Article contents

If you’re buying a house, you should get buildings insurance in advance and ask your insurance provider to start it on the day you exchange contracts (that’s the point where you’re legally obliged to buy the property).

Buying a home? Congrats! We know that insurance is a boring topic, but it’s really important to make sure your fabulous new pad is as protected as it can be. Plus, getting it sorted is a lot more straightforward than you might think!

Here, we’ll explain when to get buildings insurance if you’re buying a house, and why it’s something you need. But first…

Buildings insurance is a kind of insurance that protects your home. You have to pay a set amount of money each month or year, known as your premium. In return, if your home gets damaged, your insurance provider (the people that give out insurance) will pay to repair or rebuild it.

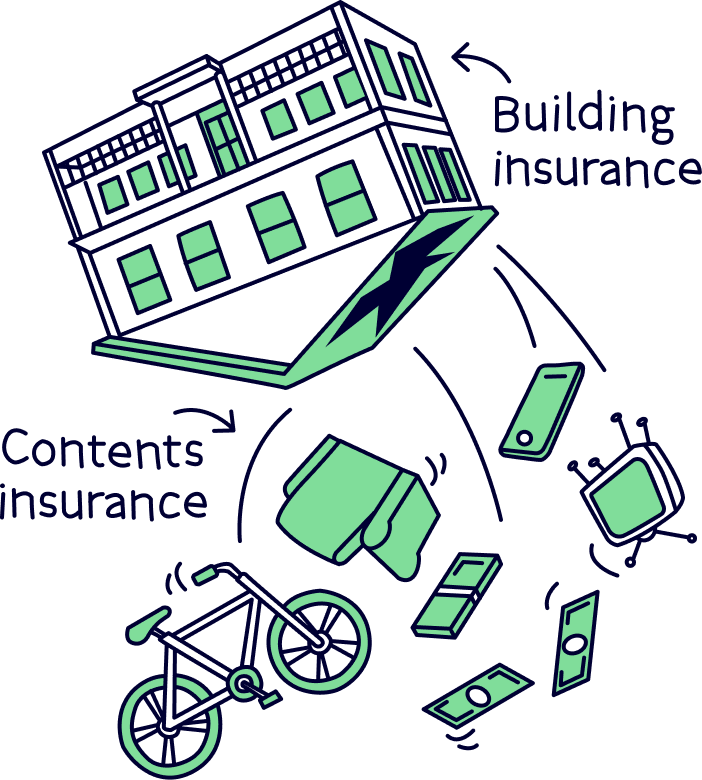

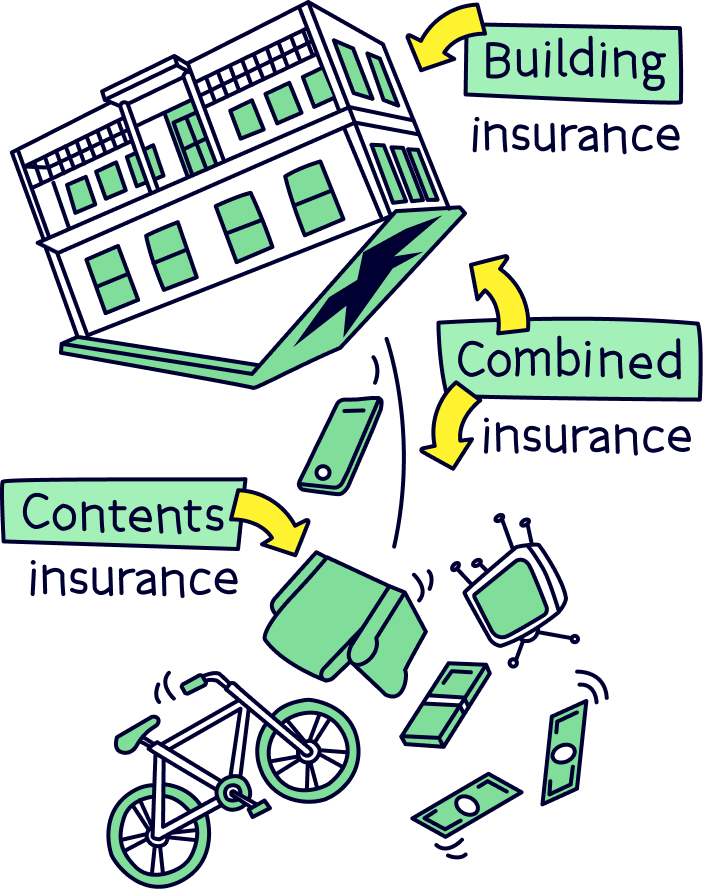

There are actually 2 types of home insurance, and buildings insurance is just 1 of them. Buildings insurance protects your home’s structure, as well as its permanent fixtures and fittings (things like windows, floors and sinks). Meanwhile, contents insurance protects the things you keep in your home (anything from electricals to furniture and jewellery).

Imagine someone picked up your house and shook it upside down. As a general rule, buildings insurance covers everything that would stay put, while contents insurance covers everything that would fall out.

You can also get something called combined insurance, which is buildings insurance and contents insurance rolled into 1. If you need both, combined insurance is often cheaper than getting both types of cover separately.

Buildings insurance isn’t a legal requirement but most people who buy a house do need it (not to mention the fact that it’s really useful!).

Why? Well, most mortgage lenders (the people who give out mortgages) will only give you a mortgage if you get buildings insurance. That means, unless you have enough money to buy a house without a mortgage, you’ll need to get it.

That said, even if you don’t need a mortgage, we’d still recommend getting buildings insurance (and preferably, contents insurance too!). Your property will probably be the most expensive thing you own. So, imagine how you’d feel if something happened to it! Not only would you lose your home, but you’d lose all the money you’ve put into it as well.

Buildings insurance will give you peace of mind that if something happens to damage or even completely destroy your home, you’ll get the money you need to repair or rebuild it.

There are 2 main ways you can own a property in the UK: freehold and leasehold.

If you own the freehold of a property, that means you own the building and the land it sits on. This applies to nearly everyone who buys a house (although there are some exceptions). And it means you’ll need to sort out your own buildings insurance.

On the other hand, if you own the leasehold, that means you own the property but not the building or the land. Basically, you’re purchasing the right to live in the property for a set number of years. You’ll normally be a leaseholder if you’re buying a flat.

If you’re a leaseholder, you won’t normally need to get buildings insurance (although it’s important to check the lease to make sure!). That’s because buildings insurance will be the responsibility of the freeholder. However, you will usually have to pay a yearly fee, known as the service charge. This will contribute towards the costs of looking after the building (which will normally be managed by a managing agent) – including the cost of buildings insurance.

That said, not everyone who owns a flat is a leaseholder. Sometimes, you’ll get a share of the freehold, which means you’ll jointly own the freehold with the people who own the other flats in your building. In this case, you’ll need to work with them to make sure there’s buildings insurance in place, which will normally mean splitting the cost between you.

If you’re buying a house, you’ll normally need to have buildings insurance in place when you exchange contracts.

Exchanging contracts is the moment when you become legally committed to buying the property. Up until this point, either you or the seller could pull out of the sale at any moment. But after you’ve exchanged contracts, you’re legally obliged to go ahead and buy it (and the seller is legally obliged to go ahead and sell it to you!).

Normally, you’ll exchange contracts around 1 to 2 weeks before all the money goes through and you get the keys (called completion). But it could be longer or shorter depending on what you agree with the seller.

Anyway, exchanging contracts is usually the time when the building will stop being covered by the seller’s buildings insurance. It’s important to make sure your cover starts at this point so that there aren’t any gaps in the building’s protection.

Not only that, but if you’re getting a mortgage, this is the moment where your mortgage lender will require you to have buildings insurance in place. If you don’t, your lender could refuse to give you your mortgage, which could end up delaying or even stopping the property sale completely. Obviously, that’s something to avoid!

Okay, so here’s the thing. Just because you have to have buildings insurance when the contracts are exchanged, that doesn’t mean that exchange day has to be a mad rush!

Instead, most buildings insurance providers will let you buy your buildings insurance in advance and choose what day you want it to start. In fact, it’s usually cheaper this way too. Buying your home insurance 3 weeks before you want it to start can save you over 20%!

Your conveyancer (the person who’ll be helping you to sort out the legal side of buying a house, known as conveyancing) will normally let you know what date you’ll be exchanging contracts ahead of time. Once you know what date it’ll be, you can go ahead and sort out buildings insurance.

All you have to do is tell your insurance provider what date you’ll be exchanging and voila! Your cover will start on the right day without you having to do anything more.

Just remember that exchange dates can change and house purchases can fall through (although we’re crossing our fingers that yours goes totally smoothly!). If that happens, make sure to tell your insurance provider your new exchange date or cancel your insurance if you don’t need it anymore. You don’t want to end up paying for insurance you don’t need!

Once you know that exchange day is approaching, it’s time to go ahead and get that buildings insurance sorted. But what exactly do you need to do? Just follow these simple steps.

When you get buildings insurance, you’ll need to tell your insurance provider how much cover you want – in other words, the maximum amount of money you’ll need them to pay you if your home gets damaged.

One common mistake is insuring your home’s market value (how much it’s likely to sell for) instead of insuring its rebuild value (how much it would cost to rebuild if it was knocked down). Funnily enough, it costs much less to rebuild a home than it costs to buy one, as the land it sits on is actually worth more than you might think. So, it’s important to insure its rebuild value rather than its market value, to avoid paying more than you need to.

To get a rough idea of your home’s rebuild value, you can use the Association of British Insurers' calculator.

Now, obviously, you need buildings insurance. But it’s a good idea to consider contents insurance as well.

Contents insurance covers all the belongings you keep inside your house, like your furniture, TV, dishwasher and jewellery. If something happens to your building, like a flood or a fire, the chances are your belongings will get damaged too. And replacing all your belongings is likely to cost a lot more than you think.

If you want to cover both your building and your belongings, you can either get 2 separate policies (your policy is a fancy word for your insurance contract). Or, you can get both rolled into 1 with a combined policy. Although it’s worth checking both and comparing the prices, a combined policy will normally be cheaper than getting both types of home insurance separately.

Plus, it’s normally a lot more convenient. If there’s an accident that causes damage to both your building and belongings, you’ll only have to report the damage to 1 provider instead of 2. And it will avoid arguments where you have 2 insurance providers who are both claiming that the other should pay!

Note: Often, your belongings will add up to much more than you think. If you’re getting contents insurance or combined insurance, make sure you don’t underestimate how much your belongings are worth as this could lead to you not getting enough money if something happens to them.

Now that you know what you’re looking for, it’s time to start hunting for deals. The first place we’d recommend looking is the top comparison sites. They’ll take a few details from you before showing you lots of different deals from lots of different insurance providers, so that you can compare them and find the best one for you.

In an ideal world, we’d recommend checking all 4 of the top comparison sites, as they’ll each show you slightly different deals. However, if you’re in a rush, you can just check the top 1 or 2. We’ve ordered them in terms of range of insurers searched and speed, to make things super easy!

Read our guide to home insurance to make sure your home is as protected as it can be.

Searches 65 different providers and get a freebie voucher if you buy.

Good range of providers, and get Meerkat Meals – discount on takeaways and eating out.

Searches 55 of the biggest providers and takes less than 5mins.

Searches 37 different companies – worth a quick check to find providers other sites may not work with.

Read our guide to home insurance to make sure your home is as protected as it can be.

There are a few insurance providers that won’t show up on comparison sites at all. It’s a bit annoying, but it’s basically because they’d rather you went to them directly.

The biggest (and the only one we’d really recommend checking) is Direct Line. It often has some great deals so head over to its website to get a quote and compare it to the other deals you’ve found on comparison sites.

If you really want to make sure you’ve got the best possible deal, we’d recommend getting on the phone or live chat (chatting to them on their website) with your chosen insurance provider, to ask whether they can give you a discount.

It’s not a vital step and it won’t always work. But if you’re feeling brave and there’s a chance of making a saving, it’s worth giving it a go, right?

Finally, before you go ahead and get your buildings insurance, make sure you’re completely happy with the deal you’ve selected.

Remember, it’s not all about price, but also about the protection you’re getting. Every insurance provider will offer slightly different things. It’s important to read the policy really carefully so you know exactly what’s included and what isn’t before going ahead.

As part of this, make sure you’re happy with any add-ons you’ve selected. Insurance providers are really good at selling you extra cover, like ‘accidental damage cover’ (which can protect your belongings from accidents like red wine spills) or ‘personal belongings cover’ (which can protect possessions you take outside of the home, like your mobile phone or laptop). However, it’s important to make sure you need any extras you’re considering as there’s no point in paying more for something you’re not going to use.

Similarly, check that you’re happy with the excess on your policy (your excess is a set amount of money you have to pay if you ask your insurance provider to cover the cost of something, known as making a claim). It can be tempting to go with a high excess as this can lower your monthly or yearly cost. However, it’s really important that you can afford your excess as otherwise, you won’t be able to afford to make a claim if something happens to your home.

Anyway, assuming everything looks good, congrats! You can go ahead and let your insurance provider know when you want your cover to start. Sorted!

If you already own a home, you probably already have buildings insurance. So, what should you do if you’re moving? Well, there are 2 options.

Many insurance providers will let you take your existing policy with you to your new home. Hooray!

Most buildings insurance lasts for a year before it renews. If you leave during this time, you’ll usually have to pay a fee known as a cancellation fee. Transferring your existing policy to your new home can be a good option as it will avoid you having to pay this.

Just bear in mind that your insurance provider may still charge you a fee for making changes to your policy. And you might also have to pay a higher monthly or yearly cost depending on what your new home is like and where it is.

It’s also really important to make sure that there’s no gap in cover if you’re not moving into your new property straight away. Remember, you’ll need to have buildings insurance in place at your new pad from the day of exchanging contracts, but you usually won’t get the keys until a week or 2 later.

Many insurance providers will be happy to cover your old property as well as your new one until you move, but you’ll need to check with your insurer to make sure.

If you can’t transfer your existing policy to your new home (or it’s expensive to do so), you could simply cancel your existing policy and get a new one for your new place. In fact, even if your existing provider is happy to transfer your policy, it’s worth checking how much it would cost to cancel and get a new one with a different provider, just in case it works out cheaper!

Your existing provider may well have been the cheapest option for your current home, but they probably won’t be able to give you the best deal on your new home. So, it’s worth shopping around.

Just remember that you’ll have to pay a cancellation fee if you’re leaving your current deal early. It may still be worth switching, but it’s important to factor this fee in when you’re comparing prices.

If you’re buying a house and your exchange date is approaching, you know what to do! Just follow our simple steps above to get your buildings insurance in place nice and early.

Then, let your insurance provider sort out the rest while you focus on much more exciting things – like testing out sofas in showrooms and sending out housewarming invites. You’ll be cracking open the champagne in your brand new (protected!) pad before you know it!

Read our guide to home insurance to make sure your home is as protected as it can be.

Read our guide to home insurance to make sure your home is as protected as it can be.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things insurance, with many years of combined experience writing and talking about the range of insurance cover available. Some of our team were top financial advisors. We understand the ins and outs of insurance, how to communicate insurance in an easy to understand way (we hope you agree), and of course, how to get the best insurance deal for you.

More than 10 years of combined experience researching and writing about insurance

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of insurance companies researched and reviewed

We follow a strict editorial code to ensure you get the best information possible