Article contents

You sure can! As long as you can cover the mortgage repayments you'll be fine.

Straight to the point, yes you can get a mortgage and buy a house with a part time job, as long as you’ve got a stable job with a modest income you should be fine.

Here’s an overview of all what might influence your ability to get a mortgage and how much you can borrow.

Mortgage lenders are concerned a lot with risk, and therefore job stability is a key factor in their lending decision for those with a part time job.

This means how long you’ve been working in your current role and for your current employer. Typically in a full time position 3 months worth of pay history is enough but for part time you may want to wait a few months longer to at least have a wider range of lenders to choose from.

Your broker may know some lenders that can offer as short as 1 month, but it may not be the best deal for you. And very occasionally you may find a lender who will lend on a future contract of work.

Part time work tends to lend itself to short periods of work as you have more important things going on in your life than just working! But that doesn’t necessarily mean everyone is moving around jobs all the time. If you’ve got a permanent contract and are happy with the hours, lenders will love you.

Having a minimum number of hours on your contract means guaranteed pay, and that’s all a lender is looking for. If you don’t have a minimum number of hours and are perhaps on a zero hours contract, you may find it more difficult to find a lender, but it’s not impossible. You’ll be seen as higher risk, so you may have limited options at slightly higher interest rates.

Habito will find your best deal, fast, all with award-winning service.

The big drawback of working part time is typically a lower salary, which, as the amount you can borrow is based on how much you earn, means you will typically get a lower mortgage amount.

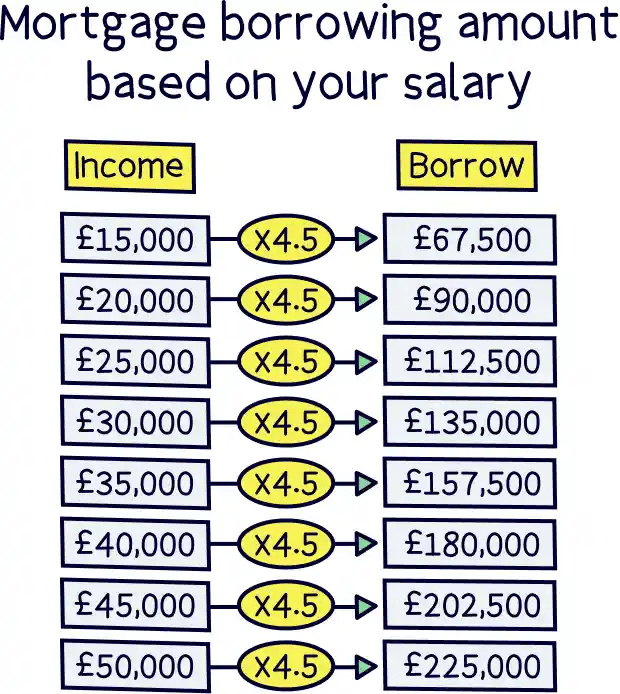

The very general rule of thumb for working out how much you can borrow is taking your total income and multiplying it by 4.5. So if you earn £20,000 per year, you could get a mortgage for £90,000.

However, lenders have what’s called a minimum income threshold, which means they won’t lend to those earning under this amount, because the risk of not paying the repayments is too high. This is typically £20,000.

However don’t despair, we’ve just looked at salary, but you might have some additional sources of income you’re not aware of just yet to get a higher total income – the real figure lenders care about.

Good news, some lenders also take into account any benefits you receive, typically with part time jobs these are:

Total these up and add them to your salary to get a total income amount. However, some lenders will cap the amount of benefits you can add to your salary, it varies from lender to lender, so do get advice from a mortgage broker.

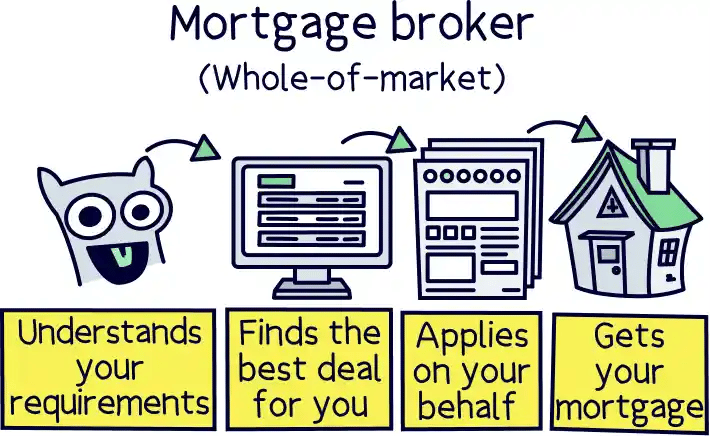

Not sure where to find a good mortgage broker? Check out Habito¹, they've got award-winning service, and guarantee to get you the best mortgage deal, all for free. How great is that?

Habito will find the best mortgage for you, all for free, and with great service. But better than that, if you’re buying a home, they’ll handle the whole process for you – that’s the legal work and survey, and everything else. It’s a huge stress and time saver, and comes at a great price.

Habito is run by Monzo, which is a very large and successful modern bank (often called a mobile bank).

Habito will find your best deal, fast, all with award-winning service.

If the job is stable and the income is reliable, you may be able to use this too, but not in all cases, depending on the lender. It’s worth bringing up when you speak to your mortgage broker.

As with mortgages for those with full time jobs, you still need to prove you can afford the monthly repayments. This isn’t to do with just your total income, it’s the remaining cash you have left after you deduct all of your outgoings – that’s all the bills and regular payments you have as part of your lifestyle.

If you’re just about scraping by, and there’s a lot of us who are, it’s just how life is sometimes, lenders will see this as fairly high risk and prefer not to lend.

If you can plan ahead a few months before applying for a mortgage, try and reduce all unnecessary expenses, and try to have a reasonable figure left in your bank account each month. This will help with affordability.

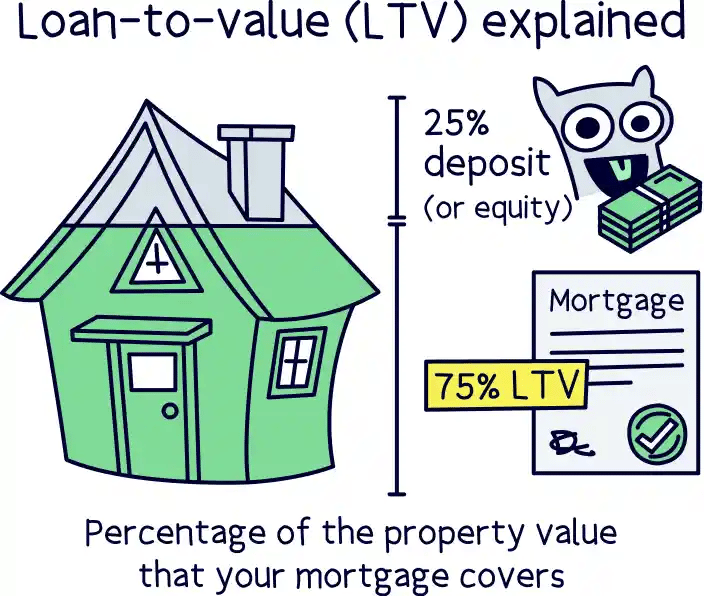

It may be a bit harder to save for a deposit if you are working part-time, but having a larger deposit can make a huge difference in the interest rate and the overall cost of the mortgage.

A larger deposit means a lower loan-to-value (LTV), that’s the ratio of how much you are borrowing from the lender versus how much deposit you are putting in to buy the house, the more your put in, the less risk it is for the lender, and so they effectively reward you with lower interest rate.

It might be harder to save, but consider holding out a bit longer to get up to at least 15% deposit.

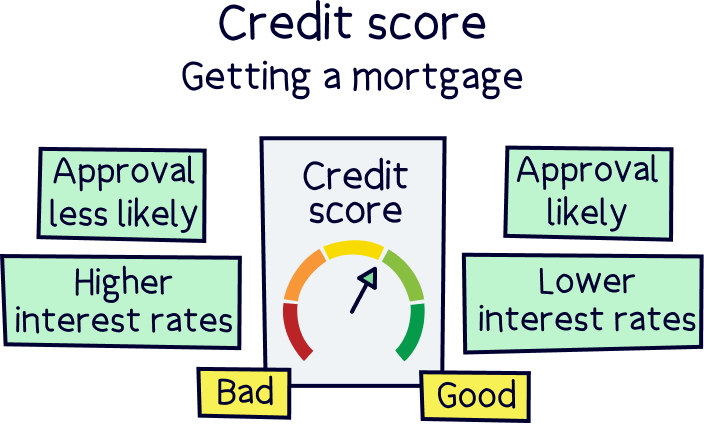

Again back to the risk for the lender, that’s what mortgages are all about. If you have a bad or poor credit rating, that’s a bad sign for them. However, it doesn’t mean the end of the road, even with a part-time job and income.

It’s best to have a high credit rating, and there is a a lot you can do to improve that, such as credit building credit cards and of course paying bills on time, but staying on topic, if you have a bad credit rating and a part-time job, you may still be able to get a mortgage, but be prepared to pay a higher interest rate to offset the risk to the lender.

Speak to a specialist mortgage broker for advice if you are in this situation.

So a quick summary, you do not need a full time job to get a mortgage, you can get a mortgage working part time but it depends on the stability of your job, your income and your ability to pay the mortgage off each month (your affordability).

We always recommend using a mortgage broker to help find the right mortgage for you, and this is especially important for those in a part-time position.

Our recommendation for mortgage brokers is Habito¹, it's free, they've got award-winning service, and will guarantee to get you the best mortgage deal.

Habito will find your best deal, fast, all with award-winning service.

Habito will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Habito will find your best deal, fast, all with award-winning service.