Article contents

Contents insurance is a special kind of insurance that protects your belongings at home. You make payments every month or year and in return, your insurance will pay to repair or replace your possessions if they’re damaged or stolen.

We know that insurance might sound boring. But if something bad happens to your belongings while they’re at home, contents insurance will suddenly sound like the most exciting thing in the world!

Here, we’ll tell you everything you need to know about contents insurance, from why it’s so great to what it costs and how much you need. But first…

Contents insurance is a special kind of insurance that protects your belongings if they’re damaged or get stolen at home.

Wondering what insurance is in the first place? Well, an insurance policy is a contract where you agree to pay money to an insurance provider and in return, they agree to fork out if something happens to whatever you’ve insured.

There are lots of different kinds of insurance. You can get pet insurance, which covers your vet bills if your pet gets poorly. You can get travel insurance, which covers the cost if something bad happens while you’re abroad. And you can get home insurance, which covers the cost if something happens to your home or the contents inside it.

Contents insurance is a type of home insurance which covers your belongings while they’re at home (or in your shed or garage). You pay money every month or year, called your insurance premium. Then, if any of your belongings are damaged, you can ask your insurance provider to cover the cost of repairing or replacing them, called making a claim. You’ll just have to contribute a bit of money towards it which is set in advance, called your excess.

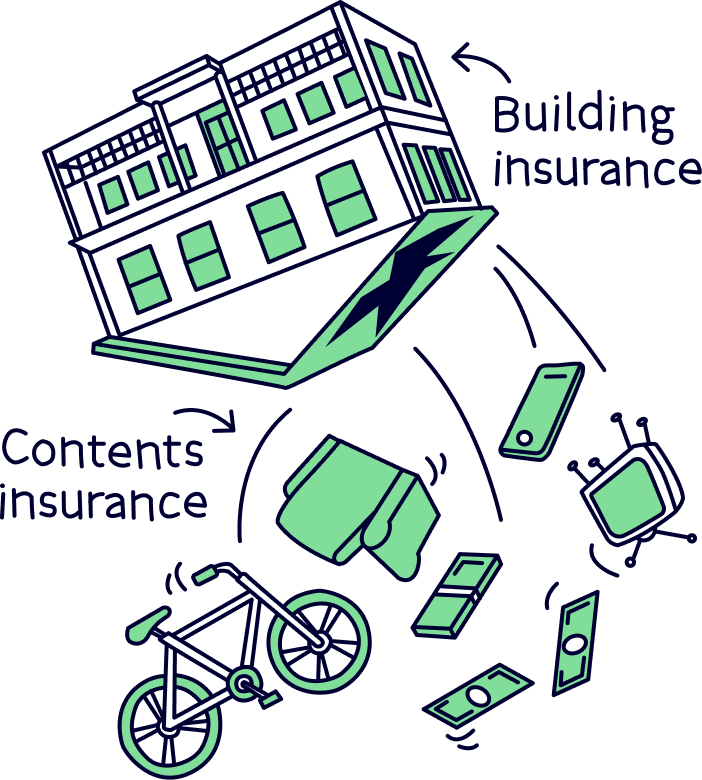

Every contents insurance policy is different, so it’s really important to check your policy carefully to see what’s included in yours. However, as a general rule of thumb, imagine you turned your house upside down. Contents insurance will normally cover any belongings that would fall out – so things like your electronic devices, furniture, books and clothes.

On the other hand, anything that would be left in the house will normally be covered by a different type of home insurance called buildings insurance – that includes your building’s structure and permanent fixtures and fittings..

Contents insurance will normally also cover…

Exactly what is covered and when will vary between policies, so it’s super important to check what yours covers. But most will pay out if the damage is caused by something unexpected, like a burglary, explosion, fire, flooding, riot, storm or by vandalism.

Now, as great as contents insurance is, there are some things that it won’t cover. Here’s the lowdown.

Are you subletting (where you rent out some or all of your home to someone else)? Or renting a room in a larger house share? If the answer’s yes to either of these questions then bear in mind that some burglaries may also not be covered.

Basically, if your home is burgled but there are no signs of forced entry, your insurance provider may refuse to pay out as there won’t be any proof that someone actually broke in from the outside.

Always let your insurance provider know as soon as possible if you’re subletting so you can make sure you’re as protected as you can be. Or, if you live in a houseshare, check out our guide to what home insurance you need if you rent – here, we’ll help you decide whether you should get insurance for the whole home or just for your room. We’d also recommend checking out Urban Jungle¹, a contents insurance provider that’s great for renters.

Contents insurance costs on average £57 per year in the UK. That’s just £4.75 per month! These costs (known as premiums) are from MoneySuperMarket’s UK price index.

That said, your exact cost will depend on lots of different things, like where you live, how much your belongings are worth and how high you want your excess to be. Remember, your excess is the amount you have to pay when you make a claim. The higher your excess is, the lower your monthly or yearly cost will be but the more you’ll end up paying if your items are damaged.

If you’re wondering whether or not contents insurance is worth it, we’d say yes every time! Of course, even £4.75 a month is a cost you’ll want to avoid paying if you don’t need to. But this is a very small amount compared to what you’d have to pay to replace all your belongings if they were destroyed in a fire and you didn’t have contents insurance to protect them!

Of course, there are some things that money can’t replace, like your kids’ drawings, your diary or your 50-metre swimming badge. But at least contents insurance can give you peace of mind that, if something bad happens, you’ll be able to replace all those non-sentimental items that will help you move on with your life.

Remember how we said that buildings insurance is another type of home insurance that protects your building’s structure and its permanent fixtures and fittings? Well, on its own, buildings insurance costs £111 per year on average (according to the UK price index we mentioned earlier). That works out at £9.25 per month.

It’s more expensive than contents insurance as usually, it will cost more to rebuild your home if it’s destroyed than what it would cost to replace the items within it.

Anyway, if you need both buildings and contents insurance, it’s usually cheapest to get something called combined insurance. That’s a policy that includes both buildings insurance and contents insurance in one. According to the UK price index, the average cost of combined insurance is £140 per year (£11.70).

Okay, so first things first, you don’t legally need any kind of home insurance at all. But even though you might not technically need it, that doesn’t mean it’s not a good idea.

First, let’s look at contents insurance. If you had to replace your belongings, it would probably cost a lot more than what you think, as you’d most likely need to buy new versions of everything. This could be really tricky for most people to afford in one go.

Contents insurance will give you the peace of mind that, whether just one item or all your belongings are destroyed, you’ll have the funds you need to repair or replace them. In this way, you’re protecting everything you’ve worked hard for.

Now for buildings insurance. Whether you need to consider it or not will depend on whether or not you own your home. If you’re renting, you won’t need buildings insurance as your building’s structure will be your landlord’s responsibility.

If you’re a homeowner and you have a mortgage, on the other hand, you will need to get buildings insurance. This is because mortgage lenders won’t normally give you a mortgage without it. However, whether you have a mortgage or not, buildings insurance is really important.

Consider what would happen if your house was destroyed in a fire or flood. Without buildings insurance, you probably wouldn’t be able to afford to rebuild your home, which could leave you in a really difficult situation. In other words, buildings insurance might not be legally necessary, but trust us: if you’re a homeowner, you don’t want to be without it!

Nobody likes paying more than they have to! So, we bet you’re wondering how you can make sure you’re keeping your contents insurance costs as low as possible. Here are some simple steps you can take to nail it.

Instead of buying your contents insurance at the last minute, try to buy it around 3 weeks before you need your cover to start. This could save you around 20%.

The absolute best time to get your contents insurance is 21 days in advance. But if you spot a good deal that you want to bagsy, you could get it even earlier. A lot of insurance providers (like Aviva and Churchill) will be happy to agree a price with you up to 90 days before you want your insurance to start.

This step won’t apply to you if you’re renting. But if you own your own home, you’re likely to get a cheaper deal by buying combined insurance (which rolls both contents insurance and buildings insurance into one) instead of splashing out on contents and buildings insurance separately.

As an added bonus, getting protection for both your contents and building from the same provider will help to avoid arguments about who should pay when your policies overlap. And it’ll mean you only have to report damage to 1 provider instead of 2 if there’s an accident that affects both your building and possessions – so you’ll save on admin too!

When you get your contents insurance, your provider will ask you how much all your belongings added together are worth. It’s really important that you don’t underestimate this as it could mean you’re not able to claim enough to replace them all if they get destroyed.

Most importantly, think about how much it would cost to replace your belongings with brand new ones, rather than going off what you think your belongings might sell for used. We’ll look at how much contents insurance you might need in a bit.

Sometimes, you can get a discount if you get your contents insurance policy and your car insurance policy from the same provider. Most of the time, you just need to tell your insurance provider you’ve already got an insurance policy with them and they’ll give you a discount on the second policy you take out. So it’s really easy and you don’t even need to get both insurance policies at the same time if you don’t want to!

Just make sure that you still compare costs. You never know, it might still be cheaper overall to get your contents insurance and car insurance from different providers!

Often, insurance providers will try to sell you extras when you’re buying your insurance policy, known as ‘add-ons.’ And they’re normally really good at it! Just be careful that you don’t get drawn into paying for any add-ons you don’t actually need.

Look carefully at what’s already included in the standard insurance policy and avoid doubling up. For example, if you have kids, you might think that an ‘accidental damage’ add-on would be a good idea so that you can replace anything your children break at home. But many standard contents insurance policies cover this as standard, even though they often won’t cover kinds of accidental damage like accidents caused by pets.

Most insurance providers will ask you what kind of locks you have before giving you a quote, as this will affect how easy it is for someone to burgle you. And guess what? Splashing on locks that are more secure can reduce your insurance costs.

To save money, use the Master Locksmiths Association to find a locksmith and ask them to install a 5-lever mortice deadlock that conforms to British Standard 3621. That might sound like gobbledigook, but it’s basically a really secure lock that insurers and the police love.

It’s important to be honest about what kind of locks you have as, if you put down the wrong one and you get burgled, your provider might refuse to pay out. Use this handy guide to work out what kind of locks you have.

This one only really applies if you already have insurance, rather than if you’re hunting for a deal for the first time. Basically, insurance providers are a bit cheeky and they don’t really want you to make a claim. After all, they don’t really enjoy giving you money!

Because of this, if you don’t make a claim for more than a year, they’ll normally give you a discount on your insurance the next year, known as a no claims bonus. In contrast, if you do make a claim, they’ll often see you as a more expensive customer and will charge you more accordingly. Urgh!

Don’t get us wrong, we’re not saying you shouldn’t claim on your insurance – that’s what it’s there for after all! Instead, we’re just saying that if there’s only a small amount of damage that won’t cost much to repair, it might not be worth making a claim as you’d lose your discount and may end up paying more in the long run.

Similarly, remember that you’ll have to pay a contribution when you make a claim, known as your excess. If your excess is high and repair or replacement costs are low, it might not be worth making a claim.

Remember how we said that you’ll need to work out how much your items are worth all added together when you get contents insurance? Well, this is so that you can work out how much cover to get. Too little and your insurance provider won’t give you enough money to cover your damaged items. Too much and you’ll end up paying for cover that you don’t really need.

Stats released by Admiral show that people tend to underestimate how much their possessions are worth by as much as 45%! Underinsuring by this amount can be a real problem.

First, if all your possessions are damaged, you’ll only get 45% of the money you need to replace them. But secondly, even if only 1 item is damaged – your TV, for example – you’ll only get 45% of the cost of that item from your insurance provider, known as the ‘averages clause.’

So, how much contents insurance should you have?

Well this will depend on how big your house is, how many items you have in each room and how much it would cost to replace them all with brand new versions. The average contents value for a 3-bed house is around £41,000 according to insurance provider Admiral.

On top of the value of your items, you’ll need to think about how much it would cost to stay in a hotel or somewhere similar if your home becomes uninhabitable for a while.

Luckily, you don’t have to walk around with a pen and paper doing complicated calculations – our friends at Urban Jungle have got a handy calculator you can use to make things quick and easy!

Now you know all there is to know about contents insurance. Hooray! But you don’t yet know how to actually get it!

Here’s how to get a great deal on your contents insurance.

First things first, compare different insurance providers and deals using some of the top comparison sites. This is probably the best way to get a really good idea of what’s available and at what cost.

Wondering why we’ve recommended using more than one? Well, it’s because these sites won’t all show exactly the same deals.

If you’re a bargain hunter keen to get the very best price, we’d recommend using a couple. Here's the best for contents insurance:

Our recommended provider for contents insurance is Urban Jungle. The cover is great, it's quick and super cheap. Plus, get £20 in free credit.

Get £20 off when you sign up with Nuts About Money.

The perfect contents insurance – monthly rolling contracts, covers the whole house (including landlords furniture), up to £40,000 worth of stuff, and best of all protects 6 unrelated people, inside and outside the home. Starts at £5 per month too.

Searches 65 different providers and get a freebie voucher if you buy.

Good range of providers, and get Meerkat Meals – discount on takeaways and eating out.

Our recommended provider for contents insurance is Urban Jungle. The cover is great, it's quick and super cheap. Plus, get £20 in free credit.

Some providers won’t show up on comparison sites at all, as they’d rather have customers go straight to them. By checking some of these providers too, you’ll give yourself the best possible chance of getting the very best deal.

The only direct-only provider we’d recommend checking when it comes to contents insurance is Direct Line. They’ve often got good deals, so get a quote on their website and compare it to the other quotes you’ve uncovered on comparison sites.

Sometimes, it helps to get a recommendation from a friend, family member or… us! If you want our tuppence, we love Urban Jungle for contents insurance.

Get £20 off when you sign up with Nuts About Money.

The perfect contents insurance – monthly rolling contracts, covers the whole house (including landlords furniture), up to £40,000 worth of stuff, and best of all protects 6 unrelated people, inside and outside the home. Starts at £5 per month too.

Our recommended provider for contents insurance is Urban Jungle. The cover is great, it's quick and super cheap. Plus, get £20 in free credit.

Great for people who rent as well as for people who own their home, Urban Jungle is all about fair prices, monthly rolling plans (so you don’t have to be tied in for a whole year) and no hidden fees. At Nuts About Money, we love young companies who are taking on the big, bad insurance providers so we hope you’ll love Urban Jungle as much as we do!

Found a deal you like? Well, we bet you’d like it even more if you could get a discount on it! If you’re feeling brave enough, now’s the time to get on the phone to your insurance provider or start typing into the live chat to ask if they could give you a special deal.

We’re not going to lie, it doesn’t work every time. But it does work occasionally so, if you’re in the mood, it’s definitely worth a try!

Finally, make sure to triple, quadruple check that you’re happy with the policy you’re buying before you get trigger-happy. Brush up on exactly what your contents insurance policy includes and make sure it covers everything you need.

Check you’re happy not just with the premium (your yearly or monthly cost) but also the excess (how much you’ll have to contribute if you make a claim). It’s true that a higher excess can lead to a lower upfront cost, but at the end of the day, there’s no point in getting insurance if you’re not going to be able to afford to use it when things go wrong!

Totally happy? In which case, all that’s left is to set a date for your cover to start or start it straight away. Enjoy your newfound peace of mind!

Home is where the heart is. So, it makes sense to protect all those things that make your home what it is.

Of course, if anything happens to your belongings, it’ll always be devastating – especially as there are some sentimental things that insurance can’t replace (your kid’s first tooth or that letter from your nan, for example). But it would be even more devastating to find yourself without the funds you need to repair and replace all those objects that money can buy. Just follow our steps above to get protected and buy yourself that all-important peace of mind.

Our recommended provider for contents insurance is Urban Jungle. The cover is great, it's quick and super cheap. Plus, get £20 in free credit.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things insurance, with many years of combined experience writing and talking about the range of insurance cover available. Some of our team were top financial advisors. We understand the ins and outs of insurance, how to communicate insurance in an easy to understand way (we hope you agree), and of course, how to get the best insurance deal for you.

More than 10 years of combined experience researching and writing about insurance

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of insurance companies researched and reviewed

We follow a strict editorial code to ensure you get the best information possible

Our recommended provider for contents insurance is Urban Jungle. The cover is great, it's quick and super cheap. Plus, get £20 in free credit.