Find out how much you could borrow with a mortgage.

More options

To borrow this visit Habito¹.

To borrow this visit Tembo¹.

To borrow this or more visit Tembo¹.

Estate agents require a mortgage in principle (accurate estimate). Get one online in minutes with Tembo.

This is a document with a very strong indication of what you could borrow. You'll need it to plan your buying budget and view properties.

You can get one online, and in just a few minutes, with our recommended mortgage advisors:

Free online service

Habito can also provide a mortgage in principle, find the best mortgage deal based on your circumstances and even help with all the legal work too.

Get 50% off

Get a mortgage in principle to find out what you could borrow with a mortgage. Their service is award-winning, plus they'll find the best mortgage deal from over 20,000 mortgages and even apply for it on your behalf.

Saving and scrimping to be able to buy your dream home? Wondering how much you could actually borrow? You’re in the right place!

Here, we’ll show you how to work out roughly what you can borrow for a mortgage and how to compare mortgages. Plus, we’ll reveal what mortgage lenders will look at when they’re deciding how big a mortgage to give you (lenders are the people that give out mortgages). Enjoy!

First things first, every lender is different. So, they’ll each have their own unique criteria for deciding how much they’ll be willing to let you borrow.

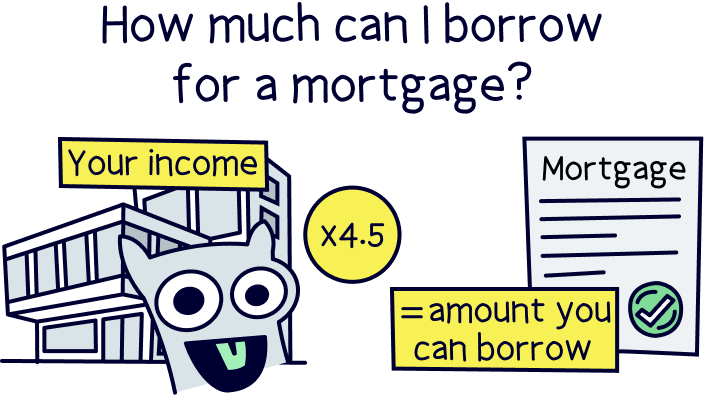

However, as a general rule of thumb, lenders will let you borrow roughly 4.5 x your income (before tax). That means to work out roughly how big a mortgage you can get, you can take your yearly income and multiply it by 4.5.

Let’s look at an example. Say you earn £24,000 per year. That means that, on your own, you can probably borrow around £108,000 (24,000 x 4.5 = 108,000).

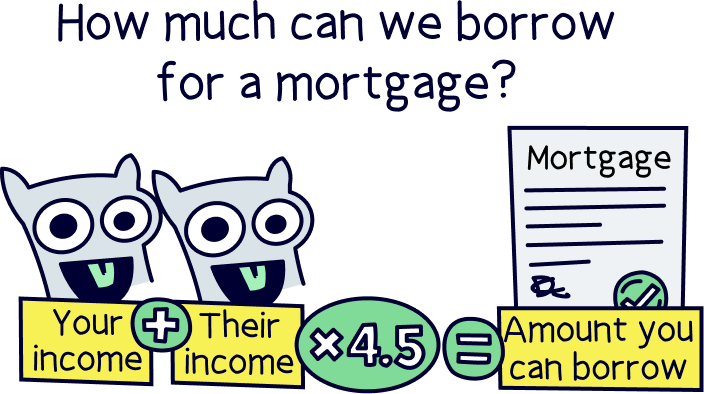

Now let’s say you’re teaming up with someone else to get a joint mortgage (that’s where you buy a home with at least one other person, normally your partner). If you earn £24,000 per year and they also earn £24,000 per year, you’ll probably be able to borrow around £216,000. That’s because between you, you’re earning £48,000 (and 48,000 x 4.5 = 216,000). Simple!

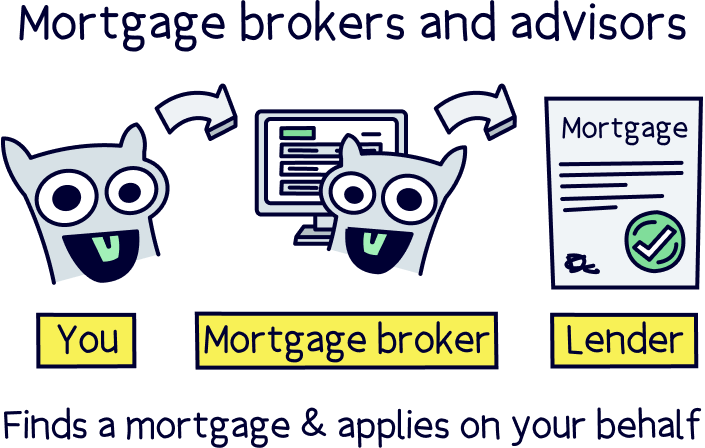

Of course, lenders will do lots of other checks besides just looking at your salary and the exact amount you can borrow will depend on your personal circumstances. To get a clear idea of exactly how much you could borrow, you’re best off chatting to a whole-of-market mortgage broker (also known as a mortgage advisor).

They’ll take the time to understand your personal circumstances and will be able to compare all the different types of mortgages, mortgage deals and mortgage lenders out there, to see how much you could borrow for your mortgage (and to find you the best deals!).

If you're not sure where to find one, check out Tembo¹, they've got award-winning service, and will guarantee to find you the best mortgage deal. You'll also get 50% off their fees with Nuts About Money. Habito¹ is another great option and they are free to use!

If you’re just looking for a quick indication of how much you can borrow, you can use our mortgage calculator above. Or try Tembo’s mortgage calculator¹ – it’s super fast, and will show you options to borrow even more.

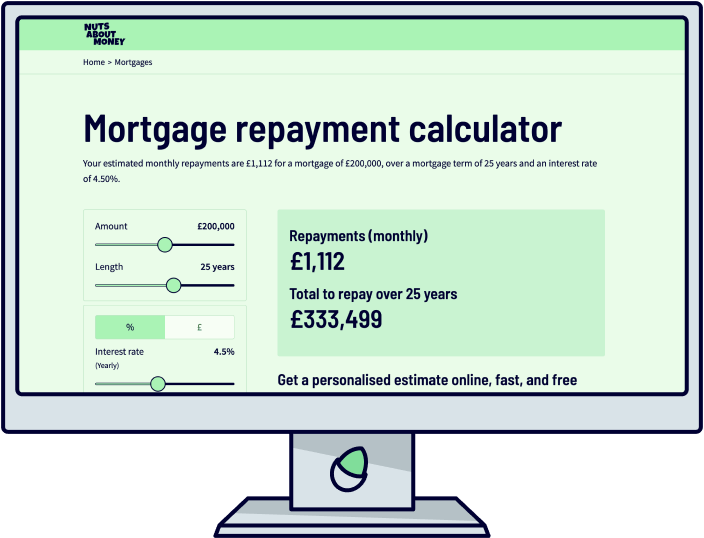

And if you want to see your mortgage repayments and the total cost of a mortgage visit our mortgage repayment calculator.

Note: mortgage calculators will just give you a rough idea about how much you can borrow. There is a bit more to it, and each mortgage lender can be a bit different when it comes to their borrowing criteria (technically called an affordability assessment). Let’s run through what could impact your mortgage borrowing.

Okay, so you know how we said that it’s not quite as simple as just multiplying your salary by 4.5? Well, most lenders will look at some key areas besides your income when they’re deciding how much they’re happy to lend you. Here are the main ones.

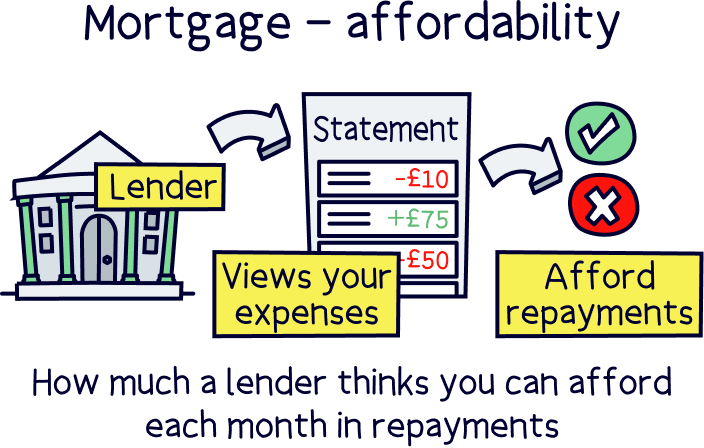

Affordability is all about how much a lender thinks you’re going to be able to afford each month in repayments. Think about it: if you were lending someone money, you’d want to find out whether they had a decent chance of being able to pay it back – right?

Well, lenders are the same. They want to make sure that you’re going to be able to afford to keep up with the repayments before they agree to give you a mortgage.

This is where those checks on your salary come in. In general, they won’t want you to borrow more than around 4.5 x your income because any more than this and you might not be earning enough to keep up with the repayments.

However, they’ll also look at your expenses. After all, no matter how much you earn, you’re going to struggle to pay your mortgage if you fritter all your money away on fancy cars and nights out! Often, your lender will ask for your bank statements so they can get an idea of how much disposable income you have.

Nuts About Money tip: Watch your spending when you’re thinking about applying for a mortgage. If you can, steer clear of expensive holidays and extravagant purchases for a bit. This way, you can avoid sending potential lenders red flags!

It sounds obvious, but you’ll only be able to borrow the full 4.5 x your income as a mortgage if you’re buying a property that’s worth at least that amount. If you’re buying a cheaper property, your mortgage will be for less.

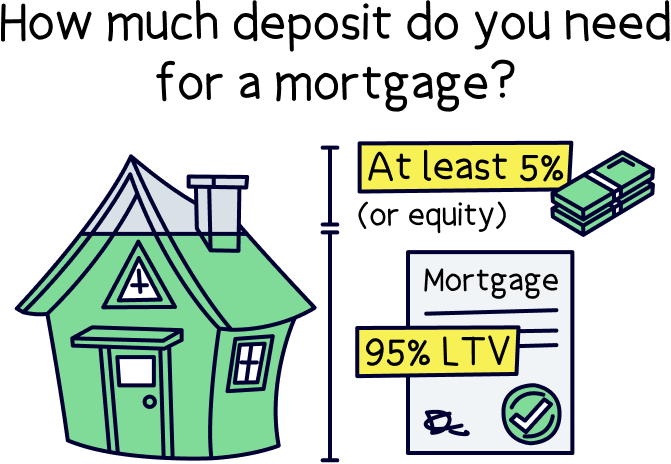

On top of that, most lenders won’t want you to borrow more than 95% of the value of the property you’re buying, known as a 95% loan-to-value ratio (LTV). This means that in order to unlock the full amount of borrowing available to you, you’ll need to be able to save up a mortgage deposit that’s worth at least 5% of the property.

In other words, consider how much deposit you’ve saved. If you don’t have a deposit big enough to cover 5% of the property you’re looking at, you’ll normally need to set your sights on a property that’s worth less and, therefore, borrow less money from your lender.

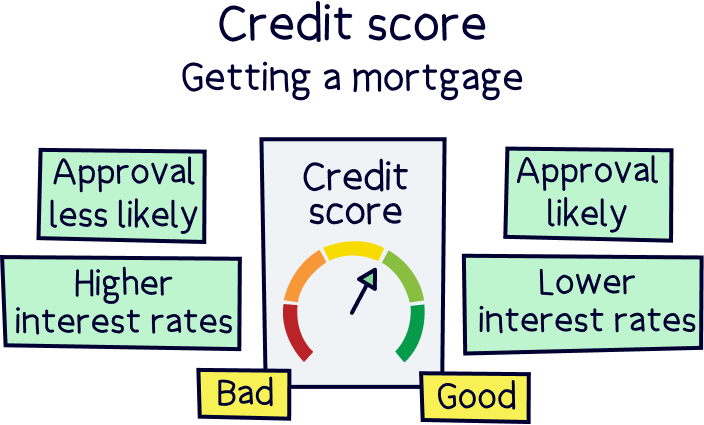

Your credit score is a number lenders use to find out how good you’ve been with money in the past. Everyone has one – it’s basically like a footprint of your financial history, where everything you’ve done money-wise is taken into account.

So, why do lenders care about it?

Well, they use your credit score to see how reliable you are with money. If you’ve had trouble with money in the past, like struggling to pay other loans back, they’ll see this as a sign that you might struggle again. And they’ll often be less willing to lend to you as a result.

Don’t worry. If your credit score isn't in great shape, this doesn’t necessarily mean you can’t get a mortgage. However, it might mean that you can borrow less or that you need a bigger deposit to persuade lenders to approve you for one.

We’d always recommend using a mortgage broker to help you find the best mortgage for you. However, this is all the more important if you have a bad credit score, as they’ll be able to advise you on which lenders are most likely to approve you and they’ll also handle the application for you to make sure it’s as strong as possible (Tembo¹ specialise in mortgages for people with credit problems).

We’ve already talked about the fact that your salary will affect how much you can borrow. But did you know that your job can also have an effect on how willing a lender will be to give you a mortgage?

If you’re self-employed or on a fixed-term contract, it’s often harder to prove your income than it is for someone in a salaried position.

Think about it: if you’re in a salaried job, you’ll usually get paid the same amount every month and you’ll have payslips to prove it. If you’re self-employed, however, your income is more likely to go up and down each month, based on how much work you’ve had. Similarly, if you’re on a fixed-term contract, you may well have periods between jobs where you’re out of work.

This means it can be a little bit trickier for the self-employed or for people on fixed-term contracts to get mortgages (although it’s still totally doable!).

For instance, you’ll normally need to be self-employed for around 2 years before applying for a mortgage, or 12 months at the very minimum if you’re very lucky. This is because most lenders will want to look at your accounts from the last 2 or 3 tax years (compared to salaried employees who normally only need a few months of payslips!). You might also need to put down a bigger deposit.

Similarly to people who have bad credit scores, you’ll generally have fewer lenders to choose from if you’re self-employed or a fixed-term contractor. So, we’d always recommend talking to an experienced mortgage broker who can point you in the direction of suitable lenders.

Worried that you won’t be able to borrow enough to afford that home you’ve set your sights on? Don’t worry, all is not lost. There are a few different ways that you can increase the amount you can borrow from a mortgage lender or even just afford a more expensive house. Here are a few tips.

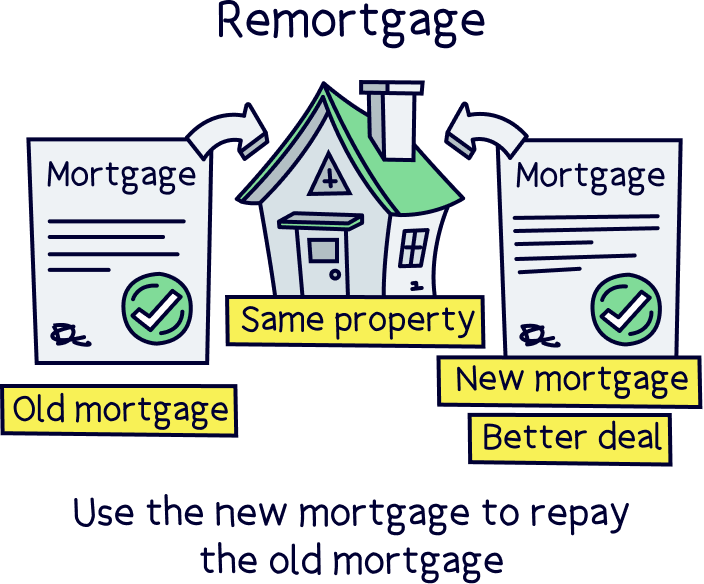

Working out how much you could borrow for a remortgage is pretty much exactly the same as a new mortgage on a new property for a first time buyer (or home mover). However, you’re probably more concerned with the monthly payments and the interest rate, and changing things like the mortgage term.

It’s still dependent on your yearly income (and any other applicants), and dependent on your current financial commitments – things that could affect your monthly payments, so that’s things like utility bills, outstanding loans, child maintenance, car finance etc (things in a mortgage lenders’ affordability assessment).

If you’re looking for a quick quote for monthly mortgage repayments and an interest rate, just head over to our mortgage repayment calculator – it focuses more on monthly mortgage payments rather than specifically how much you can borrow.

That’s presuming you’re more interested in changing your monthly payments now you’ve actually got the mortgage, and interest rate and maybe mortgage term (all of which you can do if you’re coming up to the end of your fixed term). If you’re looking to release equity (release cash), here’s how to remortgage to release equity.

Note: If you're looking to remortgage, take a look at our mortgage comparison.

Want to get a clearer picture of exactly how much you might be able to borrow for a mortgage?

The first step you can do by yourself, it's super easy, it's to use the mortgage calculator above!

If you want a more accurate figure, head over to Tembo’s mortgage calculator¹ and in a few minutes you'll get a good idea about how much you could borrow for a mortgage, and how much the monthly payments will be and even the interest rate.

You'll also be able to see real mortgage deals from mortgage lenders. All you need is your total annual income (yearly income from both of you if it's a joint mortgage. By the way, your partner is called a second applicant).

The next is to talk to a mortgage broker. They’re experts in mortgages and will take the time to learn all about your unique situation before advising you on how big a mortgage you’re likely to be able to get your hands on.

If you're not sure where to find a good mortgage broker, check out Tembo¹, they're award-winning, and will guarantee to find you the best deal. (Get 50% off their fee with Nuts About Money too.) Alternatively, visit Habito¹, they're a great free online mortgage broker.

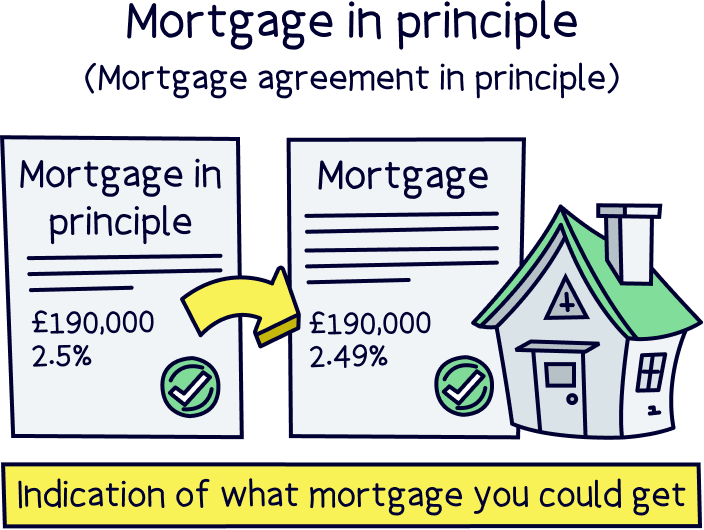

Once you’ve seen what deals are available to you, your mortgage broker will then be able to apply for a mortgage in principle for you. This is a document from a mortgage lender showing how much they think they’d be willing to lend you based on a few straightforward checks.

A mortgage in principle is a great way to get a better idea of whether you’ll get accepted for a mortgage and how big that mortgage could be (although it’s not a guarantee). This will help to guide you in your house hunt, so you don’t go falling in love with a property that you have no chance of being able to afford.

Once you’ve found your dream property, you just need to give your mortgage broker the go-ahead. They can then apply to turn your mortgage in principle into an actual mortgage. Fingers crossed, you pass the final few checks with flying colours and your mortgage offer will drop through your letterbox before you know it.

Hopefully, now you have a rough idea of how much you’ll be able to borrow from a mortgage lender, and how much the monthly payments might be.

Not sure yet? Use the mortgage calculator above, or visit Tembo’s mortgage calculator¹ it only takes a few minutes, and you’ll get the borrowing amount, monthly mortgage repayments and an interest rate.

However all mortgage lenders are different, so when you’re ready to get house hunting, speak to a mortgage advisor, they’ll get you a mortgage in principle, which firms up how much you could borrow and often from a mortgage lender, so it’s a bit more real.

A mortgage advisor will not only find the best mortgage deal for you, given your financial circumstances, but they’ll even sort out the whole mortgage application for you when the time comes, from start to finish. Pretty great right?

There’s only one rule when it comes to mortgage advisors – use a whole-of-market broker! Otherwise, you can’t be sure you’re getting the best mortgage deal for you.

Not sure where to find a broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money.

Alternatively visit Habito¹, a free online mortgage broker. Or view all our recommended mortgage brokers.

It won’t be long before you’re jangling the keys to your brand new home!

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo's service is award-winning, plus they'll find the best mortgage deal from over 20,000 mortgages and even apply for it on your behalf.