Article contents

You don’t legally have to get home insurance, but we’d really recommend it! If you rent, you should get a type called contents insurance, which covers your belongings if they’re damaged or stolen at home.

If you don’t own your home, you might be thinking ‘is home insurance really worth it for me?’ The answer? Yes! It’s absolutely worth it to make sure that all your most-loved possessions are as protected as they can be.

Here, we’ll take a look at what home insurance can do for you as a renter and what kind you should get.

Home insurance is a special type of insurance that protects your home and belongings.

Basically, you pay a sum of money each month or year, called your insurance premium. In return, if your home or possessions get damaged, you can ask your home insurance provider (the people who give out home insurance) to pay to get them fixed or replaced. This is called making a claim.

Just bear in mind that, when you make a claim, you’ll still need to pay part of it yourself. This will be a set amount that you agree with your insurance provider when you get your insurance, and is known as your excess.

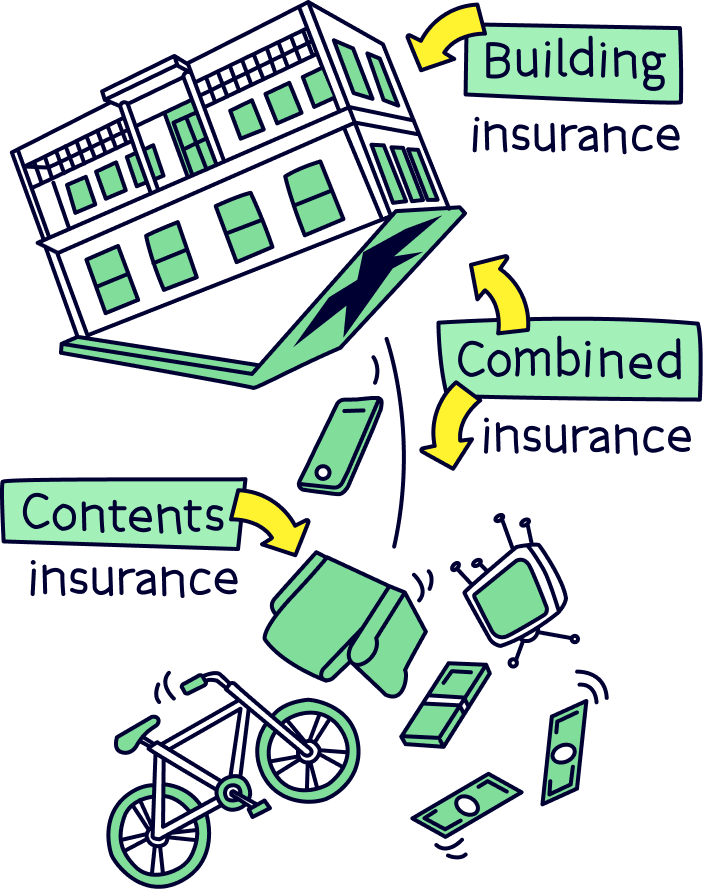

There are three types of home insurance, and not all of them are designed for renters. Here are the different types and whether you need them or not.

In summary, the only home insurance you need if you rent is contents insurance. Easy!

You’re going to hate us for saying this, but it’s impossible to say exactly what your contents insurance will cover without looking at your policy. Your policy is a kind of contract that lays out exactly what you have to pay and what you get in return. And, to make matters a little bit confusing, each one is different!

That said, most contents insurance policies will protect your possessions from loss or damage caused by:

So, if any of these things cause damage to the contents of your home, your insurance provider should cover the cost for you!

Wondering which of your belongings will be included? Well, as a general rule of thumb, contents insurance will protect anything that would fall out of your home if you tipped it upside down. So that includes your TV, clothes, phone, couch, books, computer, rug… you get the idea! It can even include the contents of your fridge!

Usually, your contents insurance will also include replacing your keys or locks if it’s needed. And it even includes replacing cash that’s stolen from your home (although before you get tempted to stash wads of cash under your mattress, be aware that most policies will limit how much you can claim for!).

Lots of contents insurance policies also cover tenants’ liability, which is awesome if you’re renting. It means your insurance provider will cover the cost of repairs to your landlord’s items and furniture if you accidentally damage them – so no more awkward conversations with your landlord! One of our favourite insurance providers that offer this is Urban Jungle¹, but we’ll tell you more about why they’re so great in a bit!

Contents insurance can also protect you legally in case someone is seriously injured inside your home. Imagine your neighbour comes round for tea and hurts themselves tripping up on a corner of your rug. If it’s found to be your fault, your contents insurance will cover the costs, including paying for a lawyer for you. Fingers crossed that doesn’t happen, but it’s good to know that you’re protected just in case!

Before you get too excited thinking you can use your contents insurance to replace all those old belongings that need updating, hang fire. As great as contents insurance is, there are a few things it won’t cover. Such as...

The simple answer is no. You don’t legally need home insurance if you rent. BUT (yep, there’s always a but!) we’d strongly recommend that you get contents insurance.

The chances are your home contains all your most valuable and treasured possessions. No matter how careful you are, there’s always a possibility that they get damaged or stolen.

Some of your possessions just won’t be replaceable – your kid’s first drawing, your wedding photo album… you get the gist. But there are things that money can buy. Contents insurance will give you peace of mind that, if something bad happens, you’ll be able to afford to get your belongings repaired or replaced so that you can move on with your life.

Not only that, but it’s normally pretty cheap considering how much money you could save if things do go wrong. The average cost of contents insurance per year is £57. That comes to just £4.75 per month! These prices are based on the second 3 months of 2021 as revealed in MoneySuperMarket’s UK price index.

Just watch out that you don’t do something called underinsuring. When you get contents insurance, you’ll need to estimate how much all your belongings are worth added together. One common mistake people make is looking at how much their items are worth now rather than how much it would cost to buy them new. This can lead to underinsuring, which is when you underestimate how much your belongings all add up to.

So, why is underinsuring such a problem? Well, let’s say you only insure 50% of the value of your possessions. If all your possessions are destroyed, your insurance provider will only give you 50% of the money you need to get them all repaired or replaced. Gulp!

But that’s not all. A lot of the time, just one of your belongings will be damaged – your TV, for example. If you’ve underinsured by 50% and your insurance provider sends someone round to examine your TV, they might notice that your belongings add up to a lot more than what you said. So, they’ll probably only cover 50% of the cost of your TV, since you only covered 50% of your belongings.

The lesson? Don’t try to save money by underestimating how much your belongings are worth!

If you’re renting a whole home to live in by yourself or to share with your partner or family, things will be super straightforward. Remember, contents insurance is exactly the same for people who rent as it is for people who own their home!

However, if you’re renting with non-family members, not all insurance providers will be happy to give you insurance. Why? Well, it often increases the chance of items going missing or of things getting damaged.

Don’t worry, we’re not saying your housemates are thieves or that they’re going to go around breaking your things! It’s just that if you share with others, there’ll probably be more people that you don’t know coming in and out of your home.

Now, you can (and should!!) still get contents insurance. But there’ll be a few extra things to bear in mind.

Do you live with a group of friends? Then it’s often easiest to get one contents insurance policy between all of you.

By pitching in together, you get to split the cost (kerching!). And, perhaps more importantly, everyone’s belongings will be covered no matter whether they’re in your bedroom or a shared living space. Makes life easy, right?

Just bear in mind that getting a joint contents insurance policy like this will link you to your housemates (known as ‘association’). While you might love your housemates to bits, being associated with them when it comes to insurance isn’t always a good thing.

In a nutshell, if one of your housemates makes a claim, it will mean that everyone’s prices will go up the next year. Plus, if you move out and want to get a new contents insurance policy elsewhere, you’ll still have to declare your housemate’s claim, which could lead to higher costs.

It’s not necessarily the end of the world, and it might well be worth it to know that your belongings are protected. But it’s definitely something to be aware of all the same!

Do you live in a houseshare but just rent your own room? If you’d rather not chip in with your housemates, you can get room-only contents insurance.

Room-only insurance will only protect you and your possessions, not your housemates’. So, you won’t be linked to your housemates through association like you would if you got a joint policy with them.

However, it’s not all roses and butterflies. First, if your belongings are stolen while they’re in communal areas (rather than your room), your insurance provider probably won’t cover the cost unless there are signs of forced entry. This is because there’s always a chance that another tenant or one of their friends just wandered into your home and took them!

Secondly, even if your belongings are in your room, they’ll only be protected from theft if you have a lock on the door and you keep your door locked while you’re out. If there’s no sign of forced entry to your room, it’s unlikely that your insurance provider will pay as, again, how do they know that someone actually broke in?

Are you a student who’s temporarily away at uni? In this case, before you fork out on home insurance, check whether you actually need it. You might (if you’re very lucky!) already be covered on your parents’ home insurance, under its ‘temporarily removed from the home’ section.

You might be surprised, but a lot of policies will still cover your belongings while they’re at another address, as long as your parents’ home is still your main permanent residence. If your parents have a ‘personal belongings’ add-on to their policy, your items might even be covered while you’re out and about with them. Not bad at all!

If you’re not covered on your parents’ insurance (or you don’t fancy sponging off them!) then you should still get contents insurance. Especially as you’ll probably be meeting and living with lots of new people! Check out our guide to student contents insurance to learn more.

Finally, if you’re ready to get your most treasured belongings protected, you’ll want to know how to actually get home insurance. And, how to get the best insurance for the best price! Just follow these simple steps to nail it.

First things first, compare contents insurance deals using the top comparison sites. We say ‘sites’ rather than ‘site’ because each comparison site will include slightly different deals. To make sure you don’t miss out on any that are particularly awesome, it’s best to use a few!

We’ve listed the 4 comparison sites that we’d recommend using below, in order of just how great we think they are.

Our recommended provider for contents insurance is Urban Jungle. The cover is great, it's quick and super cheap. Plus, get £20 in free credit.

Searches 65 different providers and get a freebie voucher if you buy.

Good range of providers, and get Meerkat Meals – discount on takeaways and eating out.

Our recommended provider for contents insurance is Urban Jungle. The cover is great, it's quick and super cheap. Plus, get £20 in free credit.

As fabulous as comparison sites are, there are a few insurance providers that they can’t show you. That’s because some insurance providers want customers to come straight to them, so they don’t make their deals available to comparison sites. We know, it’s pretty annoying!

For contents insurance, the only provider we’d recommend checking is Direct Line. If you have time, get a quote from them using their website and compare it to the other deals you find in step 1. Direct Line is a big insurance provider with lots of affordable options that comparison sites won’t show you, so it’s worth checking!

Feeling a bit lazy or simply want a recommendation from someone you trust? We love, love, love Urban Jungle¹ for contents insurance.

Get £20 off when you sign up with Nuts About Money.

The perfect contents insurance – monthly rolling contracts, covers the whole house (including landlords furniture), up to £40,000 worth of stuff, and best of all protects 6 unrelated people, inside and outside the home. Starts at £5 per month too.

Our recommended provider for contents insurance is Urban Jungle. The cover is great, it's quick and super cheap. Plus, get £20 in free credit.

Their policies are designed especially for renters and they’re particularly perfect if you’re living with friends or strangers. The insurance covers the whole house, including protection for you and up to 6 unrelated people. Plus, it includes tenants liability cover so your landlord’s items and furniture will all be protected against accidents.

As if that wasn’t enough, Urban Jungle covers all your items outside of the home as well as inside it. So, you won’t even need to get extra cover for your mobile phone or laptop! With deals starting at as little as £5 per month, it’s a bit of a steal in our books!

Finally, do one last check to make sure you’re totally happy with the insurance policy you’ve selected. Remind yourself of what it covers and check that you definitely need any extras you’ve added. Insurance providers are great at selling extra cover on top of your standard policy, but you’ll want to be careful that you’re not paying extra for cover you don’t actually need.

For example, you might be thinking about getting ‘accidental damage’ cover because you’re worried about your children breaking things. But lots of standard contents insurance policies actually cover accidents caused by children (even though they don’t often cover other kinds of accidents) so if you look carefully, you might find that you don’t need it after all!

Before confirming your new policy, you’ll also want to check that you’re comfortable with the price. You’ll need to make sure that you can afford the yearly or monthly payments, but you’ll also need to make sure that you can afford the excess. Remember, the excess is the money you have to pay when you make a claim, so it’s important to make sure you’ve got the funds to take advantage of your insurance if the worst happens.

If you’re feeling good about everything, then congrats! All that’s left is to confirm your selection and tell your new insurance provider when you want the cover to start (you could even start straight away!).

Your home is where you keep all your most important belongings. We know there are some that money can’t buy, but there are others that it can. Think about your clothes, laptop, furnishings, lamps, books, artwork, and all the other things you’d need to replace if some disaster destroyed your home.

Contents insurance will mean that, if the worst happens, you’ll be able to afford to repair or replace all of them. If that’s not worthwhile then we don’t know what is! Just follow our steps above to get the best deal on your home insurance and enjoy that all-important peace of mind.

Our recommended provider for contents insurance is Urban Jungle. The cover is great, it's quick and super cheap. Plus, get £20 in free credit.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things insurance, with many years of combined experience writing and talking about the range of insurance cover available. Some of our team were top financial advisors. We understand the ins and outs of insurance, how to communicate insurance in an easy to understand way (we hope you agree), and of course, how to get the best insurance deal for you.

More than 10 years of combined experience researching and writing about insurance

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of insurance companies researched and reviewed

We follow a strict editorial code to ensure you get the best information possible

Our recommended provider for contents insurance is Urban Jungle. The cover is great, it's quick and super cheap. Plus, get £20 in free credit.