Article contents

Contents insurance protects your personal and valuable items in your home, you’ll need to get this yourself – you won’t be protected by your landlord's insurance.

All too often people think they’ll never need contents insurance and decide to rent a home without it. And some renters – often known as ‘tenants’ – think they don’t need it because their possessions are protected by their landlord’s insurance, which they most probably aren’t.

Either way, you’re taking a big risk by not taking out contents insurance while renting. It’s true that you might never need it – we all hope you’ll never need it – but you just never know what might happen in the future.

Contents insurance gives you peace of mind that the value of the items you own won’t be lost in the event of a fire, flood, theft, or any other scenario (which we’ll cover later).

In this guide to contents insurance for renters, we’ll explain what it is, why you might need it and how you can get the best deal for your situation.

Just here to find the best deal? here's how.

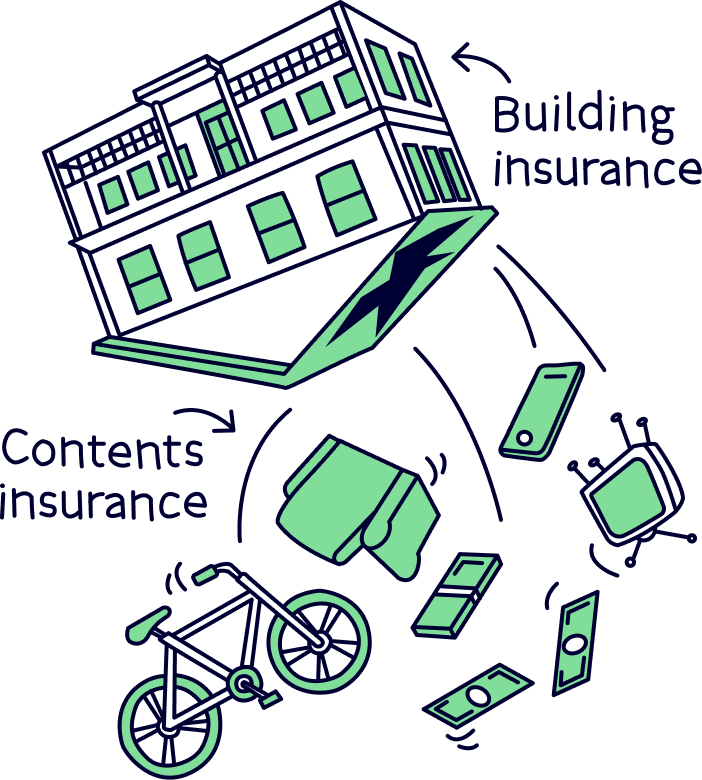

It’s the type of home insurance that protects the value of your personal belongings if worse comes to worst while you’re renting. You might hear contents insurance mentioned alongside things like ‘buildings insurance’. But it’s important to know the difference.

You might think that your items are covered by your landlord’s building insurance, but this usually only covers the building itself – things like the walls, floors, ceilings, roof, plumbing. If anything were to happen to your personal items, the chances are you wouldn’t be compensated if you relied on your landlord’s insurance.

This is where contents insurance comes in. It protects your personal items’ value so that you don’t lose out financially should anything bad happen, such as theft, fire or flooding.

Your insurance is based on the combined value of the items you own – the more valuable your items are, the more you’ll typically pay for contents insurance.

Contents insurance – you guessed it – covers the contents of your home. These are the items that you own and that aren’t part of the building’s structure itself.

Imagine this: you tip your house upside down. Whatever falls out comes under ‘contents insurance’; whatever doesn’t fall out is part of the building and comes under ‘buildings insurance’.

Different contents insurance policies cover different specific items and different scenarios, but you’ll find that most contents insurance policies cover:

Because different insurance providers offer different types of cover, it helps to shop around and take a look at what all the providers can offer you. Later on we’ll take you through the steps to getting the best contents insurance deal for you.

Not everything you own will necessarily be covered by your contents insurance, and there’ll probably be scenarios your insurance won’t cover.

The main exceptions that usually aren’t covered by contents insurance are:

If you have items on this list – for example, items used for your business that you keep at home, or items covered outside the home – it doesn’t mean you definitely won’t be able to get contents insurance to cover them. It just means you might need to ask insurers to add extra items onto your cover.

A lot of insurers have systems that allow for bespoke insurance policies like this, with additional ‘add-ons’ that you can choose when you compare quotes and purchase – more on how to find the best deal below.

The simple answer to this is that it totally depends where you look (which particular insurers and comparison sites, for example) and on your personal circumstances (where you live or your home’s security, for example). Insurers will weigh up the risk of something happening in your specific neighbourhood and to your particular home that might put your items at risk, and they’ll use that for your tenants’ insurance quote.

Your insurance is based on the combined value of the items you own – the more valuable your items are, the more contents insurance you’ll pay.

Data from MoneySuperMarket’s UK Price Index shows that the average cost of contents insurance is around £57 per year in 2021. When you think that £57 is just a couple of takeaways, contents insurance doesn't sound so expensive, does it?

One thing’s for sure: it’s definitely worth shopping around when you’re looking for contents insurance while renting. There are a lot of insurers, each with their own pros and cons, so you’ll thank yourself if you do some digging into what works best for you.

Comparison sites are your best friend when you’re looking for a great deal. Using them only takes a few minutes and could save you a load of money. Later in this guide we’ll take you through how to find the best deal on content insurance.

The amount you insure your items for will depend entirely on how much stuff you own, and how much it’s worth.

It’s important not to be too vague when totting up the value of your items – if you underestimate the value of your possessions you might not get as much money back as you need if you happen to make a claim in the future; and if you overestimate the value you’ll probably end up paying more than you need to for your insurance.

And you might be surprised about the combined value of your personal items. You might think ‘how do I own £35k’s worth of stuff?!’ But remember that it’s the value of replacing the item brand new, so the total value of your contents quickly adds up.

All in all, it’s important to give accurate amounts to your insurer – this’ll make sure you don’t lose out if anything bad happens. Nuts about Money exists to help you save money, and this is one of those areas where you might need to pay fractionally more for your insurance to make sure you don’t lose money in the long term.

There are no rules around when you should take out contents insurance. Of course, the earliest you could get insurance is from the day you move in, but you can take out insurance for your items at any time during your tenancy.

It’s worth us saying too that there’s no legal requirement for you to take out contents insurance. After all, it’s your personal items on the line, not anyone else’s. But we recommend having insurance for the items you own.

Maybe you’ve already had a peek at some contents insurance providers to see what’s on the market, and have been bamboozled by the amount of choice there is. We hear you – that’s why we exist!

Or maybe you don’t even know where to start with insurance for your items, and you found our guide as a starting point. We hear you too! We’re here to help.

It can seem overwhelming when you’re thinking about insurance and finance services. It’s not as if we were ever taught how to manage our finances, so don’t be disheartened if you don’t know where to start.

Happily there are a few ways to go about getting renters contents insurance. Here are the key steps:

Comparison sites are your friend. They analyse loads of insurance providers, break down their policies and give you a straightforward comparison of each. And they do this all for free!

All you need to do is put in some of your details – things like where you live, whether you own the property, how many people live there – and they’ll search for you. They’ll gather policies covering a wide range of contents insurance options, from the biggest household names to some lesser-known but trustworthy – and potentially cheaper – alternative providers.

Something to remember is that each comparison site has its own unique set of insurers they search, although there’s loads of overlap, so you’ll see the same companies on all, but it means you’ll get a slightly different set of results from each. And that’s okay! All this means is that it’s worth you taking the time to check your results from various comparison sites.

Of course we don’t expect you to trawl through every single deal on every single comparison site. It makes sense to start with one, then move onto a second and even a third if you have time. It generally takes around five minutes to enter your details and get some quotes on comparison sites.

Here are the top sites we recommend for contents insurance:

Our recommended provider for contents insurance is Urban Jungle. The cover is great, it's quick and super cheap. Plus, get £20 in free credit.

Get £20 off when you sign up with Nuts About Money.

The perfect contents insurance – monthly rolling contracts, covers the whole house (including landlords furniture), up to £40,000 worth of stuff, and best of all protects 6 unrelated people, inside and outside the home. Starts at £5 per month too.

Searches 65 different providers and get a freebie voucher if you buy.

Our recommended provider for contents insurance is Urban Jungle. The cover is great, it's quick and super cheap. Plus, get £20 in free credit.

What happens once you’ve got your comparison site quotes? Generally there’ll be a link to the deal on the insurer’s own site, and there you can see the deal in more detail – you should be able to see exactly what’s covered and work out whether it’s right for you. Be wary of providers upselling though! This is when they’ll try to get you to sign up for additional items to be covered in your insurance. Think carefully about whether you need these before you confirm your contents insurance.

While comparison sites are a must when you’re looking for a contents insurance deal, it can also be worthwhile checking out deals directly with providers. Sometimes providers don’t give comparison sites full access to their deals, so make sure you’re not missing out.

Direct Line is a key insurance provider that you won’t find on comparison sites. It’s worth getting a quote from them to see how it stacks up with the other providers. It might take a bit more time doing it this way, so we totally get it if it’ll take too long for you. But it can be a great way to get a deal that’s better for you.

Remember, getting a quote for insurance doesn’t mean you’re committing to taking out insurance with that provider, so it helps to shop around.

There are some insurance providers that might not be household names (yet) but that can still offer you a great deal and often even better customer service.

Here's our recommended provider for contents insurance:

Get £20 off when you sign up with Nuts About Money.

The perfect contents insurance – monthly rolling contracts, covers the whole house (including landlords furniture), up to £40,000 worth of stuff, and best of all protects 6 unrelated people, inside and outside the home. Starts at £5 per month too.

Our recommended provider for contents insurance is Urban Jungle. The cover is great, it's quick and super cheap. Plus, get £20 in free credit.

You might not see them on comparison sites. Get a quote directly with them – it only takes a few minutes – and you might kick yourself if you don’t.

What’s great about Urban Jungle is that their insurance cover is designed for renters, it's all online and takes just a few minutes to apply – say goodbye to time-consuming phone calls and being put on hold.

It might sound like a pain, but hopefully by now you’ve seen how easy it is to search for new contents insurance deals.

When your insurance policy ends – this’ll depend on the length of your contract, but for this example let’s say 12 months – don’t just let it renew for another 12. A lot of insurers raise prices after that first 12 months – sneaky, right? – so you could save money if you shop around when your first 12 months are nearly up.

If any of the items covered by your contents insurance or lost or damaged, here’s what you should do.

Learn more about making a claim on contents insurance.

Generally, contents insurance policies come with what’s called a ‘compulsory excess’. This is the amount of your claim that you will pay. For example, if your laptop gets stolen and you make a claim for £700, and your compulsory excess is £50, you’ll get £650 from your insurer and you’ll pay the additional £50.

You might also have an additional ‘voluntary excess’. You can choose whether you have this on your policy, and you can choose how much it’ll be.

Usually, the higher your excess, the lower your overall contents insurance will cost you. But remember that if you opt for a higher excess in order to get a cheaper overall insurance deal, you’ll need to make sure you can afford to make up the items(s) cost if you need to make a claim.

To be honest, we’re not surprised you’re here. Insurance is way too complicated and you just haven’t been given the knowledge and the tools to get the best deal for you and your home. In this guide we’ve covered the essentials you need to know when you’re looking for contents insurance for tenants.

To summarise what we’ve covered:

Contents insurance is important – you might not think you need it, but it’s better to be safe than sorry.

Most of your items will be covered by contents insurance, so you’ll have peace of mind that you won’t lose out if the worst happens.

There’s no one-size-fits-all contents insurance – it all depends on the value of the items you own.

So shop around to get the best deal for you! Just follow our steps to find the best deal, and you'll be sorted in no time.

We exist to help ease your money worries, so we hope that with this guide to contents insurance for renters you’ve gained some knowledge about this tricky topic.

Our recommended provider for contents insurance is Urban Jungle. The cover is great, it's quick and super cheap. Plus, get £20 in free credit.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things insurance, with many years of combined experience writing and talking about the range of insurance cover available. Some of our team were top financial advisors. We understand the ins and outs of insurance, how to communicate insurance in an easy to understand way (we hope you agree), and of course, how to get the best insurance deal for you.

More than 10 years of combined experience researching and writing about insurance

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of insurance companies researched and reviewed

We follow a strict editorial code to ensure you get the best information possible

Our recommended provider for contents insurance is Urban Jungle. The cover is great, it's quick and super cheap. Plus, get £20 in free credit.