Article contents

Most mortgage lenders don’t offer mortgages designed especially for first-time buyers. Instead, the best mortgage for first-time buyers will normally be a standard mortgage that happens to cater well for people who have smaller deposits.

Are you buying a property for the first time? Wondering where the best mortgage deals are for first-time buyers?

Well, you’re in the right place! Here, we’ll look at everything you need to know about finding the best mortgage as a first-time buyer. But first things first...

A mortgage for first-time buyers is exactly what it says on the tin: it’s a mortgage for someone who has never owned a property before!

However, you can’t really apply for a ‘first-time buyer mortgage.’ Why? Well, they just don’t exist!

That’s right, mortgage lenders don’t really create mortgages that are specially designed for first-time buyers (mortgage lenders are the people who give out mortgages).

We mean, if you’re a student, there are a few mortgage lenders who offer specially designed student mortgages.

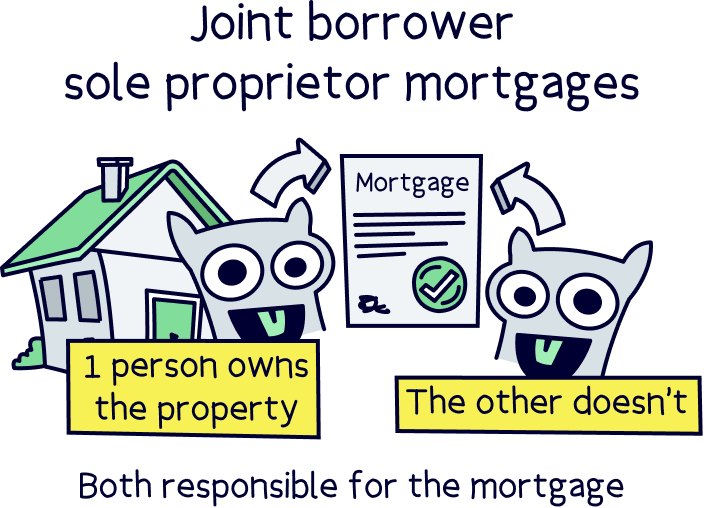

And if you have a parent or relative who wants to help you get on the property ladder, lots of lenders will offer guarantor mortgages or joint borrower sole proprietor mortgages (these are both mortgages where your parent or family member agrees to take some responsibility for your monthly repayments). If you’re interested in getting one of these mortgages, check out Tembo¹, they specialise in them (get 50% off their fee with Nuts About Money).

But mortgages created especially for first-time buyers? Not so much! There’s the odd one here and there, but they don’t really look any different from any other mortgage. So, generally, if you’re buying a property for the first time, you’ll just get a normal mortgage designed for any old Tom, Dick or Harry – including people who’ve owned properties before.

Tembo will find your best deal, fast, all with award-winning service.

You’re going to hate us for saying this, but there is no best mortgage or mortgage lender for first-time buyers. Sorry! Every first-time buyer is different, so the best mortgage for you might not be the best mortgage for someone else.

That said, as a first-time buyer, there are a few things that you’re more likely to be dealing with, and so the best mortgage lender for you will probably be one who can easily cater to those requirements. For example, you’re more likely to:

Now, there’s every chance that you’re a first-time buyer who has a great credit score, has saved up a whopping deposit and earns a fortune. In which case, the best mortgage for you will probably be no different from the best mortgage for someone who’s owned a property previously.

But if the things we’ve listed above ring a bell, the best mortgage lender for you will be one who’s happy to lend to you (and give you as good a deal as possible) despite the fact you’re a liiiittle bit riskier than other borrowers out there. That’s likely to be a little bit harder (although still totally possible!).

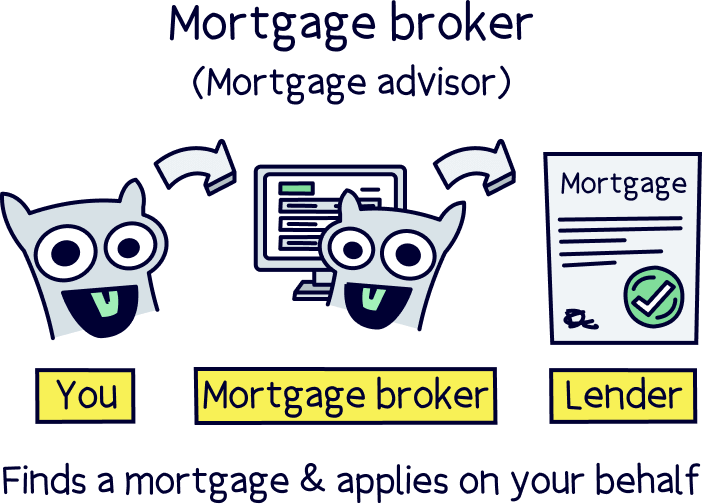

The best way to find the right lender and mortgage deal for you is to get the help of a mortgage broker (also known as a mortgage advisor). Which brings us onto...

You don’t technically have to use a mortgage broker to find the best mortgage for you. You can also go straight to individual mortgage lenders to apply for a mortgage directly. But we think that using a mortgage broker is important, especially if you’re a first-time buyer.

Why? Well, there are over 100 mortgage lenders out there who all have different criteria. As a first-time buyer, the chances are a lot of those lenders won’t want to give you a mortgage, but annoyingly, if you apply for a mortgage and get rejected, this can show up on your credit score and make it harder for you to get approved for a mortgage in the future. Urgh!

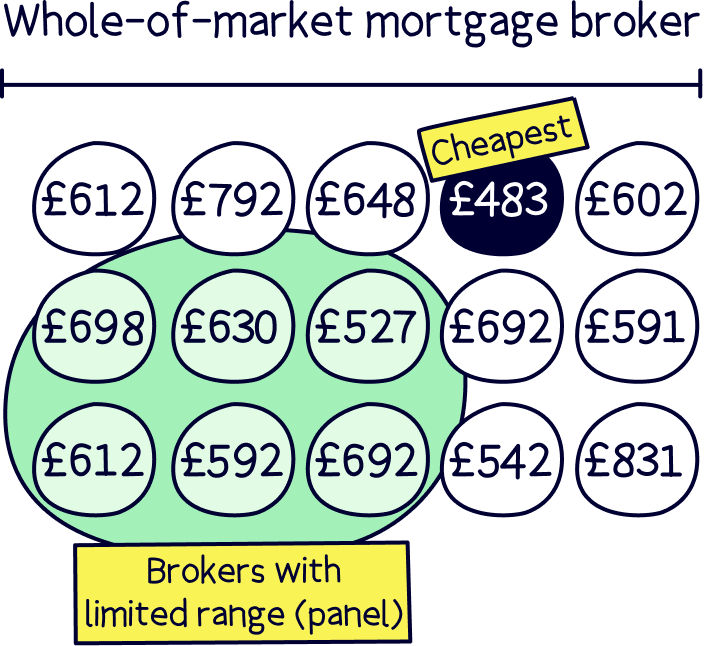

Mortgage brokers are experts in mortgages and they specialise in helping people to find the best mortgages for them. They’ll take the time to learn all about your personal circumstances and then they’ll compare all the different mortgages from all the different lenders to find the best one for you (as long as you choose a broker who can compare all the different mortgages, known as a ‘whole-of-market’ mortgage broker).

They’ll also be familiar with the ins and outs of each lender. So, they’ll know which lenders are most likely to accept you, helping you to avoid getting rejected for a mortgage unnecessarily. Oh, and they’ll even fill out your whole application for you.

Ultimately, working with a mortgage broker will save you both time and money and make it more likely that you’ll get accepted for that mortgage you’re after. If you need any help finding one of these superheroes, check Tembo¹, they've got award-winning service and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money.

Get 50% off the standard fee

Tembo is an all-round amazing mortgage broker, in fact, they're award-winning, and not just online.

They can help with pretty much every mortgage out there, from buying a home to switching deals, and on top of that, have unique options to increase your borrowing such as an Income Boost¹ and Deposit Boost¹.

They'll handle the whole mortgage for you too, and the service is great.

Habito will find the best mortgage for you, all for free, and with great service. But better than that, if you’re buying a home, they’ll handle the whole process for you – that’s the legal work and survey, and everything else. It’s a huge stress and time saver, and comes at a great price.

Habito is run by Monzo, which is a very large and successful modern bank (often called a mobile bank).

Tembo will find your best deal, fast, all with award-winning service.

Now, finding the best mortgage for you isn’t just about finding the cheapest deal out there. There are lots of different mortgage types, sizes and durations. So, it’s oh-so-important to make sure that the mortgage you’re choosing fits your needs.

Here are some of the main things you’ll want to think about when you’re umming and ahhing about which is the best mortgage for you as a first-time buyer.

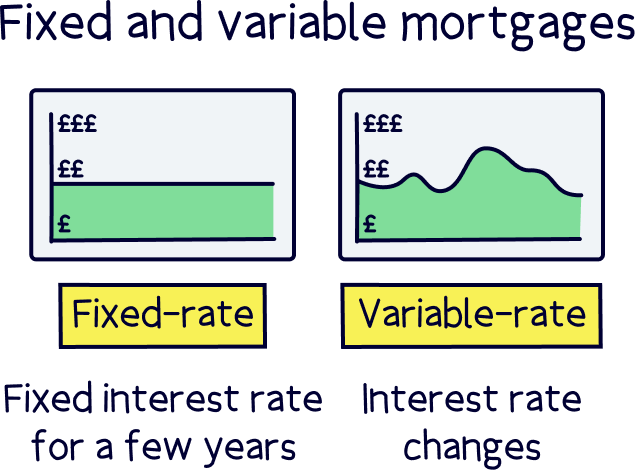

There are 2 main groups of mortgages: fixed-rate and variable-rate.

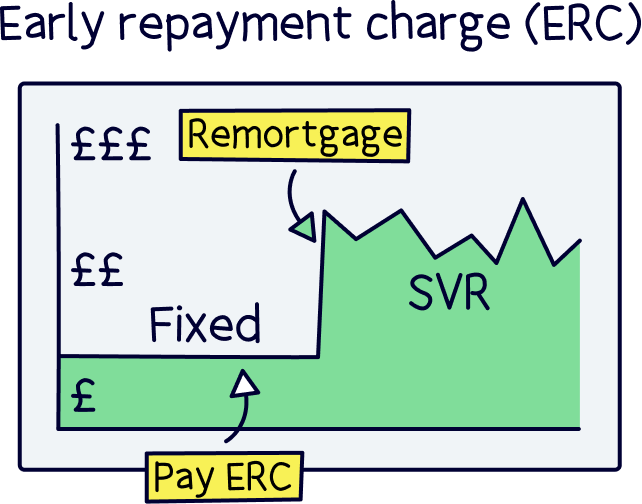

A fixed-rate mortgage is one where your interest rates, and therefore your monthly repayments, are set at a fixed cost for a specific period of time (interest rates are what lenders charge you for the pleasure of borrowing their money, and is usually a percentage of what you owe). They can be fixed for any length of time, but most often they’ll be fixed for 2, 3 or 5 years (known as your fixed-rate period).

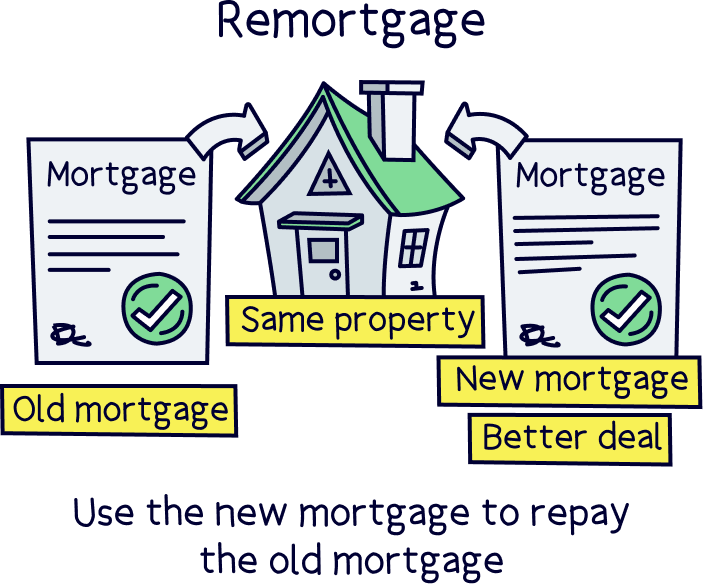

After this, your prices will go up but you can avoid this by remortgaging (where you swap your current mortgage for a new one, either with your existing lender or a different one altogether).

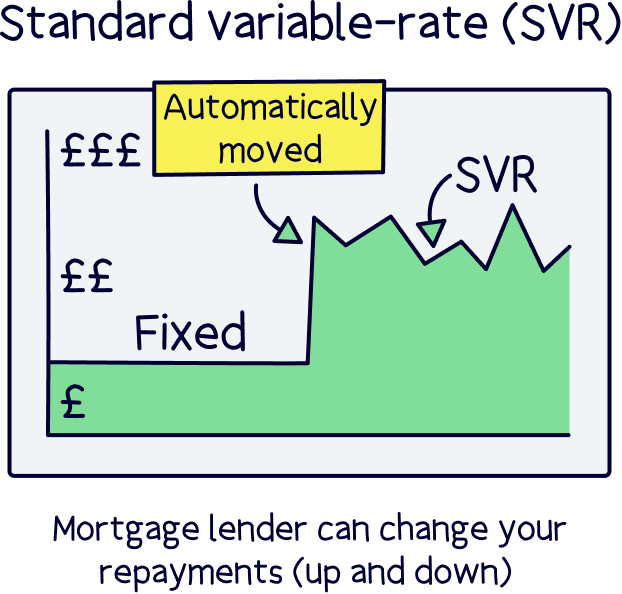

On the other hand, a variable-rate mortgage is one where your interest rates can move around, which means your monthly repayments can change month-to-month.

There’s one variable-rate mortgage that you’ll want to avoid at all costs, which is called the standard variable rate (SVR). This is the rate that your lender will automatically put you on when any deals you have (like your fixed-rate mortgage) come to an end. Not only is it extremely expensive, but your mortgage lender could technically move your interest rates up or down whenever they fancy (although they’ll normally move them at the same time as the Bank of England’s base rate, which is the official borrowing rate).

However, there are lots of different types of variable mortgages, and most are a lot better than the SVR. For instance, a tracker mortgage is a variable-rate mortgage where your interest rates can only move up or down in line with the Bank of England’s base rate. As long as the base rate doesn’t go up too high, this can often end up being the cheapest mortgage type out there (especially right now, while rates are at an all-time low). Similarly, a discount variable rate mortgage works in the same way as the SVR but gives you a discount for a set period of time so your monthly repayments are lower.

So anyway, which one is better for first-time buyers? Fixed or variable?

As always, it’s going to depend on your personal circumstances and a mortgage broker will be able to give you bespoke advice on what’s best for you. But if you’ve never owned a property before, you might find it safest to fix your mortgage. In fact, this is the type of mortgage that most people get.

With a fixed-rate mortgage, you’ll know exactly how much you need to pay each month, at least for a couple of years. That will make it much easier to budget, which will hopefully mean you’re never caught out struggling to afford your monthly repayments!

The downsides? Well, if interest rates suddenly drop, you won’t get to benefit from cheaper monthly repayments. And if you want to leave your fixed-rate mortgage before your fixed-rate period has ended, you’ll have to pay a fee called an early repayment charge, which can be pretty hefty. So, if you get this kind of mortgage, you’ll ideally want to avoid leaving until your fixed-rate period ends!

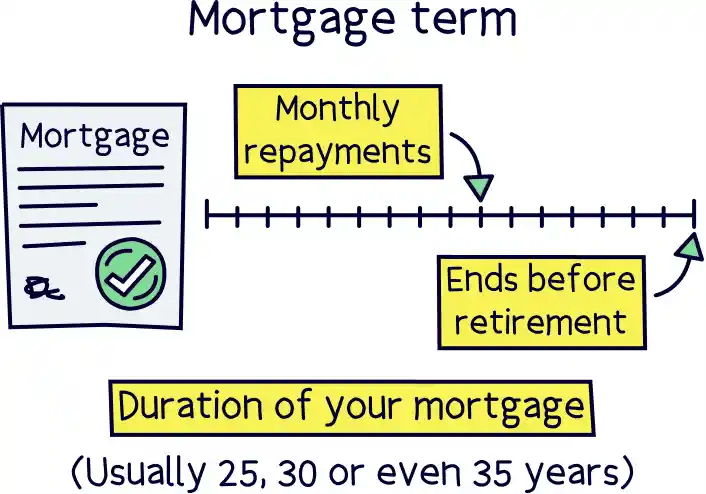

Your mortgage term refers to the duration of your mortgage. Basically, your mortgage lender will calculate your repayments so that you’ve paid off your entire mortgage by the end of this time.

Your mortgage term could technically be any length at all. However, you’ll need it to be short enough so that you pay off your entire mortgage before you hit retirement age. And you’ll need it to be long enough so that you can spread out your repayments over many years and keep them affordable.

Normally, your mortgage term will be 25, 30 or even 35 years. But what’s best?

Well, if you’re a younger first-time buyer who’s on a budget, the chances are a longer mortgage term will be appealing. By spreading your repayments out over 35 years or even longer, you’ll be able to keep your monthly repayments fairly low. Plus, if you’re a first-time buyer who’s still a way off from retirement, your lender will probably be happy to give you one of these longer mortgage terms.

However, this does come with its downsides. Yes, you’ll be paying less each month, but you’ll actually end up paying more overall as the longer your mortgage term, the longer you’ll have to pay interest for. Ultimately, it’s all going to be down to how easily you can afford the monthly repayments and whether it’s more important to you to save money now or in the long run.

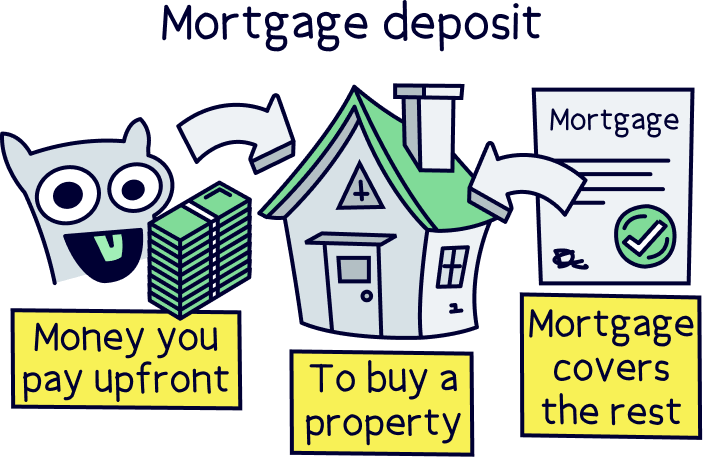

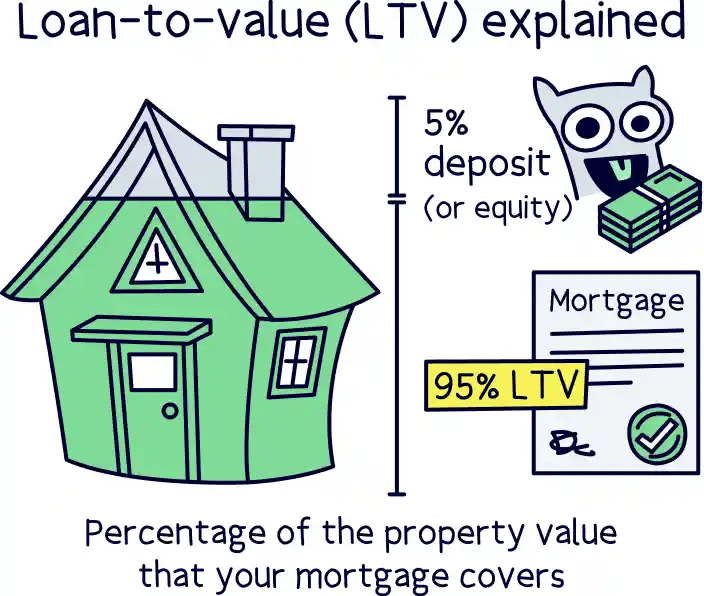

Your loan-to-value (LTV) ratio is about how much of your property’s value is going to be covered by your mortgage versus how much is going to be covered by your deposit.

Let’s look at an example.

Say you’re buying a property that’s worth £200,000 and you’ve managed to save up a £20,000 deposit. This would mean you’d need to borrow £180,000 from your mortgage lender, which would give you an LTV of 90% (90% of 200,000 = 180,000).

On the other hand, if you saved up a bigger deposit, your LTV would be lower. Imagine you saved up a £50,000 deposit and you still wanted to buy that same £200,000 property. In this case, you’d only need to borrow £150,000 from your mortgage lender, making your LTV 75% (75% of 200,000 = 150,000).

The biggest LTV you can normally get is 95%, meaning you need to put forward a deposit of at least 5% of your property’s value. But in an ideal world, you want to make your LTV as low as possible.

That’s because the lower your LTV, the better the deals you can usually access. Plus, if a lender isn’t sure whether they’re willing to give you a mortgage or not, putting forward a bigger deposit can help to seal the deal (it’s a long story, but lenders basically like it when people share the risk with them by forking out a bigger deposit).

However, if you’re a first-time buyer, it can be tricky to save up a big deposit. You might be in a rush to buy and reluctant to spend another year or two renting while you continue saving. And of course, you won’t have the luxury of selling a house to boost your savings and afford a bigger deposit! For that reason, a lot of first-time buyers tend to look for mortgages with higher LTVs, around 90% or even the maximum 95% we told you about earlier.

Okay, okay, so we know what you’re wondering: who has the best mortgage rates for first-time buyers? And what are they?

Well, like we keep saying, the best mortgage lender for you won’t be the best mortgage lender for someone else. The deals you can access will be pretty different depending on how big your deposit is, what your credit score is, what type of mortgage you’re after and how long you want your mortgage term to be.

BUT if we assume that you’re a ‘typical’ first-time buyer who’s young(ish), doesn’t have a huge deposit, isn’t earning buckets and hasn’t got the most amazing credit score, we can give you a rough idea.

Let’s say that you’re buying a £200,000 property and you’re paying a deposit of £20,000 (giving you a pretty high LTV of 90%). Let’s also imagine that you want a fixed-rate mortgage and that you’ve chosen a 30-year mortgage term.

In this case, some of the mortgage lenders with the best rates are HSBC, Barclays and Nationwide. Leeds Building Society, Yorkshire Building Society and Halifax all do pretty good deals too, and they’re all willing to accept applications from first-time buyers.

Just remember that these might not be the best lenders or deals for you, depending on what your situation is. To find the best deal, we’d always recommend working with a mortgage broker who can compare all your options and recommend the right mortgage for you.

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service and will find you the best deal. Plus, get 50% off with Nuts About Money.

If you’re ready and raring to find the best mortgage for you as a first-time buyer, the first step is to find a mortgage advisor. They’ll take the time to learn all about you before helping you search for the best mortgage and lender given your personal circumstances.

With a bit of help, you’ll be jangling the keys to your very own home (and benefiting from the best deals available to you!) before you know it. Congrats in advance!

Remember, Tembo¹ are perfect for those trying to get on the property ladder. They have award-winning service, will find the best mortgage for you, and have unique options to increase your borrowing (plus get 50% off their fee with Nuts About Money).

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.