Article contents

Students can get mortgages but they’ll usually need a guarantor. A guarantor is someone who legally has to pay your mortgage for you if you can’t.

If you’re a student, you’re probably familiar with high rental costs and grotty accommodation. But it doesn’t have to be this way! What if we told you that you could buy your very own place and deck it out just how you want? Here, we’ll look at everything to do with mortgages for students, and how to get one.

Yes! Contrary to what you might think, there’s nothing that says ‘students can’t get mortgages', but it's a lot harder than finding a good student broadband deal or student contents insurance.

That said, getting a mortgage as a student in the UK can be a little tricky. Not because you’re a student exactly, but because as a student, you’re more likely to:

Of course, you might well be a student who has a credit score, has a decent income and has saved up enough money for a meaty deposit. If that’s you, congrats! There’s nothing to stop you from going out and applying for a standard mortgage – after all, you’re not so different from a non-student.

On the other hand, if you’re more like the typical student we’ve described, that’s fine as well. There are a number of mortgage providers who offer mortgages designed just for students like you.

When we talk about a student mortgage, we’re talking about a mortgage for someone who’s in full-time education and aged 18 or over.

But no two lenders or borrowers are the same. So, these deals can look very different. Some lenders offer specific student mortgages, but others may encourage you to take out a less specialised mortgage, such as a ‘guarantor mortgage’ or a ‘family springboard mortgage.’

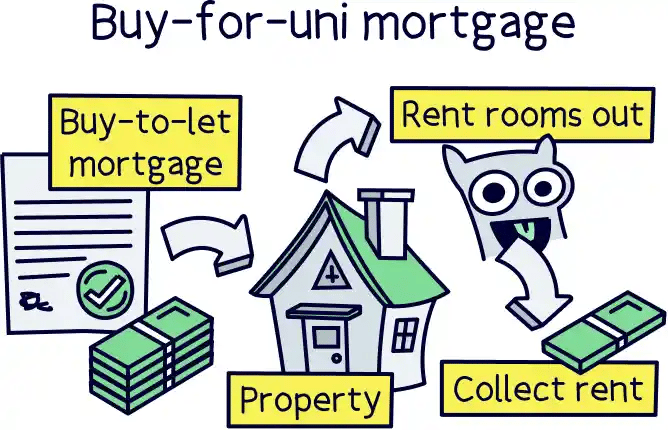

Some lenders even offer ‘buy-for-uni mortgages,’ where they’ll support you to become a live-in student landlord. We’ll look at this in more detail later.

Tembo will find your best deal, fast, all with award-winning service.

Mortgage lenders usually want to know that you’re making enough money to keep up your monthly repayments. That’s not easy if you’re in full-time education!

So, how can you convince lenders that you’ll pay it back? Here are two things you can do to make it more likely that you’ll get accepted for a student mortgage in the UK.

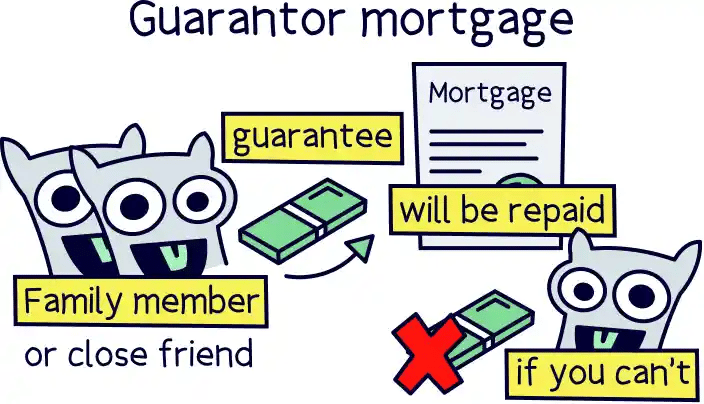

A guarantor is someone who agrees to pay your mortgage for you if you can’t. It’s a great way to persuade a lender to approve you for a mortgage as it means they’re likely to get their money back even if you can’t keep up the mortgage repayments yourself.

BUT asking someone to be your guarantor is a pretty big deal. Usually, they’ll have to use their own home as ‘security.’ This means that if neither of you can keep up the monthly repayments, their property could be seized. Eek!

For that reason, your guarantor will typically be someone who trusts you completely, like a parent, grandparent or legal guardian. Normally, your guarantor will also have to be someone who:

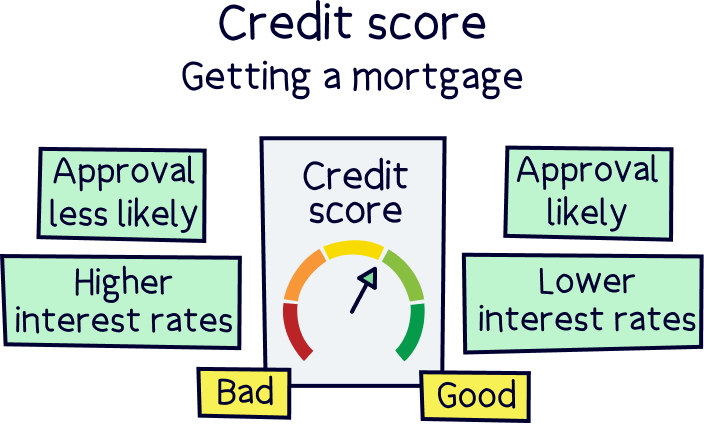

Most mortgage lenders will do checks on your guarantor to make sure that they have a decent credit score and that they can afford the mortgage repayments (in case you can’t).

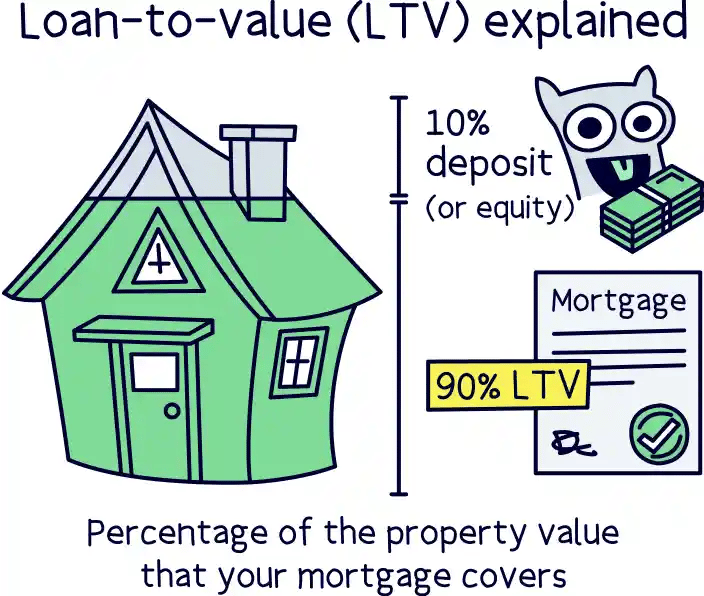

The relationship between the amount you want to borrow and the amount you’re paying upfront is known as the loan-to-value ratio (or LTV).

For example, if you want to buy a house that’s worth £200,000 and you’ve saved a £20,000 deposit, you’ll need to borrow £180,000. This means an LTV of 90% (because you’re borrowing 90% of the property’s value and paying 10% upfront).

In short, the more you can pay upfront, the more likely you are to get a mortgage. Think about it: putting down a big deposit shows mortgage lenders that you’re a serious buyer. It also means you’re taking on a bigger share of the risk.

That said, there are some building societies and banks that offer students a 100% LTV. Just bear in mind that the interest rates will usually be very high (which means you’ll end up paying more overall). Plus, you’ll generally need a guarantor that lenders are super happy with for one of these because otherwise it’s a big risk for lenders.

At the end of the day, if you put down a deposit, you’ll get access to a much bigger choice of mortgage products and deals – especially if you can put down a large one!

A buy-for-uni mortgage is essentially a buy-to-let mortgage for students. In other words, it allows you to buy a property as a student and then rent out the spare rooms to help cover the cost of your mortgage repayments.

This kind of mortgage can be a great way to get on the property ladder and potentially even make some money while you’re at it. The Guardian recently shone a spotlight on a student who stands to make at least £30,000 this way.

But how achievable is it?

Well, if you have a guarantor, you could borrow up to 100% of the house’s value. So, it’s pretty achievable even for a penniless student (as long as you’re lucky enough to have a guarantor who can afford to put their house on the line for you!).

That said, you’ll still need to tick certain boxes. For example, to qualify for a student buy-to-let mortgage with Loughborough Building Society, you’ll need to:

That doesn’t sound too bad, right? But before you jump in at the deep end, take a second to think it through a little further.

Buying a house is a big responsibility, and being a landlord can be pretty stressful. You’ll need to make sure your housemates pay their rent on time, and there’s quite a bit of admin involved.

Not only that, but buy-for-uni mortgages tend to come with high interest rates – in 2022, they were generally between 4.4% and 4.6%. Take our word for it when we say that’s a lot higher than normal!

Don’t get us wrong, this could be a great opportunity. Just think it through carefully first.

If you’re umming and ah-ing about whether to take the leap and get a student mortgage, we’re here to help. Here are some pros and cons.

If you’re a PhD student, there’s no reason why you couldn’t get a student mortgage in the same way as an undergrad. However, if you’re hoping to use your PhD stipend as a proof of income instead of using a guarantor, you might find it a little tricky.

Why? Well, you’ll only be receiving your stipend for a set period of time. So, you might not have enough money to keep up your monthly repayments once your PhD is finished. Don’t worry, we’re not trying to scare you. It’s just your mortgage lender will want some guarantees they’re going to get their money back (this isn’t too different from getting a mortgage as a fixed-term contractor).

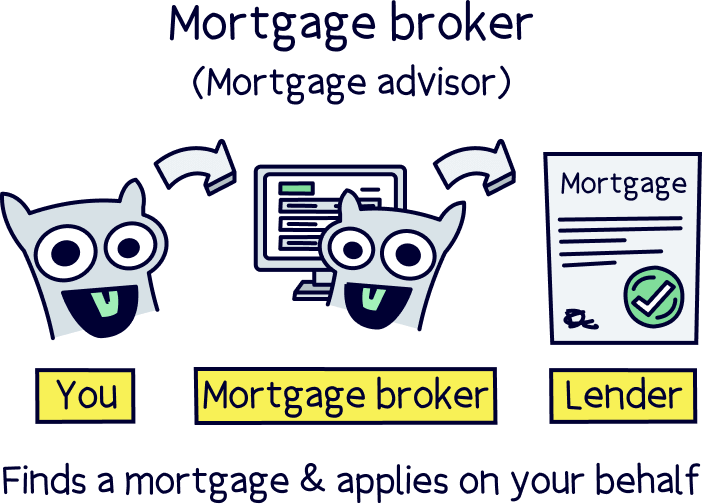

A lender might be more likely to approve you for a mortgage if you’re doing some teaching on the side or some other part-time work. Ultimately, your best bet is getting in touch with a mortgage broker to talk everything through and find out whether there’s a lender who’s likely to offer you a mortgage.

Everyone is different. So, without looking through your bank statements and getting on the phone to your mum or dad (assuming they’ve agreed to be a guarantor) it’s impossible to say which student mortgage provider would be best for you.

However, here are a few lenders who are known for offering mortgages for students in the UK:

Don’t forget that there are over 100 mortgage providers in the UK. Much as we’d love to, we can’t list them all! Lots of mainstream providers offer first-time mortgages or guarantor mortgages that are open to students, but it all depends on your individual circumstances.

To find the best mortgage provider for you, make sure you chat to a mortgage broker. A broker will take the time to get to know your needs and will be able to recommend the best lenders and deals for you. They’ll even take care of the whole application process from start to finish (there’s a reason we call them lifesavers!).

As you can see, getting a mortgage as a student is a lot more achievable than you might think. So, what are you waiting for?

If there’s someone in your life who you think might be willing to act as a guarantor, it might just be worth asking the question. Then, if it’s a yes, get a mortgage broker to guide you through the whole process.

Our recommendation for a mortgage advisor who specialises in student mortgages is Tembo¹, and they've got award-winning service. You'll also get 50% off their fee with Nuts About Money.

Get 50% off the standard fee

Tembo is an all-round amazing mortgage broker, in fact, they're award-winning, and not just online.

They can help with pretty much every mortgage out there, from buying a home to switching deals, and on top of that, have unique options to increase your borrowing such as an Income Boost¹ and Deposit Boost¹.

They'll handle the whole mortgage for you too, and the service is great.

Habito will find the best mortgage for you, all for free, and with great service. But better than that, if you’re buying a home, they’ll handle the whole process for you – that’s the legal work and survey, and everything else. It’s a huge stress and time saver, and comes at a great price.

Habito is run by Monzo, which is a very large and successful modern bank (often called a mobile bank).

Tembo will find your best deal, fast, all with award-winning service.

Fingers crossed, you could be jangling the keys to your very own home before you know it!

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.