Article contents

A joint borrower sole proprietor mortgage is when a parent, friend or family member shares your mortgage with you to help you get on the property ladder.

Desperate to get on the property ladder? Need some help from a parent, friend or family member? 56% of first-time property buyers under the age of 35 have financial help from their mum or dad (according to Legal & General).

A joint borrower sole proprietor mortgage is one way that young people (or anyone struggling to get on the property ladder) can get that leg up they need. Here’s all you need to know.

Tembo will find your best deal, fast, all with award-winning service.

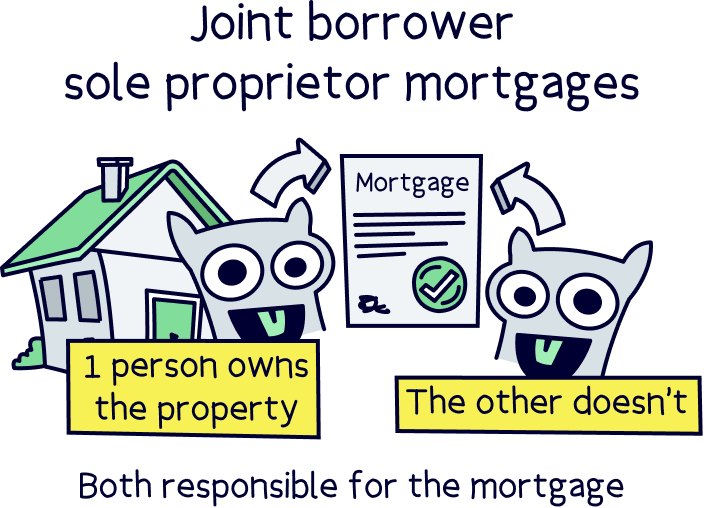

A joint borrower sole proprietor mortgage (also known as a JBSP) is where two or more people share a mortgage but they don’t share the property they're buying. In other words, even though they’re all responsible for paying for the property, only one of them actually owns it.

Huh? Why would anyone want to pay for something they don’t get to own?

Well, it can be really hard for young people to get on the property ladder – especially if they haven’t been in the world of work for long. By taking out a joint borrower sole proprietor mortgage, parents, family members or even friends who are (usually) older and more financially stable can help. Get in!

That said, these aren’t just great for young people. If you’re struggling to get a mortgage because you’re self-employed or you have a bad credit score (a score that shows how good you’ve been with money in the past), a joint borrower sole proprietor mortgage could be the answer. Plus, even though joint borrower sole proprietor mortgages are aimed at first-time buyers, you don’t have to be a first-time buyer to get one. Even if you already own your own home, you may be able to change from a standard mortgage to a joint borrower sole proprietor one if you have a parent or family member who wants to help with your mortgage repayments.

Okay, so here’s the really important bit: with a joint borrower sole proprietor mortgage, even though only one person owns the property, everyone who’s on the mortgage is responsible for keeping up with the monthly repayments.

Let’s say you’ve bought a property with the help of your mum. On a joint borrower sole proprietor mortgage, that means if, for some reason, you don’t pay your mortgage one month, your mum legally has to pay it for you.

Equally, if your mum promised she’d contribute towards the repayments and one month she forgets or decides not to, you’ll legally have to make the whole payment yourself. Good luck with that!

Technically, you can get a joint borrower sole proprietor mortgage with anyone. But let’s be honest: it’s not exactly a great idea to get one with any old randomer you meet in the street! You’ll need to really trust each other and have each other’s backs for it to work.

For this reason, most people who get joint borrower sole proprietor mortgages do it with a parent or family member. Ideally, whoever you choose will also need to be in a better financial position than you are. This way, they can help with two main things:

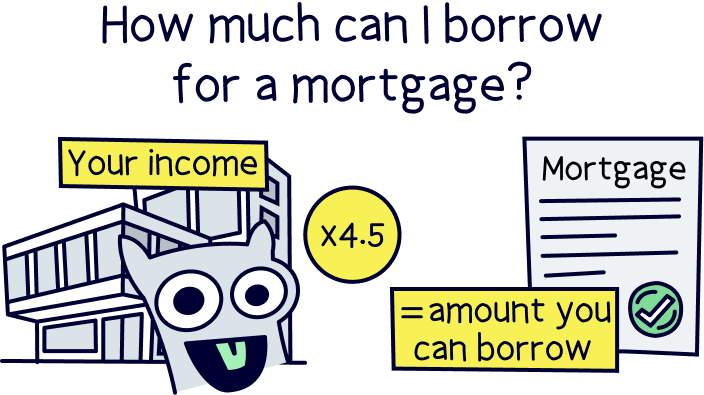

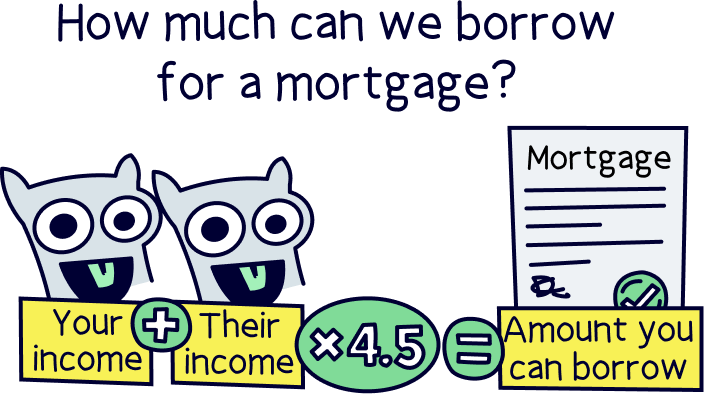

Normally, lenders (the guys that give out mortgages) will let you borrow 4.5 x your yearly income. By teaming up with a family member to get a mortgage, you’ll be able to combine your incomes to borrow more.

For example, say you earn £20,000 per year. On your own, you’d probably be able to borrow around £90,000 (20,000 x 4.5 = 90,000). Now let’s say your family member earns £40,000 per year. Between you, you’ll be earning a yearly income of £60,000 and will probably be able to borrow around £270,000 (60,000 x 4.5 = 270,000). Pass the bubbly!

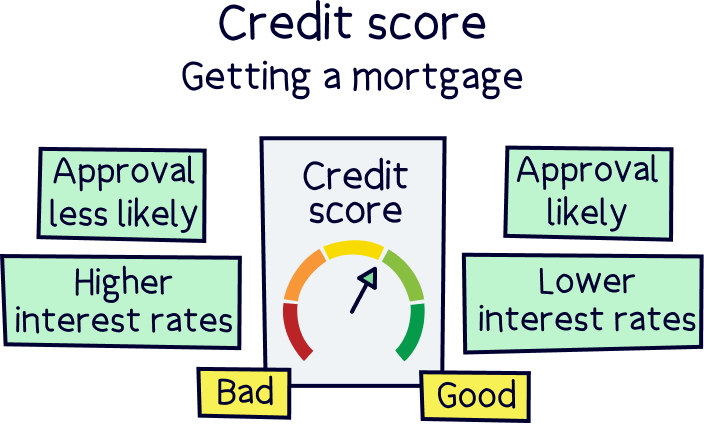

Your credit score is a score that’s used to show how good you are with money. If you have a good credit score, as far as lenders are concerned, it’s a pretty good sign that you’ll pay your mortgage back without a problem. If you have a bad one, however, alarm bells will start ringing.

The problem is that lots of young people haven’t yet had a chance to build up any kind of credit score at all. If that sounds like you (or you’ve got a bad credit score) then teaming up with someone who has years of experience paying off their credit cards and paying their bills on time can help. By putting them on the mortgage alongside you, a lender will feel more confident that they’re going to get their money back.

A joint mortgage is a mortgage that’s shared between two or more people, just like a joint borrower sole proprietor mortgage.

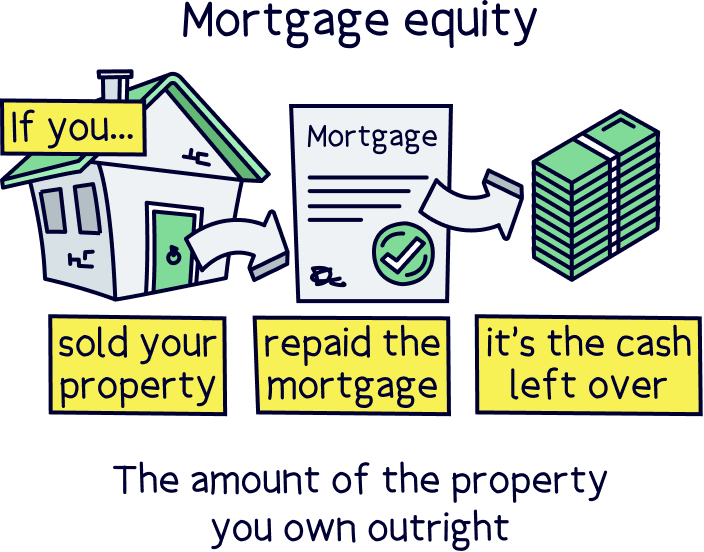

However, with a joint mortgage, the people who get a mortgage together jointly own the property they’re buying. This means that if the property is sold, the equity (the amount you own after you’ve paid back the mortgage) will get split between everyone.

On the other hand, with a joint borrower sole proprietor mortgage, only one person actually owns the property. This means that whoever’s helping you with the mortgage won’t get any money if the property gets sold.

So, which one’s best for you?

Well, it totally depends on your situation and how generous your parents or family members are!

If they want to get a share of the equity once the property gets sold, they might prefer a joint mortgage which will allow them to co-own your home with you. But if they just want to help you get on the property ladder and they’re not interested in making a profit, a joint borrower sole proprietor mortgage could be the perfect fit.

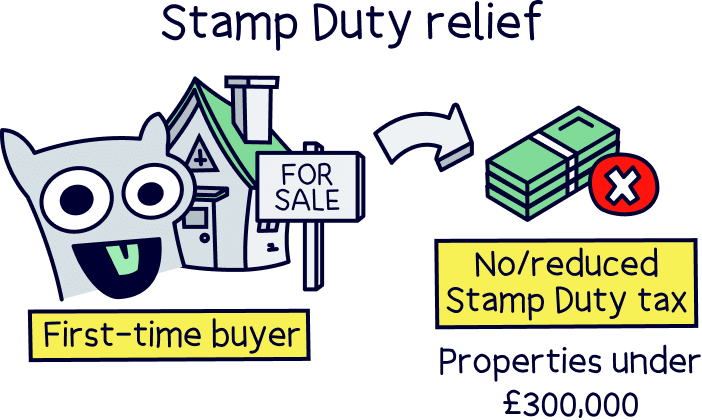

If you’re still umming and ahhing about which one suits you better, it’s also worth factoring in Stamp Duty (a tax that gets charged on property purchases).

Note: first-time buyers don’t have to pay any Stamp Duty if they’re buying a property for less £300,000, thanks to something called Stamp Duty relief. However, if your parent or family member has owned a home before and they get a joint mortgage with you, you won’t qualify for the Stamp Duty relief anymore. Worse still, if they currently own a home, between you, you’ll have to pay 5% Stamp Duty on top of the standard rate on the whole property, because it will count as a second home.

In contrast, with a joint borrower sole proprietor mortgage, they won’t affect the Stamp Duty owed at all, as the property won’t be bought in their name. Phew!

A guarantor mortgage is another kind of mortgage that’s designed for parents and family members to help someone get on the property ladder.

Just like a joint borrower sole proprietor mortgage, your parent or family member (known in this case as your guarantor) won’t legally own the property. But unlike a joint borrower sole proprietor mortgage, they’re only responsible for paying the mortgage if you can’t.

Basically, with a guarantor mortgage, your family member is just there as a plan B.

By promising that they’ll pay the mortgage if you can’t, they’ll give your lender that extra peace of mind that between you, you’ll keep up with the monthly repayments. But in an ideal world, you’ll be paying the mortgage yourself. Your family member is just there in case things go wrong!

Joint borrower sole proprietor mortgages can be total lifesavers if you’re struggling to get a mortgage. But they’re not all roses and sunshine! To help you work out whether they’re right for you, here are the main pros and cons.

Joint borrower sole proprietor mortgages are quite niche, which means they’re not offered by that many lenders. Even the lenders that do offer them will all have different rules about who qualifies.

For example, some lenders will let you take out a joint borrower sole proprietor mortgage with anyone, while others will only lend to you if it’s with a family member. Some will want you to prove that within five years, you’ll be able to afford the mortgage repayments by yourself, while others will be happy to let your parent or family member contribute forever.

They’ll also have different maximum age limits, which could affect the duration of the mortgage you can get (known as your mortgage term). We know, we know, age is just a number. But most mortgage lenders will want everyone on the mortgage to be below a certain age by the time the mortgage ends – often 75 but sometimes up to 85.

To help find the right lender for you, we’d recommend getting a ‘whole-of-market’ mortgage broker involved (also known as a mortgage advisor). Not only can they compare all the deals available from lots of different lenders, but they’ll also be able to fill out the whole application for you and guide you along every step of the way.

Our recommendation for the best broker to help with joint borrower sole proprietor mortgages is:

Get 50% off the standard fee

Tembo is an all-round amazing mortgage broker, in fact, they're award-winning, and not just online.

They can help with pretty much every mortgage out there, from buying a home to switching deals, and on top of that, have unique options to increase your borrowing such as an Income Boost¹ and Deposit Boost¹.

They'll handle the whole mortgage for you too, and the service is great.

Tembo will find your best deal, fast, all with award-winning service.

So, what do you think? Fancy getting your foot firmly on the first rung of the property ladder?!

First things first, have a chat with a parent, family member or friend who you think might be suitable to feel them out. If they’re up for it, then what are you waiting for? Just get in touch with a mortgage broker to start the ball rolling.

You’ll be assembling flat pack furniture in your very own home before you know it. Enjoy!

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.