Article contents

It couldn’t be easier to protect your stuff and get peace of mind at Uni. You could be all sorted with a great deal in a few minutes. All you need to decide is how much protection you’d like!

Heading off to university for the first time? Or just getting ready to return for another year? You probably have a to-do list as long as your arm, but make sure to add ‘contents insurance’ to your list – it’s a lifesaver for replacing all your expensive possessions should you lose them or get stolen, such as your all-important laptop – especially after you’ve spent all your cash in freshers week!

Here’s a quick run through of what student contents insurance actually is, and how to get the best deal.

Contents insurance for students, also known as renters insurance and simply home insurance, is protection for all of the stuff you take to university - your mobile, your laptop, your clothes - that kind of thing.

Insurance is peace of mind for you, that if anything happens to your stuff, like fire damage, flood damage, theft, or accidental damage, you’ll get some cash to cover the cost of replacing them, or simply just given a brand new replacement.

Sounds pretty sensible so far, right? But why do students need it?

Whether you’re living in halls or in private accommodation (that’s a fancy way of saying a student house with a landlord), you’ll want to get contents insurance because:

1. You will be living with and meeting a lot of new people, especially if it’s your first year at university. And you may have new people round your pad all the time for drinks and parties. This can obviously be a lot of fun, but it does mean that you might have the odd thing or two go missing – sadly not everyone is as honest as you are.

2. Unfortunately, burglary can be slightly more common in student accommodation. Large groups of young students often bring large numbers of valuable items with them – in other words, the jackpot for burglars and thieves. But don’t panic, it’s still incredibly rare.

3. You’re moving away from your family home. Previously you might have been protected by your parent's or legal guardian's insurance policy, but now you’re independent, you’ll have to start doing adult stuff yourself. Sigh!

However, in some cases, you might actually remain covered by your parents and their contents insurance - it all depends on their insurance plan. It’s worth checking in with them (and their insurer) before sorting your own insurance policy - some might call this ‘sponging’, but we prefer the term ‘being savvy’!

Some universities will provide basic contents insurance in student halls, how handy! And it normally covers the communal areas as well as your room.

However, this insurance is often limited to specific items, so you might not be fully covered if you have some more unusual things such as musical instruments. So check in with your university when you get the chance, it might save you a few pennies!

You have a big decision to make, should you just get contents insurance for just your room or should you get contents insurance for everyone and the whole house? (And normally split the bill between you).

It’s entirely up to you and your relationship with your housemates, but if you’re all happy to pay your fair share (luckily contents insurance isn’t expensive), then you might just want to insure the whole house on one policy, saving the admin work for everyone and you’ll get all the bedrooms, plus the communal rooms insured too!

This will vary depending on your policy, but the majority of your belongings will usually be covered. This includes things like:

Sometimes you may need to ‘list’ (mention to the insurer) high-value items, just so they’re covered properly. Usually this includes items worth more than £1,000 - often things like jewellery/watches, laptops and bikes.

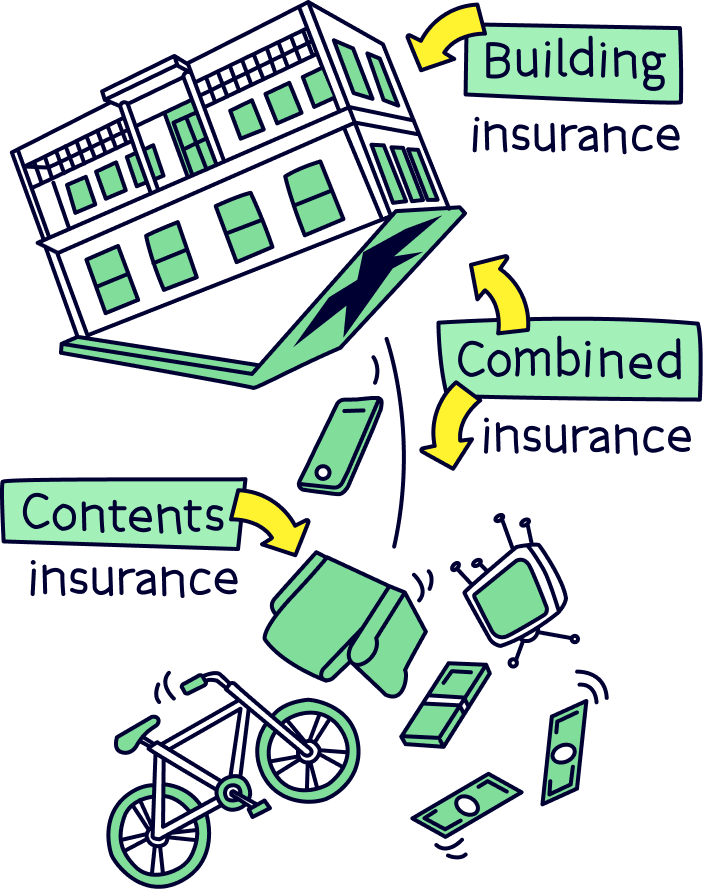

Nuts About Money tip: If you turned your house upside down everything that would fall out is contents insurance. Everything still inside the house is called 'Building insurance'.

With basic contents insurance your items are only covered while they’re in your home. This means that if your laptop or mobile is stolen in the library or coffee shop, for example, then you won’t be covered.

The good news is that you can get cover for all your gear outside of your house with a more comprehensive plan. It’s slightly more expensive per month, but very much worth it.

There are also some more specific insurance add-ons that you might want to consider:

Let’s quickly clear up some common insurance jargon you might come across so you can be confident when shopping for the right deal.

Premium: this is just a fancy word for the price of your insurance.

Policy: this is the insurance plan itself; what’s covered and all the details of how it’s covered.

Claim: if anything ever happens to your insured items - you’re essentially asking your insurer to pay out compensation based on your policy. For example, let’s say your mobile phone is covered by your contents insurance, and is then stolen, you’d raise a claim with your insurer.

Excess: this is the amount of money you would have to pay out if you ever make a claim. For example, let’s say you have a bike covered for £500, and you’ve agreed to a £50 excess, if your bike is stolen or damaged, you’ll be paid out £450 by the insurance company, and you’ll cover the remaining £50 with your excess.

Why would you ever choose to pay a higher excess? Good question!

A higher excess usually means you’ll be paying a lower premium (cost) for your insurance. That’s because you’re taking on more ‘risk’ in the event that you need to make a claim, and volunteering to pay more towards any compensation costs.

On the other hand, a lower excess usually means you’ll be paying a higher premium. That’s because you’re taking on less ‘risk’, and the insurer is paying out more for any claims, and so they balance this by charging you a higher premium.

If you’re someone prone to losing or damaging their possessions, for example, then you might prefer to pay a higher premium, and keep your excess to a minimum. That way, the insurer will cover more of the costs if you ever need to make a claim.

In most cases, your insurer will require a compulsory excess (i.e. the minimum you’ll need to contribute) and also offer a voluntary excess – you can increase your voluntary excess in return for a lower premium.

There’s a lot of insurance providers out there, so it can be tricky to know where to start, but luckily for you, you’re reading this!

Follow these 3 steps and you’ll be covered in no time and be sure you’ll be on the best deal for you.

Have a look on the comparison sites below – all you need to do is put in a few details and they’ll search a wide range of providers in a few seconds and show you the best options out there.

They all search slightly different providers so if you’ve got a bit more time, check all of them. We’ve ordered them so you’ll typically find the best deals and speedier sites first, so if time’s an issue just check the top one or two.

Our recommended provider for students contents insurance is Getsafe. The cover is great, it's quick and super cheap.

Get £20 off when you sign up with Nuts About Money.

Designed for renters – monthly rolling contracts, covers the whole house (including landlords furniture), up to £40,000 worth of stuff, and best of all protects 6 unrelated people, inside and outside the home. Starts at £5 per month too.

Searches a wide range of providers (up to 66), only takes a few minutes and you could save up to £181.

Our recommended provider for students contents insurance is Getsafe. The cover is great, it's quick and super cheap.

Sometimes providers don’t like to give comparison sites access to their deals, they want customers to come directly to them. How inconvenient!

For contents insurance, the only one worth checking is Direct Line. They can sometimes offer competitive deals so it’s worth checking if you’ve got time.

We love companies taking on entire industries, they often offer much better service than bigger companies and are super competitive with their prices! And luckily for you, there’s a great one taking on the contents insurance industry… Getsafe!

It’s contents insurance, buildings insurance, or both, called home insurance, made to suit you. It’s super low cost – you start with basic cover and just add what you need. As simple as that. It’s easy to set up, all from your phone or their website. You can’t go wrong. Get a quick quote on their website too.

Our recommended provider for students contents insurance is Getsafe. The cover is great, it's quick and super cheap.

You might have seeon the comparison sites but favoured bigger brands, or a comparison site might not have access to their deals. But it’s worth getting a quote directly from them, it only takes a few minutes.

The cover is designed for renters, so it covers the whole house, includes protection for you and up to 6 unrelated people, plus the landlord's items and furniture (tenants liability cover), and all of your items outside of the home too.

Plus it’s all online and takes just a few minutes, so no awkward phone calls and being on hold. And the prices are good.

And there you have it, it’s super easy to get contents insurance for your student home, no stress and no anxiety needed, you can relax and feel assured that if anything should happen you’re protected. Another adult thing done and dusted.

And once it’s sorted out, you can focus on other important uni stuff – like finding the student union… Cheers!

Our recommended provider for students contents insurance is Getsafe. The cover is great, it's quick and super cheap.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things insurance, with many years of combined experience writing and talking about the range of insurance cover available. Some of our team were top financial advisors. We understand the ins and outs of insurance, how to communicate insurance in an easy to understand way (we hope you agree), and of course, how to get the best insurance deal for you.

More than 10 years of combined experience researching and writing about insurance

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of insurance companies researched and reviewed

We follow a strict editorial code to ensure you get the best information possible

Our recommended provider for students contents insurance is Getsafe. The cover is great, it's quick and super cheap.