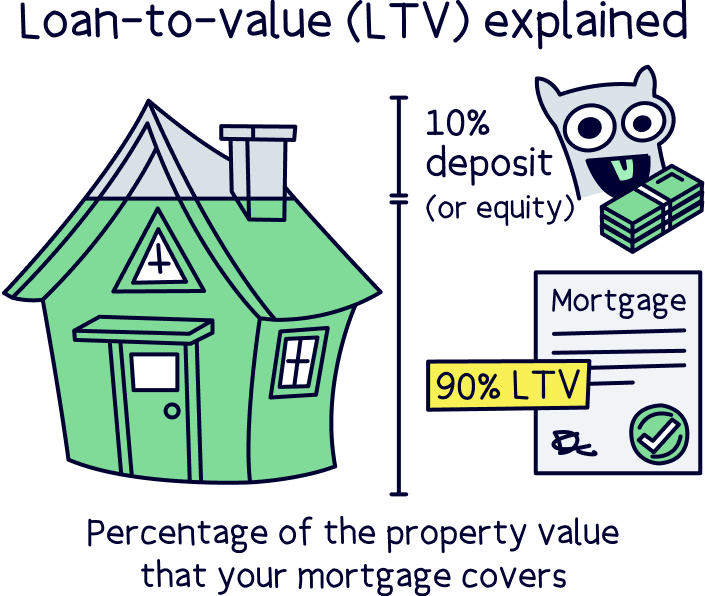

The deposit (or equity) is used to work out how much of the property value your mortgage would cover. So, if you have a 10% deposit, your mortgage would have to cover the remaining 90% of the property price. This is called your loan-to-value, it’s the loan amount (mortgage) as a percentage of the property price.

The lower your loan-to-value (or LTV), the better interest rate you’ll normally get, as the mortgage lender is risking less of their cash vs the property price.

Remember, a mortgage is ‘secured’ against the property – which means if you don’t pay your mortgage repayments, the mortgage lender can take ownership of the whole property (which they’d then sell to recover the mortgage amount). This is a last resort.

Anyway, a mortgage-in-principle is effectively how much you can borrow. And a mortgage agreement-in-principle is often a much firmer agreement with a mortgage provider that they’re happy to give you a mortgage for a certain amount and at a certain interest rate.

We've tried to simplify this as much as possible but it's pretty confusing. If you don't understand it all dont worry, a decent mortgage broker will explain and handle this all for you. An online broker is typically faster at providing you with a mortgage-in-principle.

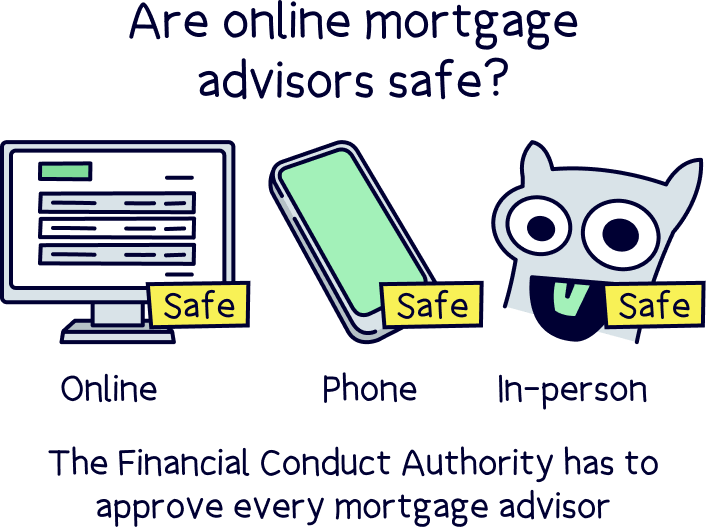

Yep! All mortgage advisors, however they come, over the phone, in-person, or online are all effectively the same when it comes to your protection – it’s just their methods of communication and how good they are at their job that change.

So whichever one you choose to use, you’ll have the same protection from the Financial Conduct Authority (FCA). The Financial Conduct Authority needs to approve the broker before they can help customers, and they’ll be constantly reviewed to make sure they’re giving customers the correct mortgage advice and treating customers fairly.

Whichever broker you use, such as online, you’ll benefit from the Financial Services Compensation Scheme (FSCS) – which means you’ll get compensation if you were given bad advice which resulted in you getting the wrong mortgage deal.

It’s worth checking the Financial Services Register to make sure the mortgage adviser you want to use is properly registered and has permission to give mortgage advice, you can search with their name, or ask for their firm reference number. If you use any of the above recommended brokers, you don’t have to check (unless you want to), they are registered.

We recommend you don’t use your estate agent’s broker (or conveyancer). You can’t be sure that they’ll be able to search the whole market for the right mortgage for you – some just have a very limited number of lenders they can choose from.

The customer service can be pretty poor too – and often it’s done face-to-face in the estate agents office when they can fit you in, unlike an online service where you can chat online whenever suits you.

The estate agent is often either getting commission or the broker is employed by the agent, so you can’t be sure the recommendation is genuine. And the broker will often charge a broker fee too, which can be over £500.

Our advice here is to research the broker properly. Don't just take your estate agent's recommendation.

We recommend you seriously consider one of the online mortgage brokers above. It will be on your terms, after researching which broker is the best fit for you. Don’t be pressured by the agent! Remember the online mortgage brokers are fee free, so you'll save money too.

Estate agent conveyancers are typically bad too – they often have an interest in you buying the home (more money for the agent and their own commission) and can leave important things out, or not explain things to you that they should be – particularly if you’re buying a new build from a developer on a housing estate. It’s best to get your own solicitor or conveyancer so that you have someone on your side.

Let’s recap the pros and cons of using one of our recommended online mortgage brokers for your mortgage.

If you can't tell we're big fans of online mortgages here – most of us here have got our mortgages online ourselves.

They’re a much easier way of getting a mortgage, everything works around you, rather than the mortgage advisor, and you can be sure you’ll get the perfect mortgage for you from every mortgage out there.

And, they’ll handle the whole application process too.

They’re perfect if you’re a first time buyer, moving home, or just remortgaging to a better deal. Even buy-to-let landlords.

If you're ready to get your mortgage online, head over to Tembo¹, they've got award-winning service, and will guarantee to get you the best deal. (And get 50% off their fee with Nuts About Money.)

Alternatively, check out our top online mortgage brokers above. You can also see the latest interest rates with our mortgage comparison tool.

One last thing: You can estimate your monthly repayments for a mortgage with our mortgage repayment calculator.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

It’s an award-winning mortgage broker with awesome service, and they'll find your best deal. Get 50% off their fee too.