Article contents

Home insurance is a special kind of insurance that protects your home and its contents from damage. You pay some money every month or year and in return, your insurance provider will pay if your home or belongings are damaged.

What is home insurance? How much does it cost? And do you need it?!

If you’ve been wondering what the deal is with home insurance, you’re in the right place. Here, we’ll answer all your questions to make you into a total pro when it comes to protecting your home from damage.

Home insurance is a special kind of insurance that protects your home and the contents inside it.

Let’s rewind a little bit. There are these people called insurance providers who sell contracts called ‘insurance policies.’ These contracts are a bit like a mobile phone contract or an energy contract. But instead of getting 4G or energy, you’re getting protection for your home.

With a home insurance policy, you normally have to pay a little bit every month or year, called an insurance premium. Then, if something happens to your home or the contents inside it, you can tell your insurance provider and ask them to cover the cost, called ‘making a claim’ (just bear in mind that you’ll still need to contribute a little bit yourself, known as your ‘excess’).

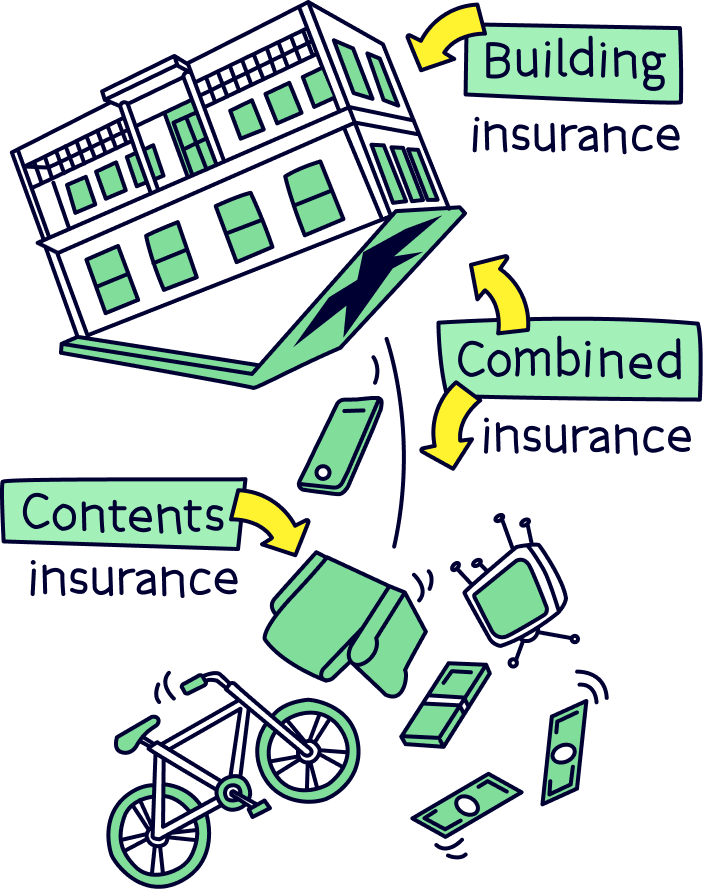

There are 3 main types of home insurance:

Every home insurance policy is different. So, it’s impossible to say for sure exactly what your home insurance will cover. Sorry!

That said, most home insurance policies will cover unexpected damage caused by things like:

We mean, hopefully, the chances of earthquakes or riots destroying your home and belongings are small, but you never know!

As well as paying to fix damage caused by these issues, home insurance could pay for you to stay in a hotel or B&B if you can’t stay in your home. It will also pay for replacement keys and locks if yours are damaged, and even replace any cash that gets stolen from your home (that said, there are limits to how much you can claim for, so check your policy carefully if you’re planning on hiding heaps of cash under your mattress!).

Both contents and buildings insurance can also protect you legally in case your home causes damage to someone else. This is known as legal liability protection. Don’t worry, it’s not as complicated as it sounds!

Imagine someone comes to your home and seriously hurts themselves by tripping up on a corner of your rug. If it’s found to be your fault, your contents insurance will cover the costs, including paying for a lawyer for you. Now imagine your chimney stack falls from your building and seriously injures a passerby or damages your neighbour’s home. In this case, your buildings insurance will do the same thing.

As you can see, home insurance covers lots of stuff. But before you get too excited thinking that you can claim left, right and centre, there are some things that it won’t cover. Here are the main ones.

So, do you actually need home insurance? Well, the simple answer is no. It’s not a legal requirement.

That said, a lot of it will depend on whether you own your own home. If you do and you have a mortgage, you probably will need at least buildings insurance. This is because mortgage lenders (the people who give out mortgages) normally won’t give you a mortgage without it.

Even if you don’t have a mortgage though, we’d strongly recommend getting buildings insurance if you own your home. Your property is probably the most valuable thing you own. Imagine if something happens to it – not only would you lose your home, but you’d lose all the money you’ve invested in it too!

If you rent, on the other hand, you won’t normally need to worry about buildings insurance at all as your building’s structure is the responsibility of your landlord. However, the contents of your home will still be your responsibility so we’d still recommend getting contents insurance.

Think about it: your home probably contains all your most precious belongings. And, no matter how careful you are, there’s always a chance that something unexpected could happen.

Contents insurance will give you peace of mind that, if the worst happens, you’ll be able to repair or replace all those things that you care most about. Plus, it’s usually really cheap! Which brings us onto...

Wondering how much home insurance costs on average? Well, that depends on what kind of home insurance we’re talking about. For combined insurance (buildings and contents insurance together), the average cost is £140 per year. That works out at just £11.70 per month!

On the other hand, if you want buildings insurance by itself, that will cost on average £111 (£9.25 per month). And contents insurance by itself costs around £57 (£4.75 per month).

These costs (known as insurance premiums) are all based on prices from the second 3 months of 2021, according to MoneySuperMarket’s UK price index.

So, how much will you end up paying for your home insurance? Well, your home insurance cost (or premium!) will depend on lots of different factors. Just a few are where you live, how old you are, how valuable your possessions are (if you’re getting contents insurance) and how much your home would cost to rebuild (if you’re getting buildings insurance).

If you want to get a good idea about how much you can expect to pay for your home insurance, just follow the simple steps in our how to get home insurance section below.

Your home insurance cost (or premium!) can also change as time goes on. Firstly, if you don’t make a claim over 12 months, you can normally get a discount on your insurance provider’s price the next year. This is known as a ‘no claims discount.’ On the other hand, if you do make a claim, your costs will normally go up.

Most home insurance providers will also hike up your prices up each year regardless. Basically, they reel you in with a cheap deal and then put your prices up, hoping that you either don’t notice or that you can’t be bothered to switch. How cheeky is that?!

Since you’ll usually get the best prices as a new customer, the best way to keep costs down is to compare deals and switch providers every year. From January 2022, things will be a bit different as insurance providers will no longer be allowed to give new customers better deals than existing ones (hallelujah!). But it’ll still be worth comparing deals each year as prices are changing all the time.

No one likes paying more than they have to! So, what can you do to keep your home insurance costs down? Here are our top tips.

Waiting until the last minute to get your insurance sorted doesn’t pay. Instead, you’re likely to get the best prices by buying your home insurance in advance. In fact, buying your home insurance 3 weeks before you want it to start can actually save you over 20%!

Although you’re likely to find the very best deals around 21 days before your insurance start date, you could bag a deal even earlier if you spot a bargain. Aviva, Privilege, Direct Line and Churchill are all insurance providers who’ll be happy to agree a price with you 90 days before you want your insurance to start.

Home insurance is one area of your life where it pays to be organised.

Looking to get buildings insurance? One common mistake is covering your home’s market value (how much it’s likely to sell for) instead of insuring its rebuild value (how much it would cost to rebuild it if your home was knocked down).

Funnily enough, it’s a lot cheaper to rebuild a home than what it costs to buy one! So, by covering its rebuild value instead of its market value, you can normally make a saving. To get a rough idea of your home’s rebuild value, you can use the Association of British Insurers' calculator.

At the same time, be careful not to under-insure. When it comes to contents insurance, it’s important to work out what it would cost to replace your belongings with brand new ones (rather than going off what you think your belongings would sell for used). If you underestimate how much your belongings would cost to replace, you might not be able to claim enough to replace them all if they get destroyed.

If you own your home and you want both buildings and contents insurance, getting combined insurance is normally a lot cheaper than getting individual policies with 2 different insurance providers (always double-check though to make sure!)

On top of that, it’s a lot more convenient. Firstly, if there’s an accident that causes damage to both your building and contents, you’ll only have to report the damage to 1 provider instead of 2. And secondly, it can help to avoid arguments between insurance providers where they’re both saying that the other one should pay.

All in all, cheaper and easier is a good combo in our books!

Do you need car insurance as well as home insurance? Well, sometimes, getting them both with the same insurance provider can get you a juicy discount!

It is possible to get cover for both your car and home on the same policy. However, most of the time, you just need to get both types of insurance with the same provider and they’ll offer you a discount on the second policy you take out with them. Direct Line, Aviva and Churchill are a few examples of insurance providers that work like this.

It’s super easy as you don’t have to line up renewal dates or anything like that. Let’s say you already have a car insurance policy with a particular provider. When you want to get a quote for home insurance, you just need to tell them you already have a policy with them and they’ll normally give you a discount. Simple!

That said, it’s always worth comparing it to the cost of getting your insurance policies with 2 separate providers, just to check that it’s definitely cheaper!

Most insurance providers will give you the chance to pay extra for extra cover. For example, you could get a ‘personal belongings’ add-on to cover you for items like your handbag or mobile phone while they’re outside of your home. Or, you could get ‘accidental damage cover’ to cover you for damage caused by accidents like spilt paint or red wine on your carpet.

Just be careful to check what your home insurance policy already includes to avoid doubling up. Let’s say you’re thinking about getting an ‘accidental damage’ add-on because you’re worried about your children breaking things in the home. Well, lots of standard insurance policies actually cover accidents caused by children even though they won’t usually cover other kinds of accidents like those caused by pets. So, you might not need the add-on after all!

Similarly, some protection can be cheaper as a whole separate insurance policy rather than as an add-on. For example, if you carry lots of valuable gadgets around outside the home, gadget insurance might protect them more cheaply than a ‘personal belongings’ add-on to your home insurance policy. Likewise, if you have a bicycle that’s worth more than £1,000, it might be cheaper to get a specialised bicycle insurance policy from a provider like Laka¹, rather than adding it to your home insurance. It’s worth checking anyway!

Did you know that getting the right locks on your doors could save you money on your contents insurance? That’s right, most insurers will ask you what type of locks you have before giving you a quote. It makes sense when you think about it, as better security means less risk of burglaries!

Anyway, if you’re considering upgrading your locks to keep your insurance costs down, the best kind you can go for is a 5-lever mortise deadlock, which conforms to British Standard 3621. That might sound like gobbledygook but it’s basically a really secure type of lock that insurance providers (and the police!) love. You can install these locks yourself but it’s probably easier to get a locksmith to help you – the Master Locksmiths Association can help you find one quickly and easily.

Either way, make sure that you put down the right lock type when your insurance provider asks you for it. If you don’t and you get burgled, your provider might say that your insurance is invalid and refuse to pay out. The Master Locksmiths Association has a handy guide that can help you to find out what kind of locks you have.

Auto-renewing is when you get to the end of your insurance deal and your insurance provider automatically puts you on that same deal for the next year. It sounds nice and easy, but it’s not actually so great. The reason? They’ll normally hike your prices up.

Instead, we’d recommend comparing deals from lots of different insurance providers each year – we’ll show you how to do that easily below. That way, you can switch to the cheapest deal available and avoid the price hikes.

Just bear in mind that this will only apply if you switch before 1st January 2022. From then, home insurance providers will be banned from charging existing customers more than new customers. So, theoretically, they won’t be able to hike your prices up each year.

Now you know all about home insurance, you’ll probably be wondering how to actually get it! Don’t worry, it’s super easy. Just follow these simple steps.

First things first, use the top comparison sites to compare deals. Each of these sites will take a few details from you and then show you lots of different deals from lots of different insurance providers, to help you find the right one for you.

Just be aware that not every deal will be on every comparison site. That’s why we recommend using all 4 of the sites below before you make your final choice. But if you’re pressed for time, just check the top one or two – we’ve ordered them in terms of finding the best deal and speed.

Get a home insurance quote in minutes with Confused.com – they compare 66 different companies to find the best for you.

Searches a wide range of providers (up to 66), only takes a few minutes and you could save up to £181.

Good range of providers, and get Meerkat Meals – discount on takeaways and eating out.

Get a home insurance quote in minutes with Confused.com – they compare 66 different companies to find the best for you.

There are also a few providers that won’t show up on comparison sites at all. The biggest is Direct Line.

Direct Line often has some great deals, so it’s worth getting a quote and comparing it to the other deals you’ve found on comparison sites yourself before making your final decision.

If you’re feeling a bit lazy or you simply want an easy life then look no further. We’ve already done the hard work for you and found what we think is the best provider for contents insurance.

Get £20 off when you sign up with Nuts About Money.

Designed for renters – monthly rolling contracts, covers the whole house (including landlords furniture), up to £40,000 worth of stuff, and best of all protects 6 unrelated people, inside and outside the home. Starts at £5 per month too.

Get a home insurance quote in minutes with Confused.com – they compare 66 different companies to find the best for you.

Getting a quote from Urban Jungle takes just a few minutes and prices start at just £5 a month. And it’s even better if you’re a renter because that’s exactly who Urban Jungle is designed for.

We’re talking monthly rolling deals (instead of typical 12-month plans), cover for everyone who lives in the home (even if you’re unrelated) and even protection for the landlord’s items and furniture (called tenants liability cover). Plus, it will cover your belongings outside of the home too!

Feeling brave? Then here’s a challenge for you: once you’ve found a deal you like, try haggling!

If you already have home insurance, call your current insurance provider and tell them that you’ve found a cheaper deal. The chances are they’ll want to keep you as a customer, so they may well try and beat the quote you’ve found or try to match it.

Even if you don’t currently have a home insurance provider, we’d always recommend getting on the phone and asking for a cheaper price before you buy a deal (if you feel brave enough, of course!). It often works, but even if you don’t get anywhere, at least you’ll know you’ve tried!

Finally, remember to double and triple-check that you’re happy with the policy you’re buying before agreeing to anything. Check the price again and read the policy inside-out so you know what you’re covered for and what you’re not.

This includes checking the excess. Remember, your excess is the amount that you have to pay if you make a claim. The bigger your excess (and so the more you have to pay if you make a claim), the cheaper your yearly or monthly fee will normally be. But you’ll need to be sure that can afford it if the worst happens and you need to make a claim. Ultimately, it’s all about finding the right balance for you.

Once you’re totally happy, you can go ahead and set a date for your new insurance policy to start, or start it immediately. Congrats!

Wondering how long it will take to get the money from your insurance provider once you make a claim? Well, it depends on lots of different things, like the kind of damage you’re claiming for and how many people are involved in the process.

If you’re making a public liability claim (where your property has caused damage to someone else or their possessions), that’s likely to be a lot more complex than if you’re just claiming for a burst pipe. And so, it’s likely to take longer.

Ultimately, a claim can take anything between 48 hours and over a year to be resolved. Don’t worry though, most claims won’t take over a year so hopefully, it won’t take this long for you!

We've written more about how to claim on your contents insurance too.

First things first, you can cancel your insurance policy whenever you want.

We mean, in an ideal world, you would probably stay with your insurance provider until the end of the year (most insurance policies last for a year before they renew). That’s because, if you leave before this, you’ll often have to pay a cancellation fee (usually around £35 to £50). However, it’s up to you and, as long as you’re happy to pay the fee, there’s nothing to stop you from leaving early.

If you do have to cancel in the middle of your policy, you’ll normally get a refund for the rest of the year if you paid upfront (as long as you haven’t made a claim). Or, if you normally pay monthly, you’ll just stop getting charged. Simple!

That said, if you’re moving house, you don’t necessarily have to cancel your home insurance. Instead, you can just move your policy to a new home!

Just be aware that you might still have to pay an admin fee and your insurance costs might go up or down depending on things like where your new house is and how much it costs. So, it’s still worth shopping around in case you can get your insurance cheaper from someone else!

Either way, make sure that your insurance policy is going to be in place right up to your moving date. And, if you’re moving your policy to your new home, check whether your contents will be covered during the move itself. Sometimes, you’ll have to use a professional moving company for your cover to be valid.

Of course, we know that some things can never be replaced – like that wedding photo album or your kid’s first painting! But home insurance is oh-so-important in making sure that, if the worst happens, you’ll have the finances to repair or replace all those other things in your life that money can buy.

If you're ready to compare costs and deals, just follow our steps above. You’ll have protection for your home and belongings and that all-important peace of mind before you know it!

Get a home insurance quote in minutes with Confused.com – they compare 66 different companies to find the best for you.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things insurance, with many years of combined experience writing and talking about the range of insurance cover available. Some of our team were top financial advisors. We understand the ins and outs of insurance, how to communicate insurance in an easy to understand way (we hope you agree), and of course, how to get the best insurance deal for you.

More than 10 years of combined experience researching and writing about insurance

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of insurance companies researched and reviewed

We follow a strict editorial code to ensure you get the best information possible

Get a home insurance quote in minutes with Confused.com – they compare 66 different companies to find the best for you.